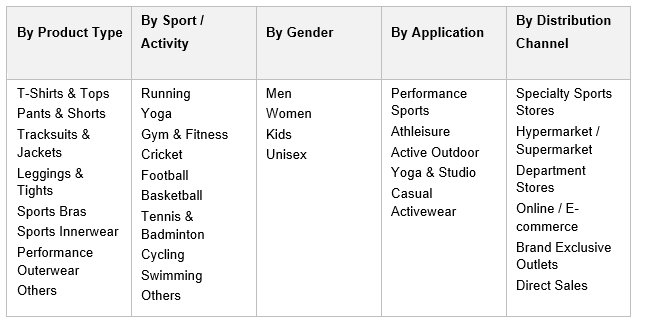

India Sports Apparel Market, By Product Type (T-Shirts & Tops, Pants & Shorts, Tracksuits & Jackets, Leggings & Tights, Sports Bras, Sports Innerwear, Performance Outerwear, Others); By Sport / Activity (Running, Yoga, Gym & Fitness, Cricket, Football, Basketball, Tennis & Badminton, Cycling, Swimming, Others); By Gender (Men, Women, Kids, Unisex); By Fabric Type (Polyester, Cotton, Cotton-Polyester Blend, Polyester-Elastane Blend, Recycled & Sustainable Fabrics, Bamboo & Organic Cotton, Others); By Price Range (Premium, Mid-Range, Mass); By Application (Performance Sports, Athleisure, Active Outdoor, Yoga & Studio, Casual Activewear); By End-User (Individual / Personal Use, Institutional, Corporate, Sports Clubs & Academies); By Distribution Channel (Specialty Sports Stores, Hypermarket / Supermarket, Department Stores, Online / E-commerce, Brand Exclusive Outlets, Direct Sales); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 130

- Report Format: pdf

- Report Price: $1800 USD

India Sports Apparel Market: Athleisure Mainstreaming, Women’s Activewear, and D2C Sportswear Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

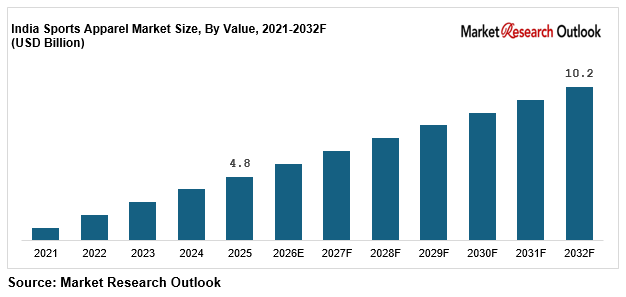

| Market Size (2025) | USD 4.8 Billion |

| CAGR (2026-2032) | 11.5% |

| Leading Segment | Men’s Sports Apparel (T-Shirts & Track Pants) |

| Fastest Growing Segment | Women’s Athleisure & Yoga Wear |

| Market Size (2032) | USD 10.2 Billion |

Source: Market Research Outlook

Market Overview: India Sports Apparel Market

The India sports apparel market size is witnessing rapid expansion, driven by rising fitness awareness, the mainstreaming of athleisure as everyday wear, growing women’s and kids’ sports participation, government-led Khelo India and Fit India programmes, rapid expansion of e-commerce, D2C sportswear brands, and quick commerce platforms, and growing investments by domestic and global sportswear majors in India-specific sports apparel manufacturing capacity, R&D, and digital-first sportswear brand platforms. Valued at USD 4.8 Billion in 2025 and projected to reach USD 10.2 Billion by 2032, growing at a CAGR of 11.5%, the Indian sports apparel industry is being fuelled by strong demand for T-shirts, track pants, leggings, sports bras, tracksuits, and performance outerwear, rising consumption across cricket, running, gym, yoga, and football, and growing institutional adoption across schools, colleges, sports academies, and IPL and ISL franchises. Men’s sports apparel leads consumption, while women’s athleisure and yoga wear is emerging as the fastest growing category in the India sports apparel market. Tightening BIS, REACH, and sustainability standards, growing ESG and recycled-content commitments, and the structural premiumisation wave are reshaping the supply landscape. As global majors including PUMA Sports India, Nike India, Adidas India, Decathlon, ASICS, Reebok, Skechers, and Under Armour expand integrated India sportswear portfolios, and D2C and digital-first sportswear brands including HRX, Cultsport, Blissclub, BoStreet, Alcis Sports, Performax, Wrogn Active, and Aurelia Active scale athleisure pipelines, the sports apparel market in India is evolving into a consumer-led, performance-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Sports Apparel Market

