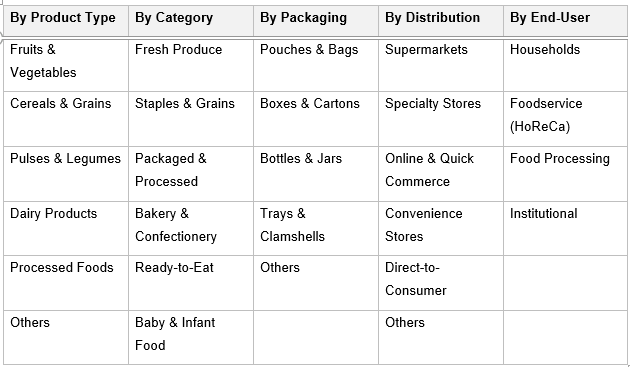

India Organic Food Market, By Product Type (Fruits & Vegetables, Cereals & Grains, Pulses & Legumes, Dairy Products, Processed Foods, Others); By Category (Fresh Produce, Staples & Grains, Packaged & Processed, Bakery & Confectionery, Ready-to-Eat, Beverages, Baby & Infant Food); By Packaging (Pouches & Bags, Boxes & Cartons, Bottles & Jars, Trays & Clamshells, Others); By Distribution Channel (Supermarkets & Hypermarkets, Specialty & Organic Stores, Online Retail & Quick Commerce, Convenience Stores, Direct-to-Consumer); By End-User (Households, Foodservice, Food Processing, Institutional); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Food, Beverage & Nutrition

- Jul 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Organic Food Market: Health Consciousness, Certification Growth and E-Commerce Expansion Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

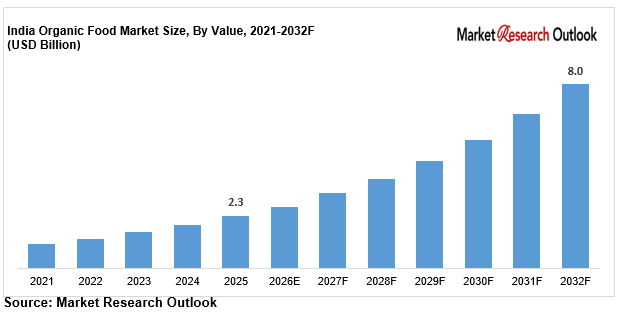

| Market Size (2025) | USD 2.3 Billion |

| CAGR (2026-2032) | 19.5% |

| Leading Segment | Cereals & Grains |

| Fastest Growing Segment | Organic Fruits, Vegetables & Processed Foods |

| Market Size (2032) | USD 8.0 Billion |

Source: Market Research Outlook

Market Overview: India Organic Food Market

The India organic food market size is witnessing rapid expansion, driven by rising health consciousness, growing certification awareness, increasing urbanization, expanding modern retail networks, rising demand for chemical-free and clean-label food, and major supply additions by domestic organic majors. Valued at USD 2.3 billion in 2025 and projected to reach USD 8.0 billion by 2032, growing at a CAGR of 19.5%, the market growth is being fuelled by strong demand from young urban consumers, rising disposable incomes, and the rapid scaling of e-commerce and quick-commerce platforms across metro and Tier-2 cities. Organic cereals and grains lead consumption with a 24% share, while fruits, vegetables, and processed foods are emerging as the fastest growing categories. Shifting consumer preferences toward healthier and safer food, growing wellness awareness, and rising demand for certified products are reshaping the supply landscape of the market. As domestic majors including Organic India, Sresta Natural Bioproducts, Nature Bio Foods, Suminter India Organics, and Phalada Agro expand integrated farm-to-shelf capacity, and D2C brands including Pro Nature, Conscious Food, and Just Organik scale certified pipelines, the India organic food market is evolving into a consumer-led, certification-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Organic Food Market

- The India organic food market size is projected to grow from USD 2.3 billion in 2025 to USD 8.0 billion by 2032, registering a strong CAGR of 19.5%, driven by accelerated health-driven demand, rising certified adoption, and the structural shift toward premium packaged organic food across urban India.

