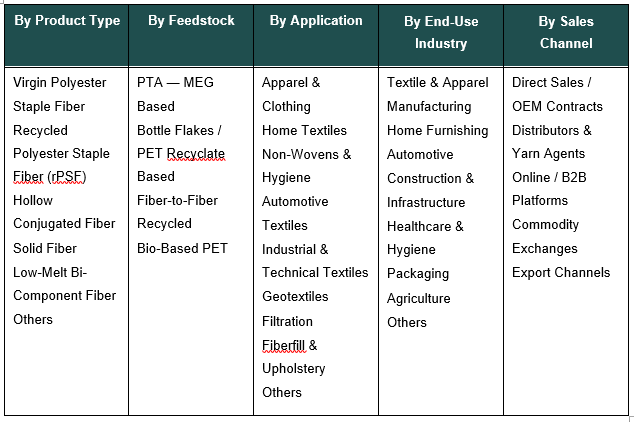

India Polyester Staple Fiber Market, By Product Type (Virgin Polyester Staple Fiber, Recycled Polyester Staple Fiber (rPSF), Hollow Conjugated Fiber, Solid Fiber, Low-Melt Bi-Component Fiber, Others); By Denier (Below 1.4 D, 1.4–2 D, 2–6 D, 6–15 D, Above 15 D); By Cut Length (Below 32 mm, 32–38 mm, 38–51 mm, 51–76 mm, Above 76 mm); By Color (Raw White, Dyed / Dope-Dyed, Optical White, Black, Others); By Finish (Semi-Dull, Bright, Super Bright, Trilobal); By Feedstock (PTA — MEG Based, Bottle Flakes / PET Recyclate Based, Fiber-to-Fiber Recycled, Bio-Based PET); By Application (Apparel & Clothing, Home Textiles, Non-Wovens & Hygiene, Automotive Textiles, Industrial & Technical Textiles, Geotextiles, Filtration, Fiberfill & Upholstery, Others); By End-Use Industry (Textile & Apparel Manufacturing, Home Furnishing, Automotive, Construction & Infrastructure, Healthcare & Hygiene, Packaging, Agriculture, Others); By Sales Channel (Direct Sales / OEM Contracts, Distributors & Yarn Agents, Online / B2B Platforms, Commodity Exchanges, Export Channels); By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Chemicals & Advanced Materials

- Apr 2026

- Pages 160

- Report Format: pdf

- Report Price: $1800 USD

India Polyester Staple Fiber Market: Technical Textiles Boom Meets Recycled PSF and Circular-Economy Shift, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

| Market Size (2025) | USD 4.25 Billion |

| CAGR (2026-2032) | 8.8% |

| Leading Segment | Virgin PSF for Spinning & Apparel |

| Fastest Growing Segment | Recycled PSF (rPSF) |

| Market Size (2032) | USD 7.68 Billion |

Source: Market Research Outlook

Market Overview — India Polyester Staple Fiber Market

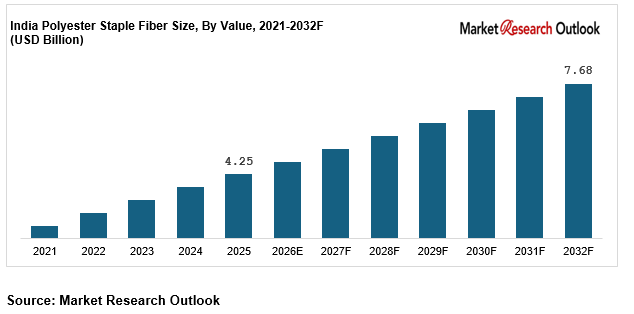

The India polyester staple fiber market is expanding steadily, supported by the growth of technical textiles, non-wovens, and rising demand across apparel and home textiles. The India Polyester Staple Fiber Market is valued at USD 4.25 billion in 2025 and is projected to reach USD 7.68 billion by 2032, growing at a CAGR of 8.8 percent.

Demand is being driven by spinners, non-woven manufacturers, automotive OEMs, and global apparel brands, with increasing emphasis on performance, cost efficiency, and supply reliability. While virgin PSF continues to dominate overall consumption, recycled polyester staple fiber is emerging as the fastest-growing segment.

The supply landscape is also evolving. Expansion in PET bottle collection under EPR norms, early-stage fiber-to-fiber recycling initiatives, and wider adoption of dope-dyed fiber are reshaping how PSF is produced and sourced in India. At the same time, producers such as Reliance Industries, Indo Rama Synthetics, JBF Industries, Ganesha Ecosphere, and Filatex India are scaling capacity to meet both domestic and export demand.

Overall, the market is gradually transitioning toward a more sustainability-driven and application-focused structure, with growing relevance in export markets and technical textile applications.

Key Report Takeaways — India Polyester Staple Fiber Market

- The India polyester staple fiber market is projected to grow from USD 4.25 billion in 2025 to USD 7.68 billion by 2032, at a CAGR of 8 percent, supported by expanding technical textiles, steady growth in apparel and home textiles, and increasing adoption of recycled fiber.

- Recycled polyester staple fiber (rPSF) is the fastest-growing segment, expected to expand at 14 to 16 percent annually, driven by global brand commitments toward recycled content and more sustainable sourcing practices.

- Policy support through the PLI scheme, PM MITRA parks, and the National Technical Textiles Mission is strengthening domestic manufacturing, with companies such as Reliance Industries, Indo Rama, Ganesha Ecosphere, and JBF Industries expanding capacity.

- Demand from non-wovens, hygiene products, automotive interiors, and geotextiles is rising, with technical textile applications expected to contribute over 30 percent of total demand by 2032, up from around 22 percent in 2025.

- Investments in fiber-to-fiber recycling, dope-dyed PSF, and specialty fibers such as low-melt bi-component products are improving product differentiation and supporting India’s position as a competitive PSF manufacturing and export base.

Key Market Drivers — India Polyester Staple Fiber Market

Expansion of Technical Textiles and Non-Wovens Driving PSF Demand in India

Growth in the India polyester staple fiber market is being supported by the steady expansion of the technical textiles and non-wovens segment, which is growing at around 11 to 13 percent annually. Government initiatives such as the National Technical Textiles Mission and PLI scheme are accelerating investments, with the broader technical textiles market expected to approach USD 50 billion by 2030.

Polyester staple fiber plays a central role across applications including hygiene products, automotive interiors, geotextiles, medical textiles, and filtration media. Demand is increasing for specialised fiber types such as hollow conjugated fiber, low-melt bi-component fiber, and customised denier variants used in spunbond, meltblown, and needle-punched non-woven processes.

On the ground, rising production of products such as diapers, sanitary napkins, wipes, and filtration materials is directly translating into higher and more consistent fiber consumption. This shift is gradually making technical textiles and non-wovens a more stable and high-growth demand segment within the overall market.

Adoption of Recycled Polyester Staple Fiber and Circular Economy Mandates

Recycled polyester staple fiber (rPSF) is becoming a central growth driver in the India polyester staple fiber market, currently accounting for around 28 to 30 percent of total consumption and expected to exceed 40 percent by 2032.

This shift is being driven by global apparel and home-textile brands committing to higher recycled content, alongside India’s Extended Producer Responsibility (EPR) norms, which are improving PET bottle collection and feedstock availability. As a result, recycled fiber is moving from a niche segment to a mainstream sourcing requirement.

India has also emerged as a key production hub for rPSF, with companies such as Ganesha Ecosphere, Reliance Industries (Recron Green Gold), JB Ecotex, and Shakti Polyweave expanding capacity to meet both domestic and export demand.

This transition toward circularity is not only changing raw material sourcing but also influencing pricing structures, supply chains, and long-term competitiveness across the market.

Government-Led PLI Support, MITRA Parks, and Domestic PSF Capacity Expansion

Government initiatives such as the Production Linked Incentive (PLI) scheme for man-made fibers and technical textiles, along with PM MITRA parks and ATUFS, are supporting long-term growth in the India polyester staple fiber market.

Investment activity has been strong, with India-focused announcements in PSF capacity, recycling infrastructure, and downstream technical textiles exceeding USD 2.5 billion between 2023 and 2025. This reflects growing confidence in both domestic demand and export potential.

