Thailand EV Manufacturing Supply Chain Market, By Battery Type (Lithium-Ion, Nickel-Metal Hydride, Solid-State); By Vehicle Type (Battery Electric Vehicles, Plug-in Hybrid Electric Vehicles, Hybrid Electric Vehicles); By Component (Battery Cells & Packs, Electric Motors, Power Electronics, Charging Systems & Infrastructure, Thermal Management Systems); By Supply Chain Stage (Raw Material Suppliers, Battery Manufacturers, EV OEMs, Tier-1 & Tier-2 Component Suppliers, Aftermarket & Recycling); By End-User Industry (Passenger Cars, Commercial Vehicles, Two-Wheelers, Buses & Public Transport); By Trend Analysis, Competitive Landscape & Forecast, 2026-2032

- Manufacturing

- Feb 2026

- Pages 150

- Report Format: pdf

- Report Price: $2500 USD

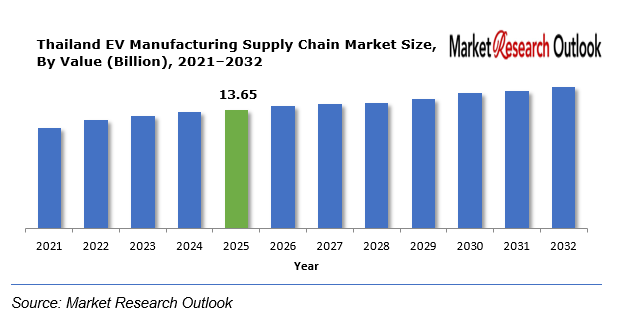

Thailand EV Manufacturing Supply Chain Market, Size & Forecast 2021-2032

The Thailand EV Manufacturing Supply Chain Market size was estimated at USD 13.65 Billion in 2025. During the forecast period, the Thailand EV Manufacturing Supply Chain Market size is projected to grow at a CAGR of 20.5% reaching a value of USD 50.42 Billion by 2032. The growth of the Thailand EV Manufacturing Supply Chain Market is primarily fueled by proactive government initiatives aimed at accelerating the adoption of electric vehicles across the country. Policies such as tax incentives for EV manufacturers, subsidies for EV purchases, and support for the development of charging infrastructure are encouraging both local and international companies to invest heavily in Thailand’s EV ecosystem. In parallel, significant foreign direct investment is flowing into battery production facilities, enabling the localization of critical components such as lithium-ion cells, electric motors, and power electronics. This investment not only strengthens the domestic supply chain but also positions Thailand as a regional hub for EV manufacturing in Southeast Asia. Moreover, rising consumer demand for passenger EVs, coupled with increasing electrification of commercial vehicles and public transportation, is prompting companies to expand local battery manufacturing and vehicle assembly operations.

EV Manufacturing Supply Chain – Overview

The Thailand EV Manufacturing Supply Chain covers the full range of activities required to produce EVs and their components, including raw material sourcing, battery production, electric motor and power electronics manufacturing, vehicle assembly, and aftermarket support. The supply chain ensures that EV production meets quality, safety, and performance standards while addressing sustainability goals through battery recycling and energy-efficient manufacturing.

Thailand EV Manufacturing Supply Chain Market

Growth Drivers

Government Incentives & EV Policies

The Thailand EV Manufacturing Supply Chain Market is strongly supported by proactive government measures aimed at accelerating the adoption of electric vehicles. Thailand has introduced a series of policies, including tax exemptions for EV manufacturers, subsidies for consumers purchasing electric vehicles, and incentives for battery producers and raw material suppliers. These policies are designed not only to attract foreign investment but also to strengthen domestic capabilities by encouraging localization of EV production and battery assembly. By reducing entry barriers and financial risks, these initiatives incentivize companies to establish manufacturing plants, enhance R&D activities, and develop robust supply chains within the country. Over the forecast period from 2026 to 2032, such policy-driven support is expected to play a critical role in sustaining market growth, making Thailand a key hub for EV manufacturing in Southeast Asia.

