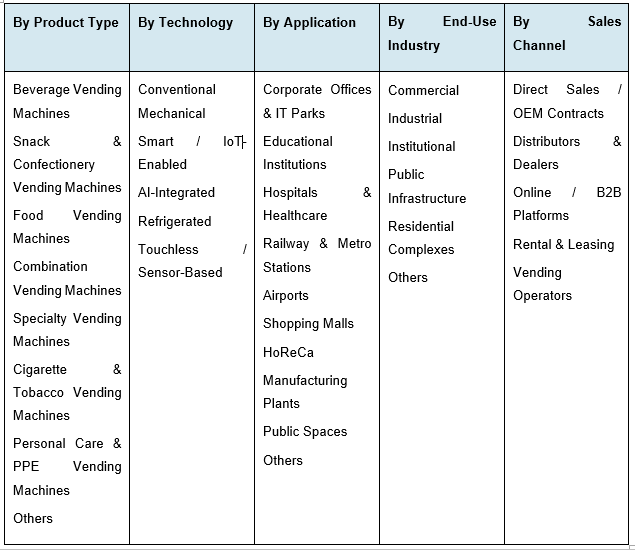

India Vending Machine Market, By Product Type (Beverage Vending Machines, Snack & Confectionery Vending Machines, Food Vending Machines, Combination Vending Machines, Specialty Vending Machines, Cigarette & Tobacco Vending Machines, Personal Care & PPE Vending Machines, Others); By Technology (Conventional Mechanical, Smart / IoT-Enabled, AI-Integrated, Refrigerated, Touchless / Sensor-Based Vending Machines); By Payment Mode (Cash-Based, Card-Based, UPI / QR Code-Based, Mobile Wallet & NFC, Multi-Payment Enabled); By Application (Corporate Offices & IT Parks, Educational Institutions, Hospitals & Healthcare, Railway & Metro Stations, Airports, Shopping Malls, HoReCa, Manufacturing Plants, Public Spaces, Others); By End-Use Industry (Commercial, Industrial, Institutional, Public Infrastructure, Residential Complexes, Others); By Sales Channel (Direct Sales / OEM Contracts, Distributors & Dealers, Online / B2B Platforms, Rental & Leasing, Vending Operators); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 150

- Report Format: pdf

- Report Price: $1800 USD

India Vending Machine Market: Smart Vending and Cashless Payment Adoption Powers Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

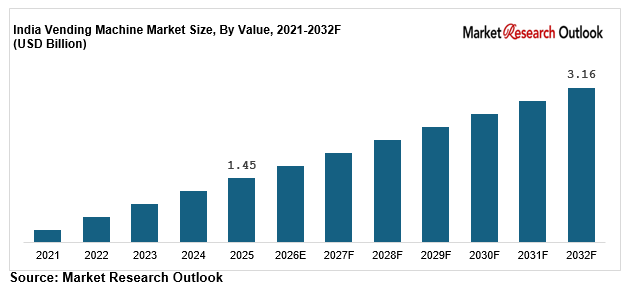

| Market Size (2025) | USD 1.45 Billion |

| CAGR (2026-2032) | 11.8% |

| Leading Segment | Beverage Vending Machines |

| Fastest Growing Segment | Smart / IoT-Enabled & UPI-Enabled Vending Machines |

| Market Size (2032) | USD 3.16 Billion |

Source: Market Research Outlook

The India vending machine market size is witnessing strong and consistent growth, driven by rapid expansion of corporate offices, IT/ITeS infrastructure, and increasing deployment across metro stations, airports, hospitals, and educational institutions. The India vending machine market is valued at USD 1.45 billion in 2025 and is projected to reach USD 3.16 billion by 2032, growing at a CAGR of 11.8%. This growth is supported by rising demand for automated retail, cashless transactions, and smart vending machines across high-footfall environments. Beverage vending machines continue to dominate the India vending machine market due to strong demand for tea, coffee, and cold beverages across corporate and institutional applications.

A major shift shaping the India vending machine market is the transition toward smart vending machines, IoT-enabled vending machines, and UPI-integrated vending systems. These advanced machines offer real-time monitoring, contactless payments, and improved operational efficiency, making them the fastest-growing segment in the India vending machine market. Increasing compliance with FSSAI standards, BIS energy norms, and corporate ESG commitments around hygiene and sustainability is further influencing adoption. At the same time, global players such as Sanden Vendo, Crane Merchandising Systems, N&W Global Vending, Azkoyen, and Selecta, along with domestic companies like Tata Coffee, Atlantis Industries, Wendor, and Daalchini Technologies, are expanding manufacturing and smart vending capabilities, positioning the India vending machine market as a digital-first and high-growth ecosystem through 2032.

