India Solar Rooftop Market, By Solar Panel Type (Monocrystalline, Polycrystalline, Bifacial, Thin-Film, BIPV, Others); By Connectivity Type (On-Grid, Off-Grid, Hybrid); By Component (Solar Modules, Inverters, Mounting Structures, Battery Storage, Cables & BoS, Monitoring Systems); By Capacity (Below 3 kW, 3 to 10 kW, 10 to 100 kW, 100 kW to 1 MW, Above 1 MW); By Application (Net Metering, Captive Consumption, Power Purchase Agreement, Group / Virtual Net Metering, Self-Consumption); By End-User (Residential, Commercial, Industrial, Government & Institutional, Educational); By Business Model (CAPEX, OPEX / RESCO, Hybrid Model, Direct EPC, Online Aggregators); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Solar Rooftop Market: PM Surya Ghar Yojana and C&I Decarbonisation Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

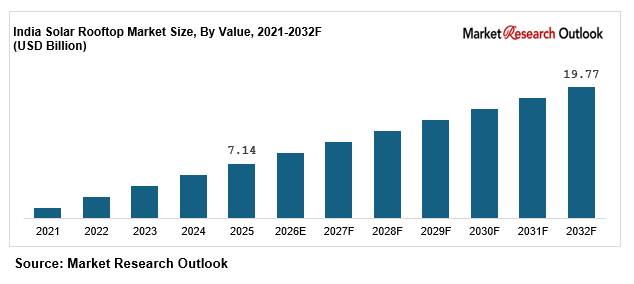

| Market Size (2025) | USD 7.14 Billion |

| CAGR (2026-2032) | 15.6% |

| Leading Segment | Residential Rooftop Solar (On-Grid Monocrystalline) |

| Fastest Growing Segment | Commercial & Industrial (C&I) Rooftop Solar |

| Market Size (2032) | USD 19.77 Billion |

Source: Market Research Outlook

Market Overview: India Solar Rooftop Market

The India solar rooftop market size is witnessing rapid expansion, driven by the world’s largest domestic rooftop solar scheme PM Surya Ghar Muft Bijli Yojana, falling solar PV module prices, accelerated commercial and industrial rooftop solar adoption, expanding state-level net metering coverage, and major manufacturing capacity additions by Indian solar majors. Valued at USD 7.14 billion in 2025 and projected to reach USD 19.77 billion by 2032, growing at a CAGR of 15.6%, the India solar rooftop market growth is being fuelled by strong residential demand under PM Surya Ghar Yojana, rising C&I procurement tied to corporate decarbonisation and Time-of-Day tariff regimes, and growing institutional adoption across schools, hospitals, and government buildings. Residential rooftop solar leads consumption, while the commercial and industrial segment is emerging as the fastest growing category. Tightening ESG mandates, RE100 commitments by Indian corporates, and the national 500 GW renewable energy target by 2030 are reshaping the supply landscape. As domestic majors including Tata Power Solar, Adani Solar, Waaree Energies, Vikram Solar, and Goldi Solar expand integrated module-to-installation capacity, and rooftop solar EPC players including Amplus Solar, CleanMax, Mahindra Susten, and Jakson scale C&I project pipelines, the India solar rooftop market is evolving into a policy-led, technology-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Solar Rooftop Market

- The India solar rooftop market size is projected to grow from USD 7.14 billion in 2025 to USD 19.77 billion by 2032, registering a strong CAGR of 15.6%, driven by accelerated PM Surya Ghar Yojana-led residential adoption, rising C&I rooftop solar uptake, and the structural shift toward decentralised clean energy generation.

- Residential rooftop solar dominates the India solar rooftop market, accounting for over 45% of total installed capacity in 2025, driven by PM Surya Ghar Muft Bijli Yojana subsidies of up to INR 78,000 per household, falling system costs, and rising electricity tariffs across urban and semi-urban India.

- Commercial and industrial (C&I) rooftop solar is emerging as the fastest growing segment in the India solar rooftop market, expected to grow at 18 to 22% annually as Time-of-Day tariffs, RE100 commitments, ESG-led procurement, and corporate decarbonisation mandates reshape sourcing strategies.

