Japan Semiconductor Power & Water Dependency Analysis Market, By Power Dependency Level (Low Power Intensity Fabs, Moderate Power Intensity Fabs, High Power Intensity Fabs, Ultra-High Power Intensive Advanced Node Fabs); By Water Dependency Level (Low Water Consumption Facilities, Moderate Water Consumption Facilities, High Ultra-Pure Water (UPW) Dependent Fabs, Recycled Water Integrated Fabs); By Fabrication Facility Type (Integrated Device Manufacturer (IDM) Fabs, Foundry Fabs, OSAT (Outsourced Semiconductor Assembly & Testing) Facilities, R&D and Pilot Line Facilities); By Technology Node (Mature Nodes (28nm and Above), Advanced Nodes (7nm–28nm), Leading Edge Nodes (Below 7nm), Specialty Process Nodes (Power, Analog, MEMS, Sensors)); By Utility Infrastructure Type (Grid-Connected Power Supply, On-Site Gas Turbine / Cogeneration, Renewable Energy Integrated Facilities, Water Recycling & Reclamation Systems, Dedicated Industrial Water Supply Networks); By End-Use Semiconductor Application (Automotive Semiconductors, Consumer Electronics, Industrial & Robotics, Telecommunications & 5G, AI & High-Performance Computing, Power Electronics); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Chemicals & Advanced Materials

- Mar 2026

- Pages 120

- Report Format: pdf

- Report Price: $2500 USD

Japan Semiconductor Power & Water Dependency Analysis Market, Size & Forecast 2021-2032

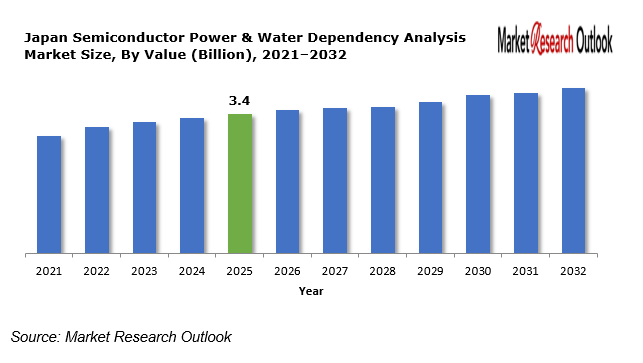

The Japan Semiconductor Power & Water Dependency Analysis Market size was estimated at USD 3.4 Billion in 2025. During the forecast period, the Japan Semiconductor Power & Water Dependency Analysis Market size is projected to grow at a CAGR of 11.8% reaching a value of USD 7.4 Billion by 2032. The establishment of new semiconductor factories in Kyushu and Hokkaido) along with the increased electricity needs of advanced node production and the major funding for water recycling systems and renewable energy projects) drive the current growth of the market. The transition to artificial intelligence and automotive semiconductor technology plus high-performance computing systems results in a major increase of both electrical consumption and ultra-pure water requirements.

Semiconductor Power & Water Dependency Analysis – Overview

The production of semiconductor power and water dependency depends on electrical power requirements and ultra-pure water needs which fabrication plants use to create their wafers. The advanced semiconductor production process needs nonstop electrical power to run its lithography and etching and deposition and cleanroom activities. The production process suffers financial losses which amount to millions of dollars whenever the electrical grid experiences even brief interruptions. Water plays a crucial role in both wafer cleaning and chemical processing at leading-edge fabs which need to use millions of gallons every day. Japan’s industrial strategy now prioritizes three key areas which include enhancing grid reliability and increasing renewable energy use and building water recycling systems to decrease environmental and operational hazards from semiconductor manufacturing.

Japan Semiconductor Power & Water Dependency Analysis Market

Growth Drivers

Government Subsidies & Strategic Semiconductor Revival

The Japanese government has introduced substantial funding programs to revitalize domestic semiconductor manufacturing capacity. The support for Rapidus and TSMC’s Kumamoto facility and memory expansion projects leads to faster progress in building semiconductor factories and their necessary utility systems. The developed systems of the project need strong grid connections and renewable energy sources and advanced water treatment facilities to achieve both sustainable operation and productive efficiency.

Challenges

Grid Reliability & Energy Transition Risks

Japan needs to overcome power supply problems which arise from its commitment to renewable energy sources. The semiconductor fabs need consistent voltage and frequency control which will require them to spend money on both on-site cogeneration systems and backup power solutions. Fab operators face financial challenges because of increasing electricity prices and decarbonization requirements.