- The India sports apparel market size is projected to grow from USD 4.8 Billion in 2025 to USD 10.2 Billion by 2032, registering a strong CAGR of 11.5%, driven by accelerating athleisure mainstreaming, rising women’s and kids’ sports apparel demand, and the structural shift toward digital-first sportswear distribution.

- T-shirts and track pants dominate the Indian sports apparel industry, accounting for over 48% to 52% of total revenue in 2025, supported by mass and mid-range consumption across men, women, and kids, with PUMA Sports India, Nike India, Adidas India, and Decathlon scaling India-specific assortments.

- Women’s athleisure and yoga wear is emerging as the fastest growing category in the Indian sports apparel industry, expected to grow at 16% to 19% annually as urban Indian women shift toward dermatologist-tested, performance-led, and design-forward activewear across Tier I and Tier II cities.

- Online and quick commerce channels are scaling rapidly in the sports apparel market in India, contributing over 28% to 32% of total revenue in 2025, driven by Myntra, Amazon, Flipkart, Tata CLiQ, AJIO, Nykaa Fashion, Blinkit, and Zepto, structurally expanding the digital sportswear opportunity.

- Rising investments by global sportswear majors PUMA, Nike, Adidas, Decathlon, ASICS, Reebok, Skechers, and Under Armour, plus Indian D2C sportswear brands HRX, Cultsport, Blissclub, BoStreet, Alcis Sports, Performax, and Wrogn Active in sportswear R&D, contract manufacturing, and India-specific athleisure platforms are supporting the India sports apparel market forecast 2032.

Key Market Drivers: India Sports Apparel Market

Rising Fitness Awareness, Gym and Yoga Participation, and Athleisure-as-Everyday Trend Driving Sports Apparel Consumption

Growth in the India sports apparel market is being driven by rising fitness awareness, rapid expansion of gym, yoga, running, and cricket participation, and the mainstreaming of athleisure as everyday wear across Indian metros. Organised gym and fitness centre footfall in India has grown at a CAGR of 13% to 15% between 2021 and 2025, with chains such as Cult.fit, Gold’s Gym India, Anytime Fitness, Snap Fitness, and Talwalkars driving demand for performance leggings, sports bras, gym T-shirts, and tracksuits. Yoga participation has scaled rapidly in metro and Tier II Indian cities, supported by International Yoga Day, Patanjali Yogpeeth, and digital fitness platforms. Urban Indian consumers now wear athleisure for 35% to 40% of casual occasions, blurring the line between workout and everyday wear. These trends are creating strong, multi-year structural pull-through demand across the India sports apparel market through 2032.

Source: Market Research Outlook

Rapid Expansion of E-Commerce, D2C Sportswear Brands, and Quick Commerce Reshaping Sports Apparel Distribution

Rapid scaling of e-commerce, D2C sportswear brands, and quick commerce is a major catalyst for the Indian sports apparel industry, with online channels expected to account for over 30% of sports apparel sales by 2027, up from less than 14% in 2021. Marketplaces including Myntra, Amazon, Flipkart, Tata CLiQ, AJIO, and Nykaa Fashion are driving discovery and trial of premium sportswear, while quick commerce platforms such as Blinkit, Zepto, Instamart, and BB Now are accelerating impulse activewear category turnover. D2C-first sportswear brands including HRX, Cultsport, Blissclub, BoStreet, Alcis Sports, Performax, and Wrogn Active are leveraging influencer-led marketing, performance media, and athlete endorsements to acquire customers. Established sports apparel majors including Nike India, Adidas India, PUMA Sports India, ASICS, Decathlon, Skechers, and Under Armour have also ramped up direct online stores, exclusive online drops, and influencer ecosystems, reinforcing the omnichannel transformation of the segment through 2032.

