India Lithium-Ion Battery Recycling Market, By Battery Type (Lithium Cobalt Oxide, Lithium Iron Phosphate, