India Packers and Movers Market, By Service Type (Home Relocation, Corporate & Office Relocation, Vehicle Transportation, Warehousing & Storage, International Relocation, Specialty & Value-Added Services); By Offering (Packing & Unpacking, Loading & Unloading, Transportation, Storage & Warehousing, Insurance & Claims, Vehicle Relocation, Tracking & Value-Added); By Mode of Transportation (Road, Railway, Air Cargo, Sea Freight, Multimodal); By Booking Channel (Online Aggregators & Apps, Company Websites & D2C, Offline Direct Booking, Agents & Brokers, Corporate Contracts, Others); By End-User (Residential, Commercial, Industrial, Government); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- Jul 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Packers and Movers Market: Urbanization, Corporate Mobility and Aggregator-Led Digitization Power Structural Growth, Forecasts 2032

Report Description

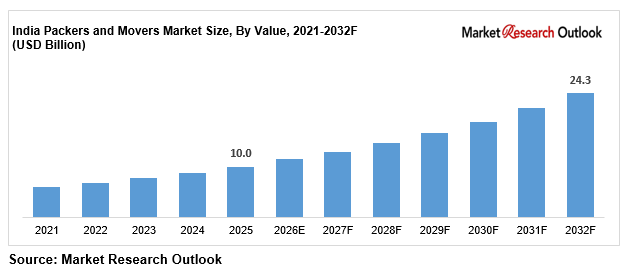

| Study Duration | 2021-2032 |

| Market Size (2025) | USD 10.0 Billion |

| CAGR (2026-2032) | 13.5% |

| Leading Segment | Home / Household Relocation |

| Fastest Growing Segment | Warehousing & Storage |

| Market Size (2032) | USD 24.3 Billion |

Source: Market Research Outlook

Market Overview: India Packers and Movers Market

The India packers and movers market size is witnessing rapid expansion, driven by accelerating urbanization, inter-city migration, rising corporate mobility, the shift from unorganized to organized services, growing warehousing demand, and rapid digitization by aggregator platforms. Valued at USD 10.0 billion in 2025 and projected to reach USD 24.3 billion by 2032, growing at a CAGR of 13.5%, the India packers and movers market growth is being fuelled by strong demand from urban households, nuclear families, and corporates, rising professional-service awareness, and the rapid scaling of online aggregators across metro and Tier-2 cities. Home relocation leads consumption, while the warehousing and storage segment is emerging as the fastest growing category. Shifting customer preferences toward organized, technology-enabled, and insured relocation, growing corporate mobility, and rising demand for value-added services are reshaping the supply landscape of the India packers and movers market. As organized majors including Agarwal Packers & Movers, Writer Relocations, PM Relocations, and Gati expand professional networks, and technology-enabled players including Porter, NoBroker, and Pikkol scale app-based platforms, the India packers and movers market is evolving into a consumer-led, technology-driven, and increasingly formalized ecosystem with strong long-term growth potential.

Key Report Takeaways: India Packers and Movers Market

- The India packers and movers market size is projected to grow from USD 10.0 billion in 2025 to USD 24.3 billion by 2032, registering a strong CAGR of 13.5%, driven by accelerated urbanization, rising corporate mobility, and the structural shift from unorganized to organized professional services across urban India.

- Home and household relocation dominates the India packers and movers market, accounting for 60% of total value in 2025, driven by strong demand for local and inter-city household shifting, the deep presence of players such as Agarwal Packers & Movers, Writer Relocations, and Porter, and rising urban demand across organized and app-based channels.

- Warehousing and storage is emerging as the fastest growing segment in the India packers and movers market, expected to grow at 22% annually as hybrid work, downsizing, and corporate mobility trends reshape service strategies across metro and Tier-2 markets.

- Rapid scaling of organized networks and aggregators, with the industry facilitating over 8.2 million relocations across India in 2025, is structurally expanding the India packers and movers market across residential, commercial, and industrial categories.

- Rising investments by organized and technology-enabled majors such as Agarwal Packers & Movers, Writer Relocations, Porter, and NoBroker in service networks, GPS tracking, and insurance are strengthening supply and supporting the India packers and movers market forecast 2032.

