India Residential Water Purifier Market, By Technology (Reverse Osmosis (RO), Ultraviolet (UV), Ultrafiltration (UF), RO+UV+UF, Gravity-Based, Activated Carbon, Others); By Installation Type (Wall-Mounted, Counter-Top, Under-Sink, Faucet/Tap-Mounted); By Capacity (Below 7L, 7 to 10L, 10 to 15L, Above 15L); By Distribution Channel (Online E-Commerce, Specialty Stores, Hypermarkets & Modern Retail, Direct Selling, Others); By Price Range (Economy, Mid-Range, Premium); By End-User (Independent Households, Apartments & Gated Communities, Tier-2 & Tier-3 Households); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Residential Water Purifier Market: Declining Groundwater Quality and Premium Smart Purifier Adoption Drive Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

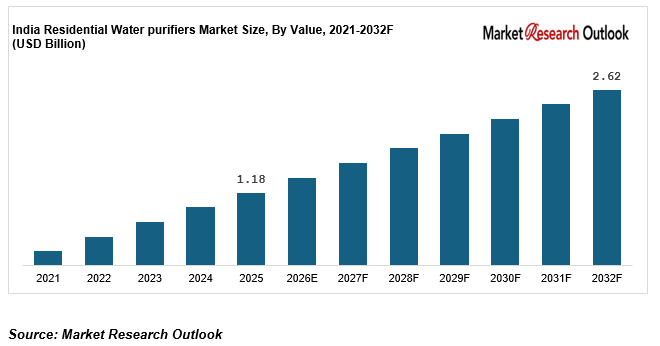

| Market Size (2025) | USD 1.18 Billion |

| CAGR (2026-2032) | 12.1% |

| Leading Segment | Reverse Osmosis (RO) Water Purifiers |

| Fastest Growing Segment | Smart IoT-Connected and Alkaline-Mineral Water Purifiers |

| Market Size (2032) | USD 2.62 Billion |

Source: Market Research Outlook

Market Overview: India Residential Water Purifier Market

The India residential water purifier market size is witnessing rapid expansion, driven by deteriorating groundwater quality, rising TDS levels across major Indian metros, accelerating urban water contamination, expanding premium and smart IoT-connected water purifier adoption, and major capacity additions by Indian water purifier brands. Valued at USD 1.18 Billion in 2025 and projected to reach USD 2.62 Billion by 2032, growing at a CAGR of 12.1%, the India residential water purifier market growth is being fuelled by strong household demand under metros and tier-1 cities, rising tier-2 city procurement tied to growing health awareness and disposable income, and accelerating apartment and gated community installations. Reverse osmosis (RO) and RO+UV+UF combination water purifiers lead consumption, while smart IoT-connected, alkaline-mineral, and copper-infused residential water purifiers are emerging as the fastest growing category. Tightening BIS quality requirements, the IS 16240 RO water recovery norm, and growing e-commerce penetration are reshaping the supply landscape. As branded players including Eureka Forbes, Kent RO Systems, HUL Pureit, LivPure, and A.O. Smith expand integrated residential water purifier portfolios, and consumer durable majors including Havells, Blue Star, Whirlpool, LG Electronics, Faber, Bosch, and Crompton scale premium product pipelines, the India residential water purifier market is evolving into a consumer-led, technology-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Residential Water Purifier Market

- The India residential water purifier market size is projected to grow from USD 1.18 Billion in 2025 to USD 2.62 Billion by 2032, registering a strong CAGR of 12.1%, driven by accelerated urban water quality concerns, rising health awareness, and the structural shift toward premium, smart IoT-connected residential water purifier adoption across urban India.

- Reverse osmosis (RO) and RO+UV+UF combination water purifiers dominate the India residential water purifier market, accounting for over 62% of total installed units in 2025, driven by deteriorating groundwater quality, rising TDS levels across major metros, and growing consumer preference for multi-stage purification.

- Smart IoT-connected, alkaline-mineral, and copper-infused residential water purifiers are emerging as the fastest growing category in the India residential water purifier market, expected to grow at 18 to 22% annually as premium urban households, health-conscious consumers, and connected home adopters reshape sourcing priorities.

- Rapid scaling of e-commerce and D2C channels, with Amazon India, Flipkart, Croma, Reliance Digital, and brand websites including KentRO.com and Aquaguard.com contributing 32 to 36% of total water purifier sales, is structurally expanding the India residential water purifier market across metros, tier-1, and emerging tier-2 cities.

- Rising investments by domestic water purifier brands such as Eureka Forbes, Kent RO Systems, HUL Pureit, LivPure, and A.O. Smith in R&D, manufacturing capacity, smart IoT product lines, and AMC service networks are strengthening local supply and supporting the India residential water purifier market forecast 2032.

Key Market Drivers: India Residential Water Purifier Market

Declining Groundwater Quality, Rising TDS Levels, and Urban Water Contamination Driving India Residential Water Purifier Market Adoption

Growth in the India residential water purifier market is being driven by deteriorating groundwater quality and rising water contamination across urban and semi-urban India. The Central Ground Water Board (CGWB) reports that approximately 71% of districts in India have groundwater contamination from fluoride, nitrate, arsenic, iron, or heavy metals, while TDS (Total Dissolved Solids) levels in major metros now routinely exceed 500 ppm, well above the WHO drinking water guideline. Urban centres including Delhi NCR, Mumbai, Bengaluru, Hyderabad, Pune, Chennai, and Jaipur face documented water-quality challenges, with hardness, microbial contamination, and pesticide residues frequently reported. The Bureau of Indian Standards (BIS) IS 10500:2012 drinking water specification mandates strict potable water parameters, fuelling household-level water treatment adoption across the India residential water purifier market. India’s piped water coverage under Jal Jeevan Mission has expanded to over 79% of rural households by 2025, but raw water quality concerns persist. Combined with the National Centre for Disease Control reporting over 1.4 million water-borne illness cases annually, demand for residential RO, UV, and UF purifiers continues to scale across the India residential water purifier market through 2032.

Rising Disposable Income, Urbanisation, and Health Awareness Boosting Premium Water Purifier Demand in India

The India residential water purifier market is benefiting from rising disposable income, accelerating urbanisation, and heightened consumer health consciousness. India’s urban population is projected to reach 600 million by 2031, with per capita disposable income growing at 7 to 8% annually, supporting upgrade-cycle demand from gravity-based and standalone candle filters toward branded RO, UV, and UF residential water purifier systems. Premium residential water purifier penetration in India is estimated at only 12 to 14% of urban households, against 65 to 70% in metros of comparable Asian economies, indicating significant headroom for premium upgrade across the India residential water purifier market. Leading brands including Eureka Forbes Aquaguard, Kent RO Systems, HUL Pureit, LivPure, A.O. Smith, and Havells have launched premium segments priced INR 20,000 to 50,000 with copper-infused, alkaline-mineral, mineral guard, hot and cold dispensing, and smart IoT-connected models targeting affluent urban consumers. Increased post-pandemic health awareness, growing nuclear family lifestyles, and rising spend on home consumer durables (now 4.5 to 5.0% of urban household income) are reinforcing residential water purifier market premiumisation across metros and tier-1 cities of India through 2032.

Expansion of E-Commerce, Smart IoT-Connected Water Purifiers, and D2C Platforms Strengthening India Residential Water Purifier Market

Rapid expansion of online channels and digital purchase platforms is a major catalyst for the India residential water purifier market, with e-commerce now contributing an estimated 32 to 36% of total water purifier sales. Online platforms including Amazon India, Flipkart, Croma, Reliance Digital, Tata Neu, and brand D2C websites such as KentRO.com, Aquaguard.com, and Livpure.com have scaled assortment across budget, mid-range, and premium residential water purifier ranges. Indian consumers are increasingly purchasing water purifiers online based on third-party certifications, BIS markings, product reviews, and EMI-led financing offers. Smart IoT-connected residential water purifiers with mobile app integration, real-time water quality monitoring, filter-life indicators, and AMC scheduling are gaining strong traction in metros, with Kent ZWW, A.O. Smith X-Series, LivPure Smart Connect, and HUL Pureit Eco range leading the connected category. Subscription-based AMC models, doorstep filter replacement, and digital service platforms are accelerating customer retention and lifetime value, broadening the India residential water purifier market reach across metros, tier-1, and emerging tier-2 cities through 2032.

Key Market Challenges: India Residential Water Purifier Market

High Upfront Cost, Recurring Filter Replacement, and AMC Pricing Restricting Tier-2 and Tier-3 City Penetration of India Residential Water Purifier Market

The India residential water purifier market continues to face significant pricing barriers, particularly for premium RO and smart IoT-connected models. Branded residential water purifiers from Aquaguard, Kent, HUL Pureit, LivPure, A.O. Smith, and Havells range between INR 8,000 and 50,000, with premium models priced INR 25,000 to 50,000, placing them out of reach for the average Indian household earning below INR 5 lakh annual income. Annual AMC contracts cost INR 2,500 to 6,000, and recurring filter replacement, including RO membrane, sediment, and carbon filters, costs INR 1,500 to 4,000 per cycle (typically annual), adding to total cost of ownership across the India residential water purifier market. Middle-class and lower-middle-class Indian households remain price-sensitive, with many still relying on boiling, chlorine tablets, candle filters, or unbranded local water purifiers. Tier-2 and tier-3 city distribution gaps, limited service network coverage of premium brands, and dependence on AMC-based pricing models continue to restrict penetration of the India residential water purifier market across smaller cities, semi-urban, and rural regions of India through 2032.

Water Wastage from RO Purifiers and Growing Environmental Concerns Limiting India Residential Water Purifier Market Growth

A growing environmental and sustainability challenge facing the India residential water purifier market is the high water wastage rate associated with conventional reverse osmosis (RO) systems, which typically reject 50 to 80% of input water as wastewater. In a country facing acute water scarcity, where the NITI Aayog Composite Water Management Index reports that 21 Indian cities including Bengaluru, Hyderabad, Chennai, and Delhi face severe water stress, the rejected water from RO purifiers raises significant sustainability concerns. The National Green Tribunal (NGT) directed in 2019 and reiterated through 2024 that RO purifiers should not be used where TDS levels are below 500 ppm, and mandated water-recovery rates above 60% for new RO purifiers across the India residential water purifier market. The Bureau of Indian Standards has subsequently introduced revised specifications under IS 16240 for residential RO water purifiers, requiring minimum 50% water recovery, posing reformulation and product redesign requirements for manufacturers. Compliance costs, consumer education on appropriate technology selection across RO, UV, and UF categories, and the gradual transition to low-wastage RO systems continue to be near-term execution challenges for the India residential water purifier market.

Counterfeit Products, Unorganised Local Players, and Weak BIS Quality Enforcement Creating India Residential Water Purifier Market Fragmentation

The India residential water purifier market remains highly fragmented, with a significant share of category sales attributed to unbranded, locally assembled, and counterfeit water purifier products operating without BIS certification or compliance oversight. Industry estimates suggest that unorganised and counterfeit residential water purifier products account for 22 to 26% of total market volumes, primarily concentrated in tier-2 and tier-3 cities, semi-urban markets, and price-sensitive consumer segments. Branded players including Eureka Forbes, Kent RO Systems, HUL Pureit, LivPure, and A.O. Smith have repeatedly raised concerns around counterfeit Aquaguard and Kent-branded products, fake spare parts, and substandard RO membranes flooding online and offline channels of the India residential water purifier market. The Bureau of Indian Standards has introduced IS 16240 standard for residential RO purifiers and BIS-mandated quality marking, but enforcement remains uneven across states, with limited consumer awareness about authenticated dealer networks. Lack of mandatory minimum water quality certification, weak post-sale service standards, and counterfeit spare parts continue to fragment the India residential water purifier market and limit consumer confidence across tier-2 and tier-3 cities of India through 2032.

Key Market Trends: India Residential Water Purifier Market

Rapid Adoption of Smart IoT-Connected, Alkaline-Mineral, and Copper-Infused Residential Water Purifiers in India

The India residential water purifier market is undergoing a clear technology shift toward smart IoT-connected, alkaline-mineral, copper-infused, and hot/cold dispensing models, with these advanced technologies expected to capture over 28% of new water purifier installations by 2028. Smart connected water purifiers from Kent ZWW, A.O. Smith X-Series, LivPure Smart Connect, HUL Pureit Eco, and Aquaguard Glory now offer real-time water quality monitoring, filter-life indicators, mobile app integration, and AMC scheduling through companion applications. Alkaline-mineral and copper-infused residential water purifier variants, retailing at INR 18,000 to 45,000, are gaining strong traction across metros as consumers seek health-positioning benefits. Brands including LivPure Copper Guard, Aquaguard Marvel, Kent Supreme Alkaline, and Havells Max Alkaline have aligned product portfolios to this premium technology mix. This technology transition, combined with rising consumer willingness to invest in connected residential wellness, is reinforcing the India residential water purifier market forecast 2032 across premium urban and metro residential segments.

Growth of Subscription-Based AMC, Doorstep Filter Replacement, and Service-as-a-Subscription Models in India Residential Water Purifier Market

A clear shift toward subscription-based annual maintenance contracts (AMC), doorstep filter replacement, and service-as-a-subscription business models is reshaping the India residential water purifier market, particularly in metros and tier-1 cities. Leading brands including Eureka Forbes, Kent RO Systems, HUL Pureit, LivPure, A.O. Smith, and Havells now offer multi-year AMC packages priced INR 2,500 to 6,000 per year, including doorstep filter replacement, sediment and RO membrane changes, sanitisation, and 24×7 customer service. Eureka Forbes has built an installed base of over 21 million water purifier customers across India, with AMC and after-sales services contributing a growing share of recurring revenue. Online aggregators and service-on-demand platforms such as Urban Company, NoBroker, and brand-led digital service applications are also reducing customer acquisition costs and accelerating residential water purifier adoption across both replacement and first-time buyer segments of the India residential water purifier market.

Capacity Expansion by Domestic Brands, D2C Distribution, and Vertical Integration of Membrane and Filter Manufacturing

A wave of D2C investment, capacity expansion, and vertical integration is reshaping the India residential water purifier market supply landscape. Combined India-focused capital expenditure announcements by Eureka Forbes, Kent RO Systems, HUL Pureit, LivPure, A.O. Smith, and Havells exceeded USD 220 million between 2022 and 2025. Eureka Forbes, under Lunolux Limited and Advent International ownership since 2022, has scaled R&D and manufacturing across Hyderabad and Bhiwadi facilities. Kent RO Systems operates major manufacturing plants at Noida and Roorkee, while A.O. Smith expanded its Bengaluru facility for premium RO and hot water solutions. HUL Pureit, leveraging Hindustan Unilever’s pan-India distribution, has scaled across over 5,000 retail touchpoints and online channels. Domestic membrane, filter, and RO component manufacturing under Production Linked Incentive (PLI) and Make-in-India incentives is gradually reducing import dependence on Chinese and South Korean RO membranes. Combined with rising premium urban demand and expanding tier-2 city penetration, these developments are reinforcing the India residential water purifier market forecast 2032 across the entire value chain.

Segmental Insights: India Residential Water Purifier Market

By Technology: RO and RO+UV+UF Combination Dominate the India Residential Water Purifier Market

Reverse osmosis (RO) and RO+UV+UF combination water purifiers lead the India residential water purifier market technology landscape, accounting for an estimated 62 to 65% of total installed units, driven by deteriorating groundwater quality, rising TDS levels above 500 ppm across major metros, and growing consumer preference for multi-stage purification. RO and RO+UV+UF combination water purifiers are the dominant technology category across Aquaguard, Kent, HUL Pureit, LivPure, A.O. Smith, and Havells portfolios. Standalone UV and UF water purifiers contribute another 18 to 22% of the India residential water purifier market, primarily in regions with relatively lower TDS such as coastal Maharashtra, parts of Kerala, and select metros. Gravity-based and activated carbon water purifiers account for 10 to 14% of the India residential water purifier market, led by HUL Pureit Classic, Kent Gold, and Tata Swach in budget and rural segments. In 2025, leading water purifier brands including Eureka Forbes Aquaguard, Kent RO Systems, HUL Pureit, LivPure, and A.O. Smith scaled up smart IoT-connected, alkaline-mineral, and copper-infused premium ranges, reinforcing segment dominance in the India residential water purifier market.

By Distribution Channel: Online E-Commerce Grows Fastest While Specialty Retail Leads Volume

Specialty stores and direct selling networks continue to lead the India residential water purifier market by total volume, accounting for approximately 42 to 46% of total water purifier sales, driven by branded dealer networks of Eureka Forbes, Kent RO Systems, HUL Pureit, LivPure, and A.O. Smith across India’s tier-1 and tier-2 cities. Online e-commerce is the fastest growing distribution channel within the India residential water purifier market, expanding at 22 to 26% annually, with Amazon India, Flipkart, Croma, Reliance Digital, Tata Neu, and brand D2C platforms now contributing 32 to 36% of total sales. Hypermarkets and modern retail, including Reliance Smart, Tata Croma, and More Retail, account for another 15 to 18% of the India residential water purifier market, primarily in metros and tier-1 cities. Direct selling, a traditional Eureka Forbes strength, contributes around 8 to 10% of category volume. Leading brands have aligned omni-channel strategies, with growing investment in digital marketing, EMI financing, and doorstep AMC services, driving premium residential water purifier adoption across the India residential water purifier market.

Regional Insights: India Residential Water Purifier Market

Regional analysis of the India residential water purifier market shows that South India and West India collectively account for approximately 55 to 58% of total water purifier sales, driven by Karnataka, Tamil Nadu, Telangana, Andhra Pradesh, Kerala, Maharashtra, and Gujarat, supported by high urbanisation, growing apartment population, and concentrated metro consumer demand. North India contributes around 26 to 28% of demand, led by Delhi NCR, Punjab, Haryana, Uttar Pradesh, and Rajasthan, supported by acute groundwater contamination concerns (high TDS, fluoride, arsenic) and rising health-conscious household purchases. Central and East India together account for 16 to 18% of demand, supported by Madhya Pradesh, Chhattisgarh, West Bengal, Bihar, and Odisha, where Jal Jeevan Mission-led awareness and rising tier-2 city affluence are accelerating residential water purifier adoption. In 2025, capacity additions and dealer expansion by Eureka Forbes across Karnataka, Tamil Nadu, and Maharashtra, Kent RO Systems across Delhi NCR and Uttar Pradesh, HUL Pureit across pan-India FMCG distribution, and A.O. Smith across Bengaluru and Hyderabad reinforced regional supply hubs, supporting closer execution of premium and smart IoT-connected residential water purifier offerings across the India residential water purifier market.

Recent Developments: India Residential Water Purifier Market

- The India residential water purifier market witnessed strong momentum in product launches and capacity expansion during 2024 and 2025. Eureka Forbes, under Lunolux and Advent International ownership since 2022, launched Aquaguard Glory and Aquaguard Marvel smart IoT-connected ranges, while Kent RO Systems introduced Kent Supreme Alkaline and Kent ZWW Smart Connect. LivPure launched LivPure Smart Connect with copper guard, and A.O. Smith expanded its X-Series and hot/cold dispensing premium range. Combined product launches and category innovation are strengthening the India residential water purifier market across the premium segment.

