India VAM Market, By Application (Polyvinyl Acetate, Polyvinyl Alcohol, EVA, VAE, PVB, Others); By End-Use Industry (Adhesives & Sealants, Paints & Coatings, Packaging Films, Textiles & Fibers, Automotive, Solar Photovoltaic, Others); By Grade (Adhesive, Coating, Polymer, Fiber, Specialty); By Distribution Channel (Direct Sales, Distributors & Traders, Importers, Online B2B, Specialty Distributors, Tolling); By End-User (Paints & Coatings, Packaging, Adhesives & Sealants, Solar & Specialty); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Chemicals & Advanced Materials

- Jun 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India VAM Market: Adhesives Demand, Solar Manufacturing and EVA/VAE Innovation Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

| Market Size (2025) | USD 540 Million |

| CAGR (2026-2032) | 8.1% |

| Leading Segment | Polyvinyl Acetate (Adhesives & Sealants) |

| Fastest Growing Segment | EVA & VAE Derivatives |

| Market Size (2032) | USD 935 Million |

Source: Market Research Outlook

Market Overview: India VAM Market

The India VAM market size is witnessing rapid expansion, driven by accelerating adhesives and coatings demand, growing solar module manufacturing, rising construction activity, expanding packaging and footwear production, increasing demand for EVA and VAE derivatives, and major capacity additions by domestic acetyls producers. Valued at USD 540 million in 2025 and projected to reach USD 935 million by 2032, growing at a CAGR of 8.1%, the India VAM market growth is being fuelled by strong demand from downstream adhesives, paints, and solar manufacturers, rising industrial activity, and the rapid scaling of vinyl acetate monomer derivative production across industrial clusters. Polyvinyl acetate leads consumption, while the EVA and VAE derivative segment is emerging as the fastest growing category. Shifting demand toward high-performance derivatives, growing solar capacity, and rising demand for low-VOC and specialty applications are reshaping the supply landscape. As domestic majors including GNFC, Jubilant Ingrevia, Laxmi Organic, Pidilite, and Asian Paints expand integrated VAM derivative capacity, and global VAM producers including Celanese, LyondellBasell, Wacker, and Dairen scale India supply pipelines, the India VAM market is evolving into a demand-led, innovation-driven, and increasingly localized ecosystem with strong long-term growth potential.

Key Report Takeaways: India VAM Market

- The India VAM market size is projected to grow from USD 540 million in 2025 to USD 935 million by 2032, registering a strong CAGR of 8.1%, driven by accelerated adhesives and coatings demand, rising solar-grade EVA adoption, and the structural shift toward high-performance vinyl acetate monomer derivatives across industrial India.

- Polyvinyl acetate dominates the India VAM market, accounting for over 46% of total consumption in 2025, driven by strong demand for adhesives and sealants, the deep presence of downstream players such as Pidilite, Jubilant, and Laxmi Organic, and rising industrial demand across packaging, woodworking, and construction applications.

- EVA and VAE derivatives are emerging as the fastest growing segments in the India VAM market, expected to grow at 11% to 15% annually as solar manufacturers, construction formulators, and low-VOC coating producers reshape sourcing strategies across industrial and metro markets.

- Rapid scaling of solar module manufacturing, with over 50 GW of planned Indian solar cell and module capacity by 2030, is structurally expanding the India VAM market across EVA encapsulant, adhesives, and coatings categories.

- Rising investments by domestic players such as GNFC, Jubilant Ingrevia, Laxmi Organic, Pidilite, and Asian Paints in acetyls capacity, derivative production, and specialty VAM applications are strengthening local supply and supporting the India VAM market forecast 2032.

Key Market Drivers: India VAM Market

Rising Adhesives, Paints and Coatings Demand and Solar Manufacturing Driving VAM Consumption Across India

Growth in the India VAM market is being driven by rising adhesives and coatings demand, the expansion of solar module manufacturing, and aggressive scaling of downstream derivative capacity across industrial clusters in Gujarat, Maharashtra, and Tamil Nadu. India’s adhesives and sealants demand crossed 1.9 million tonnes in 2025, with consumption growth climbing to 9% and projected to reach 2.6 million tonnes by 2030. Solar module manufacturing capacity has expanded from around 18 GW in 2022 to over 38 GW in 2025, led by EVA encapsulant demand across players such as Pidilite, Asian Paints, Berger, Jubilant, and Supreme. Polyvinyl acetate and EVA have become signature VAM derivatives for these applications, with average VAM landed prices ranging between USD 1,050 and USD 1,400 per tonne. Per-capita VAM consumption in India remains below 0.2 kg per year, indicating significant long-term headroom for growth. Rising urbanization, with over 510 million urban residents, falling solar tariffs, and growing aspirational construction are creating strong structural pull-through demand across the India VAM market.

Growing Construction Activity, Rising Packaging Demand, and Shifting Toward High-Performance Derivatives Fuelling Premium VAM Adoption

The India VAM market is benefiting from sustained growth in industrial output, with construction sector output rising by over 70% between 2014 and 2024 according to MOSPI, alongside continued cost reductions in modern derivative processing, emulsion polymerization, and downstream integration. Average landed VAM prices in India now range between USD 1,050 and USD 1,400 per tonne, with specialty and solar grades commanding USD 1,500 to USD 1,800 per tonne. Domestic acetyls and derivative capacity has scaled rapidly, with organized derivative throughput exceeding 1.9 million tonnes by 2025, led by Pidilite, Jubilant Ingrevia, Laxmi Organic, GNFC, and Asian Paints. BIS quality standards, REACH-aligned norms, and growing trust in domestically processed VAM derivatives have further strengthened organized supply, supporting price competitiveness across the India VAM market. Downstream adhesives and coatings applications now account for over 60% of VAM consumption, with formulators preferring high-performance, low-VOC, and specialty derivatives.

Product Innovation in EVA, VAE, and Specialty PVOH Grades Strengthening Downstream Derivative Growth

Rapid growth in EVA and VAE derivatives is a major catalyst for the India VAM market, with the EVA segment projected to grow at 11% to 15% annually through 2032. Solar manufacturing accounts for roughly 40% of incremental EVA demand, creating strong demand for high vinyl acetate content encapsulant films. Performance-driven formulation under construction, packaging, and coatings trends, durability targets, and growing low-VOC awareness are driving large consumers toward specialty VAM derivative consumption. The BIS quality and labelling norms updated in 2024 have increased transparency for industrial buyers, accelerating premium VAM derivative adoption to hedge against rising performance demands. Leading VAM derivative innovators such as Pidilite, Wacker, Asian Paints, Jubilant Ingrevia, and Laxmi Organic have scaled EVA, VAE, and PVOH pipelines, with the solar-grade EVA segment alone representing an estimated USD 80 million addressable opportunity within Indian solar markets. Government solar programs combined with infrastructure-led procurement are structurally expanding India VAM market growth across all major end-use categories through 2032.

Key Market Challenges: India VAM Market

Heavy Import Dependence and Limited Domestic VAM Production Capacity

The India VAM market continues to face challenges around heavy import dependence and limited domestic capacity among industrial consumers, with a typical year seeing over 70% of vinyl acetate monomer demand met through imports before any local value addition. While domestic acetyls investments and growing demand for VAM derivatives have improved availability, organized VAM production within India remains thin at only a few specialized sites, reflecting bottlenecks in feedstock integration, capital intensity, and global price competition. Industry experts continue to caution against supply concentration risks for adhesive and coating producers, while specialty and solar-grade VAM capacity within India remains underdeveloped. India’s continued dependence on imported monomer limits supply security among mid-sized and MSME processors across the India VAM market.

Feedstock Price Volatility and Global Supply Disruptions Across Industrial Clusters

The India VAM market faces structural complexity from variations in feedstock availability, logistics density, and supply timelines across different clusters. While industrial hubs such as Mumbai, Ahmedabad, Vadodara, Chennai, and Hyderabad have well-established chemical logistics frameworks with port and storage access above 80%, others maintain limited storage infrastructure and longer supply lead times. Average inventory cover for imported VAM ranges between 15 and 45 days, and unbroken feedstock supply remains a key bottleneck in inland cluster rollout. Differential availability of bonded warehousing, storage tankage, and last-mile transport across states creates operational complexity for VAM derivative players such as Pidilite, Jubilant, Laxmi Organic, and GNFC operating pan-India. While the Department of Chemicals has launched capacity incentive schemes, supply fragmentation remains a near-term challenge for the India VAM market.