- Organic cereals and grains dominate the India organic food market, accounting for 24% of total value in 2025, driven by India’s staple food culture, growing preference for chemical-free grains, the deep presence of brands such as Organic India, 24 Mantra, and Nature Bio Foods, and rising urban demand across organized retail and online channels.

- Organic fruits, vegetables, and processed foods are emerging as the fastest growing segments in the market, expected to grow at 21% annually as health-conscious consumers, urban families, and wellness-focused millennials reshape sourcing strategies across metro and Tier-1 markets.

- Rapid scaling of certified farmland, with 1.76 million hectares under organic farming across India by 2025 and a target of 2 million hectares, is structurally expanding the India organic food market across modern retail, foodservice, and online delivery categories.

- Rising investments by domestic majors such as Organic India, Sresta Natural Bioproducts, Nature Bio Foods, Suminter India Organics, and Phalada Agro in certified supply chains, premium packaging, and processed organic variants are strengthening local supply and supporting the market forecast 2032.

Key Market Drivers: India Organic Food Market

Rising Health Consciousness, Urbanization, and Growing Awareness of Chemical-Free Food Driving Organic Food Demand Across India

Growth in the market is being driven by rising health consciousness, rapid urbanization, and growing awareness of the risks of chemical pesticides and fertilizers across metro, Tier-1, and Tier-2 cities. India’s urban population crossed 510 million in 2025, with urbanization rates climbing to 36% and projected to reach 40% by 2030. Certified organic farmland has expanded to 1.76 million hectares in 2025, with a national target of 2 million hectares, supported by schemes such as PKVY and MOVCDNER. Certified organic production reached 2.9 million metric tonnes in 2025, spanning cereals, millets, pulses, oilseeds, and spices. Organic food carries a price premium of 25% over conventional food, positioning it as a wellness and lifestyle choice. Rising youth population, with over 65% of Indians below age 35, growing clean-label awareness, and rising aspirational consumption are creating strong structural pull-through demand across the market.

Rising Disposable Incomes, Premiumization, and Shifting Dietary Preferences Fuelling Organic Food Adoption

The India organic food market is benefiting from sustained growth in disposable incomes, with per-capita income rising 70% between 2014 and 2024 according to MOSPI, alongside a growing middle class and accelerating premiumization. Certified organic products now command a price premium of 25% over conventional alternatives, with urban households increasingly willing to pay for chemical-free and traceable food. Average retail prices for staples range near INR 180 per kg, while premium and superfood variants command INR 350 per kg. Domestic organic production capacity has scaled rapidly, led by Organic India, Sresta Natural Bioproducts, Nature Bio Foods, Suminter India Organics, and Phalada Agro. FSSAI Jaivik Bharat labelling, NPOP certification, and growing trust in certified products have further strengthened organized supply, supporting value realisation across the market. Young consumers between 25 and 44 years now account for 60% of organic food consumption, with millennial and Gen-Z buyers preferring clean-label products, premium packaging, and doorstep convenience.

Government Support and E-Commerce Expansion Strengthening the Organic Food Market

Strong government support and rapid e-commerce expansion are major catalysts for the India organic food market, with the processed and packaged segment projected to grow at 21% annually through 2032. Since 2015-16, 59.74 lakh hectares have come under organic farming through the PKVY and MOVCDNER schemes, offering financial aid, certification, and marketing support to farmers. India’s organic food exports reached USD 665 million in FY2024-25, reinforcing the sector’s global significance. The FSSAI Jaivik Bharat framework and NPOP certification have increased transparency for organic buyers, accelerating certified adoption. E-commerce and quick-commerce platforms such as BigBasket, Swiggy Instamart, Zepto, and Blinkit are scaling organic distribution, with Swiggy Instamart partnering farmer-led cooperative Bharat Organics in 2025 to offer 21 certified staples. Government nutrition programs combined with rising corporate and D2C investment are structurally expanding India organic food market growth across all major end-user categories through 2032.