Key Market Drivers: India Packers and Movers Market

Rapid Urbanization, Inter-City Migration, and Corporate Mobility Driving Demand

Growth in the India packers and movers market is being driven by rapid urbanization, inter-city migration, and rising corporate mobility across metro, Tier-1, and Tier-2 cities. India’s urban population crossed 510 million in 2025, with urbanization rates climbing to 36% and projected to reach 40% by 2030, driving continuous relocation demand. The industry facilitated over 8.2 million relocations in 2025, including 6.1 million household moves and 2.1 million commercial and office relocations. Rising employee mobility between cities, driven by the expansion of the corporate sector and multinational corporations in hubs such as Bangalore, Mumbai, and Delhi NCR, is creating steady demand for professional relocation services. Growing nuclear families, a large floating population, and project-based professional mobility further strengthen demand. Rising consumer awareness of safe and secure relocation is creating strong structural pull-through demand across the India packers and movers market.

Nuclear Families, E-Commerce and Logistics Growth, and Rising Demand for Professional Organized Services

The India packers and movers market is benefiting from growing nuclear families, rapid e-commerce and logistics growth, and rising demand for professional organized services. The rising number of nuclear families and dual-income households is increasing the frequency of household relocation across urban India. Rapid e-commerce and logistics expansion has strengthened transport, warehousing, and last-mile infrastructure that supports professional relocation. Consumers increasingly prefer organized movers over unorganized local transporters, driven by demand for safe, secure, and hassle-free relocation. The residential segment accounts for 60% of the India packers and movers market, driven by local and inter-state household shifting, packing, and door-to-door services. Domestic service capacity has scaled rapidly, led by Agarwal Packers & Movers, Writer Relocations, PM Relocations, and Gati. Rising awareness of insured, tracked, and professional relocation has further strengthened organized supply, supporting value realisation across the India packers and movers market. Corporate and commercial relocation accounts for the remaining 40%, driven by office shifting and employee mobility.

Technology Adoption Through Online Aggregators, GPS Tracking, and Apps, Plus Formalization

Strong technology adoption, aggregator platforms, and rising formalization are major catalysts for the India packers and movers market, with the warehousing and storage segment projected to grow at 22% annually through 2032. Online aggregators and app-based platforms including Porter, NoBroker, LogisticsMart, and Sulekha allow customers to compare providers on price and reviews, bringing structure to a fragmented market. GPS tracking, real-time consignment visibility, inventory management software, and route optimization have transformed the relocation experience. The top 10 organized players currently hold only 8% of the India packers and movers market, with 92% held by over 50,000 unorganized operators, indicating significant long-term formalization headroom. Leading organized and technology-enabled players including Agarwal Packers & Movers, Writer Relocations, Porter, and NoBroker have scaled digital and service pipelines, with the organized segment representing an estimated USD 2.5 billion addressable opportunity in India. Technology adoption combined with formalization is structurally expanding India packers and movers market growth across all major categories through 2032.

Key Market Challenges: India Packers and Movers Market

Highly Fragmented, Unorganized Market with Inconsistent Quality and Pricing Opacity

The India packers and movers market continues to face challenges around high fragmentation, an unorganized base, inconsistent quality, and pricing opacity. Over 92% of the India packers and movers market is held by more than 50,000 unorganized operators, while the top 10 organized players control only 8% share. This fragmentation creates inconsistent service quality, pricing opacity, and limited accountability across the value chain. Customers often struggle to compare providers, verify credentials, or secure standardized pricing, particularly outside metro cities. India’s continued dependence on informal operators and the slow pace of formalization limit predictable, standardized service across the India packers and movers market.

Low Insurance Penetration, Delivery Delays, and Weak Consumer Trust

The India packers and movers market faces structural complexity from low insurance penetration, delivery delays, and weak consumer trust across different cities. While metros such as Delhi, Mumbai, Bengaluru, Chennai, and Hyderabad have organized providers and better standards, smaller cities maintain limited professional and insured options. Only 12% of moves in India are insured, leaving customers exposed to damage and loss risks. Delivery delays, damage to goods, and occasional fraud continue to erode consumer confidence, with over 12,800 complaints filed with the National Consumer Helpline in 2025. Differential availability of insured, tracked, and reliable services across states creates operational complexity for players such as Agarwal Packers & Movers, Writer Relocations, and Porter operating pan-India. While formalization is rising, trust and insurance gaps remain a near-term challenge for the India packers and movers market.

Rising Fuel, Vehicle, and Labour Costs, Seasonality, and Thin Margins

The India packers and movers market faces practical constraints around rising fuel, vehicle, and labour costs, seasonality, and thin margins across the value chain. Volatility in fuel prices, vehicle maintenance, and labour costs raises overall operating expenses and squeezes margins, particularly for smaller operators. Demand is highly seasonal, with peak relocation concentrated in summer months coinciding with school vacations, creating capacity and utilization challenges. Average operating margins for organized packers and movers in India stand near 15%, reducing the effective profitability of new capacity amid cost pressures. Route optimization, technology adoption, warehousing diversification, and value-added services are emerging as solutions to differentiate, but cost volatility and seasonality remain barriers to consistent profitability across the India packers and movers market.

