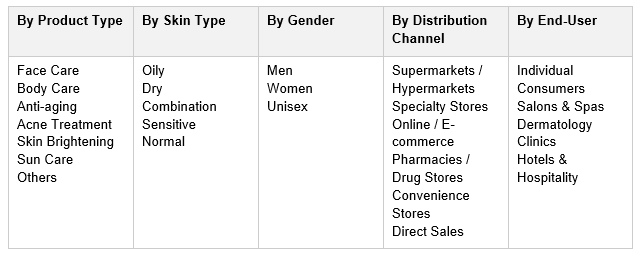

India Skincare Market, By Product Type (Face Care, Body Care, Anti-aging, Acne Treatment, Skin Brightening, Sun Care, Others); By Skin Type (Oily, Dry, Combination, Sensitive, Normal); By Gender (Men, Women, Unisex); By Price Range (Mass, Premium, Luxury); By Ingredient Type (Synthetic/Chemical, Natural/Organic, Ayurvedic, Vegan); By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online/E-commerce, Pharmacies/Drug Stores, Direct Sales); By End-User (Individual Consumers, Salons & Spas, Dermatology Clinics, Hotels & Hospitality); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 130

- Report Format: pdf

- Report Price: $1800 USD

India Skincare Market: Premiumization, Active Ingredients, and D2C Clean Beauty Growth Power Structural Demand, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

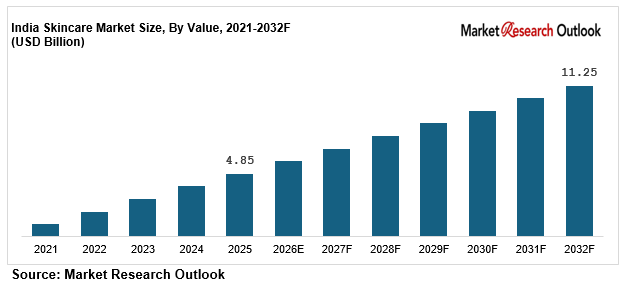

| Market Size (2025) | USD 4.85 Billion |

| CAGR (2026-2032) | 12.8% |

| Leading Segment | Face Care (Moisturizers & Cleansers) |

| Fastest Growing Segment | Active Ingredient Serums & Clean Beauty |

| Market Size (2032) | USD 11.25 Billion |

Source: Market Research Outlook

Market Overview: India Skincare Market

The India skincare market size is witnessing rapid expansion, driven by rising disposable income, accelerating urbanization across Tier-I, Tier-II, and Tier-III cities, expanding personal grooming and self-care culture, growing aspirational consumption of active ingredients, K-beauty inspired multi-step routines, and the rapid scaling of e-commerce, D2C, and quick-commerce distribution platforms. Valued at USD 4.85 billion in 2025 and projected to reach USD 11.25 billion by 2032, growing at a CAGR of 12.8%, the India skincare market growth is being fuelled by mass-market face care adoption, rising premium serum and active-ingredient sales, expanding men’s and unisex skincare segments, and growing institutional demand from salons, dermatology clinics, spas, and luxury hospitality. Face care leads consumption, while active-ingredient serums and clean beauty formulations are emerging as the fastest growing category. Strengthening influencer-led marketing, dermatologist-recommended routines, and clean-beauty preferences by Indian consumers, alongside aggressive product launches by leading brands, are reshaping the supply landscape. As domestic majors including Hindustan Unilever, Emami, Dabur, Patanjali, Mamaearth (Honasa), Plum, Wow Skin Science, and Forest Essentials scale mass and premium product portfolios, and global majors including L’Oreal, Nivea, Procter & Gamble, and The Body Shop deepen India-specific innovation, the India skincare market is evolving into a brand-led, premiumizing, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Skincare Market

- The India skincare market size is projected to grow from USD 4.85 billion in 2025 to USD 11.25 billion by 2032, registering a strong CAGR of 12.8%, driven by accelerated urbanization, rising premium skincare adoption, and the structural shift toward active-ingredient routines across urban and Tier-II Indian markets.

- Face care dominates the India skincare market, accounting for over 58% of total category value in 2025, driven by mass-market price points of INR 150 to INR 850 for cleansers and moisturizers, rising daily-use skincare behaviour, and strong distribution across supermarkets, pharmacies, kirana stores, and online platforms across urban and semi-urban India.