- Rapid scaling of PM Surya Ghar Muft Bijli Yojana, with over 16 lakh installations completed by mid-2025 and a target of one crore households by FY27, is structurally expanding the India solar rooftop market across residential, government, and Model Solar Village categories.

- Rising investments by domestic solar majors such as Tata Power Solar, Adani Solar, Waaree Energies, Vikram Solar, and Goldi Solar in module manufacturing, cell capacity, and integrated rooftop solar EPC are strengthening local supply and supporting the India solar rooftop market forecast 2032.

Key Market Drivers: India Solar Rooftop Market

PM Surya Ghar Muft Bijli Yojana and Rising Government Subsidies Driving Residential Rooftop Solar Adoption

Growth in the India solar rooftop market is being driven by the rapid scaling of PM Surya Ghar Muft Bijli Yojana (PMSGMBY), the world’s largest domestic rooftop solar scheme, launched in February 2024 with a financial outlay of INR 75,021 crore. The scheme targets one crore households by FY27 and offers Central Financial Assistance of up to INR 78,000 per household for systems above 3 kW, along with collateral-free loans at 7% interest. By mid-2025, over 16 lakh installations had been completed, with monthly registrations crossing 70,000 households. Per-capita rooftop solar penetration in India remains below 5% of addressable residential rooftops, indicating significant long-term headroom for growth. Government targets, falling system costs of INR 35,000 to 45,000 per kW, and electricity bill savings of up to 100% for 28% of beneficiaries are creating strong structural pull-through demand across the India solar rooftop market.

Falling Solar PV Module Prices and Improving Cost Economics Strengthening Rooftop Solar Returns

The India solar rooftop market is benefiting from a sustained decline in solar PV module prices, which have fallen by over 80% between 2010 and 2024 according to IRENA, alongside continued cost reductions in inverters, mounting structures, and balance of system components. Average residential rooftop solar system costs in India now range between INR 35,000 and 45,000 per kW, with payback periods compressed to 4 to 5 years for residential installations and 3 to 4 years for C&I projects. Domestic module manufacturing capacity has scaled rapidly, with Indian module capacity exceeding 80 GW by 2025, led by Waaree Energies, Adani Solar, Vikram Solar, Tata Power Solar, and Goldi Solar. Approved List of Models and Manufacturers (ALMM) policy and Basic Customs Duty on imports have further strengthened domestic supply, supporting price competitiveness across the India solar rooftop market.

Corporate Decarbonisation, ESG Mandates, and Time-of-Day Tariffs Driving C&I Rooftop Solar Demand

Rapid growth in commercial and industrial rooftop solar is a major catalyst for the India solar rooftop market, with the C&I segment projected to grow at 18 to 22% annually through 2032. Corporate decarbonisation commitments under RE100, science-based targets, and Scope 2 emission reductions are driving large enterprises and MSMEs toward captive rooftop solar consumption. The Central Electricity Regulatory Commission’s Time-of-Day (ToD) tariff rollout in 2025 has increased peak-hour electricity costs for commercial users, accelerating rooftop solar adoption to hedge against rising grid power costs. Leading C&I rooftop solar EPC players such as Amplus Solar, CleanMax Enviro Energy, Mahindra Susten, ReNew Power, and Jakson have scaled OPEX and RESCO project pipelines, with the C&I segment alone representing an estimated 15 GW addressable opportunity within Indian MSMEs. Government infrastructure programs combined with corporate ESG procurement are structurally expanding India solar rooftop market growth across all major end-user categories through 2032.

Key Market Challenges: India Solar Rooftop Market

High Upfront Capital Cost and Limited Access to Affordable Financing for Residential Consumers

The India solar rooftop market continues to face challenges around high upfront capital costs and limited access to affordable financing for residential consumers, with a typical 3 kW residential system costing INR 1.6 lakh to 2.2 lakh before subsidies. While PM Surya Ghar Muft Bijli Yojana provides up to INR 78,000 in subsidy and the JanSamarth portal offers loans at 7% interest, application-to-installation conversion under PMSGMBY remains at only 22.7% as of mid-2025, reflecting bottlenecks in financing access, vendor capacity, and approval processes. Banks and NBFCs continue to be cautious in extending unsecured rooftop solar loans to lower-income households, while EMI-linked financing for systems above 3 kW remains underdeveloped. India’s continued dependence on traditional capital expenditure models for residential rooftop solar limits adoption among middle-income and rural households across the India solar rooftop market.