Geopolitical Impact on Japan Semiconductor Power & Water Dependency Analysis Market

Geopolitical tensions between countries directly impact semiconductor supply chains and technology transfer policies which create economic effects on markets. Japan has increased its domestic chip production capabilities because of strategic competition between countries who develop advanced semiconductor technology. The organization establishes technological abilities through its international partnerships which include TSMC but this creates higher risks of operating interruptions. The period from 2026 to 2032 will see infrastructure investment decisions shaped by energy security needs and regional trade relationships.

Japan Semiconductor Power & Water Dependency Analysis Market

Segmental Coverage

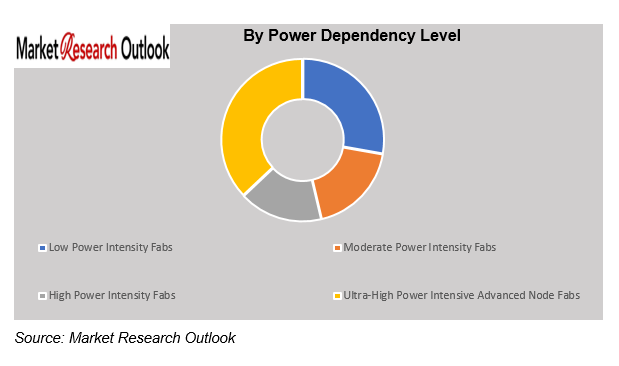

Japan Semiconductor Power & Water Dependency Analysis Market – By Power Dependency Level

Based on power dependency level, the market is segmented into Low Power Intensity Fabs, Moderate Power Intensity Fabs, High Power Intensity Fabs, and Ultra-High Power Intensive Advanced Node Fabs. The period of forecast shows that ultra-high power intensive fabs will achieve their highest growth rate because of the ongoing development of advanced semiconductor manufacturing facilities which produce leading-edge technology and facilities which produce artificial intelligence technology. The advanced nodes which operate below 7nm require sophisticated lithography systems together with EUV equipment and high-precision cleanroom environments and continuous process control systems which all consume more electricity than mature-node fabs. The rising demand for next-generation logic production in Japan has resulted in a substantial increase of overall power density across all semiconductor manufacturing facilities. The electricity requirements for AI-focused chip production increase because AI accelerators together with high-performance processors need manufacturers to implement more intricate wafer manufacturing processes which demand stricter quality standards and extended production time.

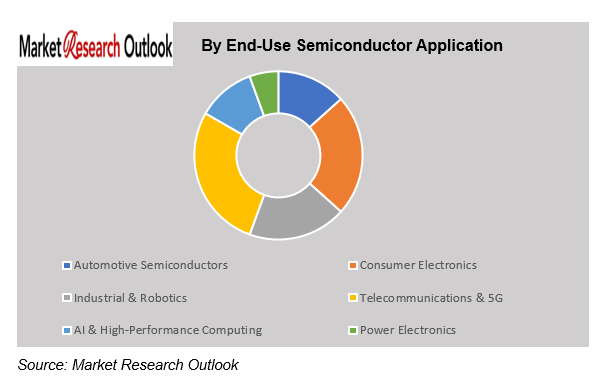

Japan Semiconductor Power & Water Dependency Analysis Market – By End-Use Semiconductor Application

Based on end-use semiconductor application, the market is segmented into Automotive Semiconductors, Consumer Electronics, Industrial & Robotics, Telecommunications & 5G, AI & High-Performance Computing, and Power Electronics. The Japanese automotive industry serves as the primary growth engine for Automotive Semiconductors through its production of vehicles and its development of advanced driver-assistance systems and electric vehicles and hybrid technologies. Japan hosts major automotive original equipment manufacturers and Tier-1 suppliers which depend on advanced microcontrollers and power semiconductors and sensors and analog chips. The move of vehicles toward electrification and autonomous operation leads to increased semiconductor usage in every vehicle. The automotive industry requires continuous and steady demand for automotive-grade chips to support power electronics used in EV drivetrains and battery management systems and in-vehicle networking and safety-critical systems. The automotive manufacturing sector establishes strict quality and reliability standards which create continuous demand for domestic semiconductor production.

Competitive Landscape

Key participants in the Japan Semiconductor Power & Water Dependency Analysis market include Taiwan Semiconductor Manufacturing Company, Rapidus Corporation, Sony Semiconductor Solutions, Kioxia Corporation, Renesas Electronics Corporation, Rohm Semiconductor, Micron Technology Japan, SUMCO Corporation, Tokyo Electron (TEL), and SCREEN Semiconductor Solutions, and Other Prominent Players. These companies are implementing strategic growth initiatives in order to gain a competitive advantage. The strategies being largely adopted include mergers and acquisitions, strategic alliances, joint ventures, licensing agreements, and new product launches. With the implementation of these strategies, the market participants aim to increase product portfolios, as well as enhance regional presence for long-term sustainable business growth in the Semiconductor Power & Water Dependency Analysis industry of Japan.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | Japan |

| Product/ Service Segmentation | Power Dependency Level, Water Dependency Level, Fabrication Facility Type, Technology Node, Utility Infrastructure Type, End-Use Semiconductor Application |

| Key Players | Taiwan Semiconductor Manufacturing Company, Rapidus Corporation, Sony Semiconductor Solutions, Kioxia Corporation, Renesas Electronics Corporation, Rohm Semiconductor, Micron Technology Japan, SUMCO Corporation, Tokyo Electron (TEL), and SCREEN Semiconductor Solutions, and Other Prominent Players. |

Market Segmentation

- By Power Dependency Level

- Low Power Intensity Fabs

- Moderate Power Intensity Fabs

- High Power Intensity Fabs

- Ultra-High Power Intensive Advanced Node Fabs

- By Water Dependency Level

- Low Water Consumption Facilities

- Moderate Water Consumption Facilities

- High Ultra-Pure Water (UPW) Dependent Fabs

- Recycled Water Integrated Fabs

- By Fabrication Facility Type

- Integrated Device Manufacturer (IDM) Fabs

- Foundry Fabs

- OSAT (Outsourced Semiconductor Assembly & Testing) Facilities

- R&D and Pilot Line Facilities

- By Technology Node

- Mature Nodes (28nm and Above)

- Advanced Nodes (7nm–28nm)

- Leading Edge Nodes (Below 7nm)

- Specialty Process Nodes (Power, Analog, MEMS, Sensors)

- By Utility Infrastructure Type

- Grid-Connected Power Supply

- On-Site Gas Turbine / Cogeneration

- Renewable Energy Integrated Facilities

- Water Recycling & Reclamation Systems

- Dedicated Industrial Water Supply Networks

- By End-Use Semiconductor Application

- Automotive Semiconductors

- Consumer Electronics

- Industrial & Robotics

- Telecommunications & 5G

- AI & High-Performance Computing

- Power Electronics

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- Japan Semiconductor Power & Water Dependency Analysis Market Insights

- Growth Drivers

- Restraints

- Opportunities

- Challenges

- Utility & Water Stress Exposure Analysis

- Technological Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Industry Value Chain & Entry Points

- Japan Semiconductor Power & Water Dependency Analysis Market: Regulatory Framework

- Japan Semiconductor Power & Water Dependency Analysis Market: Marketing Strategies

- Japan Semiconductor Power & Water Dependency Analysis Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Power Dependency Level

- Low Power Intensity Fabs

- Moderate Power Intensity Fabs

- High Power Intensity Fabs

- Ultra-High Power Intensive Advanced Node Fabs

- By Water Dependency Level

- Low Water Consumption Facilities

- Moderate Water Consumption Facilities

- High Ultra-Pure Water (UPW) Dependent Fabs

- Recycled Water Integrated Fabs

- By Fabrication Facility Type

- Integrated Device Manufacturer (IDM) Fabs

- Foundry Fabs

- OSAT (Outsourced Semiconductor Assembly & Testing) Facilities

- R&D and Pilot Line Facilities

- By Technology Node

- Mature Nodes (28nm and Above)

- Advanced Nodes (7nm–28nm)

- Leading Edge Nodes (Below 7nm)

- Specialty Process Nodes (Power, Analog, MEMS, Sensors)

- By Utility Infrastructure Type

- Grid-Connected Power Supply

- On-Site Gas Turbine / Cogeneration

- Renewable Energy Integrated Facilities

- Water Recycling & Reclamation Systems

- Dedicated Industrial Water Supply Networks

- By End-Use Semiconductor Application

- Automotive Semiconductors

- Consumer Electronics

- Industrial & Robotics

- Telecommunications & 5G

- AI & High-Performance Computing

- Power Electronics

- By Power Dependency Level

- Market Size & Forecast, 2021-2032

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution By End-Use Industry

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List Of Key Players And Their Offerings

- Japan Semiconductor Power & Water Dependency Analysis Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- Geopolitical Impact On Japan Semiconductor Power & Water Dependency Analysis Market

- Company Profile

- Taiwan Semiconductor Manufacturing Company

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- Swot Analysis

- Taiwan Semiconductor Manufacturing Company

**(Same Data Pointers Will Be Provided For The Below Companies)

- Rapidus Corporation

- Sony Semiconductor Solutions

- Kioxia Corporation

- Renesas Electronics Corporation

- Rohm Semiconductor

- Micron Technology Japan

- SUMCO Corporation

- Tokyo Electron (TEL)

- SCREEN Semiconductor Solutions

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown Of Primary Research Respondents, By Country

- Assumption & Limitation

- Qualitative Research

* Financial information in case of non-listed companies will be provided as per availability

**The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. What is the expected growth rate of the Japan Semiconductor Power & Water Dependency Analysis Market during the forecast period?

Ans: The Japan Semiconductor Power & Water Dependency Analysis Market size was estimated at USD 3.4 billion in 2025.

2. What is the expected growth rate of the Japan Semiconductor Power & Water Dependency Analysis Market during the forecast period?

Ans: Japan Semiconductor Power & Water Dependency Analysis Market is expected to grow at a CAGR of around 11.8% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Japan Semiconductor Power & Water Dependency Analysis Market by 2032?

Ans: The Japan Semiconductor Power & Water Dependency Analysis Market is projected to reach a value of approximately USD 7.4 billion by 2032.

4. What are the major factors driving the growth of the Japan Semiconductor Power & Water Dependency Analysis Market?

Ans: The establishment of new semiconductor factories in Kyushu and Hokkaido) along with the increased electricity needs of advanced node production and the major funding for water recycling systems and renewable energy projects) drive the current growth of the market.

5. Name the key players operating in the Japan Semiconductor Power & Water Dependency Analysis Market.

Ans: The key players of Japan Semiconductor Power & Water Dependency Analysis Market are Taiwan Semiconductor Manufacturing Company, Rapidus Corporation, Sony Semiconductor Solutions, Kioxia Corporation, Renesas Electronics Corporation, Rohm Semiconductor, Micron Technology Japan, SUMCO Corporation, Tokyo Electron (TEL), and SCREEN Semiconductor Solutions, and Other Prominent Players.

6. Which is the fastest-growing power dependency level segment in the Japan Semiconductor Power & Water Dependency Analysis Market?

Ans: The period of forecast shows that ultra-high power intensive fabs will achieve their highest growth rate because of the ongoing development of advanced semiconductor manufacturing facilities which produce leading-edge technology and facilities which produce artificial intelligence technology.

Frequently Asked Questions

1. What is the expected growth rate of the Japan Semiconductor Power & Water Dependency Analysis Market during the forecast period?

Ans: The Japan Semiconductor Power & Water Dependency Analysis Market size was estimated at USD 3.4 billion in 2025.

2. What is the expected growth rate of the Japan Semiconductor Power & Water Dependency Analysis Market during the forecast period?

Ans: Japan Semiconductor Power & Water Dependency Analysis Market is expected to grow at a CAGR of around 11.8% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Japan Semiconductor Power & Water Dependency Analysis Market by 2032?

Ans: The Japan Semiconductor Power & Water Dependency Analysis Market is projected to reach a value of approximately USD 7.4 billion by 2032.

4. What are the major factors driving the growth of the Japan Semiconductor Power & Water Dependency Analysis Market?

Ans: The establishment of new semiconductor factories in Kyushu and Hokkaido) along with the increased electricity needs of advanced node production and the major funding for water recycling systems and renewable energy projects) drive the current growth of the market.

5. Name the key players operating in the Japan Semiconductor Power & Water Dependency Analysis Market.

Ans: The key players of Japan Semiconductor Power & Water Dependency Analysis Market are Taiwan Semiconductor Manufacturing Company, Rapidus Corporation, Sony Semiconductor Solutions, Kioxia Corporation, Renesas Electronics Corporation, Rohm Semiconductor, Micron Technology Japan, SUMCO Corporation, Tokyo Electron (TEL), and SCREEN Semiconductor Solutions, and Other Prominent Players.

6. Which is the fastest-growing power dependency level segment in the Japan Semiconductor Power & Water Dependency Analysis Market?

Ans: The period of forecast shows that ultra-high power intensive fabs will achieve their highest growth rate because of the ongoing development of advanced semiconductor manufacturing facilities which produce leading-edge technology and facilities which produce artificial intelligence technology.