- Active-ingredient serums and clean beauty products are emerging as the fastest growing segment in the India skincare market, expected to grow at 22% to 28% annually, as aspirational consumers, women, and millennials trade up from basic moisturizers to Niacinamide, Vitamin C, Hyaluronic Acid, Retinol, and AHA/BHA-based premium serums across metro markets.

- Rapid scaling of D2C beauty platforms, quick-commerce channels, and social commerce, with online skincare sales crossing 28% to 32% of premium skincare demand by mid-2025, is structurally expanding the India skincare market across men’s, women’s, and unisex skincare categories.

- Rising investments by domestic majors such as Honasa Consumer (Mamaearth), Plum Goodness, Wow Skin Science, Lotus Herbals, Forest Essentials, and Minimalist (acquired by HUL) in new product launches, dermatologist tie-ups, and clean-beauty formulations are strengthening domestic supply and supporting the India skincare market forecast 2032.

Key Market Drivers: India Skincare Market

Rising Disposable Income, Urbanization, and Growing Skincare Awareness Among Indian Millennials and Gen-Z

Growth in the India skincare market is being driven by rising disposable income, accelerating urbanization, and a structural shift in skincare behaviour among urban and semi-urban Indian consumers. India’s per-capita disposable income has grown at over 9% annually between 2020 and 2025, supporting discretionary spend on personal care, skincare, and grooming categories. Skincare penetration among urban Indian consumers has crossed 72% in 2025, up from 58% in 2020, while per-capita skincare consumption remains well below global benchmarks of USD 35 to USD 60, indicating significant headroom for category expansion. Daily-use skincare behaviour among the 18 to 40 age cohort, supported by social media exposure, work-from-home routines, video-call culture, and rising social interaction, is structurally pulling demand into the India skincare market. Mass-priced skincare products between INR 150 and INR 850, available across modern trade, pharmacies, general trade, and online platforms, continue to drive high-volume penetration across the country.

Premiumization, K-Beauty Influence, and Growing Demand for Active Ingredients

The India skincare market is benefiting from a strong premiumization wave, with consumers, especially women and millennials, trading up from basic moisturizers and cleansers to premium serums, essences, and active-ingredient-driven routines. Premium skincare sales in India grew by over 26% in 2025 according to leading industry trackers, driven by rising aspirational consumption, K-beauty multi-step routine influence, and growing exposure to international skincare categories. Average ticket sizes for premium skincare in India range from INR 600 to INR 3,500 for serums, while luxury skincare from brands such as Estée Lauder, Clinique, La Mer, Kiehl’s, and Sunday Riley is seeing growing adoption in metro cities and Tier-I markets. Active ingredients including Niacinamide (5% to 10%), Vitamin C (10% to 20%), Hyaluronic Acid, Retinol (0.1% to 1%), AHA, BHA, and Peptides are increasingly central to consumer purchasing decisions, with over 65% of urban skincare buyers in 2025 actively researching ingredient lists. Domestic premium and prestige players such as Minimalist (now under HUL), The Derma Co. (Honasa), Plum Goodness, Forest Essentials, and Dot & Key are scaling active-ingredient serum portfolios. Premium gifting occasions, including weddings, Diwali, Raksha Bandhan, and corporate gifting cycles, account for nearly 25% of premium skincare sales, supporting structural growth across the India skincare market.

E-commerce Expansion, D2C Brands, Influencer-Led Marketing, and Quick-Commerce Accelerating Category Growth

Rapid growth in online and D2C distribution is a major catalyst for the India skincare market, with the e-commerce channel projected to grow at 22% to 26% annually through 2032. Online skincare sales now account for an estimated 28% to 32% of total category value, led by platforms such as Nykaa, Amazon, Flipkart, Myntra, Tira, Purplle, and direct brand websites. Quick-commerce platforms including Blinkit, Zepto, Swiggy Instamart, and BigBasket Now have emerged as new growth engines, contributing 7% to 10% of urban skincare sales by mid-2025. Influencer-led marketing, particularly on Instagram, YouTube, and short-form video platforms, is reshaping consumer discovery, with over 72% of urban millennials citing social media as their primary skincare discovery channel. Leading D2C and digital-first brands such as Mamaearth, The Derma Co., Plum Goodness, Minimalist, Bella Vita Organic, Dot & Key, mCaffeine, Earth Rhythm, and SugarPop have scaled aggressive influencer, content, and performance marketing pipelines, supporting structural expansion of the India skincare market across all major end-user categories through 2032.