Volatility in Ethylene and Acetic Acid Prices and Energy Costs Impacting Overall VAM Margins

The India VAM market faces practical constraints around feedstock price volatility, energy cost inflation, and margin compression across the value chain. Global ethylene and acetic acid prices have risen by 12% to 18% between 2022 and 2025, while energy and freight input costs including power, gas, and shipping have moved up by 8% to 14% over the same period. Smaller VAM derivative producers face additional complexity in passing through cost increases without losing volume. Average gross margins for VAM derivatives in India range between 18% and 28%, reducing the effective profitability of new capacity by 4% to 10%. Domestic acetyls integration, energy-efficient process upgrades, and high-value specialty derivatives are emerging as solutions to differentiate, but capital intensity and limited feedstock availability remain barriers to widespread adoption across the India VAM market.

Key Market Trends: India VAM Market

Rapid Adoption of Solar-Grade EVA, VAE Emulsions, and Specialty Derivatives in India

The India VAM market is undergoing a clear technology shift toward solar-grade EVA, VAE emulsions, and specialty derivatives, with these advanced grades expected to capture over 25% of new VAM derivative demand by 2027. Solar EVA encapsulant films deliver vinyl acetate content of 28% to 33%, compared to 18% to 25% for general-purpose grades, while VAE emulsions add superior low-VOC and binding performance for water-based coatings. Leading domestic and global producers including Pidilite, Wacker, Jubilant Ingrevia, Asian Paints, and Supreme have scaled EVA, VAE, and specialty derivative production capacity through 2024 and 2025. Specialty VAM derivatives with high purity, barrier, and adhesion performance are also gaining traction, particularly in industrial hubs such as Mumbai and Ahmedabad where solar and coatings demand is rising, with players like Berger, Laxmi Organic, and GNFC offering performance-positioned VAM derivatives for high-growth buyers. This product transition is reinforcing the India VAM market forecast 2032 across both industrial and solar categories.

Growth of Domestic Acetyls Capacity, Downstream Integration, and Localized Supply in the India VAM Market

A clear shift toward domestic acetyls capacity, downstream integration, and localized supply models is reshaping the India VAM market, particularly in the adhesives and coatings segment. Under derivative integration strategies by players such as Pidilite, Jubilant, Laxmi Organic, and GNFC, VAM-based products are produced with feedstock cost advantages typically 5% to 12% below imported-equivalent levels. Leading VAM derivative producers including Pidilite and Asian Paints have built combined downstream reach exceeding 800 industrial accounts, with adhesives ranking among the top VAM consuming applications. Channel partners and B2B platforms such as IndiaMART, TradeIndia, and specialty distributors are also reducing procurement costs and accelerating VAM adoption across both adhesives and coatings segments of the India VAM market. By 2025, domestic VAM derivatives account for over 30% of VAM-based product value in India, up from less than 18% in 2020, with industrial buyers increasingly preferring localized supply security over import reliance.

Capacity Expansion by Domestic Acetyls Producers and Specialty Derivative Investments

A wave of domestic capacity expansion and specialty derivative investments is reshaping the India VAM market supply landscape. Combined India-focused capital expenditure announcements in acetyls, VAM derivatives, and downstream integration exceeded USD 1.2 billion across 2023 to 2025. Pidilite expanded VAM derivative capacity across its adhesives lines, Jubilant Ingrevia scaled acetyls and specialty intermediates at its Gajraula and Bharuch sites, Laxmi Organic commissioned new acetyls capacity in Maharashtra, GNFC expanded its Bharuch facility, and Asian Paints grew its emulsion and VAE derivative portfolio. BIS quality reforms, Production Linked Incentive (PLI) scheme allocations for chemicals exceeding INR 10,900 crore, and reduced duties on key feedstocks have structurally favoured organized supply. Combined with solar manufacturing driving EVA demand and packaging procurement scaling rapidly, these developments are reinforcing the India VAM market forecast 2032 across the entire value chain.

Segmental Insights: India VAM Market

By End-User: Adhesive & Sealant Producers Segment Dominates the India VAM Market

The adhesive and sealant producers end-user segment dominates the India VAM market, accounting for an estimated 44% to 48% of total consumption, driven by rising construction demand, growing packaging and woodworking activity, and improving derivative economics. Polyvinyl acetate and VAE-based formulations are the dominant VAM derivatives within this segment, with adhesive and emulsion grades capturing over 72% of producer-level VAM purchases. The paints and coatings manufacturers segment contributes another 24% to 27% of demand, driven by decorative coatings, low-VOC paints, and industrial finishes adopting VAM derivatives as a core binder. The packaging and film converters segment accounts for 14% to 17%, led by flexible packaging, laminates, and barrier film applications. In 2025, leading VAM consumers including Pidilite, Asian Paints, Jubilant, Laxmi Organic, and Supreme scaled up adhesives and coatings derivative deployment under construction and packaging expansion, reinforcing segment dominance in the India VAM market.