- Domestic water purifier brands have deepened India-focused capacity expansion. In 2025, Eureka Forbes scaled R&D and manufacturing at Hyderabad and Bhiwadi facilities, Kent RO Systems expanded Noida and Roorkee manufacturing, A.O. Smith expanded its Bengaluru plant, HUL Pureit leveraged Hindustan Unilever’s pan-India distribution across over 5,000 retail touchpoints, and LivPure scaled D2C and online distribution. Domestic RO membrane and filter manufacturing under Production Linked Incentive scheme allocations is gradually reducing import dependence, strengthening domestic supply and supporting the India residential water purifier market forecast 2032.

- E-commerce and AMC subscription momentum has gained strong traction across the India residential water purifier market. In 2025, leading brands including Eureka Forbes, Kent RO Systems, HUL Pureit, LivPure, A.O. Smith, and Havells expanded multi-year AMC packages, doorstep filter replacement subscriptions, and EMI-led online financing. Strategic partnerships between water purifier brands, e-commerce platforms such as Amazon India and Flipkart, and digital service platforms including Urban Company are positioning India as one of the most actively scaling residential water purifier markets in Asia, strengthening long-term competitive positioning in the India residential water purifier market forecast 2032.

Key Market Players: India Residential Water Purifier Market

- Eureka Forbes Limited (Aquaguard)

- Kent RO Systems Limited

- Hindustan Unilever Limited (HUL Pureit)

- LivPure Pvt. Ltd. (Sar Group)

- O. Smith India Water Products Pvt. Ltd.

- Havells India Limited

- Blue Star Limited

- Whirlpool of India Limited

- LG Electronics India Pvt. Ltd.

- Faber India (Franke Faber India Pvt. Ltd.)

- Bosch Limited

- Crompton Greaves Consumer Electricals Ltd.

- Panasonic India Pvt. Ltd.

Report Scope

In this report, the India Residential Water Purifier Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

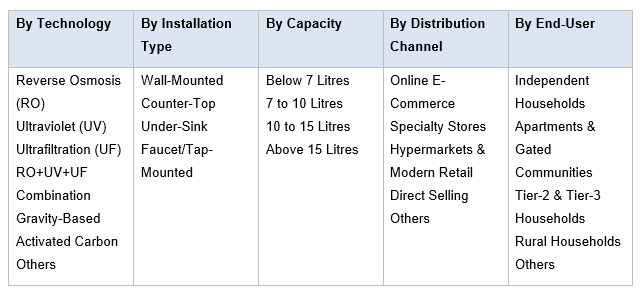

- By Technology

- Reverse Osmosis (RO)

- Ultraviolet (UV)

- Ultrafiltration (UF)

- RO+UV+UF Combination

- Gravity-Based

- Activated Carbon

- Others

- By Installation Type

- Wall-Mounted

- Counter-Top

- Under-Sink

- Faucet/Tap-Mounted

- By Capacity

- Below 7 Litres

- 7 to 10 Litres

- 10 to 15 Litres

- Above 15 Litres

- By Distribution Channel

- Online E-Commerce

- Specialty Stores

- Hypermarkets & Modern Retail

- Direct Selling

- Others

- By End-User

- Independent Households

- Apartments & Gated Communities

- Tier-2 & Tier-3 Households

- Rural Households

- Others

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Residential Water Purifier Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging D2C water purifier brands, specialty alkaline-mineral and copper-infused purifier producers, smart IoT-connected residential water purifier developers, or niche tier-2 city distributors operating across the India residential water purifier market.

The India Residential Water Purifier Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Technology

- By Installation Type

- By Capacity

- By Distribution Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Residential Water Purifier Market

- India Residential Water Purifier Market Insights

- Market Dynamics

- Growth Drivers

- Declining groundwater quality, rising TDS levels, and urban water contamination driving India residential water purifier market adoption.

- Rising disposable income, urbanisation, and health awareness boosting premium water purifier demand in India.

