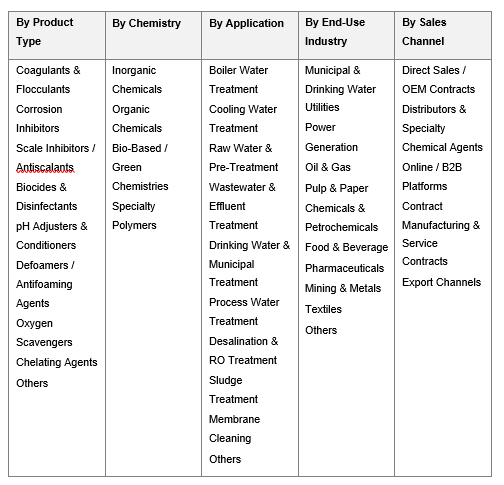

India Water Treatment Chemicals Market, By Product Type (Coagulants & Flocculants, Corrosion Inhibitors, Scale Inhibitors / Antiscalants, Biocides & Disinfectants, pH Adjusters & Conditioners, Defoamers / Antifoaming Agents, Oxygen Scavengers, Chelating Agents, Others); By Chemistry (Inorganic Chemicals, Organic Chemicals, Bio-Based / Green Chemistries, Specialty Polymers); By Functional Type (Aluminium-Based, Iron-Based, Polymer-Based, Chlorine-Based, Bromine-Based, Phosphonate-Based, Others); By Form (Liquid, Powder, Granular / Solid, Tablet / Briquettes); By Application (Boiler Water Treatment, Cooling Water Treatment, Raw Water & Pre-Treatment, Wastewater & Effluent Treatment, Drinking Water & Municipal Treatment, Process Water Treatment, Desalination & RO Treatment, Sludge Treatment, Membrane Cleaning, Others); By End-Use Industry (Municipal & Drinking Water Utilities, Power Generation, Oil & Gas, Pulp & Paper, Chemicals & Petrochemicals, Food & Beverage, Pharmaceuticals, Mining & Metals, Textiles, Others); By Sales Channel (Direct Sales / OEM Contracts, Distributors & Specialty Chemical Agents, Online / B2B Platforms, Contract Manufacturing & Service Contracts, Export Channels); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Chemicals & Advanced Materials

- Apr 2026

- Pages 150

- Report Format: pdf

- Report Price: $1800 USD

India Water Treatment Chemicals Market, Size & Forecast, 2021-2032

Report Description

| Study Duration | 2021-2032 |

| Market Size (2025) | USD 1.65 Billion |

| CAGR (2026-2032) | 8.5% |

| Leading Segment | Coagulants & Flocculants |

| Fastest Growing Segment | Bio-Based & ZLD-Driven Specialty Chemicals |

| Market Size (2032) | USD 2.92 Billion |

Source: Market Research Outlook

Market Overview: India Water Treatment Chemicals Market

The India water treatment chemicals market size is witnessing strong expansion, driven by rapid growth in municipal water and sewage infrastructure, rising industrial wastewater treatment demand, and increasing adoption of zero liquid discharge and water recycle and reuse systems. Valued at USD 1.65 billion in 2025 and projected to reach USD 2.92 billion by 2032 at a CAGR of 8.5%, the India water treatment chemicals market growth is supported by sustained demand from municipal utilities, power generation, oil and gas, pulp and paper, food and beverage, pharmaceuticals, mining, and textile industries.

The India water treatment chemicals market is shifting from traditional alum and chlorine-based dosing toward high-performance, bio-based, and specialty water treatment chemicals across municipal treatment, industrial cooling water, boiler systems, and advanced wastewater treatment applications. Coagulants and flocculants continue to dominate consumption, while bio-based and ZLD-driven specialty chemistries are emerging as the fastest-growing segments.

Demand dynamics are evolving, with utilities, EPC contractors, and industrial operators prioritising water quality outcomes, regulatory compliance, and long-term performance-based chemical programs over cost-driven procurement. This transition is strengthening the role of integrated chemical solutions across water treatment value chains.