Net Metering Policy Variations and DISCOM Approval Delays Across States

The India solar rooftop market faces structural complexity from variations in net metering policies, capacity caps, and DISCOM approval timelines across different states. While states such as Gujarat, Maharashtra, Karnataka, and Rajasthan have progressive net metering frameworks with capacity limits raised to 1 MW, others maintain restrictive caps and lengthy technical feasibility processes. Average DISCOM approval timelines range between 30 to 90 days, and grid synchronisation delays have emerged as a key bottleneck in PMSGMBY rollout. Differential treatment of group net metering, virtual net metering, and gross metering across states creates operational complexity for rooftop solar EPC players such as Tata Power Solar, Amplus Solar, CleanMax, and Mahindra Susten operating pan-India. While the Ministry of New and Renewable Energy has standardised processes for systems below 10 kW, regulatory fragmentation remains a near-term challenge for the India solar rooftop market.

Roof Space Constraints, Structural Limitations, and Shading in Dense Urban Areas

The India solar rooftop market faces practical constraints around roof space availability, structural load-bearing capacity, and shading challenges in dense urban areas. Indian cities such as Mumbai, Delhi, Bengaluru, Chennai, and Kolkata have significant roof area constraints in high-rise residential and commercial buildings, with average usable rooftop area per household often below 200 square feet. Structural limitations of older buildings, water-tank obstructions, lift rooms, and adjacent building shadows reduce the effective generation potential of installed systems by 10 to 25%. Multi-tenant residential societies face additional governance complexity in approving rooftop solar installations and allocating generated power. Bifacial modules, building-integrated photovoltaics (BIPV), and high-efficiency N-type TOPCon panels are emerging as solutions, but premium pricing and limited installer capability remain barriers to widespread adoption across the India solar rooftop market.

Key Market Trends: India Solar Rooftop Market

Rapid Adoption of N-type TOPCon, Bifacial, and High-Efficiency Solar Modules in India

The India solar rooftop market is undergoing a clear technology shift toward N-type TOPCon, bifacial, and high-efficiency solar modules, with these advanced technologies expected to capture over 55% of new rooftop solar installations by 2027. N-type TOPCon modules deliver efficiencies of 22 to 23%, compared to 19 to 21% for traditional Mono PERC, while bifacial modules add 5 to 15% additional generation through reflected light capture. Leading domestic manufacturers including Vikram Solar, Waaree Energies, Adani Solar, Goldi Solar, and Premier Energies have scaled N-type TOPCon and bifacial production capacity through 2024 and 2025. Building-Integrated Photovoltaics (BIPV) is also gaining traction, particularly in metro cities such as Mumbai and Bengaluru where rooftop space is limited, with companies like Waaree and Jakson offering BIPV solutions for green-certified commercial buildings. This technology transition is reinforcing the India solar rooftop market forecast 2032 across both residential and C&I categories.

Growth of OPEX, RESCO Business Models and Third-Party Financing in the India Solar Rooftop Market

A clear shift toward OPEX, RESCO (Renewable Energy Service Company), and third-party financing business models is reshaping the India solar rooftop market, particularly in the C&I segment. Under OPEX and RESCO models, rooftop solar developers fund the entire system and supply electricity to consumers under long-term Power Purchase Agreements (PPAs) of 15 to 25 years at tariffs typically 20 to 40% below grid power costs. Leading RESCO and OPEX players including Amplus Solar, CleanMax Enviro Energy, Mahindra Susten, ReNew Power, and Tata Power Solar have built combined operational portfolios exceeding 4 GW of contracted C&I rooftop solar capacity. Online aggregators and digital platforms such as PM Surya Ghar national portal, vendor marketplaces, and EMI-linked financing platforms are also reducing customer acquisition costs and accelerating rooftop solar adoption across both residential and commercial segments of the India solar rooftop market.

Capacity Expansion by Domestic Solar Module Manufacturers and Vertical Integration

A wave of domestic capacity expansion and vertical integration is reshaping the India solar rooftop market supply landscape. Combined India-focused capital expenditure announcements in solar module, cell, and wafer manufacturing exceeded USD 8 billion across 2023 to 2025. Waaree Energies expanded module capacity to over 13 GW, Adani Solar scaled integrated cell and module capacity to over 4 GW, Vikram Solar commissioned new TOPCon production lines, Tata Power Solar expanded its Tirunelveli facility, and Goldi Solar grew capacity to 14 GW. Approved List of Models and Manufacturers (ALMM) policy, Production Linked Incentive (PLI) scheme allocations exceeding INR 24,000 crore, and Basic Customs Duty on imports have structurally favoured domestic supply. Combined with PM Surya Ghar Yojana driving residential demand and C&I procurement scaling rapidly, these developments are reinforcing the India solar rooftop market forecast 2032 across the entire value chain.

Segmental Insights: India Solar Rooftop Market

By End-User: Residential Segment Dominates the India Solar Rooftop Market

The residential end-user segment dominates the India solar rooftop market, accounting for an estimated 45 to 48% of total installed capacity, driven by the rapid scaling of PM Surya Ghar Muft Bijli Yojana, rising electricity tariffs, and improving rooftop solar economics. Monocrystalline modules are the dominant technology within this segment, with on-grid net metering systems capturing over 80% of residential installations. The commercial segment contributes another 22 to 25% of demand, driven by retail chains, IT parks, hotels, and office complexes adopting rooftop solar to manage Time-of-Day tariff exposure. The industrial segment accounts for 20 to 22%, led by textiles, chemicals, food processing, and engineering MSMEs. In 2025, leading rooftop solar players including Tata Power Solar, Adani Solar, Waaree Energies, Amplus Solar, and CleanMax scaled up residential and C&I rooftop solar deployment under PMSGMBY and corporate ESG mandates, reinforcing segment dominance in the India solar rooftop market.

By Solar Panel Type: Monocrystalline Leads While Bifacial and TOPCon Grow Fastest

Monocrystalline solar panels lead the India solar rooftop market product landscape, accounting for approximately 65 to 68% of total rooftop solar installations, driven by their superior efficiency, compact form factor, and improving cost economics. Polycrystalline modules contribute another 18 to 20%, primarily in budget-conscious residential and rural installations. Bifacial and N-type TOPCon panels are the fastest growing categories within the India solar rooftop market, expanding at 25 to 30% annually, driven by superior efficiency of 22 to 23%, additional rear-side generation, and growing adoption in C&I and premium residential installations. Thin-film and BIPV technologies together account for 4 to 6% of the market, with BIPV expected to grow rapidly through 2032 in metro markets. Leading domestic manufacturers including Waaree Energies, Adani Solar, Vikram Solar, Tata Power Solar, and Goldi Solar have aligned product portfolios to this technology mix, driving high-efficiency module adoption across the India solar rooftop market.

Regional Insights: India Solar Rooftop Market

Regional analysis of the India solar rooftop market shows that West India and North India collectively account for approximately 55 to 60% of total rooftop solar installed capacity, driven by Gujarat (which alone contributes 29% of total India rooftop solar capacity), Maharashtra (Mumbai, Pune industrial belt), Rajasthan, Haryana, and Uttar Pradesh, supported by progressive state net metering policies and strong solar irradiance levels. South India contributes around 22 to 25% of demand, led by Karnataka, Tamil Nadu, Telangana, and Kerala, supported by industrial and commercial rooftop solar adoption in IT and manufacturing clusters around Bengaluru, Chennai, Hyderabad, and Coimbatore. Central and East India together account for 15 to 18% of demand, supported by Madhya Pradesh, Chhattisgarh, West Bengal, and Odisha, where PM Surya Ghar Yojana adoption is accelerating. In 2025, capacity additions and EPC operations by Tata Power Solar across Tamil Nadu and Karnataka, Adani Solar in Gujarat, Amplus Solar across pan-India C&I sites, and CleanMax across Maharashtra and Rajasthan reinforced regional supply hubs, supporting closer execution of residential and C&I projects across the India solar rooftop market.