Key Market Challenges: India Organic Food Market

High Price Premium of Organic Food Limiting Affordability and Frequency of Consumption

The India organic food market continues to face challenges around high price premiums and limited consumption frequency among price-sensitive consumers, with organic food priced 25% higher than conventional alternatives on average. While certification reforms by FSSAI and growing demand for clean-label products have improved transparency, organic food consumption frequency in metro cities remains limited to a small share of the household grocery basket, reflecting affordability pressures, income disparity, and price sensitivity. Lower-income and middle-income households continue to prioritise conventional food due to cost, while premium organic variants remain concentrated in metro and Tier-1 markets. India’s continued price gap between organic and conventional food limits mass adoption among value-conscious households across the market.

Fragmented Supply Chain, Cold-Chain Gaps, and Short Shelf Life Across Tier-2 and Tier-3 Cities

The India organic food market faces structural complexity from a fragmented supply chain, limited cold-chain coverage, and short shelf life across different cities. While metros such as Delhi, Mumbai, Bengaluru, Chennai, and Hyderabad have established organic retail and cold-chain frameworks, smaller cities maintain limited cold-storage infrastructure and longer delivery times. Average shelf life for fresh fruits and vegetables ranges shorter than conventional produce, and unbroken cold-chain transport remains a key bottleneck in Tier-2 and Tier-3 rollout. Differential availability of certified retail shelves, aggregation infrastructure, and last-mile cold transport across states creates operational complexity for organic players such as Organic India, 24 Mantra, Nature Bio Foods, and Suminter operating pan-India. While the government has launched supply-chain support schemes, infrastructure fragmentation remains a near-term challenge for the India organic food market.

Volatility in Organic Input Costs, Lower Farm Yields, and Certification Costs Impacting Overall Margins

The India organic food market faces practical constraints around input cost volatility, lower farm yields, and certification costs across the value chain. Organic farming yields are lower than conventional farming during the transition period, while certification and traceability costs add to input expenses. Packaging input costs including pouches, cartons, and jars have moved up over recent years, and smaller organic brands face additional complexity in passing through cost increases without losing volume. Average gross margins for branded food in India stand near 32%, reducing the effective profitability of new launches. Farmer producer organizations, group certification, and supply-chain aggregation are emerging as solutions to differentiate, but premium pricing and limited consumer awareness remain barriers to widespread adoption across the market.

Key Market Trends: India Organic Food Market

Rapid Adoption of Processed Foods, Superfoods, and Millets in India

The India organic food market is undergoing a clear product shift toward organic processed foods, superfoods, and millets, with these advanced variants expected to capture over 20% of new organic product launches by 2027. Organic millets, quinoa, and superfoods deliver strong nutrition positioning, while ready-to-eat and ready-to-cook organic meals serve convenience-focused urban consumers. Leading domestic brands including Organic India, Sresta Natural Bioproducts, Nature Bio Foods, and Pro Nature have scaled processed and superfood production capacity through 2024 and 2025. Functional organic products with added nutrition and fortification are also gaining traction, particularly in metro cities such as Mumbai and Bengaluru where wellness consumers are rising, with brands like Conscious Food, Just Organik, and Organic Tattva offering health-positioned organic variants. This product transition is reinforcing the market forecast 2032 across both retail and online categories.

Growth of E-Commerce, Quick-Commerce, and D2C Distribution in the India Organic Food Market

A clear shift toward e-commerce, quick-commerce, and direct-to-consumer distribution models is reshaping the India organic food market, particularly in the urban and metro segment. Under quick-commerce platforms such as BigBasket, Swiggy Instamart, Zepto, and Blinkit, certified products are delivered within 30 minutes, expanding organic reach beyond organized retail. Leading platforms have built combined operational reach exceeding 800 Indian cities, with staples ranking among the fastest-growing grocery categories ordered online. Online aggregators and D2C brands are also reducing customer acquisition costs and accelerating organic adoption across both retail and quick-commerce segments of the market. By 2025, online channels account for 18% of packaged food sales in India, up from 6% in 2020, with metro buyers increasingly preferring subscription and same-day delivery convenience over in-store purchase.

