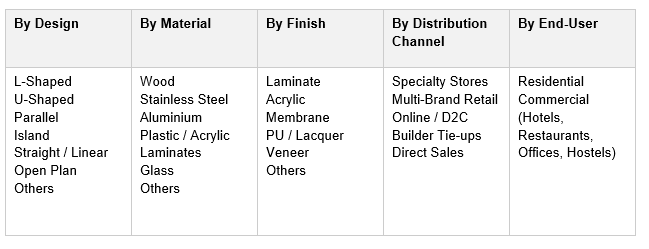

India Modular Kitchen Market, By Design (L-Shaped, U-Shaped, Parallel, Island, Straight/Linear, Open Plan, Others); By Product Type (Base Cabinet, Wall Cabinet, Tall Unit, Drawer Unit, Accessories); By Material (Wood, Stainless Steel, Aluminium, Plastic/Acrylic, Laminates, Glass, Others); By Finish (Laminate, Acrylic, Membrane, PU/Lacquer, Veneer, Others); By Price Range (Economy, Mid-Range, Premium, Luxury); By Distribution Channel (Specialty Stores, Multi-Brand Retail, Online/D2C, Builder Tie-ups, Direct Sales); By End-User (Residential, Commercial); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Modular Kitchen Market: Urbanization, Apartment Culture, and Premium Interior Spend Power Structural Demand, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

| Market Size (2025) | USD 2.85 Billion |

| CAGR (2026-2032) | 13.3% |

| Leading Segment | L-Shaped Kitchen (Laminate Finish) |

| Fastest Growing Segment | Smart / Connected Modular Kitchens |

| Market Size (2032) | USD 6.85 Billion |

Source: Market Research Outlook

Market Overview: India Modular Kitchen Market

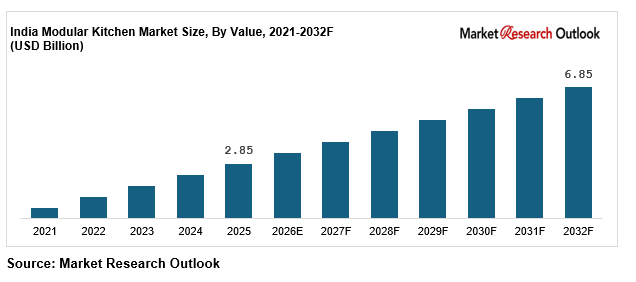

The India modular kitchen market size is witnessing rapid expansion, driven by rising disposable income, accelerating urbanization across Tier-I, Tier-II, and Tier-III cities, expansion of nuclear families and apartment culture, the rapid scaling of organized real estate and ready-to-move-in housing supply, and growing aspirational consumption among urban Indian households. Valued at USD 2.85 billion in 2025 and projected to reach USD 6.85 billion by 2032, growing at a CAGR of 13.3%, the India modular kitchen market growth is being fuelled by strong residential adoption in apartments and villas, rising premium and luxury kitchen demand among high-income households, growing commercial demand from hotels, restaurants, cafes, and corporate offices, and the rapid scaling of D2C interior platforms and builder tie-ups. L-shaped layouts lead consumption, while smart and connected modular kitchens are emerging as the fastest growing category. Strengthening interior design awareness, RERA-driven real estate transparency, and clean-home preferences by Indian consumers, alongside aggressive showroom and digital expansion by leading brands, are reshaping the supply landscape. As domestic majors including Godrej Interio, Sleek Kitchens, Spacewood, Kutchina, and Johnson Kitchens scale economy, mid-range, and premium portfolios, and global majors including IKEA, Häfele, Nobilia, and Häcker deepen India-specific innovation, the India modular kitchen market is evolving into a brand-led, design-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Modular Kitchen Market

- The India modular kitchen market size is projected to grow from USD 2.85 billion in 2025 to USD 6.85 billion by 2032, registering a strong CAGR of 13.3%, driven by accelerated urbanization, rising premium interior spend, and the structural shift from carpenter-built kitchens toward organized modular solutions across Indian metros and Tier-II cities.

- Residential end-users dominate the India modular kitchen market, accounting for over 78% of total category value in 2025, driven by strong apartment and villa demand, rising nuclear family formation, mid-range price points of INR 1.5 lakh to 5 lakh, and growing penetration across modern trade, D2C interior platforms, and builder tie-ups.

- Smart and connected modular kitchens are emerging as the fastest growing segment in the India modular kitchen market, expected to grow at 18% to 22% annually, as IoT-enabled appliances, sensor-based hardware, voice-controlled lighting, and automated drawer systems gain traction across premium urban households.

- Rapid scaling of D2C interior platforms such as Livspace, HomeLane, Pepperfry, and Bonito Designs, alongside expanding presence of global brands such as IKEA, Häfele, Nobilia, and Häcker, with online and platform-led modular kitchen sales crossing 18% to 22% by mid-2025, is structurally expanding the India modular kitchen market across residential and commercial categories.

- Rising investments by domestic majors such as Godrej Interio, Sleek Kitchens (Asian Paints), Spacewood, Kutchina, and Johnson Kitchens in manufacturing capacity, showroom expansion, and digital configurators are strengthening domestic supply and supporting the India modular kitchen market forecast 2032.

Key Market Drivers: India Modular Kitchen Market

Rising Disposable Income, Urbanization, and Nuclear Family Growth Driving Organized Kitchen Demand

Growth in the India modular kitchen market is being driven by rising disposable income, accelerating urbanization, and the structural rise of nuclear families across metro and Tier-II Indian cities. India’s per-capita disposable income has grown at over 9% annually between 2020 and 2025, supporting discretionary spend on home interiors, kitchen renovation, and lifestyle categories. Urban household penetration of branded modular kitchens has crossed 22% in 2025, up from 12% in 2020, while per-capita modular kitchen consumption remains well below global benchmarks of USD 80 to 120, indicating significant long-term headroom for category expansion. Aspirational interior spend among the 25 to 45 age cohort, supported by dual-income households, work-from-home culture, and rising influence of design content on Instagram, YouTube, and Pinterest, is structurally pulling demand into the India modular kitchen market. Mid-range modular kitchens priced between INR 1.5 lakh and INR 5 lakh, available through specialty stores, D2C platforms, and builder partnerships, continue to drive high-volume penetration across the country.

Real Estate Expansion, Apartment Culture, and Ready-to-Move-In Housing Boosting Adoption

The India modular kitchen market is benefiting from a strong tailwind from the organized real estate sector, with apartment-style housing, gated communities, and ready-to-move-in homes increasingly bundling modular kitchens as a standard offering. India’s organized residential real estate market has grown at over 14% CAGR between 2021 and 2025, with annual residential launches exceeding 4.5 lakh units across the top 8 metro cities. Average new apartment kitchen sizes of 80 to 140 square feet are well-suited to L-shaped, parallel, and straight layout modular configurations. Leading builders including DLF, Godrej Properties, Lodha, Prestige, Brigade, Sobha, and Mahindra Lifespaces are partnering with modular kitchen brands and interior platforms such as Livspace, HomeLane, Sleek, Godrej Interio, and Spacewood to deliver pre-installed modular kitchens. RERA-driven transparency, rising under-construction supply, and the shift toward premium-amenity housing are accelerating standardization of modular kitchen offerings across the India modular kitchen market.

E-commerce, D2C Brands, EMI Financing, and Influencer Marketing Accelerating Category Growth

Rapid growth in online and D2C distribution is a major catalyst for the India modular kitchen market, with the digital and D2C channel projected to grow at 22% to 26% annually through 2032. Online and platform-led modular kitchen sales now account for an estimated 18% to 22% of total category value, led by D2C interior platforms such as Livspace, HomeLane, Pepperfry Modular, Bonito Designs, and Urban Ladder Interiors. Easy EMI financing through Bajaj Finserv, HDFC, Pine Labs, and brand-tied 0% interest schemes for tenures of 12 to 24 months has structurally improved affordability of premium modular kitchens priced between INR 3 lakh and INR 8 lakh. AR-based design tools, virtual kitchen configurators, and 3D visualization apps are reshaping consumer discovery, with over 60% of urban modular kitchen buyers researching designs online before purchase. Influencer-led interior design content on Instagram, YouTube, and short-form video platforms is reinforcing aspirational demand. Leading D2C and digital-first players have scaled aggressive content, performance marketing, and design-consultation pipelines, supporting structural expansion of the India modular kitchen market across all major end-user categories through 2032.

Key Market Challenges: India Modular Kitchen Market

High Upfront Cost Limiting Middle-Income Household Adoption

The India modular kitchen market continues to face challenges around high upfront capital costs, with a typical mid-range modular kitchen costing INR 1.5 lakh to 5 lakh and premium installations crossing INR 8 lakh to 15 lakh, placing the category beyond the reach of many middle-income households. While EMI schemes from Bajaj Finserv, HDFC, Pine Labs, and brand-tied 0% interest plans have improved affordability, modular kitchens still represent a large discretionary spend versus carpenter-built alternatives priced at INR 60,000 to 1.2 lakh. Banks and NBFCs continue to be cautious in extending unsecured home interior loans to lower-income households, while EMI-linked financing for installations above INR 3 lakh remains under-penetrated in Tier-II and Tier-III cities. India’s continued price sensitivity in the under-INR 1.5 lakh kitchen segment limits adoption among middle-income and rural households across the India modular kitchen market.

Strong Unorganized Carpenter Market and Counterfeit / Look-Alike Products

The India modular kitchen market faces structural complexity from the strong presence of unorganized local carpenters and look-alike modular kitchen products. Unorganized carpenter-built kitchens, priced at INR 60,000 to 1.5 lakh, still account for over 55% of total Indian kitchen installations by volume, particularly in Tier-II, Tier-III, and rural markets. Counterfeit hardware, low-grade plywood, and unbranded acrylic finishes positioned as imitation Hettich, Häfele, Blum, or Sleek products undermine quality standards and brand-building investments by leading players. Look-alike imitations of Godrej Interio, Sleek, Kutchina, and Spacewood designs continue to challenge organized brand economics, particularly in non-metro markets. While the Bureau of Indian Standards (BIS) has standardised quality norms for plywood, MDF, and kitchen hardware under IS 303 and related codes, enforcement gaps remain. Strengthening BIS oversight, consumer awareness, and tighter e-commerce listing policies are gradually easing these pressures over time.

Skilled Installer Shortage, Long Lead Times, and After-Sales Service Gaps

The India modular kitchen market faces practical constraints around skilled installer availability, long customization lead times, and after-sales service gaps across metros and Tier-II cities. Indian cities such as Mumbai, Delhi, Bengaluru, Pune, and Hyderabad face an estimated 25% to 30% shortage of trained modular kitchen installers and finish carpenters, leading to project delays of 2 to 6 weeks beyond promised timelines. Average modular kitchen installation timelines range from 30 to 60 days, with custom premium kitchens stretching to 75 to 90 days, well above international benchmarks. After-sales service gaps, including hinge replacement, drawer slide servicing, soft-close mechanism repairs, and counter-top maintenance, remain a key consumer pain point. While leading brands such as Godrej Interio, Sleek, Häfele, Hettich, and Livspace have built service networks of 200 to 800 cities, smaller and regional players continue to face execution gaps. Investments in installer training, certification programs, and standardised service SLAs are gradually addressing these challenges across the India modular kitchen market.

Key Market Trends: India Modular Kitchen Market

Rapid Adoption of Smart, IoT-Enabled, and Connected Modular Kitchens in India

The India modular kitchen market is undergoing a clear technology shift toward smart, IoT-enabled, and connected kitchen systems, with these higher-specification categories expected to capture over 25% of premium kitchen installations by 2027. Smart modular kitchens with motion-sensor LED lighting, voice-controlled appliances, touch-to-open drawer systems, automated wall lift cabinets, and integrated smart hobs are increasingly preferred by metro and Tier-I urban consumers. Premium hardware brands including Hettich, Häfele, Blum, and Grass have scaled India-focused smart drawer and lift system portfolios. Built-in appliance brands such as Faber, Elica, Kaff, Bosch, and Siemens are integrating Wi-Fi connectivity into chimneys, hobs, ovens, and dishwashers. Long-lasting acrylic and PU-finish modular kitchens with anti-bacterial laminates, 25-year hardware warranties, and 10-year structural warranties from Godrej, Sleek, and Häcker are also gaining strong consumer traction. This technology and premiumization shift is reinforcing the India modular kitchen market forecast 2032 across both mid-range and premium categories.

Growth of Premium Materials, Sustainable Plywood, and Eco-Friendly Finishes

A clear shift toward premium materials, sustainable plywood, and eco-friendly finishes is reshaping the India modular kitchen market, particularly across the premium and luxury segments. Premium acrylic, PU lacquer, and lacquered glass finish kitchens grew by over 28% in 2024 and 2025, with leading players including Sleek, Godrej Interio, Häcker, Nobilia, Veneta Cucine, and Bonito Designs scaling premium finish portfolios. FSC-certified plywood, BWP-grade marine plywood, CARB-compliant MDF, and anti-termite particle boards are increasingly central to brand positioning, especially among urban millennial and Gen-Z consumers. Eco-friendly bamboo composites, recycled aluminium, and low-VOC adhesives are seeing structural demand in metro markets, driven by indoor air quality awareness, sustainability preferences, and green-building LEED certification. This material and finish premiumization momentum is supporting category value growth and is reinforcing structural growth across the India modular kitchen market.

Capacity Expansion, D2C Distribution, and Digital-First Brand Launches

A wave of capacity expansion, D2C distribution scaling, and digital-first brand launches is reshaping the India modular kitchen market supply landscape. Combined India-focused capital expenditure announcements by leading modular kitchen and interior players exceeded INR 3,500 crore across 2023 to 2025. Asian Paints scaled Sleek Kitchens manufacturing and showroom capacity, Godrej Interio expanded modular kitchen lines, IKEA opened new stores in Bengaluru, Mumbai, Delhi NCR, and Pune, Häfele expanded its Yamunanagar manufacturing unit, and Spacewood scaled Nagpur production. D2C interior platforms such as Livspace, HomeLane, Pepperfry, and Bonito Designs have emerged as a high-growth distribution channel, contributing over 18% to 22% of urban modular kitchen sales by mid-2025. Digital-first and design-led brands including Bonito Designs, Carafina, DesignCafe, and Furlenco Interiors are scaling 3D configurator, AR design, and virtual consultation portfolios. Combined with rising aspirational consumption and premiumization across urban India, these developments are reinforcing the India modular kitchen market forecast 2032 across the entire value chain.

Segmental Insights: India Modular Kitchen Market

By End-User: Residential Segment Dominates the India Modular Kitchen Market

The residential end-user segment dominates the India modular kitchen market, accounting for an estimated 76% to 80% of total category value, driven by rising apartment and villa demand, nuclear family growth, and improving modular kitchen economics. L-shaped layouts are the dominant design within this segment, with laminate-finish modular kitchens capturing over 55% of residential installations. The commercial segment contributes another 20% to 24% of demand, driven by hotels, quick-service restaurants, cafes, cloud kitchens, office cafeterias, and corporate pantries adopting modular kitchen solutions for hygiene compliance, design uniformity, and faster project turnaround. Within commercial, stainless steel and aluminium-based modular kitchens lead, with brands such as Godrej Interio, Häfele, Spacewood, and Veneta Cucine scaling commercial portfolios. In 2025, leading players including Godrej Interio, Sleek Kitchens, IKEA, Spacewood, Kutchina, Livspace, and HomeLane scaled up residential and commercial modular kitchen deployment under apartment bundling and renovation demand, reinforcing segment dominance in the India modular kitchen market.

By Design and Material: L-Shaped Leads While Island and Acrylic Grow Fastest

L-shaped modular kitchens lead the India modular kitchen market design landscape, accounting for approximately 38% to 42% of total installations, driven by their suitability for typical 80 to 140 square feet Indian apartment kitchen layouts, efficient corner utilization, and improving cost economics. Parallel and straight-line layouts contribute another 25% to 28%, primarily in studio apartments and compact urban housing. U-shaped layouts account for 12% to 15%, while island and open-plan kitchens are the fastest growing categories within the India modular kitchen market, expanding at 20% to 25% annually, driven by villa and luxury apartment adoption. By material, plywood and MDF lead with 60% to 65% share, while acrylic-finish modular kitchens are the fastest growing finish category, expanding at 22% to 28% annually, supported by premium urban demand. Leading domestic and global brands including Godrej Interio, Sleek, IKEA, Häfele, Spacewood, Kutchina, and Häcker have aligned product portfolios to this design and material mix, driving high-specification modular kitchen adoption across the India modular kitchen market.

Regional Insights: India Modular Kitchen Market

Regional analysis of the India modular kitchen market shows that West India and North India collectively account for approximately 58% to 62% of total category value, driven by Maharashtra (Mumbai, Pune metro housing belt), Gujarat (Ahmedabad, Surat, Vadodara premium housing), Delhi NCR, Uttar Pradesh (Noida, Lucknow), Haryana (Gurugram, Faridabad), and Punjab, supported by strong organized real estate launches, premium-amenity apartment supply, and proximity to modular kitchen manufacturing clusters. South India contributes around 25% to 28% of demand, led by Karnataka (Bengaluru), Tamil Nadu (Chennai, Coimbatore), Telangana (Hyderabad), and Kerala, supported by Tier-I urban apartment adoption, IT sector workforce demand, and a strong premium kitchen consumer base. East and Central India together account for 12% to 15% of demand, supported by West Bengal (Kolkata), Odisha (Bhubaneswar), Madhya Pradesh (Indore, Bhopal), and Chhattisgarh, where modular kitchen penetration is accelerating among Tier-II cities. In 2025, capacity additions and showroom expansion by Sleek Kitchens across West India, Godrej Interio in North India, IKEA in South India, Häfele across pan-India, and Spacewood from Nagpur reinforced regional supply hubs, supporting closer execution of residential, commercial, and builder-bundled modular kitchen projects across the India modular kitchen market.

Recent Developments: India Modular Kitchen Market

- The India modular kitchen market witnessed strong momentum in capacity expansion, brand launches, and channel scaling during 2024 and 2025. The category grew by an estimated 14% to 16% in value terms in 2025, supported by aggressive real estate launches, festive renovation cycles, builder bundling, and D2C platform expansion. Online and D2C interior platform sales crossed 18% to 22% of total category value, with premium acrylic and PU-finish kitchen sales growing by over 28% year-on-year, according to leading industry trackers. Cumulative organized branded modular kitchen penetration is projected to expand from 38% in 2025 to 55% to 60% by FY32, growing at an average 13% to 15% annually.

- Domestic modular kitchen players have deepened India-focused capacity expansion and brand portfolio building. In 2025, Asian Paints scaled Sleek Kitchens manufacturing and added new premium variants, Godrej Interio expanded modular kitchen production lines, Spacewood scaled its Nagpur facility with new automated machinery, Kutchina expanded its Kolkata production, and Johnson Kitchens added new luxury collections. IKEA opened new stores in Bengaluru, Mumbai, and Delhi NCR, while Häfele expanded its Yamunanagar manufacturing unit. These developments are strengthening domestic supply and supporting the India modular kitchen market forecast 2032.

- Premium and D2C interior platform momentum has gained strong traction in the India modular kitchen market. In 2025, leading premium and digital-first players including Livspace, HomeLane, Pepperfry Modular, Bonito Designs, DesignCafe, and Veneta Cucine scaled premium modular kitchen, smart kitchen, and luxury collection portfolios. Strategic partnerships between domestic modular kitchen brands, builders such as DLF, Godrej Properties, Lodha, Prestige, and Brigade, and online platforms are positioning India as one of the most actively scaling modular kitchen markets globally, strengthening long-term competitive positioning in the India modular kitchen market forecast 2032.

Key Market Players: India Modular Kitchen Market

- Godrej Interio (Godrej & Boyce Mfg. Co. Ltd.)

- Sleek Kitchens (Asian Paints Limited)

- Häfele India Pvt. Ltd.

- Hettich India Pvt. Ltd.

- IKEA India Pvt. Ltd.

- Spacewood Office Solutions Pvt. Ltd.

- Kutchina Home Makers Pvt. Ltd.

- Johnson Kitchens (H & R Johnson India)

- HomeLane (Bro4u Online Services Pvt. Ltd.)