Source: Market Research Outlook

Government-Led Khelo India, Fit India, and Growing Women’s and Kids’ Sports Participation Fuelling Sports Apparel Demand

Government-led sports promotion initiatives are a major catalyst for the India sports apparel market, with the Khelo India scheme covering over 1,000 academies and 35 lakh participants by 2025, and Fit India Movement reaching millions of citizens through schools, gyms, and digital fitness campaigns. Women’s sports participation in India has scaled rapidly, with growing visibility of Indian women’s cricket, kabaddi, hockey, badminton, and football teams driving structural demand for women’s sports bras, leggings, performance tops, and modest activewear. Kids’ sports apparel is also growing fast, supported by school-level sports, after-school coaching, and aspirational positioning of cricket and football academies. Combined with rising disposable income in Indian metros, the demographic dividend, and growing parental investment in children’s fitness, these dynamics are structurally expanding the sports apparel market in India across all gender and age cohorts through 2032.

Key Market Challenges: India Sports Apparel Market

High Price Sensitivity in Mass-Market Segments and Intense Competition from Unorganised Local Sports Apparel Brands

The India sports apparel market remains highly price-sensitive, particularly across mass and economy sports apparel segments where T-shirts priced below INR 500 still account for over 45% of unit volume. Intense competition between Nike India, Adidas India, PUMA Sports India, Decathlon, Reebok, ASICS, Skechers, and a fast-growing pool of D2C and local sportswear brands has compressed gross margins across mass T-shirts, track pants, tracksuits, and leggings. Aggressive trade promotions, end-of-season sales, and frequent discounting in modern trade and online channels have made it difficult for new entrants to scale profitably in the Indian sports apparel industry. Local and regional sports apparel brands across Indian cluster towns continue to compete aggressively on price, with unorganised tailoring units, club-uniform contractors, and regional manufacturers anchoring a meaningful share of school and college sports apparel demand.

Counterfeiting and Grey-Market Imports Affecting Branded Sports Apparel Margins and Brand Equity

The sports apparel market in India faces persistent challenges from counterfeiting, grey-market imports, and unauthorised resale, particularly across premium global sportswear brands. Counterfeit Nike, Adidas, PUMA, and Under Armour sports apparel is widely available in unorganised retail clusters in Delhi, Mumbai, Kolkata, Chennai, and several Tier II Indian cities, often priced 60% to 80% below the original. Online marketplaces have also faced ongoing scrutiny on third-party seller authenticity for premium sports apparel. The Indian sports apparel industry has responded with brand-protection programmes, authorised dealer networks, QR-coded authenticity tags, and selective platform partnerships with Myntra, Tata CLiQ Luxury, Nike.com, and Adidas.co.in. Despite this, counterfeit prevalence continues to affect branded sports apparel margins, brand equity, and consumer trust, particularly in mid-range categories.

Raw Material Cost Volatility, Cotton, Polyester, and Elastane Inflation Squeezing Sports Apparel Margins

The India sports apparel market is exposed to volatility in key raw materials including cotton, polyester, viscose, elastane (spandex), nylon, and recycled-PET inputs, alongside trims, dyes, and packaging. Cotton prices in India fluctuated by over 25% between 2022 and 2025, while polyester staple fibre and POY prices remained sensitive to crude-oil and import-duty cycles. Sports apparel manufacturers operating across Tirupur, Ludhiana, Bengaluru, NCR, and Surat face cost-push inflation that is difficult to fully pass through to consumer MRP, particularly in mass and economy sports apparel categories. Sea freight, road freight, and last-mile logistics costs across the Indian sports apparel industry rose by 10% to 15% post 2022, while quick commerce service fees and platform commissions add a structural margin overhang. Cost engineering, vertical integration, fabric innovation, and selective premiumisation are emerging as critical responses.