Tightening CPCB norms, enforcement of ZLD and recycle and reuse mandates, and sustainability frameworks such as IGBC and LEED are reshaping the India water treatment chemicals market. At the same time, global players such as Kemira, BASF, Solenis, Ecolab, and Veolia are expanding India-focused manufacturing and service capabilities, while domestic companies including Thermax, Ion Exchange (India), VA Tech Wabag, SNF (India), and Dorf Ketal are scaling specialty chemical capacity.

As a result, the India water treatment chemicals market is evolving into a sustainability-led, performance-driven, and application-specific ecosystem, with increasing focus on water efficiency, regulatory compliance, and long-term value creation across domestic and export markets.

Key Report Takeaways: India Water Treatment Chemicals Market

- The India water treatment chemicals market size is projected to grow from USD 1.65 billion in 2025 to USD 2.92 billion by 2032, registering a CAGR of 8.5%, driven by municipal water infrastructure expansion, industrial wastewater treatment demand, and increasing adoption of zero liquid discharge and water recycle and reuse systems.

- Coagulants and flocculants dominate the India water treatment chemicals market, accounting for over 30% of total demand, supported by widespread use in municipal water treatment, sewage treatment plants, and large-scale industrial wastewater treatment applications.

- Bio-based and ZLD-driven specialty water treatment chemicals are the fastest-growing segment, expanding at 11% to 14% annually, as sustainability mandates, stricter CPCB norms, and ESG-driven procurement accelerate demand for high-performance water treatment solutions

- National programs such as Jal Jeevan Mission, AMRUT 2.0, Namami Gange, and Smart Cities Mission, along with rapid expansion of STP and ETP capacity, are structurally increasing demand across the India water treatment chemicals market.

- Global players including Kemira, BASF, Solenis, Ecolab, and Veolia are expanding India-focused manufacturing and service capabilities, strengthening innovation and supporting long-term growth in the India water treatment chemicals market forecast 2032.

Key Market Drivers: India Water Treatment Chemicals Market

Rapid Expansion of Municipal Water and Sewage Infrastructure

Growth in the India water treatment chemicals market is being strongly driven by rapid expansion of municipal water supply, sewage treatment, and wastewater management infrastructure. Large-scale national programs such as Jal Jeevan Mission, AMRUT 2.0, Namami Gange, and Smart Cities Mission are accelerating investments in water treatment plants, sewage treatment plants, and decentralised wastewater systems across urban and rural India.

Combined central and state investments in water and sanitation infrastructure exceed USD 60 billion between 2022 and 2027, leading to the commissioning of thousands of new STPs, WTPs, and reuse-focused treatment facilities. India’s installed sewage treatment capacity has already expanded by over 35% since 2020, while access to treated water continues to improve, creating sustained long-term demand visibility.

This structural infrastructure build-out is generating a strong and recurring demand cycle for coagulants, flocculants, biocides, pH adjusters, and chlorine-based disinfectants across municipal and decentralised applications. As a result, the India water treatment chemicals market is evolving into a volume-driven and performance-linked ecosystem, supported by continuous public sector investment and rising water quality standards.

Structural Shift Toward Zero Liquid Discharge (ZLD), Recycle and Reuse Mandates

The India water treatment chemicals market is witnessing a strong shift toward zero liquid discharge, recycle, and reuse-driven treatment programs, growing at 11% to 14% annually, significantly faster than conventional chemical dosing. Tightening CPCB norms across water-stressed industrial clusters such as textiles, pulp and paper, leather, pharmaceuticals, and chemicals, along with state-level ZLD mandates in Tamil Nadu, Gujarat, Maharashtra, and Punjab, are reshaping chemical demand patterns.

ZLD plants typically require 1.5x to 2.5x higher specialty chemical consumption compared to standard effluent treatment systems, with increased use of advanced antiscalants, high-performance flocculants, and corrosion inhibitors. Global players such as Kemira, BASF, and Solenis have expanded ZLD-focused product portfolios, while domestic manufacturers are scaling specialty and bio-based chemistries, reinforcing long-term structural demand in the India water treatment chemicals market.