Recent Developments: India Solar Rooftop Market

- The India solar rooftop market witnessed strong momentum in installations and policy progress during 2024 and 2025. India added a record 7.1 GW of rooftop solar capacity in calendar year 2025, representing a 123% year-on-year increase from 3.2 GW in 2024, according to Mercom India Research. PM Surya Ghar Muft Bijli Yojana crossed 16 lakh installations by mid-2025, with the residential segment accounting for 74% of new installations. Cumulative installed rooftop solar capacity in India is projected to reach 25 to 30 GW by FY27 from 17 GW in FY25, growing at an average 33% annually.

- Domestic solar module manufacturers have deepened India-focused capacity expansion. In 2025, Waaree Energies scaled module capacity beyond 13 GW with new TOPCon lines, Adani Solar expanded vertically integrated cell and module capacity to over 4 GW, Vikram Solar commissioned new high-efficiency TOPCon and bifacial production capacity, Tata Power Solar expanded its Tirunelveli plant, and Goldi Solar grew capacity to 14 GW. Premier Energies completed a successful IPO and expanded cell manufacturing. These developments are strengthening domestic supply and supporting the India solar rooftop market forecast 2032.

- C&I rooftop solar momentum has gained strong traction in the India solar rooftop market. In 2025, leading EPC and RESCO players including Amplus Solar (Petronas), CleanMax Enviro Energy, Mahindra Susten, ReNew Power, Jakson Group, and Tata Power Renewable Energy expanded contracted C&I rooftop solar portfolios. Strategic partnerships between domestic module manufacturers and rooftop solar EPC players are positioning India as one of the most actively scaling rooftop solar markets globally, strengthening long-term competitive positioning in the India solar rooftop market forecast 2032.

Key Market Players: India Solar Rooftop Market

- Tata Power Solar Systems Limited

- Adani Solar (Adani Enterprises Limited)

- Waaree Energies Limited

- Vikram Solar Limited

- Goldi Solar Pvt. Ltd.

- Premier Energies Limited

- Mahindra Susten Pvt. Ltd.

- Amplus Solar (Amplus Energy Solutions Pvt. Ltd.)

- CleanMax Enviro Energy Solutions Pvt. Ltd.

- Jakson Group

- ReNew Power Pvt. Ltd.

- Loom Solar Pvt. Ltd.

- RenewSys India Pvt. Ltd.

Report Scope

In this report, the India Solar Rooftop Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

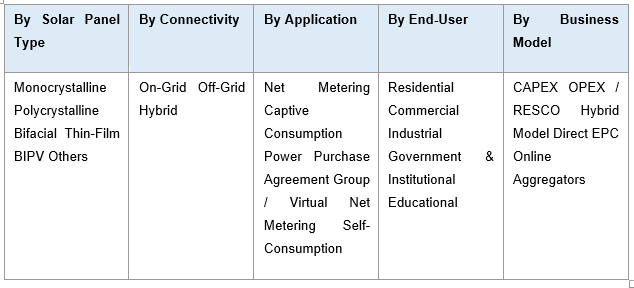

- By Solar Panel Type

- Monocrystalline

- Polycrystalline

- Bifacial

- Thin-Film

- Building-Integrated Photovoltaics (BIPV)

- Others

- By Connectivity Type

- On-Grid

- Off-Grid

- Hybrid

- By Component

- Solar Modules

- Inverters

- Mounting Structures

- Battery Storage

- Cables & Balance of System

- Monitoring Systems

- By Capacity

- Below 3 kW

- 3 to 10 kW

- 10 to 100 kW

- 100 kW to 1 MW

- Above 1 MW

- By Application

- Net Metering

- Captive Consumption

- Power Purchase Agreement (PPA)

- Group / Virtual Net Metering

- Self-Consumption

- By End-User

- Residential

- Commercial

- Industrial

- Government & Institutional

- Educational

- By Business Model

- CAPEX

- OPEX / RESCO

- Hybrid Model

- Direct EPC

- Online Aggregators

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Solar Rooftop Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic solar rooftop EPC firms, specialty BIPV and TOPCon module producers, RESCO and OPEX-model players, or niche state-level installers.

The India Solar Rooftop Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Solar Panel Type

- By Application

- By End-User

- By Connectivity Type

- By Business Model

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Solar Rooftop Market

- India Solar Rooftop Market Insights

- Market Dynamics

- Growth Drivers

- PM Surya Ghar Muft Bijli Yojana and rising government subsidies driving residential rooftop solar adoption.

- Falling solar PV module prices and improving cost economics strengthening rooftop solar returns.

- Corporate decarbonisation, ESG mandates, and Time-of-Day tariffs driving commercial and industrial rooftop solar demand.

- Restraints

- High upfront capital cost and limited access to affordable financing for residential consumers.

- Net metering policy variations and DISCOM approval delays across states creating regulatory complexity.

- Roof space constraints, structural limitations, and shading in dense urban areas limiting effective generation.

- Opportunities

- PM Surya Ghar 1 crore household target creating a massive long-term residential rooftop solar opportunity.

- Battery Energy Storage System (BESS) integration and hybrid rooftop solar solutions opening new value pools.

- Building-Integrated Photovoltaics (BIPV) and premium commercial green-building adoption supporting next-generation growth.

- Challenges

- Slow application-to-installation conversion under PM Surya Ghar Yojana limiting near-term scheme execution.

- Limited skilled workforce for rooftop solar installation, commissioning, and operations & maintenance.

- Grid integration constraints, DISCOM technical feasibility delays, and net metering capacity caps in select states.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (silicon wafers, polysilicon, glass, EVA, backsheets, aluminium frames)

- Solar Cell & Module Manufacturers (Mono PERC, TOPCon, bifacial, BIPV)

- Inverter, Mounting Structure & BoS Suppliers (string, microinverters, central inverters)

- Battery Storage & Energy Management Systems (BESS, smart inverters, monitoring platforms)

- Quality Control, R&D & Testing Laboratories (BIS, MNRE, ALMM, IEC standards)

- Distributors, Dealers & Online Aggregators (B2B and B2C platforms)

- Rooftop Solar EPC Companies (CAPEX, OPEX, RESCO, hybrid models)

- Brand Owners & Solar Service Providers (Tata Power Solar, Adani, Waaree, Vikram, Amplus, CleanMax)

- Installation, O&M & Net Metering Approvals (DISCOMs, system integrators, certified installers)

- End-Users (residential, commercial, industrial, government, educational, institutional)

- India Solar Rooftop Market: Regulatory Framework

- India Solar Rooftop Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (GW Installed Capacity)

- Market Share & Forecast

- By Solar Panel Type

- Monocrystalline

- Polycrystalline

- Bifacial

- Thin-Film

- Building-Integrated Photovoltaics (BIPV)

- Others

- By Connectivity Type

- On-Grid

- Off-Grid

- Hybrid

- By Component

- Solar Modules

- Inverters

- Mounting Structures

- Battery Storage

- Cables & Balance of System

- Monitoring Systems

- By Capacity

- Below 3 kW

- 3 to 10 kW

- 10 to 100 kW

- 100 kW to 1 MW

- Above 1 MW

- By Application

- Net Metering

- Captive Consumption

- Power Purchase Agreement (PPA)

- Group / Virtual Net Metering

- Self-Consumption

- By End-User

- Residential

- Commercial

- Industrial

- Government & Institutional

- Educational

- By Business Model

- CAPEX

- OPEX / RESCO

- Hybrid Model

- Direct EPC

- Online Aggregators

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Solar Rooftop Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Tata Power Solar Systems Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- *(Same Data Pointers Will Be Provided for The Below Companies)*

- Adani Solar (Adani Enterprises Limited)

- Waaree Energies Limited

- Vikram Solar Limited

- Goldi Solar Pvt. Ltd.