Key Market Trends: India Sports Apparel Market

Athleisure Mainstreaming, Blurring Lines Between Workout and Everyday Sports Apparel Wear

The India sports apparel market is undergoing a clear shift toward athleisure mainstreaming, with athleisure expected to account for over 45% of premium sports apparel by 2030. Indian consumers increasingly wear leggings, joggers, tracksuits, oversized T-shirts, performance hoodies, and stylised sports bras for casual occasions, workplace-casual settings, and travel, blurring the traditional line between workout wear and everyday wear. D2C sportswear brands such as HRX, Cultsport, Blissclub, BoStreet, and Wrogn Active have built propositions around athleisure-first storytelling, while global majors including Nike India, Adidas India, PUMA Sports India, and ASICS have launched India-specific athleisure capsules, lifestyle drops, and limited-edition athlete collaborations. Layered athleisure styling, oversized fits, and fashion-forward colourways are accelerating premium athleisure spend in metro Indian cities, reinforcing the structural mainstreaming of athleisure across the segment through 2032.

D2C Sportswear Brands, Influencer-Led Marketing, and Quick Commerce Growth in the India Sports Apparel Market

A clear move toward D2C-first sportswear, influencer-led marketing, and quick commerce is reshaping the India sports apparel market, particularly in the premium and mass-premium tiers. HRX (Myntra and Hrithik Roshan), Cultsport (Cult.fit), Blissclub, BoStreet (Reliance), Alcis Sports, Performax, Wrogn Active, and Aurelia Active have scaled annual sportswear revenues into the hundreds of crores by combining D2C websites, marketplaces, and athlete-led storytelling. Sports influencer marketing in India has scaled rapidly, with cricket, football, fitness, and yoga creators driving discovery on Instagram, YouTube, and short-video platforms. Quick commerce platforms now contribute 5% to 8% of online sports apparel sales in India, with sports T-shirts, leggings, sports bras, and gym accessories as fast-rotating SKUs. Established sportswear majors have responded with influencer ecosystems, digital-first launches, and creator-led drops to defend share in the Indian sports apparel industry.

Sustainable Activewear, Recycled Polyester, and Clean Fashion Gaining Traction Across the Sports Apparel Market

A wave of sustainability, recycled-polyester, and clean fashion innovation is reshaping the sports apparel market in India. Recycled-PET polyester, ocean-plastic-derived fabrics, organic cotton, bamboo blends, and waterless dyeing technologies are increasingly important to Indian sportswear consumers, with over 36% of urban Indian sports apparel buyers in 2025 willing to pay a premium for sustainable activewear. Nike India launched Move to Zero capsules, Adidas India expanded Parley for the Oceans collections featuring recycled-PET, PUMA scaled the RE:FIBRE programme, and Decathlon committed to eco-design across over 70% of its sports apparel range by 2026. Indian D2C sportswear brands including Cultsport, Blissclub, and HRX have committed to recycled-content fabrics and circular-design initiatives. These developments are reinforcing the India sports apparel market forecast 2032 across both premium and mass-premium categories.