Key Market Trends: India Packers and Movers Market

Rise of Digital Aggregators, App-Based Booking, GPS Tracking, and Virtual Surveys in India

The India packers and movers market is undergoing a clear shift toward digital aggregators, app-based booking, GPS tracking, and virtual surveys, with technology-enabled bookings expected to capture 40% of organized moves by 2027. App-based platforms, real-time tracking, and online price comparison deliver strong transparency, while virtual surveys and digital inventory tools improve the customer experience. Leading platforms including Porter, NoBroker, LogisticsMart, and Sulekha have scaled app-based relocation and aggregation through 2024 and 2025. Technology-enabled, transparent, and insured relocation services are also gaining traction, particularly in metro cities such as Mumbai and Bengaluru where digital-first consumers are rising, with organized players like Agarwal Packers & Movers, Writer Relocations, and PM Relocations offering technology-backed relocation. This service transition is reinforcing the India packers and movers market forecast 2032 across both residential and commercial categories.

Growth of Warehousing, Storage, and Value-Added Services in the India Packers and Movers Market

A clear shift toward warehousing, storage, and value-added services is reshaping the India packers and movers market, particularly in the urban and corporate segment. Warehousing and storage recorded the highest growth of 22% in 2025, driven by hybrid work models, downsizing, and companies storing excess furniture in anticipation of future expansion. Value-added services including transit insurance, specialty handling of fragile and high-value goods, vehicle relocation, and pet relocation are expanding the service portfolio. Corporate mobility and relocation management are also driving demand for managed, end-to-end services across both retail and corporate segments of the India packers and movers market. Rising demand for storage, insured moves, and premium managed relocation is structurally expanding the India packers and movers market across metro and Tier-1 clusters.

Consolidation, Professionalization, and Corporate Outsourcing Across India

A wave of consolidation, professionalization, and corporate outsourcing is reshaping the India packers and movers market supply landscape. Combined India-focused capital and expansion activity in organized relocation exceeded USD 200 million across 2023 to 2025. Organized players including Agarwal Packers & Movers, Writer Relocations, PM Relocations, and Gati expanded professional networks, while aggregators such as Porter and NoBroker scaled digital platforms. In March 2023, Porter launched a campaign aimed at simplifying packers and movers services across India, reflecting rising digital investment. Growing corporate outsourcing of employee relocation, eco-friendly packing, and professionalization have structurally favoured organized supply. Combined with rising urbanization driving demand and aggregator platforms scaling rapidly, these developments are reinforcing the India packers and movers market forecast 2032 across the entire value chain.

Segmental Insights: India Packers and Movers Market

By End-User: Residential Segment Dominates the India Packers and Movers Market

The residential end-user segment dominates the India packers and movers market, accounting for 60% of total consumption, driven by rising urbanization, nuclear families, and growing demand for professional household relocation. Home relocation, local and inter-city shifting, and door-to-door services capture the majority of residential demand. The commercial segment covering corporate and office relocation contributes 28% of demand, driven by employee mobility, office shifting, and corporate outsourcing. Industrial relocation accounts for 8%, led by plant, machinery, and warehouse moves, while government and institutional relocation accounts for 4%. In 2025, leading players including Agarwal Packers & Movers, Writer Relocations, Porter, and PM Relocations scaled up residential and commercial relocation deployment under organized network and aggregator expansion, reinforcing segment dominance in the India packers and movers market.

By Service Type: Home Relocation Leads While Warehousing and Storage Grows Fastest

Home and household relocation leads the India packers and movers market service landscape, accounting for 55% of total value, driven by strong demand for local and inter-city household shifting, packing, and door-to-door services. Corporate and office relocation contributes a significant share, supported by employee mobility and corporate outsourcing, while vehicle transportation adds meaningful volume through car and bike relocation. Warehousing and storage is the fastest growing category within the India packers and movers market, expanding at 22% annually, driven by hybrid work, downsizing, and corporate storage demand. International relocation and specialty value-added services account for a rising share, supported by premium and cross-border demand. Leading providers including Agarwal Packers & Movers, Writer Relocations, PM Relocations, and Porter have aligned service portfolios to this service mix, driving organized adoption across the India packers and movers market.