Leading producers including Reliance Industries, Indo Rama Synthetics, JBF Industries, Bombay Dyeing, Ganesha Ecosphere, and Filatex India are expanding across virgin, recycled, and specialty fiber categories, strengthening overall supply capability.

At the same time, measures such as anti-dumping duties on select imports and Quality Control Orders (QCOs) are supporting domestic manufacturers by improving price competitiveness and reducing reliance on imports.

Key Market Challenges — India Polyester Staple Fiber Market

Feedstock Price Volatility Impacting Margins

The India polyester staple fiber market remains highly exposed to fluctuations in key petrochemical feedstocks such as purified terephthalic acid (PTA) and mono-ethylene glycol (MEG), which together account for 75 to 80 percent of input costs for virgin PSF. Movements in crude oil prices, typically ranging between USD 70 to USD 95 per barrel over the past two years, have resulted in 20 to 30 percent swings in feedstock costs, directly affecting producer margins.

This volatility makes pricing less predictable and complicates long-term supply agreements with spinners and non-woven manufacturers. Partial dependence on imported PTA further adds to this exposure. In response, producers are focusing on backward integration, securing long-term contracts, and increasing the share of recycled PSF, which is relatively less sensitive to crude-linked pricing.

Substitution Pressure from Alternative Fibers

Polyester staple fiber is facing increasing competition from cotton, viscose staple fiber (VSF), and emerging bio-based alternatives, particularly in segments such as apparel and home textiles. Consumer preference for natural and breathable materials, along with growing awareness around microplastic concerns, is influencing purchasing decisions in certain markets.

Viscose, supported by domestic production, is positioning itself as a more sustainable option, while bio-based fibers are gradually gaining attention. Although PSF continues to offer advantages in cost, durability, and scalability, this shift in perception is pushing manufacturers to focus more on recycled content, traceability, and product innovation.

Rising Compliance and Environmental Costs

Environmental regulations are becoming more stringent, adding to operational complexity and cost. Compliance with CPCB norms, wastewater treatment requirements, and Zero Liquid Discharge (ZLD) mandates is increasing production costs by an estimated 8 to 12 percent.

In addition, export markets are introducing stricter requirements around sustainability reporting, carbon disclosures, and product traceability. Recycled PSF producers also face challenges in building efficient collection and sorting systems for PET feedstock.

While these factors increase short-term cost pressures, they are also raising entry barriers and favouring larger, integrated players with stronger compliance and technology capabilities.

Key Market Trends — India Polyester Staple Fiber Market

Scale-Up of Recycled PSF and Early Progress in Fiber-to-Fiber Recycling

The India polyester staple fiber market is seeing a rapid increase in recycled fiber capacity, with rPSF expanding at around 18 to 22 percent annually, significantly faster than virgin fiber.

This growth is being supported by stronger PET bottle collection under EPR norms, with collection volumes reaching an estimated 2.4 to 2.7 million tonnes annually, improving feedstock availability. At the same time, early-stage fiber-to-fiber recycling initiatives are beginning to take shape, enabling conversion of textile waste into new fiber.

Producers such as Ganesha Ecosphere, Reliance Industries, JB Ecotex, and Shakti Polyweave have expanded capacity in response to both domestic and export demand, indicating a broader shift toward circular production models.

Shift Toward Specialty and Value-Added Fiber Formats

The market is gradually moving toward higher-value and application-specific fiber formats, including dope-dyed, low-melt bi-component, and hollow conjugated PSF.

Dope-dyed fiber is gaining traction due to its ability to reduce water and energy usage by eliminating downstream dyeing processes. Low-melt fibers are increasingly used in thermal-bonded non-wovens and automotive interiors, while hollow fibers are widely adopted in fiberfill and home-textile applications.

This shift reflects a move away from standard commodity grades toward more differentiated products, particularly in segments where performance and sustainability requirements are becoming more important.