Key Report Takeaways: India Vending Machine Market

- The India vending machine market size is expected to grow from USD 1.45 billion in 2025 to USD 3.16 billion by 2032, registering a CAGR of 11.8%. This growth in the India vending machine market is being driven by expanding corporate workplaces, rising deployment across metro stations and airports, and the increasing shift toward smart vending machines and IoT-enabled vending systems.

- Beverage vending machines continue to lead the India vending machine market, accounting for over 45% of total demand. Strong consumption of tea, coffee, and cold beverages across corporate offices, educational institutions, hospitals, and HoReCa segments is sustaining their dominance within the vending machine market in India.

- Smart vending machines, IoT-enabled vending machines, and UPI-based vending systems are emerging as the fastest-growing segments in the India vending machine market, with expected growth of 16% to 20% annually. Increasing adoption of digital payments, cashless workplace policies, and demand for real-time monitoring are accelerating this transition.

- Rapid expansion of India’s corporate real estate sector, particularly across IT/ITeS hubs such as Bengaluru, Hyderabad, Pune, Chennai, Gurugram, and Noida, is structurally driving demand in the India vending machine market. Growth in Grade-A office spaces and institutional infrastructure is creating sustained deployment opportunities.

- Increasing investments by global vending machine manufacturers such as Sanden Vendo, Crane Merchandising Systems, N&W Global Vending, and Azkoyen, along with growing participation from domestic players, are strengthening manufacturing capacity and innovation in smart vending technologies, supporting long-term growth of the India vending machine market through 2032.

Key Market Drivers: India Vending Machine Market

Rapid Expansion of Corporate Offices, IT/ITeS Sector, and Modern Workplace Infrastructure

The India vending machine market is witnessing strong momentum driven by rapid expansion of corporate offices and the IT/ITeS sector, which continues to grow at 11% to 13% annually. Corporate offices and IT parks account for nearly 42% of vending machine deployment in India, making them the largest demand centre within the vending machine industry in India. Beverage vending machines dominate installations across office pantries, breakout zones, and workplace campuses due to consistent demand for tea, coffee, and ready-to-consume beverages.

Despite this growth, vending machine penetration in India remains significantly low at around 1 unit per 4,000 to 5,000 employees, compared to 1 per 80 to 100 employees in developed markets. This gap highlights substantial untapped potential for expansion across the automated retail market in India. Leading developers such as DLF, Embassy Group, RMZ, K Raheja, and Brookfield, along with major IT companies including TCS, Infosys, Wipro, HCL, and Cognizant, are expanding their office footprint, creating sustained demand for smart vending machines and beverage vending solutions.

Low penetration combined with rapid workplace expansion signals long-term structural growth for the India vending machine market.

Looking for deeper insights on deployment trends, pricing, and operator economics? Access detailed data in the full report.

Structural Shift Toward Cashless, UPI-Enabled, and IoT-Connected Smart Vending Machines

The India vending machine market is undergoing a significant shift toward cashless vending machines, UPI-enabled systems, and IoT-enabled smart vending machines, which are growing at 16% to 20% annually—nearly twice the pace of conventional machines. This transition is driven by rapid UPI adoption, with monthly transactions exceeding 18 billion, along with RBI digital payment initiatives and corporate cashless workplace policies.

Smart vending machines are transforming the vending ecosystem in India by integrating cloud-based monitoring, predictive maintenance, automated refill alerts, dynamic pricing, and AI-driven consumer analytics. These capabilities reduce operator downtime by 30% to 40% and improve operational efficiency across vending networks. Global players such as Sanden Vendo, Crane Merchandising Systems, and Azkoyen are expanding IoT-enabled portfolios, while domestic companies like Wendor and Daalchini Technologies are scaling AI-driven and contactless vending solutions.

The shift toward smart, cashless, and connected vending machines is redefining the future of the vending machine industry in India.

Accelerated Growth of Organised Retail, Transit Hubs, and Quick-Service Consumption

The India vending machine market is further supported by rapid expansion in organised retail, transit infrastructure, and quick-service consumption. The Indian metro rail network is growing at 15% to 18% annually, while airport passenger traffic is increasing at 12% to 14%, creating high-footfall environments ideal for vending machine deployment. Vending machines are increasingly installed across metro stations, airports, railway platforms, shopping malls, and quick-service retail clusters.

Government initiatives such as the Smart Cities Mission, Bharatmala infrastructure development, and regional airport expansion under UDAN are accelerating demand for automated retail solutions. Transit operators including Delhi Metro, Bangalore Metro, Chennai Metro, Mumbai Metro, and Airports Authority of India are expanding vending networks and diversifying product offerings to meet evolving consumer demand.

High-footfall transit hubs and organised retail are emerging as critical growth engines for the India vending machine market.

Key Market Challenges: India Vending Machine Market

High Upfront Capital Cost and Long Payback Periods Pressuring Operators

The India vending machine market faces significant pressure from high upfront capital investment, particularly for smart vending machines and IoT-enabled vending systems. Machine costs typically range from INR 1.8 lakh to INR 4.5 lakh for smart vending machines, while refrigerated and combination vending machines can cost between INR 3 lakh and INR 6 lakh per unit. These costs account for nearly 60% to 75% of total operator setup investment in the vending machine industry in India.

In addition, equipment financing rates in the range of 10% to 13% have resulted in 18% to 28% fluctuations in total deployment costs over the past two years. This has compressed margins for vending operators and made long-term contracts with corporate and institutional clients more challenging. Dependence on imported components such as control boards, refrigeration systems, and payment terminals further increases cost volatility across the automated retail market in India.

High capital intensity and financing pressure remain key barriers to faster scaling in the India vending machine market.

Need deeper insights on pricing benchmarks, operator margins, and ROI models? Access detailed cost analysis in the full report.

Heavy Import Dependence for Advanced Vending Machine Components and IoT Systems

The India vending machine market remains structurally dependent on imports for advanced components and IoT control systems, with 55% to 65% of high-performance parts sourced from countries such as China, Italy, Spain, Germany, and South Korea. Critical components including payment terminals, refrigeration compressors, control boards, and sensor modules are largely imported, impacting supply stability within the vending machine ecosystem in India.

This import reliance exposes vending machine manufacturers and operators to geopolitical risks, supply chain disruptions, and extended lead times ranging from 8 to 14 weeks. High-end segments such as AI-enabled vending machines, fresh food vending solutions, and PPE vending machines show even higher import intensity. While domestic manufacturing expansion by players like Atlantis Industries and Wendor, supported by PLI schemes, is expected to reduce dependency over time, supply chain risks remain a near-term constraint.

Import dependency continues to be a structural risk factor for the vending machine industry in India, impacting cost and supply timelines.

Fragmented Operator Ecosystem, Refilling Logistics Complexity, and Machine Downtime

Operational complexity is another major challenge in the India vending machine market, driven by a fragmented operator landscape and logistics-intensive servicing requirements. Over 65% of vending machine deployments are managed by small and mid-sized operators handling 50 to 500 machines, leading to inefficiencies in route management, refilling schedules, and maintenance operations.

Refilling logistics, AMC compliance, and service downtime can add 8% to 12% to overall operating costs in the vending machine market in India. At the same time, end-users across corporate offices, hospitals, educational institutions, and transit hubs demand strict service-level agreements, including uptime guarantees, hygiene standards, and regulatory compliance such as FSSAI norms. Increasing expectations around real-time consumption data, analytics dashboards, and sustainable packaging are further raising operational complexity.

Fragmentation and logistics inefficiencies are pushing the India vending machine market toward consolidation and tech-driven operator models.

Rapid Adoption of Smart, IoT-Enabled, and Contactless Vending Machines in India

The India vending machine market is undergoing a strong shift toward smart vending machines, IoT-enabled vending systems, and contactless vending machines, with smart vending growing at 16% to 20% annually. This growth is significantly higher than conventional vending machines and reflects the broader digital transformation of the vending machine industry in India. Rapid UPI adoption, RBI-led digital payment initiatives, and corporate cashless workplace policies are accelerating demand for automated and cashless vending solutions.

Touchless and sensor-based vending machines are gaining traction across corporate offices, transit hubs, and healthcare facilities as organisations prioritise hygiene, convenience, and ESG-led wellness goals. Global players such as Sanden Vendo, Crane Merchandising Systems, N&W Global Vending, Azkoyen, and Selecta have expanded their IoT-enabled and contactless vending portfolios in India, reinforcing this structural shift

Smart, connected, and cashless vending machines are redefining the future of the India vending machine market.