Key Market Challenges: India Skincare Market

High Proliferation of Counterfeit and Grey-Market Skincare Products

The India skincare market continues to face challenges around the strong presence of counterfeit and grey-market skincare products, particularly in mid and premium segments. The counterfeit and grey-market skincare economy, estimated at 18% to 22% of total category value in major metros, undermines brand-building investments by leading players such as Hindustan Unilever, L’Oreal, Nivea, P&G, and Mamaearth. Look-alike packaging, imitation Olay, Pond’s, Nivea, Lakme, Mamaearth, and Plum variants, and unauthorised online listings continue to challenge category economics. Imported luxury skincare brands face significant grey-market penetration through unofficial international channels and duty-free arbitrage. Strengthening enforcement under the Bureau of Indian Standards (BIS), CDSCO oversight, tighter e-commerce listing policies on Nykaa and Amazon, and brand-led anti-counterfeit QR code authentication are gradually easing these pressures, but counterfeit penetration remains a structural concern across the India skincare market.

Raw Material Price Volatility for Active Ingredients, Packaging, and Essential Oils

The India skincare market faces structural complexity from raw material price volatility, particularly for active ingredients, botanical extracts, surfactants, emollients, preservatives, specialty glass, and premium pump dispenser packaging. Global active ingredient prices for Niacinamide, Hyaluronic Acid, Vitamin C derivatives, and Retinol have fluctuated by 14% to 28% between 2022 and 2025, while specialty botanical extracts such as Centella Asiatica, Bakuchiol, Squalane, and Ceramides have seen sustained inflation due to limited cultivation cycles and rising global premium demand. India imports over 55% of its high-end skincare actives and specialty ingredients, exposing manufacturers to currency volatility and global supply chain risks. Glass jar, airless dispenser, dropper bottle, and pump packaging costs have also risen by 10% to 18% over 2023 to 2025, compressing gross margins for mass-market skincare manufacturers. While leading domestic ingredient houses and global majors such as Givaudan, BASF, Croda, Symrise, and Evonik are localising compounding and supply, raw material volatility remains a near-term challenge for the India skincare market.

Skin Sensitivity Concerns and Tightening Regulations on Parabens, Sulphates, and Dermatological Compliance

The India skincare market faces practical constraints around growing consumer concern over skin sensitivity, allergic reactions, and tightening regulations on parabens, sulphates, phthalates, mineral oils, and synthetic colorants. Surveys by leading dermatology associations indicate that over 22% of urban Indian consumers report mild to moderate skin reactions to chemical-based skincare and high-concentration active-ingredient products, driving demand for paraben-free, sulphate-free, fragrance-free, and dermatologically-tested formulations. Regulatory bodies including CDSCO, BIS, and the Ministry of Health are tightening labelling, ingredient disclosure, and chemical formulation norms in line with EU INCI and global cosmetic standards. The Drugs and Cosmetics Act, ingredient allergen disclosure rules, and pending sustainability mandates on packaging waste add compliance complexity for both domestic and global brands. Clean beauty, Ayurvedic, and vegan formulations from players such as Forest Essentials, Biotique, Patanjali, Mamaearth, and Just Herbs are emerging as solutions, but premium pricing and limited consumer awareness remain barriers to mass adoption across the India skincare market.

Key Market Trends: India Skincare Market

Rapid Adoption of Active Ingredients: Niacinamide, Vitamin C, Hyaluronic Acid, Retinol, and AHA/BHA

The India skincare market is undergoing a clear product mix shift toward active-ingredient-driven serums, treatments, and targeted skincare formulations, with these higher-concentration categories expected to capture over 38% of total face care category value by 2027. Niacinamide-based serums (5% to 10% concentration) targeting oil control, pore minimization, and brightening are increasingly preferred by oily and combination skin consumers, while Vitamin C serums (10% to 20%) for brightening and antioxidant protection are seeing strong daily-use adoption. Hyaluronic Acid for deep hydration, Retinol (0.1% to 1%) for anti-aging, and AHA/BHA exfoliants for acne and texture refinement are emerging as core consumer purchase categories. Domestic active-ingredient-led brands including Minimalist (HUL), The Derma Co. (Honasa), Dot & Key, Earth Rhythm, Foxtale, Pilgrim, and Deconstruct have scaled premium and prestige serum portfolios. Dermatologist-led recommendation routines, particularly through Instagram and YouTube influencers, are driving structural consumer trade-up. This active-ingredient adoption shift is reinforcing the India skincare market forecast 2032 across both mass and premium categories.

Growth of Clean Beauty, Natural, Vegan, Ayurvedic, and Dermatologist-Approved Formulations

A clear shift toward clean beauty, natural, vegan, Ayurvedic, and dermatologist-approved formulations is reshaping the India skincare market, particularly across the women’s, men’s, and premium segments. Clean-beauty positioned skincare launches grew by over 32% in 2024 and 2025, with leading players including Mamaearth, Plum Goodness, Forest Essentials, Khadi Natural, Patanjali, Just Herbs, Kama Ayurveda, and Vilvah scaling clean and Ayurvedic skincare portfolios. Vegan and cruelty-free certifications from PETA, Leaping Bunny, EWG, and Made Safe are increasingly central to D2C brand positioning, especially among Gen-Z and millennial women consumers. Paraben-free, sulphate-free, mineral-oil-free, fragrance-free, and 100% vegetarian formulations are seeing structural demand in Tier-II and Tier-III cities, driven by skin sensitivity concerns, ethical consumption, and gifting use cases. Dermatologist-approved brands such as Cetaphil, Neutrogena, La Roche-Posay, Re’equil, and Cosrx are also gaining strong traction in dermo-cosmetics. This clean and dermatologist-led skincare momentum is supporting category premiumization and is reinforcing structural growth across the India skincare market.

Capacity Expansion, Quick-Commerce Distribution, and Digital-First Brand Launches

A wave of capacity expansion, quick-commerce distribution, and digital-first brand launches is reshaping the India skincare market supply landscape. Combined India-focused capital expenditure announcements by leading skincare and personal care players exceeded INR 3,200 crore across 2023 to 2025. Honasa Consumer expanded Mamaearth, The Derma Co., and Aqualogica manufacturing capacity, Hindustan Unilever scaled Minimalist and Lakme production after acquisition, Plum Goodness added new serum production lines, Forest Essentials expanded its Lodsi Uttarakhand manufacturing unit, and Wow Skin Science scaled Bengaluru production. Quick-commerce platforms such as Blinkit, Zepto, Swiggy Instamart, and Bigbasket Now have emerged as a high-growth distribution channel for impulse skincare purchases, with quick-commerce contribution rising to 7% to 10% of urban skincare sales by mid-2025. Digital-first brands including Foxtale, Pilgrim, Earth Rhythm, Deconstruct, Dr. Sheth’s, and Bare Anatomy are scaling D2C, Nykaa, and Amazon Beauty platforms. Combined with rising aspirational consumption and premiumization across urban India, these developments are reinforcing the India skincare market forecast 2032 across the entire value chain.

Segmental Insights: India Skincare Market

By Product Type: Face Care Segment Dominates the India Skincare Market

The face care segment dominates the India skincare market, accounting for an estimated 56% to 60% of total category value, driven by mass-market price points, daily-use skincare behaviour, and strong distribution across modern trade, general trade, pharmacies, and e-commerce. Moisturizers and cleansers lead within face care, capturing over 50% of segment volumes, supported by brands such as Pond’s, Nivea, Olay, Mamaearth, Plum, Cetaphil, and Neutrogena. Serums, the fastest-growing face care sub-category, are growing at 24% to 28% annually, driven by active-ingredient adoption. The body care segment contributes another 22% to 25% of demand, driven by body lotions, body washes, and exfoliators. Sun care contributes 6% to 8%, supported by SPF awareness and dermatologist recommendations. Anti-aging accounts for 5% to 7%, while skin brightening contributes another 6% to 8%, and acne treatment around 4% to 5%. In 2025, leading brands including Hindustan Unilever, L’Oreal, Nivea, Mamaearth, Plum, Forest Essentials, and Minimalist scaled product launches and gifting variants, reinforcing segment dominance in the India skincare market.