Segmental Insights: India Sports Apparel Market

By Product Type: T-Shirts and Track Pants Dominate While Leggings, Sports Bras and Athleisure Grow Fastest

T-shirts and track pants together dominate the India sports apparel market, accounting for an estimated 48% to 52% of total sports apparel revenue in 2025, supported by mass and mid-range consumption across men, women, and kids. Tracksuits and jackets contribute another 12% to 14%, anchored in cricket, football, and gym categories. Leggings, tights, and sports bras together account for 14% to 16% of the sports apparel market in India and are the fastest growing product categories, expanding at 16% to 19% annually, driven by women’s athleisure adoption and yoga-led demand. Performance outerwear, including running jackets, windcheaters, and cycling gear, contributes 6% to 8%, with rising adoption in Tier I metros. Sports innerwear, sports socks, and accessories together represent another 8% to 10% of the Indian sports apparel industry.

By Sport and Activity: Cricket, Running, and Yoga Lead, Gym and Fitness Drive Premium Growth

Cricket-led sports apparel leads consumption in the sports apparel market in India, accounting for over 22% of revenue in 2025, anchored by team jerseys, training apparel, IPL-driven licensed merchandise, and school-level cricket. Running and outdoor sports apparel contributes another 18% to 20%, while yoga and studio activewear has scaled rapidly to 14% to 16% of revenue, supported by women’s yoga adoption and digital wellness platforms. Gym and fitness apparel contributes 16% to 18% and is among the highest-margin sub-categories, driven by premium T-shirts, leggings, joggers, and performance hoodies. Football, basketball, tennis, badminton, cycling, and swimming together account for 18% to 22% of the segment, with growth supported by football academies, the Indian Super League, and pickleball and racquet sports emerging in metro Indian cities.

By Distribution Channel: Online and Specialty Sports Stores Outpace Traditional Multi-Brand Retail

Specialty sports stores and brand exclusive outlets together account for the largest share of the India sports apparel market at 32% to 36%, anchored by Decathlon, Nike, Adidas, PUMA, ASICS, Skechers, and Reebok-branded stores across Indian metros. Online and quick commerce channels follow at 28% to 32%, led by Myntra, Amazon, Flipkart, Tata CLiQ, AJIO, Nykaa Fashion, Blinkit, and Zepto, and represent the fastest growing channels at over 20% annual growth. Hypermarkets, supermarkets, and department stores including Reliance Retail, Shoppers Stop, Lifestyle, Westside, Pantaloons, and Central contribute another 18% to 22%. Multi-brand sports retail chains and direct-corporate sales together represent 14% to 18% of revenue across the Indian sports apparel industry.

Regional Insights: India Sports Apparel Market

Regional analysis of the India sports apparel market shows that North India and West India collectively account for approximately 54% to 58% of total sports apparel consumption, driven by Delhi NCR, Punjab, Haryana, Uttar Pradesh, Rajasthan, Maharashtra, and Gujarat, supported by larger Tier I and Tier II urban clusters, higher disposable income, stronger modern trade and online sports apparel penetration, and dense gym and yoga ecosystem density. South India contributes around 25% to 28% of demand, led by Karnataka, Tamil Nadu, Telangana, and Kerala, supported by deep cricket, running, and badminton participation in Bengaluru, Chennai, and Hyderabad. East India and Central India together account for 16% to 20% of demand, supported by West Bengal, Odisha, Bihar, Madhya Pradesh, Chhattisgarh, and Jharkhand, where mass and value sports apparel continue to anchor demand. Tirupur, Ludhiana, Bengaluru, Delhi NCR, and Surat remain the largest sports apparel manufacturing and sourcing hubs. In 2025, Nike India, Adidas India, PUMA Sports India, Decathlon, ASICS, Skechers, HRX, and Cultsport expanded regional distribution, brand stores, and influencer-led marketing across Indian states, reinforcing regional supply hubs and supporting closer execution of mass and premium sports apparel orders.

Recent Developments: India Sports Apparel Market

- The India sports apparel market witnessed strong momentum across product launches, premiumisation, and digital-first expansion during 2024 and 2025. PUMA Sports India, the consistent market leader, crossed over INR 4,000 crore in annual India revenue and deepened cricket and football endorsements with the BCCI, Royal Challengers Bengaluru, and the Indian football team. Nike India and Adidas India expanded India-specific running, training, and athleisure collections, while Decathlon scaled its India footprint to over 130 stores and continued aggressive own-brand sports apparel growth across all major price tiers.