- Expansion of e-commerce, smart IoT-connected water purifiers, and D2C platforms strengthening India residential water purifier market.

- Restraints

- High upfront cost, recurring filter replacement, and AMC pricing restricting tier-2 and tier-3 city penetration.

- Water wastage from RO purifiers (50-80% reject water) and environmental concerns limiting category growth.

- Counterfeit products, unorganised local players, and weak BIS quality enforcement creating market fragmentation.

- Opportunities

- Tier-2, tier-3, and rural India penetration under Jal Jeevan Mission creating long-term residential water purifier market opportunity.

- Smart IoT-connected, alkaline-mineral, copper-infused, and hot/cold dispensing water purifiers opening new premium value pools.

- Eco-friendly low-wastage RO technologies, UV-LED purification, and subscription-based AMC models supporting next-generation growth.

- Challenges

- Slow tier-2 and tier-3 city adoption of premium and smart IoT-connected residential water purifiers restricting near-term growth.

- Limited skilled service workforce, AMC technicians, and certified installers across India residential water purifier market.

- Inconsistent BIS enforcement, counterfeit Aquaguard and Kent products, and weak post-sale service standards across smaller cities.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (RO membranes, UV lamps, activated carbon, polypropylene, PVDF, food-grade plastics)

- RO Membrane & Filter Component Manufacturers (Dow, Toray, LG Chem, Aquadyne, domestic Indian suppliers)

- UV Lamp & UV-LED Component Suppliers (Philips, Osram, domestic UV-LED makers)

- Smart IoT & Mobile App Platform Developers (Kent ZWW, A.O. Smith X-Series, LivPure Smart Connect)

- Quality Control, R&D & Water Testing Laboratories (BIS, NABL, WHO IS 10500:2012 compliance)

- Distributors, Dealers & Online Aggregators (Amazon India, Flipkart, Croma, Reliance Digital, Tata Neu)

- Branded Water Purifier OEMs (Eureka Forbes, Kent, HUL Pureit, LivPure, A.O. Smith, Havells)

- Direct-to-Consumer Brand Websites (KentRO.com, Aquaguard.com, Livpure.com)

- Service Network, AMC & Filter Replacement Technicians (brand-authorised dealers, Urban Company, NoBroker)

- End-Users (Independent Households, Apartments & Gated Communities, Tier-2 & Tier-3 Households)

- India Residential Water Purifier Market: Regulatory Framework

- India Residential Water Purifier Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Million Units Sold)

- Market Share & Forecast

- By Technology

- Reverse Osmosis (RO)

- Ultraviolet (UV)

- Ultrafiltration (UF)

- RO+UV+UF Combination

- Gravity-Based

- Activated Carbon

- Others

- By Installation Type

- Wall-Mounted

- Counter-Top

- Under-Sink

- Faucet/Tap-Mounted

- By Capacity

- Below 7 Litres

- 7 to 10 Litres

- 10 to 15 Litres

- Above 15 Litres

- By Distribution Channel

- Online E-Commerce

- Specialty Stores

- Hypermarkets & Modern Retail

- Direct Selling

- Others

- By End-User

- Independent Households

- Apartments & Gated Communities

- Tier-2 & Tier-3 Households

- Rural Households

- Others

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Residential Water Purifier Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Eureka Forbes Limited (Aquaguard)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Eureka Forbes Limited (Aquaguard)

(Same Data Pointers Will Be Provided for The Below Companies)

- Kent RO Systems Limited

- Hindustan Unilever Limited (HUL Pureit)

- LivPure Pvt. Ltd. (Sar Group)

- O. Smith India Water Products Pvt. Ltd.

- Havells India Limited

- Blue Star Limited

- Whirlpool of India Limited

- LG Electronics India Pvt. Ltd.

- Faber India (Franke Faber India Pvt. Ltd.)

- Bosch Limited

- Crompton Greaves Consumer Electricals Ltd.

- Panasonic India Pvt. Ltd.

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable