North America CCUS Market, By Technology (Pre-Combustion Capture, Post-Combustion Capture, Oxy-Fuel Combustion, Direct Air Capture (DAC)); By Service (Capture, Transportation, Utilization, Storage); By Deployment Type (Onshore CCUS Projects, Offshore CCUS Projects ); By Application (Oil & Gas, Power Generation, Cement, Steel & Metallurgy, Chemicals & Petrochemicals, Fertilizers, Hydrogen Production, Waste-to-Energy & Biomass); By Country (United States, Canada); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Energy and Power

- Feb 2026

- Pages 250

- Report Format: pdf

- Report Price: $3000 USD

North America CCUS Market, Size & Forecast 2021-2032

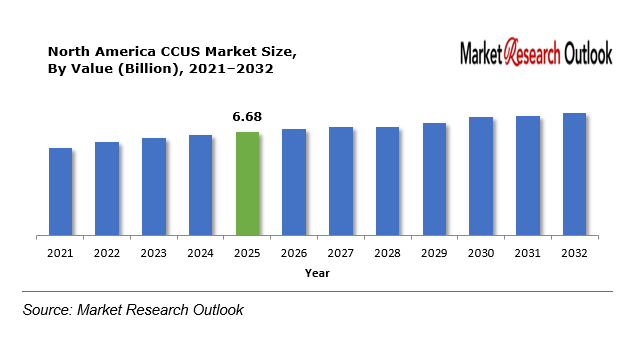

The North America CCUS Market size was estimated at USD 6.68 Billion in 2025. During the forecast period, the North America CCUS Market size is projected to grow at a CAGR of 15.4% reaching a value of USD 18.23 Billion by 2032. The North America CCUS market is expected to experience strong growth during the forecast period from 2026 to 2032 because of government support and tax benefits and increasing funding for carbon management solutions. The United States and Canada are leading the deployment of large-scale carbon capture projects across industries such as oil and gas and power generation and hydrogen production and chemicals. The combination of favorable regulatory frameworks and industrial emission reduction goals and net-zero target achievement efforts drive market expansion. The CCUS market in North America will experience growth because of carbon transport infrastructure development and increasing blue hydrogen adoption and strengthened partnerships between energy companies and technology providers.

CCUS – Overview

CCUS (Carbon Capture, Utilization, and Storage) refers to a set of technologies which capture carbon dioxide (CO₂) emissions from industrial processes power plants and other sources and either use the captured carbon for different purposes or permanently store it underground to stop its atmospheric emission. CCUS plays a crucial role in reducing greenhouse gas emissions because it enables industrial decarbonization while helping countries achieve their net-zero climate targets through its protective measures against environmental damage caused by fossil fuel and heavy industry operations.

North America CCUS Market

Growth Drivers

Growing Demand for Low-Carbon Hydrogen

The market experiences growth because industries need low-carbon hydrogen which has become their primary focus for decreasing carbon emissions and moving to renewable energy sources. CCUS technologies play a vital role in blue hydrogen production by capturing and storing carbon dioxide generated during hydrogen manufacturing. North America sees increased CCUS solution adoption because rising hydrogen infrastructure investments and government support and expanding hydrogen industrial applications.

Challenges

High Initial Capital Investment

The CCUS market faces its biggest obstacle because developing carbon capture facilities and transportation networks and long-term storage infrastructure requires high initial capital investment costs. The high costs associated with technology deployment, installation, and maintenance create obstacles for all industries, but especially for smaller companies. Long-term financial return uncertainties and regulatory framework uncertainties create investment decision-making challenges, which prevent North American CCUS projects from being implemented on a large scale.

Geopolitical Impact on North America CCUS Market

The North America CCUS market experiences major geopolitical effects that stem from energy security efforts and climate regulations and the United States-Canada border partnerships. The region’s governments are developing their domestic carbon management systems and clean energy programs to achieve international climate targets while decreasing their reliance on energy sources that produce high emissions. The establishment of tax incentives and funding programs through supportive policy frameworks has created an environment that promotes investment in CCUS infrastructure and low-carbon hydrogen production facilities. The combination of shifting political priorities and different regulatory systems between federal and state or provincial authorities and trade policy uncertainties presents challenges that will affect project schedules and investment decisions. The North American CCUS deployment process benefits from geopolitical concerns about energy transition and emission reduction efforts.