- Indian sportswear majors have deepened India-focused product innovation and capacity expansion. HRX (Myntra and Hrithik Roshan) scaled annual sportswear revenues past INR 1,200 crore, Cultsport (Cult.fit) and Blissclub continued double-digit growth in athleisure and women’s activewear, BoStreet (Reliance) expanded multi-brand sports apparel retail, and Alcis Sports, Performax, Wrogn Active, and Aurelia Active scaled mass-premium sports apparel. Reebok, under Aditya Birla Fashion and Retail’s management, accelerated India-specific store rollouts and licensed-product launches.

- Digital-first and D2C sportswear momentum has gained strong traction in the sports apparel market in India. D2C-first athleisure brands such as Blissclub raised significant equity funding and scaled women’s activewear SKUs, Cultsport scaled across Myntra, Tata CLiQ, and Cult.fit retail, while HRX continued to lead Myntra athleisure rankings. Strategic partnerships between domestic sports apparel manufacturers, IPL franchises, Indian Super League clubs, and influencer ecosystems are positioning India as one of the most actively scaling sports apparel markets globally, reinforcing the India sports apparel market forecast 2032.

Key Market Players: India Sports Apparel Market

- PUMA Sports India Pvt. Ltd.

- Nike India Pvt. Ltd.

- Adidas India Marketing Pvt. Ltd.

- Decathlon Sports India Pvt. Ltd.

- ASICS India Pvt. Ltd.

- Reebok India Company (Aditya Birla Fashion and Retail Limited)

- Skechers South Asia Pvt. Ltd.

- Under Armour India

- HRX (Myntra Designs Pvt. Ltd.)

- Cultsport (Cure.fit Healthcare Pvt. Ltd.)

- Blissclub (The Conscious Closet Pvt. Ltd.)

- Alcis Sports Pvt. Ltd.

- Nivia Sports (Freewill Sports Pvt. Ltd.)

Report Scope

In this report, the India Sports Apparel Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- T-Shirts & Tops

- Pants & Shorts

- Tracksuits & Jackets

- Leggings & Tights

- Sports Bras

- Sports Innerwear

- Performance Outerwear

- Others

- By Sport / Activity

- Running

- Yoga

- Gym & Fitness

- Cricket

- Football

- Basketball

- Tennis & Badminton

- Cycling

- Swimming

- Others

- By Gender

- Men

- Women

- Kids

- Unisex

- By Fabric Type

- Polyester

- Cotton

- Cotton-Polyester Blend

- Polyester-Elastane Blend

- Recycled & Sustainable Fabrics

- Bamboo & Organic Cotton

- Others

- By Price Range

- Premium

- Mid-Range

- Mass

- By Application

- Performance Sports

- Athleisure

- Active Outdoor

- Yoga & Studio

- Casual Activewear

- By End-User

- Individual / Personal Use

- Institutional (Schools, Colleges)

- Corporate (Offices, IT Campuses)

- Sports Clubs & Academies

- By Distribution Channel

- Specialty Sports Stores

- Hypermarket / Supermarket

- Department Stores

- Online / E-commerce

- Brand Exclusive Outlets

- Direct Sales

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the Indian sports apparel industry, including business overview, sports apparel product portfolio (T-shirts, leggings, tracksuits, sports bras, performance outerwear, athleisure), strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional sports apparel players (up to five companies), including emerging Indian D2C activewear brands, specialty yoga and athleisure producers, sports merchandising specialists, or niche state-level sports apparel manufacturers.