Regional Insights: India Packers and Movers Market

Regional analysis of the India packers and movers market shows that North India and South India collectively account for 57% of total packers and movers value, driven by Delhi NCR, Punjab, Uttar Pradesh, Karnataka, Tamil Nadu, and Telangana, supported by high urbanization, corporate hubs, and strong relocation demand. North India alone contributes 30% of demand, led by Delhi NCR, Punjab, Haryana, and Uttar Pradesh, supported by corporate mobility and household relocation in metro and Tier-1 clusters. South India contributes 27% of demand, anchored by Karnataka, Tamil Nadu, and Telangana, driven by IT and corporate professionals in Bengaluru, Chennai, and Hyderabad. West India adds 26%, anchored by Maharashtra and Gujarat, major corporate and commercial hubs, while East and Central India together account for 17%, supported by West Bengal, Odisha, and Madhya Pradesh, where organized relocation adoption is accelerating. In 2025, network expansion by Agarwal Packers & Movers across North India, Porter across South India, and organized players across West India reinforced regional supply, supporting closer execution of residential and corporate relocation projects across the India packers and movers market.

Recent Developments: India Packers and Movers Market

- The India packers and movers market witnessed strong momentum in growth and digitization during 2024 and 2025. The industry facilitated over 8.2 million relocations in 2025, including 6.1 million household moves and 2.1 million commercial relocations, growing at a double-digit rate. Warehousing and storage recorded the highest growth of 22%, driven by hybrid work and downsizing, while online aggregators expanded rapidly across metro and Tier-2 cities.

- Organized and technology-enabled majors have deepened networks and platforms. In 2024 and 2025, organized players including Agarwal Packers & Movers, Writer Relocations, PM Relocations, and Gati expanded professional networks, while aggregators such as Porter and NoBroker scaled app-based platforms and GPS tracking. These developments are strengthening organized supply and supporting the India packers and movers market forecast 2032.

- Digital and formalization momentum has gained strong traction in the India packers and movers market. In 2025, leading players including Agarwal Packers & Movers, Writer Relocations, Porter, and NoBroker expanded offerings and digital booking across metro and Tier-2 cities. Strategic focus on technology, insurance, and corporate mobility is positioning India as one of the fastest scaling relocation markets globally, strengthening long-term competitive positioning in the India packers and movers market forecast 2032.

Key Market Players: India Packers and Movers Market

- Agarwal Packers & Movers (DRS Group)

- Writer Relocations

- PM Relocations Pvt. Ltd. (PMR)

- Leo Packers & Movers

- Gati Ltd.

- Porter (Smartshift Logistics)

- Pikkol

- Maxwell Relocations

- Interem Relocations (Freightwings)

- AGS Movers India

- Santa Fe Relocation India

- NoBroker Packers & Movers

- LogisticsMart

Report Scope

In this report, the India Packers and Movers Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Service Type

- Home / Household Relocation

- Corporate & Office Relocation

- Vehicle Transportation

- Warehousing & Storage

- International Relocation

- Specialty & Value-Added Services

- By Offering

- Packing & Unpacking

- Loading & Unloading

- Transportation

- Storage & Warehousing

- Insurance & Claims

- Vehicle Relocation

- Tracking & Value-Added

- By Mode of Transportation

- Road & Trucking

- Railway

- Air Cargo

- Sea Freight

- Multimodal

- By Booking Channel

- Online Aggregators & Apps

- Company Websites & D2C

- Offline Direct Booking

- Agents & Brokers

- Corporate Contracts

- Others

- By End-User

- Residential (Households)

- Commercial (Corporate & Office)

- Industrial

- Government & Institutional

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Packers and Movers Market, including business overview, service portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging relocation platforms, specialty movers, regional players, or niche technology-enabled packers and movers brands.

The India Packers and Movers Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Service Type

- By Offering

- By Mode of Transportation

- By Booking Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Packers and Movers Market

- India Packers and Movers Market Insights

- Market Dynamics

- Growth Drivers

- Rapid urbanization, inter-city migration, and corporate mobility driving packers and movers demand across India.

- Nuclear families, e-commerce and logistics growth, and rising demand for professional organized services strengthening packers and movers consumption.

- Technology adoption through online aggregators, GPS tracking, and apps, plus formalization, accelerating packers and movers adoption.

- Restraints

- Highly fragmented, unorganized market with inconsistent quality and pricing opacity restricting organized packers and movers growth.

- Low insurance penetration, delivery delays, and weak consumer trust restricting packers and movers adoption.

- Rising fuel, vehicle, and labour costs, seasonality, and thin margins impacting overall packers and movers profitability.

- Opportunities

- Organized, branded players and aggregator platforms formalizing the packers and movers market.

- Warehousing, storage, corporate mobility, and value-added specialty services.

- Technology-enabled booking, tracking, insurance, and Tier-2 and Tier-3 expansion.