Want detailed insights on technology adoption, pricing benchmarks, and product innovation? Explore the full report.

Capacity Expansion by Global Majors and Domestic Producers

The India vending machine market is witnessing significant capacity expansion driven by both global manufacturers and domestic players. Total investments in vending machine manufacturing and IoT-enabled platforms exceeded USD 380 million between 2023 and 2025, reflecting strong confidence in the automated retail market in India. These investments are strengthening local production capabilities and accelerating product innovation.

Key developments include Sanden Vendo expanding its Bhiwadi facility, Atlantis Industries scaling its Pune manufacturing unit, and Wendor commissioning AI-enabled vending lines in Bengaluru. At the same time, companies such as Tata Coffee, Daalchini Technologies, Selecta India, and Hindustan Unilever are expanding vending networks and operator partnerships, strengthening the vending ecosystem in India

Rising investments and localisation are positioning India as a key manufacturing and innovation hub for vending machines.

Rising Role of Transit Hubs, Healthcare, and Education

Transit hubs, healthcare facilities, and educational institutions are emerging as high-growth segments in the India vending machine market, expected to account for over 32% of total demand by 2032. Rapid expansion of metro networks and airport infrastructure is creating high-footfall locations ideal for vending machine deployment. These environments are driving demand for beverage vending, snack vending, fresh food vending, and PPE vending solutions.

The Indian metro rail network is expanding at 15% to 18% annually, while airport passenger traffic is growing at 12% to 14%, reinforcing demand for quick-service and unattended retail formats. Leading players such as Tata Coffee, Nestle, Hindustan Unilever, Daalchini Technologies, Lavazza, and Wendor are scaling deployments across these segments, strengthening long-term growth across the India vending machine market

High-footfall infrastructure and institutional demand are becoming core growth pillars for the India vending machine market.

Segmental Insights: India Vending Machine Market

By Application: Corporate Offices Dominate the India Vending Machine Market

Corporate offices and IT parks remain the dominant application segment in the India vending machine market, accounting for approximately 40% to 42% of total deployment. Demand is driven by expansion of Grade-A office spaces, IT hubs, BPO centres, and flexible workspaces, where vending machines provide convenient beverage and snack solutions.

Beverage and snack vending machines lead within this segment, while smart vending machines and UPI-enabled systems are rapidly gaining share. Educational institutions and HoReCa contribute around 18% to 20% of demand, while transit hubs account for 12% to 15%, reflecting diversification across the vending machine market in India

By Product Type: Beverage Vending Machines Lead, Smart Vending Grows Fastest

Beverage vending machines dominate the India vending machine market, accounting for approximately 45% to 48% of total deployment. Their strong adoption is driven by India’s high tea and coffee consumption, low ticket size, and widespread use across corporate and institutional environments.

At the same time, smart vending machines, IoT-enabled systems, AI-integrated vending machines, and contactless vending machines are the fastest-growing categories, expanding at 16% to 20% annually. Growth is driven by digital payment adoption, hygiene requirements, and demand for real-time monitoring and analytics across the automated retail ecosystem

The shift toward smart and digital vending is transforming product mix across the India vending machine market.

Regional Insights: India Vending Machine Market

Regional trends in the India vending machine market highlight strong concentration in South India and West India, which together account for 58% to 62% of total deployment. Cities such as Bengaluru, Hyderabad, Chennai, Pune, and Mumbai lead demand due to high concentration of IT/ITeS hubs, corporate offices, and HoReCa infrastructure.

North India contributes 22% to 25% of the market, led by Delhi NCR, Gurugram, Noida, and Chandigarh, supported by corporate expansion and metro infrastructure growth. East and Central India account for 14% to 18%, driven by emerging commercial hubs such as Kolkata, Bhubaneswar, Indore, and Raipur. Capacity expansions by Sanden Vendo, Atlantis Industries, Wendor, and Daalchini Technologies are strengthening regional supply chains and improving deployment efficiency across the India vending machine market

Regional expansion beyond Tier-1 cities is unlocking the next phase of growth in the India vending machine market.