- Premier Energies Limited

- Mahindra Susten Pvt. Ltd.

- Amplus Solar (Amplus Energy Solutions Pvt. Ltd.)

- CleanMax Enviro Energy Solutions Pvt. Ltd.

- Jakson Group

- ReNew Power Pvt. Ltd.

- Loom Solar Pvt. Ltd.

- RenewSys India Pvt. Ltd.

- Other Prominent Players

- By Solar Panel Type

- Market Size & Forecast, 2021-2032

** Financial information in case of non-listed companies will be provided as per availability*

*** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable*

Frequently Asked Questions

1. How large is the India solar rooftop market and what is its growth forecast?

Ans: The India solar rooftop market is entering a high-growth phase, supported by rising electricity costs, government subsidy support, net-metering adoption, and strong residential, commercial, and industrial demand. India added around 7.1 GW of rooftop solar capacity in 2025, more than doubling from 2024, with growth strongly supported by the PM Surya Ghar programme. The market is projected to continue expanding steadily through 2032 as households, MSMEs, factories, warehouses, institutions, and commercial buildings shift toward distributed solar to reduce power costs and improve energy reliability. The report provides detailed market sizing, forecast modelling, and segment-wise analysis across capacity, value, end-use sector, system size, ownership model, and state-level demand.

2. Which segments are driving demand in the India solar rooftop market?

Ans: The India solar rooftop market segmentation shows that commercial and industrial users remain a major demand base, driven by electricity cost savings, ESG targets, captive consumption, and payback-led investment decisions. However, the residential segment is now the fastest-growing category, supported by PM Surya Ghar subsidies, simplified digital approvals, and growing consumer awareness. The report analyses rooftop solar demand across residential, commercial, industrial, institutional, government, healthcare, education, hospitality, retail, warehouse, and MSME applications. It also breaks down the market by system size, grid connectivity, ownership model, component type, installation type, and sales channel.

3. What are the key drivers of growth in the India solar rooftop market?

Ans: Key India solar rooftop market drivers include rising grid electricity tariffs, strong household-level subsidy support, accelerated commercial and industrial decarbonisation, improved financing availability, and growing adoption of solar-plus-storage and smart energy management systems. Under PM Surya Ghar, India reached nearly 24 lakh household rooftop solar adoptions by December 2025, with around 7 GW of clean energy capacity and subsidy disbursement of more than ₹13,464 crore, indicating strong policy-backed residential momentum. Demand is also being supported by falling solar module costs, domestic module manufacturing expansion, and growing demand from factories, malls, schools, hospitals, warehouses, and housing societies.

4. Which regions are driving growth in the India solar rooftop market?

Ans: Regional analysis of the India solar rooftop market shows strong growth across Gujarat, Maharashtra, Uttar Pradesh, Rajasthan, Karnataka, Tamil Nadu, Kerala, Delhi NCR, Telangana, and Andhra Pradesh. Gujarat has emerged as one of the strongest residential rooftop solar markets under PM Surya Ghar, supported by high consumer awareness, strong vendor networks, and proactive state-level implementation. Maharashtra, Uttar Pradesh, Kerala, and Rajasthan are also among the leading states for rooftop solar adoption. For commercial and industrial rooftop solar, demand is concentrated around manufacturing and consumption clusters such as Gujarat, Maharashtra, Tamil Nadu, Karnataka, Telangana, Haryana, Rajasthan, Delhi NCR, and Uttar Pradesh. The report provides state-wise and city-wise insights to help companies identify high-potential markets for EPC expansion, channel partnerships, financing, and component sales.

5. What are the latest trends in the India solar rooftop market?

Ans: The latest India solar rooftop market trends include rapid residential solar adoption, increasing C&I rooftop installations, growing interest in OPEX and RESCO models, rising demand for hybrid rooftop solar with battery storage, and wider use of digital monitoring platforms. Rooftop solar accounted for more than 19 percent of India’s total solar installations in 2025, highlighting the growing importance of distributed generation within India’s renewable energy mix. The market is also seeing stronger demand for high-efficiency modules, smart inverters, remote monitoring, energy management software, and financing-led sales models. The report provides detailed insights into emerging technology trends, policy changes, state-level opportunities, pricing benchmarks, competitive landscape, and future demand shifts across the India solar rooftop market.

Frequently Asked Questions

1. How large is the India solar rooftop market and what is its growth forecast?

Ans: The India solar rooftop market is entering a high-growth phase, supported by rising electricity costs, government subsidy support, net-metering adoption, and strong residential, commercial, and industrial demand. India added around 7.1 GW of rooftop solar capacity in 2025, more than doubling from 2024, with growth strongly supported by the PM Surya Ghar programme. The market is projected to continue expanding steadily through 2032 as households, MSMEs, factories, warehouses, institutions, and commercial buildings shift toward distributed solar to reduce power costs and improve energy reliability. The report provides detailed market sizing, forecast modelling, and segment-wise analysis across capacity, value, end-use sector, system size, ownership model, and state-level demand.

2. Which segments are driving demand in the India solar rooftop market?

Ans: The India solar rooftop market segmentation shows that commercial and industrial users remain a major demand base, driven by electricity cost savings, ESG targets, captive consumption, and payback-led investment decisions. However, the residential segment is now the fastest-growing category, supported by PM Surya Ghar subsidies, simplified digital approvals, and growing consumer awareness. The report analyses rooftop solar demand across residential, commercial, industrial, institutional, government, healthcare, education, hospitality, retail, warehouse, and MSME applications. It also breaks down the market by system size, grid connectivity, ownership model, component type, installation type, and sales channel.

3. What are the key drivers of growth in the India solar rooftop market?

Ans: Key India solar rooftop market drivers include rising grid electricity tariffs, strong household-level subsidy support, accelerated commercial and industrial decarbonisation, improved financing availability, and growing adoption of solar-plus-storage and smart energy management systems. Under PM Surya Ghar, India reached nearly 24 lakh household rooftop solar adoptions by December 2025, with around 7 GW of clean energy capacity and subsidy disbursement of more than ₹13,464 crore, indicating strong policy-backed residential momentum. Demand is also being supported by falling solar module costs, domestic module manufacturing expansion, and growing demand from factories, malls, schools, hospitals, warehouses, and housing societies.

4. Which regions are driving growth in the India solar rooftop market?

Ans: Regional analysis of the India solar rooftop market shows strong growth across Gujarat, Maharashtra, Uttar Pradesh, Rajasthan, Karnataka, Tamil Nadu, Kerala, Delhi NCR, Telangana, and Andhra Pradesh. Gujarat has emerged as one of the strongest residential rooftop solar markets under PM Surya Ghar, supported by high consumer awareness, strong vendor networks, and proactive state-level implementation. Maharashtra, Uttar Pradesh, Kerala, and Rajasthan are also among the leading states for rooftop solar adoption. For commercial and industrial rooftop solar, demand is concentrated around manufacturing and consumption clusters such as Gujarat, Maharashtra, Tamil Nadu, Karnataka, Telangana, Haryana, Rajasthan, Delhi NCR, and Uttar Pradesh. The report provides state-wise and city-wise insights to help companies identify high-potential markets for EPC expansion, channel partnerships, financing, and component sales.

5. What are the latest trends in the India solar rooftop market?

Ans: The latest India solar rooftop market trends include rapid residential solar adoption, increasing C&I rooftop installations, growing interest in OPEX and RESCO models, rising demand for hybrid rooftop solar with battery storage, and wider use of digital monitoring platforms. Rooftop solar accounted for more than 19 percent of India’s total solar installations in 2025, highlighting the growing importance of distributed generation within India’s renewable energy mix. The market is also seeing stronger demand for high-efficiency modules, smart inverters, remote monitoring, energy management software, and financing-led sales models. The report provides detailed insights into emerging technology trends, policy changes, state-level opportunities, pricing benchmarks, competitive landscape, and future demand shifts across the India solar rooftop market.