Certified Supply Expansion by Domestic Majors and Farmer Producer Organizations

A wave of certified supply expansion and farmer producer organization development is reshaping the India organic food market supply landscape. Combined India-focused investment in aggregation, processing, and certification has scaled rapidly across 2023 to 2025. Organic India expanded certified sourcing networks, Sresta Natural Bioproducts scaled 24 Mantra staples, Nature Bio Foods (LT Foods) grew export-grade rice and grains, Suminter India Organics expanded farmer aggregation, and Phalada Agro grew its Pure & Sure portfolio. FSSAI Jaivik Bharat reforms, NPOP and PGS-India certification, and PKVY and MOVCDNER support have structurally favoured organized supply. Combined with modern retail expansion driving demand and quick-commerce procurement scaling rapidly, these developments are reinforcing the market forecast 2032 across the entire value chain.

Segmental Insights: India Organic Food Market

By End-User: Households Segment Dominates the India Organic Food Market

The households and individual consumers end-user segment dominates the India organic food market, accounting for 68% of total consumption, driven by rising health consciousness, growing home cooking, and improving organic retail economics. Organic staples, fruits, and vegetables are the dominant purchases within this segment, with online and modern retail formats capturing a growing share of household organic spending. The foodservice segment covering HoReCa contributes another 16% of demand, driven by premium restaurants, cafes, and hotels adopting organic ingredients as a signature offering. The food processing and industrial segment accounts for 10%, led by organic ingredient sourcing, while institutional buyers account for the balance. In 2025, leading organic players including Organic India, 24 Mantra, Nature Bio Foods, and Pro Nature scaled up household-focused organic deployment under modern retail and online expansion, reinforcing segment dominance in the market.

By Product Type: Cereals & Grains Lead While Fruits, Vegetables & Processed Foods Grow Fastest

Organic cereals and grains lead the India organic food market product landscape, accounting for 24% of total organic food value, driven by India’s staple food culture, growing preference for chemical-free grains, and deep distribution presence. Organic fruits and vegetables contribute 22% of value, primarily across metro and Tier-1 markets, while pulses and legumes add 14%, supported by strong staple demand. Organic fruits, vegetables, and processed foods are the fastest growing categories within the market, expanding at 21% annually, driven by superior nutrition positioning, wellness trends, and growing adoption in premium urban segments. Organic dairy and processed foods together account for a growing share, with the processed organic segment expected to grow rapidly through 2032 in metro markets. Leading manufacturers including Organic India, Sresta Natural Bioproducts, Nature Bio Foods, Suminter India Organics, and Phalada Agro have aligned product portfolios to this product mix, driving premium adoption across the market.

Regional Insights: India Organic Food Market

Regional analysis of the market shows that North India and West India collectively account for 58% of total organic food value, driven by Delhi NCR, Punjab, Haryana, Maharashtra (Mumbai and Pune belt), Gujarat, and Madhya Pradesh, supported by higher disposable incomes, greater health awareness, and established organic retail infrastructure. North India alone contributes 34% of demand, led by Delhi NCR, Punjab, Haryana, and Uttar Pradesh, supported by household and modern retail organic adoption across metro and Tier-1 clusters. West India contributes 24% of demand, anchored by Maharashtra and Gujarat, while South India adds 26%, led by Karnataka, Tamil Nadu, and Telangana. East and Central India together account for 16% of demand, supported by Madhya Pradesh, West Bengal, and Sikkim, India’s first fully organic state, where certified production is accelerating. In 2025, capacity additions and distribution operations by Organic India across North India, Sresta across South India, and Suminter across West India reinforced regional supply hubs, supporting closer execution of retail and online projects across the market.

Recent Developments: India Organic Food Market

- The India organic food market witnessed strong momentum in launches and certification progress during 2024 and 2025. India added 260 new certified SKUs in calendar year 2025, representing a 28% year-on-year increase from 203 SKUs in 2024, according to industry tracking. E-commerce and quick-commerce platforms recorded strong order growth by mid-2025, with the staples segment accounting for 62% of new orders. Cumulative certified production in India reached 2.9 million metric tonnes in 2025, with organic farmland at 1.76 million hectares.

- Domestic organic majors have deepened India-focused certified supply expansion. In 2025, Organic India expanded certified sourcing networks, Sresta Natural Bioproducts scaled its 24 Mantra staples, Nature Bio Foods (LT Foods) grew export-grade rice and grains, Suminter India Organics expanded farmer aggregation, and Phalada Agro grew its Pure & Sure portfolio. Swiggy Instamart partnered farmer-led cooperative Bharat Organics to offer 21 certified staples. These developments are strengthening domestic supply and supporting the market forecast 2032.