By Price Range and Gender: Mass Leads While Premium and Men’s Skincare Categories Grow Fastest

Mass-priced skincare leads the India skincare market price-tier landscape, accounting for approximately 62% to 65% of total category value, driven by daily-use moisturizer and cleanser consumption and affordable face care options under INR 500. Premium skincare priced between INR 800 and INR 3,500 contributes another 25% to 28%, primarily in metro and Tier-I urban markets. Luxury skincare, typically priced above INR 3,500, accounts for 8% to 12% of the category, led by imported brands such as Estée Lauder, Clinique, La Mer, and SK-II. By gender, women’s skincare continues to lead category volumes with 72% to 75% share, supported by strong face care, anti-aging, and serum penetration. Men’s skincare is the fastest growing sub-segment, expanding at 18% to 22% annually, supported by brands such as Beardo, The Man Company, Bombay Shaving Company, Ustraa, Park Avenue, and Emami Fair & Handsome. Unisex skincare is also gaining traction, particularly in D2C active-ingredient categories, reflecting evolving consumer preferences across the India skincare market.

Regional Insights: India Skincare Market

Regional analysis of the India skincare market shows that West India and South India collectively account for approximately 55% to 60% of total category value, driven by Maharashtra (Mumbai, Pune metro consumption belt), Gujarat (Ahmedabad, Surat), Karnataka (Bengaluru), Tamil Nadu (Chennai, Coimbatore), Telangana (Hyderabad), and Kerala, supported by strong urban skincare penetration, dermatologist density, and proximity to skincare manufacturing clusters. North India contributes around 25% to 28% of demand, led by Delhi NCR, Punjab, Haryana, Uttar Pradesh, and Rajasthan, supported by premium skincare consumer base, gifting culture, and dry-climate driven moisturizer demand. East and Central India together account for 14% to 18% of demand, supported by West Bengal (Kolkata), Odisha, Madhya Pradesh, and Chhattisgarh, where mass skincare and Ayurvedic skincare consumption is accelerating across Tier-II cities. In 2025, capacity additions and brand activity by Hindustan Unilever across pan-India, Honasa Consumer (Mamaearth) in West India, Forest Essentials in North India, Wow Skin Science in South India, and Patanjali across Tier-II markets reinforced regional supply hubs, supporting closer execution of mass, premium, and dermo-cosmetic product strategies across the India skincare market.

Recent Developments: India Skincare Market

- The India skincare market witnessed strong momentum in product launches and channel expansion during 2024 and 2025. The category grew by an estimated 14% to 16% in value terms in 2025, supported by aggressive new product launches, dermatologist-led campaigns, festive season activations, and quick-commerce expansion. Online and D2C sales crossed 28% to 32% of total category value, with premium active-ingredient serum sales growing by over 28% year-on-year, according to leading industry trackers. Cumulative branded category penetration is projected to expand from 72% in 2025 to 85% to 90% by FY32, growing at an average 12% to 14% annually.

- Domestic skincare players have deepened India-focused capacity expansion and brand portfolio building. In 2025, Honasa Consumer expanded Mamaearth, The Derma Co., and Aqualogica production and launched new active-ingredient variants, Plum Goodness scaled serum manufacturing, Wow Skin Science added new Vitamin C and Niacinamide product lines, Forest Essentials expanded Ayurvedic premium portfolios, Minimalist (acquired by HUL) scaled active-ingredient launches, and Lotus Herbals expanded sun care offerings. Patanjali and Himalaya expanded Ayurvedic and natural skincare portfolios. These developments are strengthening domestic supply and supporting the India skincare market forecast 2032.

- Premium and D2C skincare momentum has gained strong traction in the India skincare market. In 2025, leading premium and digital-first players including Minimalist, The Derma Co., Foxtale, Pilgrim, Dot & Key, Earth Rhythm, Deconstruct, mCaffeine, and Bella Vita Organic scaled active-ingredient serums, sunscreens, and dermo-cosmetic gifting set portfolios. Strategic partnerships between domestic skincare brands, global beauty retailers such as Nykaa, Tira, Sephora India, and Shoppers Stop, and quick-commerce platforms are positioning India as one of the most actively scaling premium skincare markets globally, strengthening long-term competitive positioning in the India skincare market forecast 2032.

Key Market Players: India Skincare Market

- Hindustan Unilever Limited (Pond’s, Lakme, Vaseline, Glow & Lovely)

- L’Oreal India Pvt. Ltd. (Garnier, L’Oreal Paris)

- Nivea India Pvt. Ltd. (Beiersdorf India)

- Procter & Gamble Hygiene and Health Care Limited (Olay)

- Emami Limited (BoroPlus, Fair & Handsome)

- Dabur India Limited

- Patanjali Ayurved Limited

- Himalaya Wellness Company

- Honasa Consumer Limited (Mamaearth, The Derma Co., Aqualogica)

- Plum Goodness (Pureplay Skin Sciences)

- Wow Skin Science (Body Cupid Pvt. Ltd.)

- Forest Essentials (Mountain Valley Springs)

- Lotus Herbals Pvt. Ltd.

- Biotique (Bio Veda Action Research Co.)

- Minimalist (Be Minimalist, acquired by HUL)

Report Scope

In this report, the India Skincare Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Face Care (Cleansers, Moisturizers, Serums, Sunscreens, Masks, Toners)

- Body Care (Lotions, Creams, Body Washes, Exfoliators)

- Anti-aging

- Acne Treatment

- Skin Brightening

- Sun Care

- Others

- By Skin Type

- Oily

- Dry

- Combination

- Sensitive

- Normal

- By Gender

- Men

- Women

- Unisex

- By Price Range

- Mass

- Premium

- Luxury

- By Ingredient Type

- Synthetic / Chemical

- Natural / Organic

- Ayurvedic

- Vegan

- By Distribution Channel

- Supermarkets / Hypermarkets

- Specialty Stores

- Online / E-commerce

- Pharmacies / Drug Stores

- Convenience Stores

- Direct Sales / MLM

- By End-User

- Individual Consumers

- Salons & Spas

- Dermatology Clinics

- Hotels & Hospitality

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Skincare Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic D2C skincare brands, specialty active-ingredient and dermo-cosmetic producers, niche premium clean-beauty houses, or regional Ayurvedic skincare brands.

The India Skincare Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Skin Type

- By Gender

- By Price Range

- By Ingredient Type

- By Distribution Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Skincare Market

- India Skincare Market Insights

- Market Dynamics

- Growth Drivers

- Rising disposable income, urbanization, and growing skincare awareness among Indian millennials and Gen-Z.

- Premiumization, K-beauty influence, and growing demand for active ingredients such as Niacinamide and Vitamin C.

- E-commerce expansion, D2C brands, influencer-led marketing, and quick-commerce accelerating category growth.

- Restraints

- High proliferation of counterfeit and grey-market skincare products in mid and premium segments.

- Raw material price volatility for active ingredients, packaging, essential oils, and specialty glass.

- Skin sensitivity concerns and tightening regulations on parabens, sulphates, and dermatological compliance.

- Opportunities

- Tier-II and Tier-III city expansion creating a massive untapped skincare consumption base across India.

- Clean beauty, vegan, natural, and Ayurvedic formulations opening new premium value pools.

- Men’s skincare, dermo-cosmetics, and personalized AI-driven skincare supporting next-generation growth.

- Challenges

- Strong unorganized herbal and chemist-led skincare market limiting branded category penetration.

- Limited consumer literacy on actives, concentration grades, pH levels, and ingredient interactions.

- Supply chain complexity for premium imported actives and specialty cold-chain skincare logistics.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (active ingredients, botanical extracts, surfactants, emollients)

- Specialty Ingredient Houses & Formulators (Givaudan, BASF, Croda, Symrise, Evonik)

- Packaging Suppliers (glass jars, pump bottles, airless dispensers, sustainable PCR plastics)

- Contract Manufacturers & Private Label Producers

- Quality Control, R&D & Testing Laboratories (BIS, CDSCO, NABL, dermatology trials)

- Distributors, Wholesalers & Online Aggregators

- Brand Owners & Marketing Companies (HUL, L’Oreal, Nivea, Mamaearth, Plum, Forest Essentials)

- Retailers, Specialty Stores, Salons, Dermatology Clinics, Quick-commerce & D2C Platforms

- End-Users (individual consumers, salons & spas, dermatology clinics, hotels & hospitality)

- India Skincare Market: Regulatory Framework

- India Skincare Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Million Units)