- Challenges

- Intense competition from unorganized local operators and price-driven informal transporters.

- Limited standardization, insurance, and quality infrastructure across smaller Indian cities.

- Maintaining service quality, timeliness, and safety consistency at scale across diverse relocation routes.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Packing Material Suppliers (boxes, bubble wrap, crates, tapes, protective materials)

- Fleet & Vehicle Providers (trucks, tempos, containers, GPS systems)

- Manpower & Trained Labour (packers, loaders, drivers, supervisors)

- Packers & Movers Service Providers (organized firms, regional operators, local movers)

- Online Aggregators & Marketplaces (Porter, NoBroker, LogisticsMart, Sulekha)

- Warehousing & Storage Operators (short-term and long-term storage facilities)

- Insurance & Claims Providers (transit insurance, goods protection)

- Technology & Tracking Providers (GPS, apps, route optimization, virtual survey)

- Corporate Mobility & Relocation Partners (corporate contracts, relocation management)

- End-Customers (households, corporates, industrial, government buyers)

- India Packers and Movers Market: Regulatory Framework

- India Packers and Movers Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- By Volume (Million Relocations)

- Market Share & Forecast

- By Service Type

- Home / Household Relocation

- Corporate & Office Relocation

- Vehicle Transportation

- Warehousing & Storage

- International Relocation

- Specialty & Value-Added Services

- By Offering

- Packing & Unpacking

- Loading & Unloading

- Transportation

- Storage & Warehousing

- Insurance & Claims

- Vehicle Relocation

- Tracking & Value-Added

- By Mode of Transportation

- Road & Trucking

- Railway

- Air Cargo

- Sea Freight

- Multimodal

- By Booking Channel

- Online Aggregators & Apps

- Company Websites & D2C

- Offline Direct Booking

- Agents & Brokers

- Corporate Contracts

- Others

- By End-User

- Residential (Households)

- Commercial (Corporate & Office)

- Industrial

- Government & Institutional

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Packers and Movers Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Agarwal Packers & Movers (DRS Group)

- Introduction & Company Profile

- Service Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

(Same Data Pointers Will Be Provided for The Below Companies)

- Writer Relocations

- PM Relocations Pvt. Ltd. (PMR)

- Leo Packers & Movers

- Gati Ltd.

- Porter (Smartshift Logistics)

- Pikkol

- Maxwell Relocations

- Interem Relocations (Freightwings)

- AGS Movers India

- Santa Fe Relocation India

- NoBroker Packers & Movers

- LogisticsMart

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India packers and movers market and what is its growth forecast?

Ans: The India packers and movers market is valued at USD 10.0 billion in 2025 and is projected to reach USD 24.3 billion by 2032, growing at a CAGR of 13.5%.

2. Which segments are driving demand in the India packers and movers market?

Ans: Home relocation leads with a 60% value share, while warehousing and storage is the fastest-growing segment, driven by hybrid work and corporate downsizing trends.

3. What are the key drivers of growth in the India packers and movers market?

Ans: Key drivers include rapid urbanization, inter-city migration, corporate mobility, nuclear families, rising professional-service demand, and online aggregator and technology adoption.

4. Which regions are driving growth in the India packers and movers market?

Ans: North India and South India lead with around 57% of total value. North India alone contributes 30%, driven by Delhi NCR and corporate mobility.

5. What are the latest trends in the India packers and movers market?

Ans: Latest trends include digital aggregators and app-based booking, GPS tracking, warehousing and storage growth, insurance adoption, and corporate relocation outsourcing.

Frequently Asked Questions

1. How large is the India packers and movers market and what is its growth forecast?

Ans: The India packers and movers market is valued at USD 10.0 billion in 2025 and is projected to reach USD 24.3 billion by 2032, growing at a CAGR of 13.5%.

2. Which segments are driving demand in the India packers and movers market?

Ans: Home relocation leads with a 60% value share, while warehousing and storage is the fastest-growing segment, driven by hybrid work and corporate downsizing trends.

3. What are the key drivers of growth in the India packers and movers market?

Ans: Key drivers include rapid urbanization, inter-city migration, corporate mobility, nuclear families, rising professional-service demand, and online aggregator and technology adoption.

4. Which regions are driving growth in the India packers and movers market?

Ans: North India and South India lead with around 57% of total value. North India alone contributes 30%, driven by Delhi NCR and corporate mobility.

5. What are the latest trends in the India packers and movers market?

Ans: Latest trends include digital aggregators and app-based booking, GPS tracking, warehousing and storage growth, insurance adoption, and corporate relocation outsourcing.