Export-Oriented Growth and Policy-Driven Industry Expansion

The India polyester staple fiber market is also benefiting from stronger export orientation and policy support. Government initiatives such as the PLI scheme, PM MITRA parks, and ATUFS are encouraging investment across the textile value chain.

PSF exports are growing at around 12 to 14 percent annually, supported by demand from the US, Europe, the Middle East, and Southeast Asia. Trade agreements with markets such as the UAE and Australia, along with ongoing negotiations with the EU, are further improving export access.

As a result, India is gradually strengthening its position as a competitive manufacturing and sourcing base for polyester staple fiber, particularly in recycled and specialty segments.

Segmental Insights — India Polyester Staple Fiber Market

By Application — Apparel Leads While Technical Textiles Gain Share

Apparel and clothing remain the largest application segment, accounting for approximately 42 to 46 percent of total PSF consumption, supported by strong spinning capacity, growth in blended yarns, and steady demand in value and mid-market apparel.

Home textiles and fiberfill contribute around 22 to 25 percent, driven by both domestic consumption and export demand from large global retailers. At the same time, non-wovens and hygiene applications are among the fastest-growing segments, expanding at 13 to 15 percent annually, supported by rising use of diapers, sanitary products, wipes, and automotive interior materials.

Over time, technical textile applications are expected to increase their share to over 30 percent of total demand by 2032, reflecting a gradual shift toward more diversified and application-driven consumption.

By Product Type — Virgin PSF Dominates, Recycled Fiber Drives Growth

Virgin polyester staple fiber continues to account for the majority of consumption, with a share of approximately 68 to 72 percent, supported by large-scale integrated production across key domestic manufacturers.

However, recycled PSF is steadily gaining share, currently contributing around 28 to 30 percent and expected to exceed 40 percent by 2032. This growth is being driven by increasing demand for recycled content and more structured collection of PET feedstock.

Specialty fiber categories, including hollow conjugated, low-melt bi-component, and dope-dyed PSF, account for roughly 8 to 10 percent of the market and are growing at a faster pace, particularly in technical textiles and premium home furnishing applications.

Regional Insights — India Polyester Staple Fiber Market

West and South India together account for the largest share of production and consumption, contributing approximately 62 to 66 percent of total demand. This is supported by integrated manufacturing facilities in Gujarat and Maharashtra, along with strong textile clusters in Tamil Nadu and southern states.

North India contributes around 18 to 22 percent, driven by established textile hubs such as Panipat and Ludhiana, along with growing demand from non-wovens and hygiene manufacturing.

East and Central India account for 14 to 18 percent, supported by regional textile activity and emerging industrial developments under initiatives such as PM MITRA.

Recent capacity expansions by major producers have further strengthened these regional clusters, improving supply efficiency and enabling closer alignment with downstream industries including spinning, non-wovens, and technical textiles.

Recent Developments — India Polyester Staple Fiber Market

Recent Developments — India Polyester Staple Fiber Market

- The India polyester staple fiber market has seen strong activity in recycled fiber capacity expansion and specialty product development during 2024 and 2025. Reliance Industries expanded its Recron Green Gold portfolio, Ganesha Ecosphere added new rPSF capacity across key locations, and JB Ecotex scaled fiber-to-fiber recycling. At the same time, producers are expanding into dope-dyed, hollow conjugated, and low-melt fibers, strengthening India’s position as a diversified PSF manufacturing base.

- Global apparel and home-textile brands are increasing sourcing from India, particularly for recycled and specialty fibers. Companies such as H&M, Zara, Marks & Spencer, IKEA, Target, and Walmart have expanded long-term supplier relationships, while domestic players including Welspun, Trident, and Indo Count are scaling production in line with rising demand from non-wovens, home textiles, and technical applications.

- Policy support continues to play an important role in shaping the market. Progress under the PLI scheme, development of PM MITRA parks, and implementation of Quality Control Orders are supporting domestic manufacturing. At the same time, anti-dumping measures and trade agreements with markets such as the UAE and Australia are improving export competitiveness and strengthening India’s position in global PSF supply chains.