The India Sports Apparel Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Sport / Activity

- By Gender

- By Fabric Type

- By Price Range

- By Application

- By End-User

- By Distribution Channel

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Sports Apparel Market

- India Sports Apparel Market Insights

- Market Dynamics

- Growth Drivers

- Rising fitness awareness, gym and yoga participation, and athleisure-as-everyday trend driving sports apparel consumption.

- Rapid expansion of e-commerce, D2C sportswear brands, and quick commerce reshaping sports apparel distribution in India.

- Government-led Khelo India and Fit India programmes plus growing women’s and kids’ sports participation fuelling sports apparel demand.

- Restraints

- High price sensitivity in mass-market segments and intense competition from unorganised local sports apparel brands.

- Counterfeiting and grey-market imports affecting branded sports apparel margins and brand equity in India.

- Raw material (cotton, polyester, elastane) cost volatility and supply chain pressures squeezing sports apparel margins.

- Opportunities

- Premiumisation, technical performance fabrics, and sustainable activewear gaining traction across the Indian sports apparel industry.

- Tier II and Tier III city expansion through D2C, modern trade, and influencer-led marketing in the sports apparel market in India.

- Women’s athleisure, modest activewear, and adaptive sports apparel opening new long-term value pools.

- Challenges

- Fragmented sizing, fit, and quality standards across Indian consumers limiting scale in branded sports apparel.

- Slow penetration of premium technical sports apparel beyond Tier I metros limiting near-term growth.

- Climate variability and seasonality across Indian regions affecting fabric performance and demand patterns.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (cotton, polyester, viscose, elastane, recycled-PET, dyes, trims)

- Fabric & Knitting Mills (Tirupur, Ludhiana, Surat, NCR knitwear hubs)

- Sports Apparel Manufacturers & OEMs (cut-make-trim, contract manufacturing, brand factories)

- Quality Control, R&D & Testing Laboratories (BIS, REACH, Oeko-Tex, AATCC standards)

- Distributors, Wholesalers & Modern Trade Partners (Reliance Retail, Shoppers Stop, Lifestyle, Westside)

- E-commerce, D2C & Quick Commerce Platforms (Myntra, Amazon, Flipkart, Tata CLiQ, AJIO, Blinkit, Zepto)

- Sportswear Brand Owners & Sports Goods Majors (Nike India, Adidas India, PUMA Sports India, Decathlon)

- Specialty Sports Retail & Brand Exclusive Outlets (Nike Stores, adidas Originals, PUMA, Reebok, ASICS, Skechers)

- Sports Clubs, Academies & Institutional Buyers (school uniforms, IPL franchises, ISL clubs, athletic federations)

- End-Users (Individual / Personal Use, Institutional, Corporate, Sports Clubs & Academies)

- India Sports Apparel Market: Regulatory Framework

- India Sports Apparel Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Million Units)

- Market Share & Forecast

- By Product Type

- T-Shirts & Tops

- Pants & Shorts

- Tracksuits & Jackets

- Leggings & Tights

- Sports Bras

- Sports Innerwear

- Performance Outerwear

- Others

- By Sport / Activity

- Running

- Yoga

- Gym & Fitness

- Cricket

- Football

- Basketball

- Tennis & Badminton

- Cycling

- Swimming

- Others

- By Gender

- Men

- Women

- Kids

- Unisex

- By Fabric Type

- Polyester

- Cotton

- Cotton-Polyester Blend

- Polyester-Elastane Blend

- Recycled & Sustainable Fabrics

- Bamboo & Organic Cotton

- Others

- By Price Range

- Premium

- Mid-Range

- Mass

- By Application

- Performance Sports

- Athleisure

- Active Outdoor

- Yoga & Studio

- Casual Activewear

- By End-User

- Individual / Personal Use

- Institutional (Schools, Colleges)

- Corporate (Offices, IT Campuses)

- Sports Clubs & Academies

- By Distribution Channel

- Specialty Sports Stores

- Hypermarket / Supermarket

- Department Stores

- Online / E-commerce

- Brand Exclusive Outlets

- Direct Sales

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Sports Apparel Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- PUMA Sports India Pvt. Ltd.