- Market Share & Forecast

- By Product Type

- Face Care

- Body Care

- Anti-aging

- Acne Treatment

- Skin Brightening

- Sun Care

- Others

- By Skin Type

- Oily

- Dry

- Combination

- Sensitive

- Normal

- By Gender

- Men

- Women

- Unisex

- By Price Range

- Mass

- Premium

- Luxury

- By Ingredient Type

- Synthetic / Chemical

- Natural / Organic

- Ayurvedic

- Vegan

- By Distribution Channel

- Supermarkets / Hypermarkets

- Specialty Stores

- Online / E-commerce

- Pharmacies / Drug Stores

- Convenience Stores

- Direct Sales / MLM

- By End-User

- Individual Consumers

- Salons & Spas

- Dermatology Clinics

- Hotels & Hospitality

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Skincare Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Hindustan Unilever Limited (Pond’s, Lakme, Vaseline, Glow & Lovely)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- L’Oreal India Pvt. Ltd. (Garnier, L’Oreal Paris)

- Nivea India Pvt. Ltd. (Beiersdorf India)

- Procter & Gamble Hygiene and Health Care Limited (Olay)

- Emami Limited (BoroPlus, Fair & Handsome)

- Dabur India Limited

- Patanjali Ayurved Limited

- Himalaya Wellness Company

- Honasa Consumer Limited (Mamaearth, The Derma Co., Aqualogica)

- Plum Goodness (Pureplay Skin Sciences)

- Wow Skin Science (Body Cupid Pvt. Ltd.)

- Forest Essentials (Mountain Valley Springs)

- Lotus Herbals Pvt. Ltd.

- Biotique (Bio Veda Action Research Co.)

- Minimalist (Be Minimalist, acquired by HUL)

- Other Prominent Players

- Hindustan Unilever Limited (Pond’s, Lakme, Vaseline, Glow & Lovely)

- By Product Type

- Market Size & Forecast, 2021-2032

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India skincare market and what is its growth forecast?

Ans: The India skincare market is valued at USD 4.85 billion in 2025 and is projected to reach USD 11.25 billion by 2032, growing at a CAGR of 12.8%, supported by urbanization, premiumization, and digital retail expansion.

2. Which segments are driving demand in the India skincare market?

Ans: Face care dominates the India skincare market with over 58% value share, while active-ingredient serums (Niacinamide, Vitamin C, Hyaluronic Acid, Retinol) and clean beauty are the fastest growing segments, supported by D2C brand expansion.

3. What are the key drivers of growth in the India skincare market?

Ans: Key drivers include rising disposable income, urbanization, premiumization, K-beauty influence, active-ingredient adoption, social media-led discovery, expansion of e-commerce, D2C platforms, and quick-commerce across the India skincare market.

4. Which regions are driving growth in the India skincare market?

Ans: Maharashtra, Karnataka, Gujarat, Delhi NCR, Tamil Nadu, and Telangana lead the India skincare market, supported by strong urban consumption, premium category demand, dermatologist density, and rising Tier-II city penetration.

5. What are the latest trends in the India skincare market?

Ans: Latest trends include rapid active-ingredient adoption, clean beauty and Ayurvedic growth, men's skincare expansion, dermo-cosmetic uptake, D2C brand surge, quick-commerce delivery, and personalized AI-driven skincare across the India skincare market.

Frequently Asked Questions

1. How large is the India skincare market and what is its growth forecast?

Ans: The India skincare market is valued at USD 4.85 billion in 2025 and is projected to reach USD 11.25 billion by 2032, growing at a CAGR of 12.8%, supported by urbanization, premiumization, and digital retail expansion.

2. Which segments are driving demand in the India skincare market?

Ans: Face care dominates the India skincare market with over 58% value share, while active-ingredient serums (Niacinamide, Vitamin C, Hyaluronic Acid, Retinol) and clean beauty are the fastest growing segments, supported by D2C brand expansion.

3. What are the key drivers of growth in the India skincare market?

Ans: Key drivers include rising disposable income, urbanization, premiumization, K-beauty influence, active-ingredient adoption, social media-led discovery, expansion of e-commerce, D2C platforms, and quick-commerce across the India skincare market.

4. Which regions are driving growth in the India skincare market?

Ans: Maharashtra, Karnataka, Gujarat, Delhi NCR, Tamil Nadu, and Telangana lead the India skincare market, supported by strong urban consumption, premium category demand, dermatologist density, and rising Tier-II city penetration.

5. What are the latest trends in the India skincare market?

Ans: Latest trends include rapid active-ingredient adoption, clean beauty and Ayurvedic growth, men's skincare expansion, dermo-cosmetic uptake, D2C brand surge, quick-commerce delivery, and personalized AI-driven skincare across the India skincare market.