Challenges

High Capital Investment & Technology Costs

Despite the favorable policy environment, the EV manufacturing and battery production sector in Thailand faces significant challenges, particularly related to the high capital investment required. Setting up modern EV manufacturing facilities and lithium-ion battery plants demands enormous financial outlay, advanced technology, and skilled labor. The sourcing of rare and expensive materials such as lithium, cobalt, and nickel further adds to production costs. Additionally, the development of charging infrastructure and the integration of smart grid technologies involve considerable expenditure. For many market participants, especially small and medium enterprises, these high upfront costs can act as a barrier to entry or limit the pace of expansion. This challenge is compounded by the rapid technological evolution in EV batteries, which necessitates continuous investment in research and upgrades to remain competitive.

Geopolitical Impact on Thailand EV Manufacturing Supply Chain Market

The Thailand EV Manufacturing Supply Chain is intricately linked to global supply chain dynamics and geopolitical factors. The availability, pricing, and reliability of critical raw materials such as lithium, nickel, and cobalt are heavily influenced by the political and economic stability of countries that dominate their production, including Australia, Chile, the Democratic Republic of Congo, and Indonesia. Trade policies, tariffs, export restrictions, or sanctions imposed by these countries can lead to supply disruptions or sudden price volatility. Moreover, geopolitical tensions in key mining regions or along major shipping routes could impact the timely delivery of essential components such as battery cells, electric motors, and semiconductors. Between 2026 and 2032, such geopolitical influences may result in fluctuating raw material costs and intermittent component shortages, potentially affecting production schedules, cost structures, and overall supply chain efficiency. Companies operating in Thailand will need to strategically diversify sourcing, establish local partnerships, and optimize inventory management to mitigate these risks and maintain growth momentum in the EV sector

Thailand EV Manufacturing Supply Chain Market

Segmental Coverage

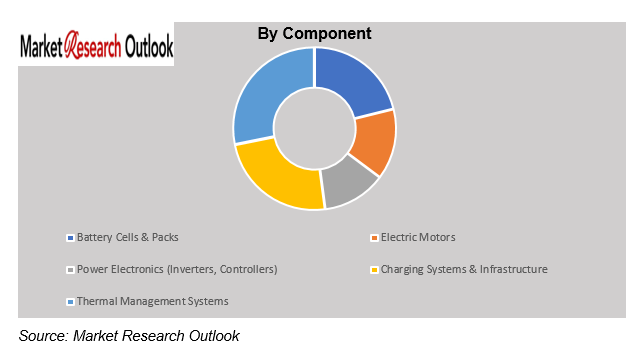

Thailand EV Manufacturing Supply Chain Market – By Component

Based on component, the Thailand EV Manufacturing Supply Chain Market is segmented into Battery Cells & Packs, Electric Motors, Power Electronics, Charging Systems & Infrastructure, Thermal Management Systems. The Battery Cells & Packs segment is expected to witness significant growth in the Thailand EV manufacturing supply chain market during the forecast period. This growth is driven by rising domestic and regional demand for electric vehicles, coupled with Thailand’s strategic initiatives to become a regional hub for EV production. Expansion of local battery production facilities, government incentives for EV adoption, and investments from global battery manufacturers such as LG Energy Solution, CATL, and Panasonic are further fueling the segment’s development. As automakers increasingly focus on in-house battery assembly and modular battery pack solutions, the Battery Cells & Packs segment is poised to capture a substantial share of the market.

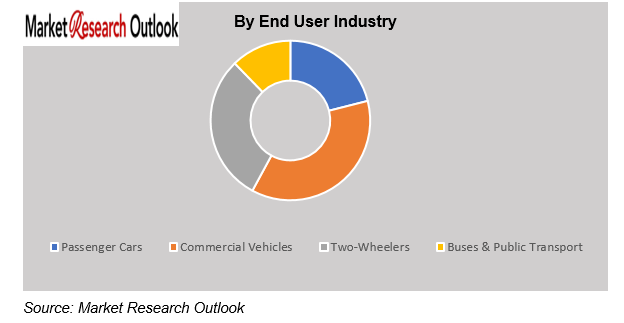

Thailand EV Manufacturing Supply Chain Market – By End User Industry

Based on end user industry, the Thailand EV Manufacturing Supply Chain Market is segmented into Passenger Cars, Commercial Vehicles, Two-Wheelers, Buses & Public Transport. The Passenger Cars segment is expected to experience strong growth during the forecast period in the Thailand EV manufacturing supply chain market. This growth is supported by increasing consumer adoption of electric passenger vehicles, government subsidies and incentives for EV buyers, and expanding EV model offerings from both domestic and international automakers. The rising awareness of environmental sustainability and the push for lower emissions are also driving demand in this segment, positioning Passenger Cars as one of the key growth areas in Thailand’s EV market.

Competitive Landscape

Key participants in the Thailand EV Manufacturing Supply Chain market include PTT Group, Delta Electronics (Thailand) PCL, Bangkok Electric Vehicle Co., Ltd., Toyota Motor Thailand Co., Ltd., Honda Automobile (Thailand) Co., Ltd., Nissan Motor (Thailand) Co., Ltd., Mitsubishi Motors (Thailand) Co., Ltd., LG Energy Solution (Thailand), CATL, BASF (Thailand) Ltd., and other prominent players and Other Prominent Players.

These companies are implementing strategic growth initiatives in order to gain a competitive advantage. The strategies being largely adopted include mergers and acquisitions, strategic alliances, joint ventures, licensing agreements, and new product launches. With the implementation of these strategies, the market participants aim to increase product portfolios, as well as enhance regional presence for long-term sustainable business growth in the EV Manufacturing Supply Chain industry of Thailand.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | Thailand |

| Product/ Service Segmentation | Battery Type, Vehicle Type, Component, Supply Chain Stage, End User Industry |

| Key Players | PTT Group, Delta Electronics (Thailand) PCL, Bangkok Electric Vehicle Co., Ltd., Toyota Motor Thailand Co., Ltd., Honda Automobile (Thailand) Co., Ltd., Nissan Motor (Thailand) Co., Ltd., Mitsubishi Motors (Thailand) Co., Ltd., LG Energy Solution (Thailand), CATL, BASF (Thailand) Ltd., and other prominent players and Other Prominent Players. |

Market Segmentation

- By Battery Type

- Lithium-Ion (Li-ion) Batteries

- Nickel-Metal Hydride (NiMH) Batteries

- Solid-State Batteries

- By Vehicle Type

- Battery Electric Vehicles (BEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Hybrid Electric Vehicles (HEVs)

- By Component

- Battery Cells & Packs

- Electric Motors

- Power Electronics (Inverters, Controllers)

- Charging Systems & Infrastructure

- Thermal Management Systems

- By Supply Chain Stage

- Raw Material Suppliers

- Battery Manufacturers

- EV OEMs

- Tier-1 & Tier-2 Component Suppliers

- Aftermarket & Recycling

- By End User Industry

- Passenger Cars

- Commercial Vehicles

- Two-Wheelers

- Buses & Public Transport

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- Thailand EV Manufacturing Supply Chain Market Insights

- Growth Drivers

- Restraints

- Opportunities

- Challenges

- Technological Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Industry Value Chain & Entry Points

- Thailand EV Manufacturing Supply Chain Market: Regulatory Framework

- Thailand EV Manufacturing Supply Chain Market: Marketing Strategies

- Thailand EV Manufacturing Supply Chain Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Battery Type

- Lithium-Ion (Li-ion) Batteries

- Nickel-Metal Hydride (NiMH) Batteries

- Solid-State Batteries

- By Vehicle Type

- Battery Electric Vehicles (BEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Hybrid Electric Vehicles (HEVs)

- By Component

- Battery Cells & Packs

- Electric Motors

- Power Electronics (Inverters, Controllers)

- Charging Systems & Infrastructure

- Thermal Management Systems

- By Supply Chain Stage

- Raw Material Suppliers

- Battery Manufacturers

- EV OEMs

- Tier-1 & Tier-2 Component Suppliers

- Aftermarket & Recycling

- By End User Industry

- Passenger Cars

- Commercial Vehicles

- Two-Wheelers

- Buses & Public Transport

- By Battery Type

- Market Size & Forecast, 2021-2032

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution By End-Use Industry

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List Of Key Players And Their Offerings

- Thailand EV Manufacturing Supply Chain Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- Geopolitical Impact On Thailand EV Manufacturing Supply Chain Market

- Company Profile

- PTT Group

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- Swot Analysis

- PTT Group

**(Same Data Pointers Will Be Provided For The Below Companies)

- Delta Electronics PCL

- Bangkok Electric Vehicle Co., Ltd.