North America CCUS Market

Segmental Coverage

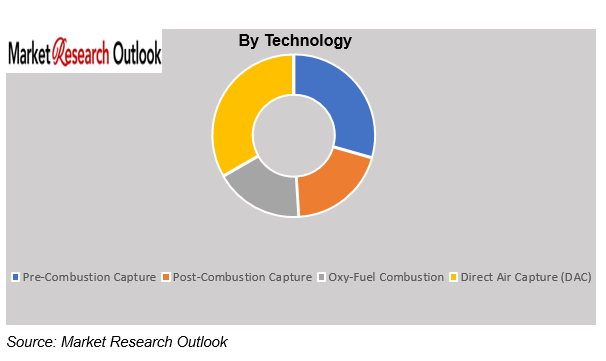

North America CCUS Market – By Technology

Based on Technology, the North America CCUS Market is segmented into Pre-Combustion Capture, Post-Combustion Capture, Oxy-Fuel Combustion, Direct Air Capture (DAC). The pre-combustion capture segment is expected to grow during the forecast period due to its increasing adoption in hydrogen production, power generation, and industrial processes that use fossil fuels as feedstock. The technology enables carbon dioxide removal before fuel combustion which makes it suitable for integrated gasification combined cycle power plants and blue hydrogen production facilities. The demand for low-carbon hydrogen combined with government policies that support clean energy and the growing investments in clean energy infrastructure across North America will drive the pre-combustion capture segment expansion during the upcoming years.

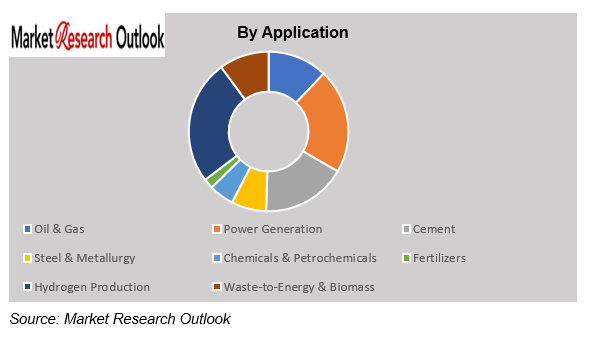

North America CCUS Market – By Application

Based on application, the North America CCUS Market is segmented into Oil & Gas, Power Generation, Cement, Steel & Metallurgy, Chemicals & Petrochemicals, Fertilizers, Hydrogen Production, Waste-to-Energy & Biomass. The oil and gas sector will experience growth during the upcoming forecast period because of rising implementation of CCUS technologies which help decrease carbon emissions from both upstream and downstream activities. North American oil and gas companies are funding carbon capture technologies to achieve their decarbonization goals for refining and processing and hydrogen production processes while they comply with environmental regulations and net-zero targets. The oil and gas sector in the North America CCUS market is expanding because of two factors which include using captured CO₂ for enhanced oil recovery (EOR) and establishing large-scale carbon storage hubs across regions like the North Sea.

Competitive Landscape

Key participants in the North America CCUS market include ExxonMobil Corporation, Chevron Corporation, Occidental Petroleum Corporation, SLB (Schlumberger), Honeywell International Inc., Fluor Corporation, Air Products and Chemicals, Inc., Linde plc, Aker Carbon Capture, Mitsubishi Heavy Industries and Other Prominent Players.

These companies are implementing strategic growth initiatives in order to gain a competitive advantage. The strategies being largely adopted include mergers and acquisitions, strategic alliances, joint ventures, licensing agreements, and new product launches. With the implementation of these strategies, the market participants aim to increase product portfolios, as well as enhance regional presence for long-term sustainable business growth in the CCUS industry of North America.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | North America |

| Product/ Service Segmentation | Technology, Service, Deployment Type, Application |

| Key Players | ExxonMobil Corporation, Chevron Corporation, Occidental Petroleum Corporation, SLB (Schlumberger), Honeywell International Inc., Fluor Corporation, Air Products and Chemicals, Inc., Linde plc, Aker Carbon Capture, Mitsubishi Heavy Industries, and Other Prominent Players. |

Market Segmentation

- By Technology

- Pre-Combustion Capture

- Post-Combustion Capture

- Oxy-Fuel Combustion

- Direct Air Capture (DAC)

- By Service

- Capture

- Transportation

- Utilization

- Storage

- By Deployment Type

- Onshore CCUS Projects

- Offshore CCUS Projects

- By Application

- Oil & Gas

- Power Generation

- Cement

- Steel & Metallurgy

- Chemicals & Petrochemicals

- Fertilizers

- Hydrogen Production

- Waste-to-Energy & Biomass

- By Country

- United States

- Canada

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- North America CCUS Market Insights

- Growth Drivers

- Restraints

- Opportunities

- Challenges

- Technology Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Industry Value Chain & Entry Points

- North America CCUS Market: Regulatory Framework

- North America CCUS Market: Marketing Strategies

- North America CCUS Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- Pre-Combustion Capture

- Post-Combustion Capture

- Oxy-Fuel Combustion

- Direct Air Capture (DAC)

- By Service

- Capture

- Transportation

- Utilization

- Storage

- By Deployment Type

- Onshore CCUS Projects

- Offshore CCUS Projects

- By Application

- Oil & Gas

- Power Generation

- Cement

- Steel & Metallurgy

- Chemicals & Petrochemicals

- Fertilizers

- Hydrogen Production

- Waste-to-Energy & Biomass

- By Country

- United States

- Canada

- By Technology

- Market Size & Forecast, 2021-2032

- United States CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- Market Size & Forecast, 2021-2032

- Canada CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution by End-Use Industry

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List of Key Players and Their Offerings

- North America CCUS Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, etc.)

- Geopolitical Impact on North America CCUS Market

- Company Profile

- ExxonMobil Corporation

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- SWOT Analysis

- ExxonMobil Corporation

- Market Size & Forecast, 2021-2032

**(same data pointers will be provided for the below companies)

- Chevron Corporation

- Occidental Petroleum Corporation

- SLB (Schlumberger)

- Honeywell International Inc.

- Fluor Corporation

- Air Products and Chemicals, Inc.

- Linde plc

- Aker Carbon Capture

- Mitsubishi Heavy Industries

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown of Primary Research Respondents, By Region

- Assumption & Limitation

- Qualitative Research

* Financial information in case of non-listed companies will be provided as per availability

**The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. What is the expected growth rate of the North America CCUS Market during the forecast period?

Ans: The North America CCUS Market size was estimated at USD 6.68 billion in 2025.

2. What is the expected growth rate of the North America CCUS Market during the forecast period?

Ans: North America CCUS Market is expected to grow at a CAGR of around 15.4% during the forecast period between 2026 and 2032.

3. What is the forecast value of the North America CCUS Market by 2032?

Ans: The North America CCUS Market is projected to reach a value of approximately USD 18.23 billion by 2032.

4. What are the major factors driving the growth of the North America CCUS Market?

Ans: The North America CCUS market is expected to experience strong growth during the forecast period from 2026 to 2032 because of government support and tax benefits and increasing funding for carbon management solutions.

5. Name the key players operating in the North America CCUS Market.

Ans: The key players of North America CCUS Market are ExxonMobil Corporation, Chevron Corporation, Occidental Petroleum Corporation, SLB (Schlumberger), Honeywell International Inc., Fluor Corporation, Air Products and Chemicals, Inc., Linde plc, Aker Carbon Capture, Mitsubishi Heavy Industries and Other Prominent Players.

6. Which is the fastest-growing application segment in the North America CCUS Market?

Ans: The oil and gas sector will experience growth during the upcoming forecast period because of rising implementation of CCUS technologies which help decrease carbon emissions from both upstream and downstream activities.

7. Which country contributes significantly to the growth of the North America CCUS Market?

Ans: The United States market will experience growth during the forecast period because of three main factors which include strong government support and favorable tax incentives and increasing investments in carbon capture utilization and storage projects.

Frequently Asked Questions

1. What is the expected growth rate of the North America CCUS Market during the forecast period?

Ans: The North America CCUS Market size was estimated at USD 6.68 billion in 2025.

2. What is the expected growth rate of the North America CCUS Market during the forecast period?

Ans: North America CCUS Market is expected to grow at a CAGR of around 15.4% during the forecast period between 2026 and 2032.

3. What is the forecast value of the North America CCUS Market by 2032?

Ans: The North America CCUS Market is projected to reach a value of approximately USD 18.23 billion by 2032.

4. What are the major factors driving the growth of the North America CCUS Market?

Ans: The North America CCUS market is expected to experience strong growth during the forecast period from 2026 to 2032 because of government support and tax benefits and increasing funding for carbon management solutions.

5. Name the key players operating in the North America CCUS Market.

Ans: The key players of North America CCUS Market are ExxonMobil Corporation, Chevron Corporation, Occidental Petroleum Corporation, SLB (Schlumberger), Honeywell International Inc., Fluor Corporation, Air Products and Chemicals, Inc., Linde plc, Aker Carbon Capture, Mitsubishi Heavy Industries and Other Prominent Players.

6. Which is the fastest-growing application segment in the North America CCUS Market?

Ans: The oil and gas sector will experience growth during the upcoming forecast period because of rising implementation of CCUS technologies which help decrease carbon emissions from both upstream and downstream activities.

7. Which country contributes significantly to the growth of the North America CCUS Market?

Ans: The United States market will experience growth during the forecast period because of three main factors which include strong government support and favorable tax incentives and increasing investments in carbon capture utilization and storage projects.