Accelerated Power, Oil & Gas, and Process Industry Expansion Driving Boiler and Cooling Water Demand

Rapid expansion in power generation, oil and gas, refining, and process industries is a major growth driver for the India water treatment chemicals market. India’s installed power capacity is expected to cross 500 GW by 2030, alongside refinery expansions exceeding 30 MMTPA and steady output growth in steel, cement, and chemicals sectors.

Boiler and cooling water systems require continuous dosing of corrosion inhibitors, scale inhibitors, oxygen scavengers, biocides, and pH conditioners, creating a stable and recurring demand base. Leading operators such as NTPC, Indian Oil Corporation, Bharat Petroleum, Hindustan Petroleum, ONGC, Reliance Industries, Tata Steel, and JSW Steel have strengthened long-term chemical service contracts.

This consistent industrial demand, combined with capacity additions through 2032, is structurally expanding the India water treatment chemicals market across both high-volume and specialty chemical segments.

Key Market Challenges: India Water Treatment Chemicals Market

Raw Material Price Volatility Linked to Crude Oil and Global Supply Disruptions

The India water treatment chemicals market remains highly sensitive to fluctuations in key raw materials such as caustic soda, chlorine, soda ash, alumina, sulphuric acid, and polymer intermediates, which account for 55% to 70% of total production cost. Volatility in crude oil, naphtha, and ammonia pricing has led to 18% to 30% swings in input costs over the past two years, compressing margins and complicating long-term supply contracts across municipal and industrial segments.

Heavy Import Dependence for Specialty Polymers and Advanced Biocides

The India water treatment chemicals market continues to rely heavily on imports for high-performance polymers and advanced biocides, with over 50% to 60% of specialty polymer demand met through imports. This dependence exposes manufacturers and end users to supply chain disruptions, extended lead times, and geopolitical risks, particularly for ZLD-grade chemistries and membrane treatment solutions.

Environmental Compliance and Rising Regulatory Complexity

The India water treatment chemicals market is facing increasing regulatory pressure under CPCB norms, ZLD mandates, and environmental compliance requirements. Manufacturing operations for coagulants, biocides, and specialty chemicals are energy-intensive, with compliance costs rising by 7% to 10%. Export markets such as the EU and US further require adherence to REACH, NSF standards, and evolving ESG disclosures, adding complexity across the value chain.

Key Market Trends: India Water Treatment Chemicals Market

Rapid Adoption of Bio-Based and ZLD-Aligned Chemistries

The India water treatment chemicals market is witnessing a strong shift toward bio-based, low-toxicity, and ZLD-aligned chemistries, growing at 11% to 14% annually. Demand is being driven by stricter environmental norms, sustainability targets, and industrial water reuse requirements, with increasing adoption of plant-based coagulants, green polymers, and advanced treatment formulations.

Capacity Expansion by Global and Domestic Players

A new investment cycle is reshaping the India water treatment chemicals market, with over USD 1.2 billion in announced capacity expansions between 2023 and 2025. Global leaders such as Kemira, BASF, Solenis, Ecolab, and Veolia are strengthening India operations, while domestic players are expanding specialty chemical and service capabilities.

Rising Role of Desalination, Recycle and Reuse, and Industrial ZLD

Desalination, water recycle and reuse, and industrial ZLD are emerging as high-growth demand segments, expected to contribute over 30% of incremental chemical consumption by 2032. Increasing desalination capacity, industrial water reuse intensity, and performance-based chemical service models are reinforcing long-term growth across the India water treatment chemicals market.

Segmental Insights: India Water Treatment Chemicals Market

By Application: Boiler and Cooling Water Treatment Lead, Wastewater Grows Fastest

The boiler and cooling water treatment segment leads the India water treatment chemicals market, accounting for 30% to 33% of total consumption, driven by strong demand from power generation, refineries, petrochemicals, steel, cement, and large process industries. Key chemistries include corrosion inhibitors, scale inhibitors, biocides, and oxygen scavengers, ensuring continuous system efficiency and asset protection. Wastewater and effluent treatment contributes 25% to 28%, while drinking water and municipal treatment accounts for 20% to 22%, supported by Jal Jeevan Mission and AMRUT 2.0. Leading operators such as NTPC, Indian Oil Corporation, Bharat Petroleum, Tata Steel, and JSW Steel have strengthened long-term chemical service contracts, reinforcing steady demand.