By Application: Polyvinyl Acetate Leads While EVA and VAE Grow Fastest

Polyvinyl acetate leads the India VAM market application landscape, accounting for approximately 46% of total VAM consumption, driven by its strong adhesives demand, deep downstream presence, and improving cost economics. Polyvinyl alcohol contributes another 15% to 18%, primarily across textiles, paper, and specialty film applications. EVA and VAE are the fastest growing applications within the India VAM market, expanding at 11% to 15% annually, driven by superior performance positioning of high vinyl acetate content grades, additional functional benefits, and growing adoption in solar and premium coatings segments. PVB and specialty VAM derivatives together account for 6% to 8% of the market, with the PVB segment expected to grow rapidly through 2032 in automotive and architectural glass markets. Leading domestic and global manufacturers including Celanese, LyondellBasell, Wacker, Pidilite, and Jubilant Ingrevia have aligned product portfolios to this application mix, driving premium VAM derivative adoption across the India VAM market.

Regional Insights: India VAM Market

Regional analysis of the India VAM market shows that West India and South India collectively account for approximately 56% to 60% of total VAM consumption, driven by Gujarat (Ahmedabad and Bharuch chemical belt), Maharashtra (Mumbai and Pune industrial belt), Tamil Nadu (Chennai manufacturing belt), Karnataka, and Telangana, supported by established chemical clusters and strong downstream consumption levels. North India contributes around 24% to 27% of demand, led by Delhi NCR, Punjab, Haryana, and Uttar Pradesh, supported by adhesives and packaging derivative adoption in industrial clusters around Delhi, Gurugram, Noida, and Lucknow. Central and East India together account for 14% to 17% of demand, supported by Madhya Pradesh, West Bengal, Bihar, and Odisha, where industrial derivative adoption is accelerating. In 2025, capacity additions and supply operations by Pidilite across Gujarat and Maharashtra, Laxmi Organic across Maharashtra, Jubilant across Uttar Pradesh, and GNFC across Gujarat reinforced regional supply hubs, supporting closer execution of adhesives and coatings projects across the India VAM market.

Recent Developments: India VAM Market

- The India VAM market witnessed strong momentum in capacity and derivative progress during 2024 and 2025. India added a record 60 new VAM derivative and emulsion lines in calendar year 2025, representing a 38% year-on-year increase from 43 lines in 2024, according to industry tracking. Solar manufacturers recorded over 28 GW of new module capacity commissioning by mid-2025, with the EVA encapsulant segment accounting for 71% of incremental VAM-linked demand. Cumulative organized VAM derivative volume in India is projected to reach 540 to 580 kilo tons by FY27 from 380 kilo tons in FY25, growing at an average 16% annually.

- Domestic acetyls and derivative producers have deepened India-focused capacity expansion. In 2025, Pidilite scaled VAM derivative capacity across its adhesives lines, Jubilant Ingrevia expanded acetyls and specialty intermediates at its Gajraula and Bharuch sites, Laxmi Organic commissioned new acetyls capacity in Maharashtra, GNFC expanded its Bharuch facility, and Asian Paints grew its emulsion and VAE derivative portfolio. Supreme Industries entered specialty packaging derivatives with new EVA-based lines. These developments are strengthening domestic supply and supporting the India VAM market forecast 2032.

- Solar and coatings VAM momentum has gained strong traction in the India VAM market. In 2025, leading consumers including Pidilite, Asian Paints, Berger Paints, Jubilant Ingrevia, Laxmi Organic, and Supreme expanded VAM derivative offerings. Strategic partnerships between global VAM producers and domestic derivative players are positioning India as one of the most actively scaling vinyl acetate monomer markets globally, strengthening long-term competitive positioning in the India VAM market forecast 2032.

Key Market Players: India VAM Market

- Celanese Corporation

- LyondellBasell Industries N.V.

- Wacker Chemie AG

- Dairen Chemical Corporation

- Kuraray Co., Ltd.

- Sipchem (Saudi International Petrochemical Company)

- Sinopec (China Petroleum & Chemical Corporation)

- Gujarat Narmada Valley Fertilizers & Chemicals Ltd. (GNFC)

- Jubilant Ingrevia Limited

- Laxmi Organic Industries Limited

- Pidilite Industries Limited

- Asian Paints Limited

- Supreme Industries Limited

Report Scope

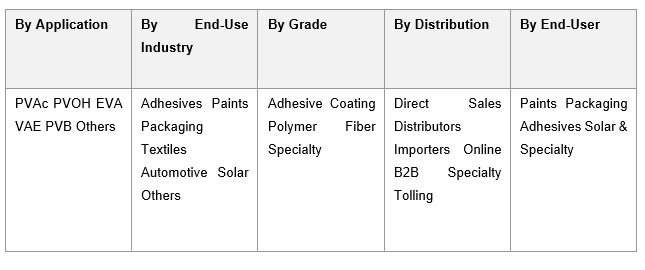

In this report, the India VAM Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Application

- Polyvinyl Acetate (PVAc)

- Polyvinyl Alcohol (PVOH)

- Ethylene Vinyl Acetate (EVA)

- Vinyl Acetate Ethylene (VAE)

- Polyvinyl Butyral (PVB)

- Others

- By End-Use Industry

- Adhesives & Sealants

- Paints & Coatings

- Packaging Films

- Textiles & Fibers

- Automotive

- Solar Photovoltaic

- Others

- By Grade

- Adhesive Grade

- Coating Grade

- Polymer Grade

- Fiber Grade

- Specialty Grade

- By Distribution Channel

- Direct Sales & Long-Term Contracts

- Distributors & Traders

- Importers & Channel Partners

- Online B2B Platforms

- Specialty Chemical Distributors

- Tolling & Institutional Supply

- By End-User

- Paints & Coatings Manufacturers

- Packaging & Film Converters

- Adhesive & Sealant Producers

- Solar & Specialty Manufacturers

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India VAM Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic VAM derivative producers, specialty EVA and VAE manufacturers, regional acetyls players, or niche specialty chemical brands.

The India VAM Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Application

- By End-Use Industry

- By Grade

- By Distribution Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India VAM Market

- India VAM Market Insights

- Market Dynamics

- Growth Drivers

- Rising adhesives, paints and coatings demand, and solar module manufacturing driving VAM consumption across India.

- Growing construction activity, rising packaging demand, and shifting toward high-performance derivatives fuelling premium VAM adoption.

- Product innovation in EVA, VAE, and specialty PVOH grades strengthening downstream VAM derivative growth.

- Restraints

- Heavy import dependence and limited domestic capacity restricting reliable VAM supply for Indian processors.

- Feedstock price volatility and global supply disruptions restricting stable VAM availability across industrial clusters.

- Volatility in ethylene and acetic acid prices and energy costs impacting overall VAM margins.

- Opportunities

- Domestic acetyls capacity, EVA, and VAE derivative innovation opening untapped demand pools across industrial hubs.

- Specialty, high-purity, and solar-grade VAM derivatives supporting next-generation growth in coatings and solar segments.

- Solar manufacturing, packaging expansion, and downstream integration creating massive VAM consumption opportunities.

- Challenges

- Intense competition from imported VAM and low-cost monomer supply from global petrochemical producers.

- Limited domestic production infrastructure and inconsistent feedstock availability across Indian clusters.

- Maintaining consistent purity, polymer-grade quality, and supply reliability at scale across diverse Indian industrial markets.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (ethylene, acetic acid, oxygen, methanol, palladium catalysts, natural gas feedstock)

- VAM & Acetyl Producers (Celanese, LyondellBasell, Dairen, GNFC, Jubilant Ingrevia)

- Feedstock & Catalyst Suppliers (ethylene, acetic acid, oxygen, palladium-gold catalysts)

- Derivative & Polymer Producers (PVAc, PVOH, EVA, VAE, PVB resins)

- Quality Control, R&D & Testing Laboratories (BIS, ASTM, ISO chemical standards)

- Distributors, Traders & Importers (B2B chemical distribution networks)

- Adhesives, Paints & Coatings Manufacturers (Pidilite, Asian Paints, Berger, Jubilant)

- Brand Owners & Specialty Formulators (Pidilite, Wacker, Asian Paints, Supreme, Jubilant)

- Channel Partners & Online B2B Platforms (IndiaMART, TradeIndia, distributors, importers)

- End-Users (adhesive makers, paint companies, packaging converters, solar manufacturers, textile mills)