Recent Developments: India Vending Machine Market

- The India vending machine market has seen strong momentum in capacity expansion and product innovation during 2024 and 2025, reinforcing growth across the vending machine industry in India. Global players such as Sanden Vendo expanded their Bhiwadi facility, while Atlantis Industries added smart and refrigerated vending machine capacity in Pune. Wendor scaled AI-integrated vending production in Bengaluru, and Crane Merchandising Systems strengthened service infrastructure across key cities. Domestic players including Tata Coffee, Daalchini Technologies, and Selecta India have also expanded operator networks and manufacturing capabilities, strengthening the automated retail market in India.

Capacity expansion and localisation are positioning India as a key manufacturing hub for smart vending machines and automated retail solutions.

- Demand-side developments in the India vending machine market have also accelerated, with corporate and institutional buyers increasing long-term sourcing partnerships. Leading companies such as TCS, Infosys, Wipro, HCL, and Cognizant expanded vending deployments across office campuses in 2025, while developers like DLF, Embassy Group, and Brookfield commissioned new Grade-A office spaces. Transit operators including Delhi Metro, Bangalore Metro, Mumbai Metro, and Airports Authority of India expanded vending machine installations across high-footfall zones, strengthening demand across the vending machine ecosystem in India.

Looking to understand buyer trends, contract structures, and demand outlook? Access deeper insights in the full report.

- Digital innovation and contactless technologies are gaining strong traction in the India vending machine market, with a clear shift toward IoT-enabled vending machines, UPI-integrated systems, and touchless vending solutions. In 2025, global manufacturers such as Sanden Vendo, Crane Merchandising Systems, N&W Global Vending, and Azkoyen launched advanced smart vending portfolios tailored for Indian corporate, healthcare, education, and transit applications. Strategic collaborations between vending machine OEMs, operators, and FMCG brands are accelerating the development of smart unmanned retail solutions across India.

Digital, contactless, and AI-enabled vending machines are shaping the next phase of growth in the India vending machine market.

Key Market Players: India Vending Machine Market

- Tata Coffee Limited (Vending Solutions)

- Nestle India Limited (Nescafé Vending)

- Hindustan Unilever Limited (BRU Vending)

- Atlantis Industries Pvt. Ltd.

- Sanden Vendo India Pvt. Ltd.

- Selecta India Pvt. Ltd.

- Wendor (Hi-Tech Robotic Systemz Limited)

- Daalchini Technologies Pvt. Ltd.

- Crane Merchandising Systems India

- N&W Global Vending India Pvt. Ltd.

- Azkoyen Group India

- Westomatic Vending Services

- Lavazza India Pvt. Ltd.

Report Scope

In this report, the India Vending Machine Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Beverage Vending Machines

- Snack & Confectionery Vending Machines

- Food Vending Machines

- Combination Vending Machines

- Specialty Vending Machines (Milk, Coffee, Tea, Tender Coconut)

- Cigarette & Tobacco Vending Machines

- Personal Care & PPE Vending Machines

- Others

- By Technology

- Conventional Mechanical Vending Machines

- Smart / IoT-Enabled Vending Machines

- AI-Integrated Vending Machines

- Refrigerated Vending Machines

- Touchless / Sensor-Based Vending Machines

- By Payment Mode

- Cash-Based

- Card-Based (Debit / Credit)

- UPI / QR Code-Based

- Mobile Wallet & NFC

- Multi-Payment Enabled

- By Application

- Corporate Offices & IT Parks

- Educational Institutions

- Hospitals & Healthcare Facilities

- Railway Stations & Metro Stations

- Airports

- Shopping Malls & Retail Outlets

- Hotels, Restaurants & Cafés (HoReCa)

- Manufacturing Plants & Factories

- Public Spaces

- Others

- By End-Use Industry

- Commercial

- Industrial

- Institutional

- Public Infrastructure

- Residential Complexes

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Dealers

- Online / B2B Platforms

- Rental & Leasing Models

- Vending Operators / Aggregators

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Vending Machine Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic vending machine OEMs, IoT-enabled smart vending specialists, global entrants, or niche segment leaders.

The India Vending Machine Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Qualitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Application

- By End-Use Industry

- By Technology

- By Payment Mode

- By Sales Channel

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Vending Machine Market

- India Vending Machine Market Insights

- Market Dynamics

- Growth Drivers

- Rapid expansion of corporate offices, IT/ITeS sector and modern workplace infrastructure driving core vending machine deployment.

- Structural shift toward cashless, UPI-enabled and IoT-connected smart vending machines aligned with digital India adoption.

- Accelerated growth of organised retail, transit hubs and quick-service consumption demand for unmanned automated retail.

- Restraints

- High upfront capital cost and long payback periods for vending machine operators pressuring margins.

- Heavy import dependence for advanced vending machine components and IoT control systems creating supply risk.

- Fragmented operator ecosystem, refilling logistics complexity and machine downtime raising operational costs.

- Opportunities

- Rapid scale-up of smart, IoT-enabled and contactless vending machines aligned with digital India and unmanned retail mandates.

- High-growth demand from metro stations, airports, hospitals and educational institutions supporting public-space vending build-out.

- Emerging opportunity for healthy snack, fresh meal and PPE vending machines targeting urban consumer wellness and convenience demand.

- Challenges

- Intense price-led competition between global vending machine majors and domestic operators compressing margins.

- Shortage of skilled field service technicians, refill operators and IoT integration specialists limiting scale-up speed of new deployments.

- Fragmented downstream operator and corporate buyer base with diverse specifications increasing customisation and inventory complexity.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Growth Drivers

- Industry Value Chain & Entry Points

- Upstream Component Suppliers (sheet metal, refrigeration units, payment terminals, microcontrollers, sensors)

- Vending Machine OEMs (Indian and global manufacturers, contract assemblers)

- IoT, Software & Telematics Providers (cloud platforms, payment gateways, monitoring software)

- System Integrators & Customisation Workshops (BIS, FSSAI, energy compliance)

- Distributors, Dealers & B2B Marketplaces

- Vending Operators & Aggregators (refilling, servicing, route management)

- Product Suppliers (beverage brands, snack brands, FMCG, fresh food, dairy)

- End Customers (corporate, education, healthcare, transport, retail, public spaces)

- Service & Maintenance Channels (AMC providers, field technicians, spare-part networks)

- Recycling & End-of-Life Handling (e-waste, refrigerant recovery)

- India Vending Machine Market: Regulatory Framework

- India Vending Machine Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (‘000 Units)

- Market Share & Forecast

- By Product Type

- Beverage Vending Machines

- Snack & Confectionery Vending Machines

- Food Vending Machines

- Combination Vending Machines

- Specialty Vending Machines (Milk, Coffee, Tea, Tender Coconut)

- Cigarette & Tobacco Vending Machines

- Personal Care & PPE Vending Machines

- Others

- By Technology

- Conventional Mechanical Vending Machines

- Smart / IoT-Enabled Vending Machines

- AI-Integrated Vending Machines

- Refrigerated Vending Machines

- Touchless / Sensor-Based Vending Machines

- By Payment Mode

- Cash-Based

- Card-Based (Debit / Credit)

- UPI / QR Code-Based

- Mobile Wallet & NFC

- Multi-Payment Enabled

- By Application

- Corporate Offices & IT Parks

- Educational Institutions

- Hospitals & Healthcare Facilities

- Railway Stations & Metro Stations

- Airports

- Shopping Malls & Retail Outlets

- Hotels, Restaurants & Cafés (HoReCa)

- Manufacturing Plants & Factories

- Public Spaces

- Others

- By End-Use Industry

- Commercial

- Industrial

- Institutional

- Public Infrastructure

- Residential Complexes

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Dealers

- Online / B2B Platforms

- Rental & Leasing Models

- Vending Operators / Aggregators

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Vending Machine Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Tata Coffee Limited (Vending Solutions)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Tata Coffee Limited (Vending Solutions)

- By Product Type

- Market Size & Forecast, 2021-2032

- Market Dynamics

(Same Data Pointers Will Be Provided for The Below Companies)

- Nestle India Limited (Nescafé Vending)

- Hindustan Unilever Limited (BRU Vending)

- Atlantis Industries Pvt. Ltd.

- Sanden Vendo India Pvt. Ltd.

- Selecta India Pvt. Ltd.

- Wendor (Hi-Tech Robotic Systemz Limited)

- Daalchini Technologies Pvt. Ltd.

- Crane Merchandising Systems India

- N&W Global Vending India Pvt. Ltd.

- Azkoyen Group India

- Westomatic Vending Services

- Lavazza India Pvt. Ltd.

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India vending machine market and what is its growth forecast?

Ans: The India vending machine market size is valued at USD 1.45 billion in 2025 and is projected to reach USD 3.16 billion by 2032, growing at a CAGR of around 11.8%. This strong growth is driven by rapid expansion of corporate offices and IT/ITeS infrastructure, increasing deployment across metro stations, airports, hospitals, and educational institutions, and the structural shift toward smart, IoT-enabled, and UPI-integrated vending machines. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across product types, technologies, and applications.

2. What are the key growth drivers of the India vending machine market?

Ans: The India vending machine market growth is primarily driven by rising adoption of cashless and UPI-based payment systems, expansion of corporate workplaces and IT parks, and increasing demand from public infrastructure such as metro stations and airports. Additional drivers include growing preference for contactless and hygiene-focused retail, smart city initiatives, and increasing participation from global and domestic vending machine manufacturers. The report offers a comprehensive analysis of these drivers along with their long-term impact on market expansion.

3. Which segment dominates the India vending machine market and which is growing fastest?

Ans: Beverage vending machines dominate the India vending machine market, accounting for over 45% of total demand due to strong adoption across corporate offices, educational institutions, and healthcare facilities. Meanwhile, smart, IoT-enabled, and UPI-integrated vending machines are the fastest-growing segment, expanding at a significantly higher rate due to digital payment adoption, remote monitoring capabilities, and increasing demand for advanced automated retail solutions. The report provides detailed segment-wise performance and future outlook.

4. What are the latest trends shaping the India vending machine market?

Ans: The market is witnessing a strong shift toward smart and IoT-enabled vending machines with features such as real-time monitoring, predictive maintenance, and AI-driven consumer analytics. Contactless and sensor-based vending systems are gaining traction due to hygiene concerns, while fresh food and refrigerated vending solutions are expanding across corporate and healthcare sectors. The report highlights these emerging trends and their role in transforming the vending machine ecosystem in India.

5. What challenges does the India vending machine market face?

Ans: The India vending machine market faces challenges including high upfront capital investment, dependence on imported components such as control boards and refrigeration systems, and operational complexities related to refilling logistics and machine uptime. Regulatory compliance with BIS and FSSAI standards also adds cost and operational pressure. Despite these challenges, ongoing investments in local manufacturing, IoT integration, and operator efficiency are expected to support long-term market growth.

Frequently Asked Questions

1. How large is the India vending machine market and what is its growth forecast?

Ans: The India vending machine market size is valued at USD 1.45 billion in 2025 and is projected to reach USD 3.16 billion by 2032, growing at a CAGR of around 11.8%. This strong growth is driven by rapid expansion of corporate offices and IT/ITeS infrastructure, increasing deployment across metro stations, airports, hospitals, and educational institutions, and the structural shift toward smart, IoT-enabled, and UPI-integrated vending machines. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across product types, technologies, and applications.

2. What are the key growth drivers of the India vending machine market?

Ans: The India vending machine market growth is primarily driven by rising adoption of cashless and UPI-based payment systems, expansion of corporate workplaces and IT parks, and increasing demand from public infrastructure such as metro stations and airports. Additional drivers include growing preference for contactless and hygiene-focused retail, smart city initiatives, and increasing participation from global and domestic vending machine manufacturers. The report offers a comprehensive analysis of these drivers along with their long-term impact on market expansion.

3. Which segment dominates the India vending machine market and which is growing fastest?

Ans: Beverage vending machines dominate the India vending machine market, accounting for over 45% of total demand due to strong adoption across corporate offices, educational institutions, and healthcare facilities. Meanwhile, smart, IoT-enabled, and UPI-integrated vending machines are the fastest-growing segment, expanding at a significantly higher rate due to digital payment adoption, remote monitoring capabilities, and increasing demand for advanced automated retail solutions. The report provides detailed segment-wise performance and future outlook.

4. What are the latest trends shaping the India vending machine market?

Ans: The market is witnessing a strong shift toward smart and IoT-enabled vending machines with features such as real-time monitoring, predictive maintenance, and AI-driven consumer analytics. Contactless and sensor-based vending systems are gaining traction due to hygiene concerns, while fresh food and refrigerated vending solutions are expanding across corporate and healthcare sectors. The report highlights these emerging trends and their role in transforming the vending machine ecosystem in India.

5. What challenges does the India vending machine market face?

Ans: The India vending machine market faces challenges including high upfront capital investment, dependence on imported components such as control boards and refrigeration systems, and operational complexities related to refilling logistics and machine uptime. Regulatory compliance with BIS and FSSAI standards also adds cost and operational pressure. Despite these challenges, ongoing investments in local manufacturing, IoT integration, and operator efficiency are expected to support long-term market growth.