By Product Type: Coagulants & Flocculants Lead While Bio-Based Specialty Chemistries Grow Fastest

Coagulants and flocculants dominate the India water treatment chemicals market, accounting for 30% to 33% share, driven by large-scale use in municipal water treatment, sewage treatment plants, and industrial wastewater treatment. Biocides and disinfectants contribute 18% to 20%, followed by corrosion inhibitors at 13% to 15%, scale inhibitors and antiscalants at 10% to 12%, and pH adjusters and oxygen scavengers at 8% to 10%. Bio-based, ZLD-grade, and specialty polymer chemistries are the fastest-growing segments, expanding at 11% to 14% annually, supported by stricter CPCB norms, sustainability targets, and industrial water reuse requirements.

Regional Insights: India Water Treatment Chemicals Market

West and South India together account for 55% to 60% of total demand, driven by strong industrial clusters across Gujarat, Maharashtra, Tamil Nadu, and Karnataka, along with refining, petrochemical, and textile industries. North India contributes 18% to 22%, supported by power generation, paper, and sugar industries, along with expanding municipal infrastructure. East and Central India account for 18% to 22%, driven by mining, metals, thermal power, and industrial growth. Capacity expansions by Kemira, BASF, Solenis, Thermax, and Ion Exchange (India) are strengthening regional supply chains and enabling closer collaboration with utilities and industrial users across the India water treatment chemicals market.

Recent Developments: India Water Treatment Chemicals Market

- The India water treatment chemicals market has witnessed strong momentum in capacity expansion and bio-based product innovation during 2024 and 2025. Kemira expanded coagulant and polymer capacity, BASF strengthened specialty water solutions, Solenis scaled formulation capabilities, and Ecolab commissioned new service hubs. Domestic players including Thermax, Ion Exchange (India), SNF (India), and Dorf Ketal expanded specialty antiscalants, biocides, and ZLD-grade polymer capacity, reinforcing India’s manufacturing strength.

- Downstream municipal utilities, power producers, and industrial operators are increasing domestic sourcing, with organisations such as NTPC, Indian Oil Corporation, Bharat Petroleum, Tata Steel, and JSW Steel scaling long-term service contracts. Rapid rollout of STPs and WTPs under Jal Jeevan Mission, AMRUT 2.0, and Namami Gange is driving sustained chemical demand, while EPC players like VA Tech Wabag, Thermax, Ion Exchange (India), and Veolia are expanding performance-based service models.

- Sustainability-led innovation is gaining strong traction in the India water treatment chemicals market. Global players including Kemira, BASF, Solenis, and Veolia are launching bio-based, low-toxicity, and ZLD-aligned chemical portfolios tailored for Indian applications. Increasing collaboration between chemical producers, EPC contractors, and industrial users is strengthening India’s position as an emerging hub for sustainable water treatment chemistries and supporting long-term market growth through 2032.

Key Market Players: India Water Treatment Chemicals Market

- Kemira India Pvt. Ltd.

- BASF India Limited

- Solenis India Pvt. Ltd.

- Ecolab India Pvt. Ltd. (Nalco Water)

- Thermax Limited

- Ion Exchange (India) Limited

- SNF (India) Pvt. Ltd.

- Dorf Ketal Chemicals India Pvt. Ltd.

- VA Tech Wabag Limited

- Buckman Laboratories (India) Pvt. Ltd.

- Veolia Water Technologies India Pvt. Ltd.

- Aquatech Systems (Asia) Pvt. Ltd.