- Toyota Motor Thailand Co., Ltd.

- Honda Automobile

- Nissan Motor

- Mitsubishi Motors

- LG Energy Solution

- CATL (Contemporary Amperex Technology Co. Ltd.)

- BASF

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown Of Primary Research Respondents, By Country

- Assumption & Limitation

- Qualitative Research

* Financial information in case of non-listed companies will be provided as per availability

**The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. What is the expected growth rate of the Thailand EV Manufacturing Supply Chain Market during the forecast period?

Ans: The Thailand EV Manufacturing Supply Chain Market size was estimated at USD 13.65 billion in 2025.

2. What is the expected growth rate of the Thailand EV Manufacturing Supply Chain Market during the forecast period?

Ans: Thailand EV Manufacturing Supply Chain Market is expected to grow at a CAGR of around 20.5% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Thailand EV Manufacturing Supply Chain Market by 2032?

Ans: The Thailand EV Manufacturing Supply Chain Market is projected to reach a value of approximately USD 50.42 billion by 2032.

4. What are the major factors driving the growth of the Thailand EV Manufacturing Supply Chain Market?

Ans: The growth of the Thailand EV Manufacturing Supply Chain Market is primarily fueled by proactive government initiatives aimed at accelerating the adoption of electric vehicles across the country.

5. Name the key players operating in the Thailand EV Manufacturing Supply Chain Market.

Ans: The key players of Thailand EV Manufacturing Supply Chain Market are PTT Group, Delta Electronics (Thailand) PCL, Bangkok Electric Vehicle Co., Ltd., Toyota Motor Thailand Co., Ltd., Honda Automobile (Thailand) Co., Ltd., Nissan Motor (Thailand) Co., Ltd., Mitsubishi Motors (Thailand) Co., Ltd., LG Energy Solution (Thailand), CATL, BASF (Thailand) Ltd., and other prominent players and Other Prominent Players.

6. Which is the fastest-growing component segment in the Thailand EV Manufacturing Supply Chain Market?

Ans: The Battery Cells & Packs segment is expected to witness significant growth in the Thailand EV manufacturing supply chain market during the forecast period.

Frequently Asked Questions

1. What is the expected growth rate of the Thailand EV Manufacturing Supply Chain Market during the forecast period?

Ans: The Thailand EV Manufacturing Supply Chain Market size was estimated at USD 13.65 billion in 2025.

2. What is the expected growth rate of the Thailand EV Manufacturing Supply Chain Market during the forecast period?

Ans: Thailand EV Manufacturing Supply Chain Market is expected to grow at a CAGR of around 20.5% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Thailand EV Manufacturing Supply Chain Market by 2032?

Ans: The Thailand EV Manufacturing Supply Chain Market is projected to reach a value of approximately USD 50.42 billion by 2032.

4. What are the major factors driving the growth of the Thailand EV Manufacturing Supply Chain Market?

Ans: The growth of the Thailand EV Manufacturing Supply Chain Market is primarily fueled by proactive government initiatives aimed at accelerating the adoption of electric vehicles across the country.

5. Name the key players operating in the Thailand EV Manufacturing Supply Chain Market.

Ans: The key players of Thailand EV Manufacturing Supply Chain Market are PTT Group, Delta Electronics (Thailand) PCL, Bangkok Electric Vehicle Co., Ltd., Toyota Motor Thailand Co., Ltd., Honda Automobile (Thailand) Co., Ltd., Nissan Motor (Thailand) Co., Ltd., Mitsubishi Motors (Thailand) Co., Ltd., LG Energy Solution (Thailand), CATL, BASF (Thailand) Ltd., and other prominent players and Other Prominent Players.

6. Which is the fastest-growing component segment in the Thailand EV Manufacturing Supply Chain Market?

Ans: The Battery Cells & Packs segment is expected to witness significant growth in the Thailand EV manufacturing supply chain market during the forecast period.