Key Market Players — India Polyester Staple Fiber Market

- Reliance Industries Limited (Recron, Recron Green Gold)

- Indo Rama Synthetics (India) Limited

- Bombay Dyeing and Manufacturing Company Limited

- JBF Industries Limited

- Ganesha Ecosphere Limited

- Filatex India Limited

- Alok Industries Limited

- JB Ecotex Limited

- Shakti Polyweave Pvt. Ltd.

- Pashupati Polytex Pvt. Ltd.

- Nirmal Fibers (P) Ltd.

- Polygenta Technologies Limited

Report Scope

In this report, the India Polyester Staple Fiber Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Virgin Polyester Staple Fiber

- Recycled Polyester Staple Fiber (rPSF)

- Hollow Conjugated Fiber

- Solid Fiber

- Low-Melt Bi-Component Fiber

- Others

- By Denier

- Below 1.4 D

- 4–2 D

- 2–6 D

- 6–15 D

- Above 15 D

- By Cut Length

- Below 32 mm

- 32–38 mm

- 38–51 mm

- 51–76 mm

- Above 76 mm

- By Color

- Raw White

- Dyed / Dope-Dyed

- Optical White

- Black

- Others

- By Finish

- Semi-Dull

- Bright

- Super Bright

- Trilobal

- By Feedstock

- PTA — MEG Based

- Bottle Flakes / PET Recyclate Based

- Fiber-to-Fiber Recycled

- Bio-Based PET

- By Application

- Apparel & Clothing

- Home Textiles

- Non-Wovens & Hygiene

- Automotive Textiles

- Industrial & Technical Textiles

- Geotextiles

- Filtration

- Fiberfill & Upholstery

- Others

- By End-Use Industry

- Textile & Apparel Manufacturing

- Home Furnishing

- Automotive

- Construction & Infrastructure

- Healthcare & Hygiene

- Packaging

- Agriculture

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Yarn Agents

- Online / B2B Platforms

- Commodity Exchanges

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Polyester Staple Fiber Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic PSF producers, recycled fiber specialists, global entrants, or niche segment leaders.

The India Polyester Staple Fiber Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021–2032

- By Product Type

- By Application

- By End-Use Industry

- By Feedstock

- By Sales Channel

- By Region

- Analyst Recommendations

- Market Overview, 2021–2032

- Geopolitical Impact on India Polyester Staple Fiber Market

- India Polyester Staple Fiber Market Insights

- Market Dynamics

- Growth Drivers

- Rapid expansion of technical textiles and non-wovens driving structural polyester staple fiber demand.

- Accelerated adoption of recycled polyester staple fiber (rPSF) and circular-economy mandates from global brands.

- Government-led PLI support, MITRA parks, and domestic PSF capacity expansion reducing import dependence.

- Restraints

- PTA and MEG feedstock price volatility linked to crude oil pressuring PSF producer margins.

- Substitution pressure from cotton, viscose, and emerging bio-based fibers constraining PSF share in apparel.

- Environmental compliance, effluent management, and EPR obligations raising PSF manufacturing compliance costs.

- Opportunities

- Rapidly expanding export opportunity for recycled PSF and specialty PSF to US, EU, and global apparel brand supply chains.

- High-growth demand from non-wovens, hygiene, automotive interiors, and geotextile applications driven by technical textiles mission.

- Emerging fiber-to-fiber recycling, dope-dyed PSF, and low-melt bi-component fiber creating premium high-margin product categories.

- Challenges

- Intense price-led competition between organised integrated PSF producers and smaller recycled-only converters compressing margins.

- Shortage of skilled polymerisation, spinning, and extrusion specialists limiting scale-up speed of new PSF capacity.