Report Scope

In this report, the India Water Treatment Chemicals Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Coagulants & Flocculants

- Corrosion Inhibitors

- Scale Inhibitors / Antiscalants

- Biocides & Disinfectants

- pH Adjusters & Conditioners

- Defoamers / Antifoaming Agents

- Oxygen Scavengers

- Chelating Agents

- Others

- By Chemistry

- Inorganic Chemicals

- Organic Chemicals

- Bio-Based / Green Chemistries

- Specialty Polymers

- By Functional Type

- Aluminium-Based

- Iron-Based

- Polymer-Based

- Chlorine-Based

- Bromine-Based

- Phosphonate-Based

- Others

- By Form

- Liquid

- Powder

- Granular / Solid

- Tablet / Briquettes

- By Application

- Boiler Water Treatment

- Cooling Water Treatment

- Raw Water & Pre-Treatment

- Wastewater & Effluent Treatment

- Drinking Water & Municipal Treatment

- Process Water Treatment

- Desalination & RO Treatment

- Sludge Treatment

- Membrane Cleaning

- Others

- By End-Use Industry

- Municipal & Drinking Water Utilities

- Power Generation

- Oil & Gas

- Pulp & Paper

- Chemicals & Petrochemicals

- Food & Beverage

- Pharmaceuticals

- Mining & Metals

- Textiles

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Specialty Chemical Agents

- Online / B2B Platforms

- Contract Manufacturing & Service Contracts

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Water Treatment Chemicals Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic water treatment chemical producers, specialty bio-based chemistry specialists, global entrants, or niche segment leaders.

The India Water Treatment Chemicals Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Application

- By End-Use Industry

- By Functional Type

- By Sales Channel

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Water Treatment Chemicals Market

- India Water Treatment Chemicals Market Insights

- Market Dynamics

- Growth Drivers

- Rapid expansion of municipal water and sewage infrastructure under Jal Jeevan Mission, AMRUT 2.0, and Smart Cities Mission accelerating water treatment chemical demand.

- Structural shift toward Zero Liquid Discharge (ZLD), recycle and reuse mandates driven by CPCB norms and tightening industrial effluent standards.

- Accelerated power, oil & gas, and process industry expansion driving boiler, cooling, and process water treatment chemical consumption.

- Restraints

- Raw material price volatility linked to crude oil, caustic soda, chlorine, and global supply disruptions pressuring producer margins.

- Heavy import dependence for specialty polymers, advanced biocides, and high-purity treatment chemicals creating supply risk.

- Environmental compliance, effluent management, and tightening regulatory complexity raising operational and compliance costs.

- Opportunities

- Rapid scale-up of bio-based, green, and low-toxicity water treatment chemistries aligned with sustainability and ESG mandates.

- High-growth demand from desalination, water recycle/reuse, and ZLD applications supporting industrial water security build-out.

- Emerging export opportunity for specialty water treatment chemicals to Middle East, Africa, and Southeast Asia with growing water infrastructure investments.

- Challenges

- Intense price-led competition between global water treatment majors and domestic producers compressing margins.

- Shortage of skilled water chemists, treatment plant operators, and application engineers limiting deployment of advanced chemistries.

- Fragmented downstream industrial customer base with diverse specifications and water chemistry profiles increasing formulation and inventory complexity.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Growth Drivers

- Industry Value Chain & Entry Points

- Upstream Raw Materials (caustic soda, chlorine, alumina, soda ash, sulphuric acid)

- Active Ingredient Producers (alum, PAC, ferric chloride, polyacrylamides, phosphonates)

- Specialty & Bio-Based Chemical Producers (green coagulants, enzyme blends, sustainable biocides)

- Formulation, Blending & Reactor Operations (batch, continuous, custom blends)

- Quality Control, R&D & Application Laboratories (BIS, NSF, REACH, WHO standards)

- Distributors, Specialty Chemical Agents & B2B Marketplaces

- Downstream Treatment Plant Operators (municipal utilities, industrial ETPs, STPs, ZLDs)

- EPC Contractors & Water Engineering Firms (process design, plant build, O&M)

- Service Providers & Chemical Programs (dosing, monitoring, performance contracts)

- End-Use Industries (municipal, power, oil & gas, paper, food, pharma, mining, textiles)

- India Water Treatment Chemicals Market: Regulatory Framework

- India Water Treatment Chemicals Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (‘000 Tons)