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- Nike India Pvt. Ltd.

- Adidas India Marketing Pvt. Ltd.

- Decathlon Sports India Pvt. Ltd.

- ASICS India Pvt. Ltd.

- Reebok India Company (Aditya Birla Fashion and Retail Limited)

- Skechers South Asia Pvt. Ltd.

- Under Armour India

- HRX (Myntra Designs Pvt. Ltd.)

- Cultsport (Cure.fit Healthcare Pvt. Ltd.)

- Blissclub (The Conscious Closet Pvt. Ltd.)

- Alcis Sports Pvt. Ltd.

- Nivia Sports (Freewill Sports Pvt. Ltd.)

- Other Prominent Players

- PUMA Sports India Pvt. Ltd.

- Market Size & Forecast, 2021-2032

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India sports apparel market and what is its growth forecast?

Ans: India sports apparel market is projected to grow from USD 4.8 Billion in 2025 to USD 10.2 Billion by 2032, at 11.5% CAGR, driven by athleisure mainstreaming, fitness growth, D2C sportswear, and rising women's activewear demand.

2. Which segments are driving demand in the India sports apparel market?

Ans: T-shirts and track pants lead with 48% to 52% revenue share, supported by mass and mid-range consumption. Women's athleisure and yoga wear is fastest growing at 16% to 19% annually, driven by urban Indian women.

3. What are the key drivers of growth in the India sports apparel market?

Ans: Key drivers include rising fitness awareness, gym and yoga participation, athleisure mainstreaming, rapid expansion of D2C sportswear and quick commerce, and government-led Khelo India and Fit India boosting women's and kids' sports apparel demand.

4. Which regions are driving growth in the India sports apparel market?

Ans: North and West India lead with 54% to 58% of demand, led by Delhi NCR, Maharashtra, Gujarat, Punjab, and Uttar Pradesh. South India contributes 25% to 28%, anchored by Karnataka, Tamil Nadu, Telangana, and Kerala.

5. What are the latest trends in the India sports apparel market?

Ans: Latest trends include athleisure mainstreaming, women's activewear growth, D2C sportswear and influencer-led marketing, quick commerce, sustainable recycled-polyester fabrics, and rising adoption of premium performance-led sportswear across cricket, running, yoga, and gym categories.

Frequently Asked Questions

1. How large is the India sports apparel market and what is its growth forecast?

Ans: India sports apparel market is projected to grow from USD 4.8 Billion in 2025 to USD 10.2 Billion by 2032, at 11.5% CAGR, driven by athleisure mainstreaming, fitness growth, D2C sportswear, and rising women's activewear demand.

2. Which segments are driving demand in the India sports apparel market?

Ans: T-shirts and track pants lead with 48% to 52% revenue share, supported by mass and mid-range consumption. Women's athleisure and yoga wear is fastest growing at 16% to 19% annually, driven by urban Indian women.

3. What are the key drivers of growth in the India sports apparel market?

Ans: Key drivers include rising fitness awareness, gym and yoga participation, athleisure mainstreaming, rapid expansion of D2C sportswear and quick commerce, and government-led Khelo India and Fit India boosting women's and kids' sports apparel demand.

4. Which regions are driving growth in the India sports apparel market?

Ans: North and West India lead with 54% to 58% of demand, led by Delhi NCR, Maharashtra, Gujarat, Punjab, and Uttar Pradesh. South India contributes 25% to 28%, anchored by Karnataka, Tamil Nadu, Telangana, and Kerala.

5. What are the latest trends in the India sports apparel market?

Ans: Latest trends include athleisure mainstreaming, women's activewear growth, D2C sportswear and influencer-led marketing, quick commerce, sustainable recycled-polyester fabrics, and rising adoption of premium performance-led sportswear across cricket, running, yoga, and gym categories.