- Fragmented upstream PET bottle collection supply chains and quality inconsistency constraining recycled PSF growth.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Dynamics

- Industry Value Chain & Entry Points

- Upstream Petrochemical Feedstock (PTA & MEG producers, crude oil-linked)

- PET Bottle Collection, Segregation & Flake Processing (EPR-driven recycled feedstock)

- Polymerisation & PSF Fiber Lines (virgin, recycled, specialty PSF producers)

- Quality Control, Certification & Traceability (GRS, RCS, OEKO-TEX, BIS, QCOs)

- Yarn Spinning & Fiber Compounding (ring spun, open-end, air-jet spinners)

- Downstream Fabric & Non-Woven Manufacturers (weaving, knitting, spunbond, meltblown)

- Garment, Home Textile & Technical Textile Brands (domestic and export-oriented)

- Distributors, Yarn Agents & B2B Marketplaces

- End-Use Industries (apparel, home furnishing, automotive, hygiene, construction, agriculture)

- Post-Use Collection, EPR Compliance & Fiber-to-Fiber Recycling Loop

- India Polyester Staple Fiber Market: Regulatory Framework

- India Polyester Staple Fiber Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (‘000 Tons)

- Market Share & Forecast

- By Product Type

- Virgin Polyester Staple Fiber

- Recycled Polyester Staple Fiber (rPSF)

- Hollow Conjugated Fiber

- Solid Fiber

- Low-Melt Bi-Component Fiber

- Others

- By Denier

- Below 1.4 D

- 4–2 D

- 2–6 D

- 6–15 D

- Above 15 D

- By Cut Length

- Below 32 mm

- 32–38 mm

- 38–51 mm

- 51–76 mm

- Above 76 mm

- By Color

- Raw White

- Dyed / Dope-Dyed

- Optical White

- Black

- Others

- By Finish

- Semi-Dull

- Bright

- Super Bright

- Trilobal

- By Feedstock

- PTA — MEG Based

- Bottle Flakes / PET Recyclate Based

- Fiber-to-Fiber Recycled

- Bio-Based PET

- By Application

- Apparel & Clothing

- Home Textiles

- Non-Wovens & Hygiene

- Automotive Textiles

- Industrial & Technical Textiles

- Geotextiles

- Filtration

- Fiberfill & Upholstery

- Others

- By End-Use Industry

- Textile & Apparel Manufacturing

- Home Furnishing

- Automotive

- Construction & Infrastructure

- Healthcare & Hygiene

- Packaging

- Agriculture

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Yarn Agents

- Online / B2B Platforms

- Commodity Exchanges

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Market Size & Forecast, 2021-2032

- Competitive Landscape

- India Polyester Staple Fiber Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Reliance Industries Limited (Recron, Recron Green Gold)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Reliance Industries Limited (Recron, Recron Green Gold)

*(Same Data Pointers Will Be Provided for The Below Companies)

- Indo Rama Synthetics (India) Limited

- Bombay Dyeing and Manufacturing Company Limited

- JBF Industries Limited

- Ganesha Ecosphere Limited

- Filatex India Limited

- Alok Industries Limited

- JB Ecotex Limited

- Shakti Polyweave Pvt. Ltd.

- Pashupati Polytex Pvt. Ltd.

- Nirmal Fibers (P) Ltd.

- Polygenta Technologies Limited

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India polyester staple fiber market and what is its growth forecast?

Ans: The India polyester staple fiber market size is valued at USD 4.25 billion in 2025 and is projected to reach USD 7.68 billion by 2032, growing at a CAGR of around 8.8 percent. This strong India polyester staple fiber market growth is driven by rapid expansion of technical textiles and non-wovens, rising apparel and home-textile consumption, accelerated recycled PSF adoption, and government-led PLI support. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India polyester staple fiber market?

Ans: The India polyester staple fiber market segmentation shows that apparel and clothing leads with approximately 42 to 46 percent share, while non-wovens and hygiene is the fastest-growing application, expanding at 13 to 15 percent annually. Virgin PSF dominates product type with 68 to 72 percent share, while recycled polyester staple fiber (rPSF) is the fastest-growing segment, expected to exceed 40 percent of PSF consumption by 2032. The report breaks down demand across product types, deniers, applications, end-use industries, and sales channels, helping businesses understand where growth is accelerating across the India polyester staple fiber market.

3. What are the key drivers of growth in the India polyester staple fiber market?

Ans: Key India polyester staple fiber market drivers include rapid expansion of technical textiles and non-wovens growing at 11 to 13 percent annually, accelerated adoption of recycled polyester staple fiber (rPSF) aligned with global apparel brand sustainability mandates, and government-led PLI support combined with PM MITRA mega textile parks. Anti-dumping duties and Quality Control Orders are further supporting domestic producers. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends shaping the India polyester staple fiber market.