- Market Share & Forecast

- By Product Type

- Coagulants & Flocculants

- Corrosion Inhibitors

- Scale Inhibitors / Antiscalants

- Biocides & Disinfectants

- pH Adjusters & Conditioners

- Defoamers / Antifoaming Agents

- Oxygen Scavengers

- Chelating Agents

- Others

- By Chemistry

- Inorganic Chemicals

- Organic Chemicals

- Bio-Based / Green Chemistries

- Specialty Polymers

- By Functional Type

- Aluminium-Based

- Iron-Based

- Polymer-Based

- Chlorine-Based

- Bromine-Based

- Phosphonate-Based

- Others

- By Form

- Liquid

- Powder

- Granular / Solid

- Tablet / Briquettes

- By Application

- Boiler Water Treatment

- Cooling Water Treatment

- Raw Water & Pre-Treatment

- Wastewater & Effluent Treatment

- Drinking Water & Municipal Treatment

- Process Water Treatment

- Desalination & RO Treatment

- Sludge Treatment

- Membrane Cleaning

- Others

- By End-Use Industry

- Municipal & Drinking Water Utilities

- Power Generation

- Oil & Gas

- Pulp & Paper

- Chemicals & Petrochemicals

- Food & Beverage

- Pharmaceuticals

- Mining & Metals

- Textiles

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Specialty Chemical Agents

- Online / B2B Platforms

- Contract Manufacturing & Service Contracts

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Water Treatment Chemicals Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Kemira India Pvt. Ltd.

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- Swot Analysis

- Kemira India Pvt. Ltd.

- Market Size & Forecast, 2021-2032

- Market Dynamics

(Same Data Pointers Will Be Provided for the Below Companies):

- BASF India Limited

- Solenis India Pvt. Ltd.

- Ecolab India Pvt. Ltd. (Nalco Water)

- Thermax Limited

- Ion Exchange (India) Limited

- SNF (India) Pvt. Ltd.

- Dorf Ketal Chemicals India Pvt. Ltd.

- VA Tech Wabag Limited

- Buckman Laboratories (India) Pvt. Ltd.

- Veolia Water Technologies India Pvt. Ltd.

- Aquatech Systems (Asia) Pvt. Ltd.

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability.

** The segmentation and the companies are subjected to modifications based on in-depth secondary research for the final deliverable.

Frequently Asked Questions

1. How large is the India water treatment chemicals market and what is its growth forecast?

Ans: The India water treatment chemicals market size is valued at USD 1.65 Billion in 2025 and is projected to reach USD 2.92 Billion by 2032, growing at a CAGR of around 8.5%. This strong India water treatment chemicals market growth is driven by accelerated municipal water and sewage infrastructure build-out, ZLD-led industrial demand, structural shift toward bio-based and specialty chemistries, and major domestic and global capacity expansions. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India water treatment chemicals market?

Ans: The India water treatment chemicals market segmentation shows that boiler and cooling water treatment dominate with approximately 30% to 33% share, followed by wastewater and effluent treatment at 25% to 28% and drinking water and municipal treatment at 20% to 22%. Coagulants and flocculants lead by product type with 30% to 33% share, while bio-based and ZLD-driven specialty chemicals are the fastest-growing segment, expanding at 11% to 14% annually. The report breaks down demand across product types, chemistries, functional types, forms, applications, end-use industries, and sales channels, helping businesses understand where growth is accelerating across the India water treatment chemicals market.

3. What are the key drivers of growth in the India water treatment chemicals market?

Ans: Key India water treatment chemicals market drivers include rapid expansion of municipal water and sewage infrastructure under Jal Jeevan Mission and AMRUT 2.0, structural shift toward Zero Liquid Discharge (ZLD), recycle and reuse mandates driven by CPCB norms, and accelerated power, oil & gas, and process industry expansion driving boiler and cooling water demand. Global water treatment majors such as Kemira, BASF, Solenis, Ecolab (Nalco Water), and Veolia are investing in India-specific manufacturing capacity, formulation labs, and service operations. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends shaping the India water treatment chemicals market.

4. Which regions are driving growth in the India water treatment chemicals market?

Ans: Regional analysis of the India water treatment chemicals market shows that West and South India together account for nearly 55% to 60% of total demand, driven by industrial clusters in Gujarat, Maharashtra, Tamil Nadu, and Karnataka, along with strong refining, petrochemical, and textile bases. North India contributes around 18% to 22%, supported by power generation, paper, sugar mills, and growing municipal infrastructure. East and Central India together account for 18% to 22%, supported by mining and metals, thermal power, and growing municipal water investments. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India water treatment chemicals market?

Ans: Key India water treatment chemicals market trends include rapid adoption of bio-based, low-toxicity, and ZLD-aligned chemistries, capacity expansion by global majors including Kemira, BASF, Solenis, Ecolab (Nalco Water), and Veolia, and rising importance of desalination, recycle/reuse, and ZLD applications. Performance-contracted chemical service models, advanced antiscalant programs for membrane systems, and sustainability-led procurement are reshaping competitive dynamics. The report provides comprehensive trend analysis, supported by company-level developments and forecast insights, helping businesses align strategy with the structural growth of the India water treatment chemicals market.

Frequently Asked Questions

1. How large is the India water treatment chemicals market and what is its growth forecast?

Ans: The India water treatment chemicals market size is valued at USD 1.65 Billion in 2025 and is projected to reach USD 2.92 Billion by 2032, growing at a CAGR of around 8.5%. This strong India water treatment chemicals market growth is driven by accelerated municipal water and sewage infrastructure build-out, ZLD-led industrial demand, structural shift toward bio-based and specialty chemistries, and major domestic and global capacity expansions. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India water treatment chemicals market?

Ans: The India water treatment chemicals market segmentation shows that boiler and cooling water treatment dominate with approximately 30% to 33% share, followed by wastewater and effluent treatment at 25% to 28% and drinking water and municipal treatment at 20% to 22%. Coagulants and flocculants lead by product type with 30% to 33% share, while bio-based and ZLD-driven specialty chemicals are the fastest-growing segment, expanding at 11% to 14% annually. The report breaks down demand across product types, chemistries, functional types, forms, applications, end-use industries, and sales channels, helping businesses understand where growth is accelerating across the India water treatment chemicals market.

3. What are the key drivers of growth in the India water treatment chemicals market?

Ans: Key India water treatment chemicals market drivers include rapid expansion of municipal water and sewage infrastructure under Jal Jeevan Mission and AMRUT 2.0, structural shift toward Zero Liquid Discharge (ZLD), recycle and reuse mandates driven by CPCB norms, and accelerated power, oil & gas, and process industry expansion driving boiler and cooling water demand. Global water treatment majors such as Kemira, BASF, Solenis, Ecolab (Nalco Water), and Veolia are investing in India-specific manufacturing capacity, formulation labs, and service operations. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends shaping the India water treatment chemicals market.

4. Which regions are driving growth in the India water treatment chemicals market?

Ans: Regional analysis of the India water treatment chemicals market shows that West and South India together account for nearly 55% to 60% of total demand, driven by industrial clusters in Gujarat, Maharashtra, Tamil Nadu, and Karnataka, along with strong refining, petrochemical, and textile bases. North India contributes around 18% to 22%, supported by power generation, paper, sugar mills, and growing municipal infrastructure. East and Central India together account for 18% to 22%, supported by mining and metals, thermal power, and growing municipal water investments. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India water treatment chemicals market?

Ans: Key India water treatment chemicals market trends include rapid adoption of bio-based, low-toxicity, and ZLD-aligned chemistries, capacity expansion by global majors including Kemira, BASF, Solenis, Ecolab (Nalco Water), and Veolia, and rising importance of desalination, recycle/reuse, and ZLD applications. Performance-contracted chemical service models, advanced antiscalant programs for membrane systems, and sustainability-led procurement are reshaping competitive dynamics. The report provides comprehensive trend analysis, supported by company-level developments and forecast insights, helping businesses align strategy with the structural growth of the India water treatment chemicals market.