- Livspace Interior Services Pvt. Ltd.

- Pepperfry Modular Kitchens

- Nobilia Kitchen India

- Häcker Kitchens India

- Bonito Designs

- Veneta Cucine India

Report Scope

In this report, the India Modular Kitchen Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Design

- L-Shaped

- U-Shaped

- Parallel

- Island

- Straight / Linear

- Open Plan

- Others

- By Product Type

- Base Cabinet

- Wall Cabinet

- Tall Unit

- Drawer Unit

- Accessories

- By Material

- Wood (Plywood, MDF, Particle Board)

- Stainless Steel

- Aluminium

- Plastic / Acrylic

- Laminates

- Glass

- Others

- By Finish

- Laminate

- Acrylic

- Membrane

- PU / Lacquer

- Veneer

- Others

- By Price Range

- Economy

- Mid-Range

- Premium

- Luxury

- By Distribution Channel

- Specialty Stores

- Multi-Brand Retail

- Online / D2C

- Builder / Real Estate Tie-ups

- Direct Sales

- By End-User

- Residential

- Commercial (Hotels, Restaurants, Offices, Hostels)

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Modular Kitchen Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic D2C interior platforms, specialty premium kitchen brands, luxury kitchen importers, or regional modular kitchen manufacturers.

The India Modular Kitchen Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Design

- By Product Type

- By Material

- By Finish

- By Price Range

- By Distribution Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Modular Kitchen Market

- India Modular Kitchen Market Insights

- Market Dynamics

- Growth Drivers

- Rising disposable income, urbanization, and nuclear family growth driving demand for organized kitchen solutions.

- Rapid expansion of real estate, apartment culture, and ready-to-move-in homes boosting modular kitchen adoption.

- E-commerce growth, D2C brands, EMI financing, and influencer-led marketing accelerating category penetration.

- Restraints

- High upfront cost of INR 1.5 lakh to 5 lakh limiting middle-income household adoption.

- Strong unorganized carpenter market and counterfeit / look-alike modular kitchen products.

- Long lead times for customization, installation delays, and after-sales service gaps.

- Opportunities

- Tier-II and Tier-III city expansion creating a massive untapped modular kitchen demand base.

- Smart, IoT-enabled, and connected kitchen solutions opening new premium value pools.

- Builder tie-ups, real estate bundling, and pre-installed kitchen offerings supporting next-generation growth.

- Challenges

- Skilled installer and carpenter shortage limiting on-time project execution across metros and Tier-II cities.

- Raw material price volatility for plywood, MDF, acrylic, stainless steel, and imported hardware.

- Limited consumer awareness of materials, finishes, ergonomic standards, and warranty terms.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (plywood, MDF, particle board, acrylic, stainless steel, glass)

- Hardware & Fittings Manufacturers (Häfele, Hettich, Blum, Ebco, Sleek, Godrej)

- Laminate, Acrylic, PU & Veneer Suppliers (Greenlam, Merino, Century, Stylam)

- Built-in Appliance & Smart Kitchen Solution Providers (Faber, Elica, Kaff, Bosch, Siemens)

- Quality Control, R&D & Testing Laboratories (BIS, FSC, CARB, IS standards)

- Distributors, Dealers & Online Aggregators

- Modular Kitchen Brand Owners (Godrej Interio, Sleek, IKEA, Spacewood, Kutchina)

- Interior Design Studios, D2C Platforms, Builder Tie-ups & Specialty Retail

- Installation, Carpenter Networks & After-Sales Service Providers

- End-Users (residential households, hotels, restaurants, hostels, corporate cafeterias)

- India Modular Kitchen Market: Regulatory Framework

- India Modular Kitchen Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Thousand Units)

- Market Share & Forecast

- By Design

- L-Shaped

- U-Shaped

- Parallel

- Island

- Straight / Linear

- Open Plan

- Others

- By Product Type

- Base Cabinet

- Wall Cabinet

- Tall Unit

- Drawer Unit

- Accessories

- By Material

- Wood (Plywood, MDF, Particle Board)

- Stainless Steel

- Aluminium

- Plastic / Acrylic

- Laminates

- Glass

- Others

- By Finish

- Laminate

- Acrylic

- Membrane

- PU / Lacquer

- Veneer

- Others

- By Price Range

- Economy

- Mid-Range

- Premium

- Luxury

- By Distribution Channel

- Specialty Stores

- Multi-Brand Retail

- Online / D2C

- Builder / Real Estate Tie-ups

- Direct Sales

- By End-User

- Residential

- Commercial (Hotels, Restaurants, Offices, Hostels)

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Modular Kitchen Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Godrej Interio (Godrej & Boyce Mfg. Co. Ltd.)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- Sleek Kitchens (Asian Paints Limited)

- Häfele India Pvt. Ltd.

- Hettich India Pvt. Ltd.

- IKEA India Pvt. Ltd.

- Spacewood Office Solutions Pvt. Ltd.

- Kutchina Home Makers Pvt. Ltd.

- Johnson Kitchens (H & R Johnson India)

- HomeLane (Bro4u Online Services Pvt. Ltd.)

- Livspace Interior Services Pvt. Ltd.

- Pepperfry Modular Kitchens

- Nobilia Kitchen India

- Häcker Kitchens India

- Bonito Designs

- Veneta Cucine India

- Other Prominent Players

- Godrej Interio (Godrej & Boyce Mfg. Co. Ltd.)

- By Design

- Market Size & Forecast, 2021-2032

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India modular kitchen market and what is its growth forecast?

Ans: The India modular kitchen market is valued at USD 2.85 billion in 2025 and is projected to reach USD 6.85 billion by 2032, growing at a CAGR of 13.3%, supported by rising urbanization, premium interior spend, and apartment-driven housing demand.

2. Which segments are driving demand in the India modular kitchen market?

Ans: Residential users dominate the India modular kitchen market with over 78% value share, while L-shaped layouts lead designs and smart, connected modular kitchens are the fastest growing segment, supported by D2C platforms and IoT adoption.

3. What are the key drivers of growth in the India modular kitchen market?

Ans: Key drivers include rising disposable income, urbanization, nuclear family growth, organized real estate expansion, builder bundling, EMI financing, D2C platform scaling, and influencer-led design discovery across India's modular kitchen market.

4. Which regions are driving growth in the India modular kitchen market?

Ans: Maharashtra, Gujarat, Delhi NCR, Karnataka, Tamil Nadu, and Telangana lead the India modular kitchen market, supported by strong organized real estate launches, apartment supply, premium housing demand, and high Tier-I urban category penetration.

5. What are the latest trends in the India modular kitchen market?

Ans: Latest trends include rapid smart and IoT kitchen adoption, premium acrylic and PU finishes, sustainable plywood, D2C interior platform growth, builder tie-ups, and rising AR-based design tools across the India modular kitchen market.

Frequently Asked Questions

1. How large is the India modular kitchen market and what is its growth forecast?

Ans: The India modular kitchen market is valued at USD 2.85 billion in 2025 and is projected to reach USD 6.85 billion by 2032, growing at a CAGR of 13.3%, supported by rising urbanization, premium interior spend, and apartment-driven housing demand.

2. Which segments are driving demand in the India modular kitchen market?

Ans: Residential users dominate the India modular kitchen market with over 78% value share, while L-shaped layouts lead designs and smart, connected modular kitchens are the fastest growing segment, supported by D2C platforms and IoT adoption.

3. What are the key drivers of growth in the India modular kitchen market?

Ans: Key drivers include rising disposable income, urbanization, nuclear family growth, organized real estate expansion, builder bundling, EMI financing, D2C platform scaling, and influencer-led design discovery across India's modular kitchen market.

4. Which regions are driving growth in the India modular kitchen market?

Ans: Maharashtra, Gujarat, Delhi NCR, Karnataka, Tamil Nadu, and Telangana lead the India modular kitchen market, supported by strong organized real estate launches, apartment supply, premium housing demand, and high Tier-I urban category penetration.

5. What are the latest trends in the India modular kitchen market?

Ans: Latest trends include rapid smart and IoT kitchen adoption, premium acrylic and PU finishes, sustainable plywood, D2C interior platform growth, builder tie-ups, and rising AR-based design tools across the India modular kitchen market.