- Online and modern retail organic momentum has gained strong traction in the market. In 2025, leading players including Organic India, 24 Mantra, Nature Bio Foods, Pro Nature, and Conscious Food expanded processed and superfood offerings. Strategic partnerships between organic brands and quick-commerce platforms are positioning India as one of the most actively scaling organic food markets globally, strengthening long-term competitive positioning in the market forecast 2032.

Key Market Players: India Organic Food Market

- Organic India Pvt. Ltd.

- Sresta Natural Bioproducts Pvt. Ltd. (24 Mantra Organic)

- Nature Bio Foods Ltd. (LT Foods)

- Suminter India Organics Pvt. Ltd.

- Phalada Agro Research Foundations Pvt. Ltd. (Pure & Sure)

- Morarka Organic Foods Ltd. (Down to Earth)

- Conscious Food Pvt. Ltd.

- Just Organik

- Pro Nature Organic Foods Pvt. Ltd.

- Organic Tattva (Genuine Organics Pvt. Ltd.)

- Tata Consumer Products Limited (Tata Sampann)

- ITC Limited (Farmland)

- Patanjali Ayurved Limited

Report Scope

In this report, the India Organic Food Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Fruits & Vegetables

- Cereals & Grains

- Pulses & Legumes

- Dairy Products

- Processed Foods

- Others

- By Category

- Fresh Produce

- Staples & Grains

- Packaged & Processed

- Bakery & Confectionery

- Ready-to-Eat

- Beverages

- Baby & Infant Food

- By Packaging

- Pouches & Bags

- Boxes & Cartons

- Bottles & Jars

- Trays & Clamshells

- Others

- By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty & Organic Stores

- Online Retail & Quick Commerce

- Convenience Stores

- Direct-to-Consumer & Farmers Markets

- Others

- By End-User

- Households & Individual Consumers

- Foodservice (HoReCa)

- Food Processing & Industrial

- Institutional

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Organic Food Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging D2C organic brands, specialty organic producers, regional farmer producer organizations, or niche state-level organic food brands.

The India Organic Food Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Category

- By Packaging

- By Distribution Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Organic Food Market

- India Organic Food Market Insights

- Market Dynamics

- Growth Drivers

- Rising health consciousness, urbanization, and growing awareness of chemical-free food driving demand across India.

- Rising disposable incomes, premiumization, and shifting dietary preferences fuelling adoption.

- Government support through PKVY, MOVCDNER, and NPOP certification, and rapid e-commerce expansion strengthening the market.

- Restraints

- High price premium limiting affordability and frequency of consumption among price-sensitive consumers.

- Fragmented supply chain, cold-chain gaps, and short shelf life restricting distribution across Tier-2 and Tier-3 cities.

- Volatility in input costs, lower farm yields, and certification costs impacting overall margins.

- Opportunities

- Organic processed foods, superfoods, and infant food innovation opening untapped consumer pools across metro cities.

- Premium, export-grade, and functional organic products supporting next-generation growth in wellness segments.

- E-commerce, quick-commerce, D2C brands, and modern retail expansion creating massive distribution opportunities.

- Challenges

- Intense competition from conventional food, mislabeled natural products, and unorganized local sellers.

- Limited certification awareness, adulteration concerns, and consumer trust deficit around organic authenticity.

- Maintaining consistent quality, certification compliance, and reliable supply at scale across diverse Indian markets.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Inputs (organic seeds, bio-fertilizers, bio-pesticides, organic feed, water)

- Organic Farmers & Farmer Producer Organizations (FPOs, cooperatives, contract growers)

- Aggregators, Processors & Organic Food Manufacturers (Organic India, 24 Mantra, Nature Bio Foods)

- Certification & Testing Bodies (NPOP, APEDA, FSSAI, accredited certification agencies)

- Ingredient & Private-Label Suppliers (grains, pulses, spices, edible oils, superfoods)

- Distributors, Wholesalers & Modern Trade (B2B and B2C distribution networks)

- Specialty Organic Stores & Supermarkets (organized retail, health-food chains)