4. Which regions are driving growth in the India polyester staple fiber market?

Ans: Regional analysis of the India polyester staple fiber market shows that West and South India together account for 62 to 66 percent of total demand, driven by integrated PSF complexes in Gujarat and strong spinning clusters in Tamil Nadu, Andhra Pradesh, and Telangana. North India contributes around 18 to 22 percent, led by the Panipat home-textile cluster, Ludhiana knitwear industry, and growing non-wovens. East and Central India together account for 14 to 18 percent, supported by PM MITRA parks in Madhya Pradesh and Odisha. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India polyester staple fiber market?

Ans: The latest India polyester staple fiber market trends include rapid scale-up of recycled polyester staple fiber (rPSF) and fiber-to-fiber recycling, rising demand for dope-dyed, low-melt bi-component, and hollow conjugated PSF formats, and government PLI-led capacity expansion combined with export-oriented growth. Dope-dyed PSF adoption reduces water consumption by 60 to 70 percent, while rPSF is projected to exceed 40 percent of total PSF consumption by 2032. The report provides detailed insights into emerging trends, innovation pipelines, and future demand shifts, helping businesses stay ahead of competition and capture new growth opportunities in the India polyester staple fiber market.

Frequently Asked Questions

1. How large is the India polyester staple fiber market and what is its growth forecast?

Ans: The India polyester staple fiber market size is valued at USD 4.25 billion in 2025 and is projected to reach USD 7.68 billion by 2032, growing at a CAGR of around 8.8 percent. This strong India polyester staple fiber market growth is driven by rapid expansion of technical textiles and non-wovens, rising apparel and home-textile consumption, accelerated recycled PSF adoption, and government-led PLI support. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India polyester staple fiber market?

Ans: The India polyester staple fiber market segmentation shows that apparel and clothing leads with approximately 42 to 46 percent share, while non-wovens and hygiene is the fastest-growing application, expanding at 13 to 15 percent annually. Virgin PSF dominates product type with 68 to 72 percent share, while recycled polyester staple fiber (rPSF) is the fastest-growing segment, expected to exceed 40 percent of PSF consumption by 2032. The report breaks down demand across product types, deniers, applications, end-use industries, and sales channels, helping businesses understand where growth is accelerating across the India polyester staple fiber market.

3. What are the key drivers of growth in the India polyester staple fiber market?

Ans: Key India polyester staple fiber market drivers include rapid expansion of technical textiles and non-wovens growing at 11 to 13 percent annually, accelerated adoption of recycled polyester staple fiber (rPSF) aligned with global apparel brand sustainability mandates, and government-led PLI support combined with PM MITRA mega textile parks. Anti-dumping duties and Quality Control Orders are further supporting domestic producers. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends shaping the India polyester staple fiber market.

4. Which regions are driving growth in the India polyester staple fiber market?

Ans: Regional analysis of the India polyester staple fiber market shows that West and South India together account for 62 to 66 percent of total demand, driven by integrated PSF complexes in Gujarat and strong spinning clusters in Tamil Nadu, Andhra Pradesh, and Telangana. North India contributes around 18 to 22 percent, led by the Panipat home-textile cluster, Ludhiana knitwear industry, and growing non-wovens. East and Central India together account for 14 to 18 percent, supported by PM MITRA parks in Madhya Pradesh and Odisha. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India polyester staple fiber market?

Ans: The latest India polyester staple fiber market trends include rapid scale-up of recycled polyester staple fiber (rPSF) and fiber-to-fiber recycling, rising demand for dope-dyed, low-melt bi-component, and hollow conjugated PSF formats, and government PLI-led capacity expansion combined with export-oriented growth. Dope-dyed PSF adoption reduces water consumption by 60 to 70 percent, while rPSF is projected to exceed 40 percent of total PSF consumption by 2032. The report provides detailed insights into emerging trends, innovation pipelines, and future demand shifts, helping businesses stay ahead of competition and capture new growth opportunities in the India polyester staple fiber market.