- India VAM Market: Regulatory Framework

- India VAM Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Kilo Tons)

- Market Share & Forecast

- By Application

- Polyvinyl Acetate (PVAc)

- Polyvinyl Alcohol (PVOH)

- Ethylene Vinyl Acetate (EVA)

- Vinyl Acetate Ethylene (VAE)

- Polyvinyl Butyral (PVB)

- Others

- By End-Use Industry

- Adhesives & Sealants

- Paints & Coatings

- Packaging Films

- Textiles & Fibers

- Automotive

- Solar Photovoltaic

- Others

- By Grade

- Adhesive Grade

- Coating Grade

- Polymer Grade

- Fiber Grade

- Specialty Grade

- By Distribution Channel

- Direct Sales & Long-Term Contracts

- Distributors & Traders

- Importers & Channel Partners

- Online B2B Platforms

- Specialty Chemical Distributors

- Tolling & Institutional Supply

- By End-User

- Paints & Coatings Manufacturers

- Packaging & Film Converters

- Adhesive & Sealant Producers

- Solar & Specialty Manufacturers

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India VAM Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Celanese Corporation

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

(Same Data Pointers Will Be Provided for The Below Companies)

- LyondellBasell Industries N.V.

- Wacker Chemie AG

- Dairen Chemical Corporation

- Kuraray Co., Ltd.

- Sipchem (Saudi International Petrochemical Company)

- Sinopec (China Petroleum & Chemical Corporation)

- Gujarat Narmada Valley Fertilizers & Chemicals Ltd. (GNFC)

- Jubilant Ingrevia Limited

- Laxmi Organic Industries Limited

- Pidilite Industries Limited

- Asian Paints Limited

- Supreme Industries Limited

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India VAM market and what is its growth forecast?

Ans: The India VAM market is valued at USD 540 million in 2025 and projected to reach USD 935 million by 2032, at a CAGR of 8.1%, supported by rising adhesives demand, solar manufacturing, and high-performance VAM derivatives.

2. Which segments are driving demand in the India VAM market?

Ans: Polyvinyl acetate leads with over 46% consumption share, while EVA and VAE derivatives are the fastest-growing segments, driven by solar manufacturers, construction formulators, and low-VOC coating producers across industrial clusters.

3. What are the key drivers of growth in the India VAM market?

Ans: Key drivers include rising adhesives and coatings demand, expanding solar module manufacturing, growing construction activity, rising packaging demand, product innovation in EVA and VAE derivatives, and scaling of domestic acetyls capacity.

4. Which regions are driving growth in the India VAM market?

Ans: West India and South India lead with around 56% to 60% of total consumption, driven by Gujarat, Maharashtra, Tamil Nadu, Karnataka, and Telangana. North India and Delhi NCR also show strong VAM demand.

5. What are the latest trends in the India VAM market?

Ans: The latest trends include rapid adoption of solar-grade EVA and VAE emulsions, growth in domestic acetyls capacity, rising demand for specialty derivatives, low-VOC coatings, and expanding downstream integration driving organized VAM supply.

Frequently Asked Questions

1. How large is the India VAM market and what is its growth forecast?

Ans: The India VAM market is valued at USD 540 million in 2025 and projected to reach USD 935 million by 2032, at a CAGR of 8.1%, supported by rising adhesives demand, solar manufacturing, and high-performance VAM derivatives.

2. Which segments are driving demand in the India VAM market?

Ans: Polyvinyl acetate leads with over 46% consumption share, while EVA and VAE derivatives are the fastest-growing segments, driven by solar manufacturers, construction formulators, and low-VOC coating producers across industrial clusters.

3. What are the key drivers of growth in the India VAM market?

Ans: Key drivers include rising adhesives and coatings demand, expanding solar module manufacturing, growing construction activity, rising packaging demand, product innovation in EVA and VAE derivatives, and scaling of domestic acetyls capacity.

4. Which regions are driving growth in the India VAM market?

Ans: West India and South India lead with around 56% to 60% of total consumption, driven by Gujarat, Maharashtra, Tamil Nadu, Karnataka, and Telangana. North India and Delhi NCR also show strong VAM demand.

5. What are the latest trends in the India VAM market?

Ans: The latest trends include rapid adoption of solar-grade EVA and VAE emulsions, growth in domestic acetyls capacity, rising demand for specialty derivatives, low-VOC coatings, and expanding downstream integration driving organized VAM supply.