- Brand Owners & D2C Organic Brands (Organic India, Pro Nature, Conscious Food, Just Organik)

- Retail Channels & Online Delivery (BigBasket, Amazon, Swiggy Instamart, Zepto, Blinkit)

- End-Consumers (households, health-conscious consumers, foodservice, institutional buyers)

- India Organic Food Market: Regulatory Framework

- India Organic Food Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- By Volume (Thousand Tonnes)

- Market Share & Forecast

- By Product Type

- Fruits & Vegetables

- Cereals & Grains

- Pulses & Legumes

- Dairy Products

- Processed Foods

- Others

- By Category

- Fresh Produce

- Staples & Grains

- Packaged & Processed

- Bakery & Confectionery

- Ready-to-Eat

- Beverages

- Baby & Infant Food

- By Packaging

- Pouches & Bags

- Boxes & Cartons

- Bottles & Jars

- Trays & Clamshells

- Others

- By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty & Organic Stores

- Online Retail & Quick Commerce

- Convenience Stores

- Direct-to-Consumer & Farmers Markets

- Others

- By End-User

- Households & Individual Consumers

- Foodservice (HoReCa)

- Food Processing & Industrial

- Institutional

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Organic Food Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Organic India Pvt. Ltd.

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

(Same Data Pointers Will Be Provided for The Below Companies)

- Sresta Natural Bioproducts Pvt. Ltd. (24 Mantra Organic)

- Nature Bio Foods Ltd. (LT Foods)

- Suminter India Organics Pvt. Ltd.

- Phalada Agro Research Foundations Pvt. Ltd. (Pure & Sure)

- Morarka Organic Foods Ltd. (Down to Earth)

- Conscious Food Pvt. Ltd.

- Just Organik

- Pro Nature Organic Foods Pvt. Ltd.

- Organic Tattva (Genuine Organics Pvt. Ltd.)

- Tata Consumer Products Limited (Tata Sampann)

- ITC Limited (Farmland)

- Patanjali Ayurved Limited

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India organic food market and what is its growth forecast?

Ans: The India organic food market is valued at USD 2.3 billion in 2025 and is projected to reach USD 8.0 billion by 2032, growing at a CAGR of 19.5%.

2. Which segments are driving demand in the India organic food market?

Ans: Organic cereals and grains lead with a 24% share, while fruits, vegetables, and processed foods are the fastest-growing segments, driven by health-conscious urban consumers.

3. What are the key drivers of growth in the India organic food market?

Ans: Key drivers include rising health consciousness, urbanization, premiumization, government support through PKVY and NPOP certification, and rapid scaling of e-commerce and quick-commerce platforms.

4. Which regions are driving growth in the India organic food market?

Ans: North India and West India lead with around 58% of total value, driven by Delhi NCR, Punjab, Maharashtra, Gujarat, and Madhya Pradesh. North India alone contributes 34%.

5. What are the latest trends in the India organic food market?

Ans: Latest trends include rapid adoption of organic processed foods and superfoods, growth in quick-commerce delivery, rising D2C brands, and expanding certified farmland and exports.

Frequently Asked Questions

1. How large is the India organic food market and what is its growth forecast?

Ans: The India organic food market is valued at USD 2.3 billion in 2025 and is projected to reach USD 8.0 billion by 2032, growing at a CAGR of 19.5%.

2. Which segments are driving demand in the India organic food market?

Ans: Organic cereals and grains lead with a 24% share, while fruits, vegetables, and processed foods are the fastest-growing segments, driven by health-conscious urban consumers.

3. What are the key drivers of growth in the India organic food market?

Ans: Key drivers include rising health consciousness, urbanization, premiumization, government support through PKVY and NPOP certification, and rapid scaling of e-commerce and quick-commerce platforms.

4. Which regions are driving growth in the India organic food market?

Ans: North India and West India lead with around 58% of total value, driven by Delhi NCR, Punjab, Maharashtra, Gujarat, and Madhya Pradesh. North India alone contributes 34%.

5. What are the latest trends in the India organic food market?

Ans: Latest trends include rapid adoption of organic processed foods and superfoods, growth in quick-commerce delivery, rising D2C brands, and expanding certified farmland and exports.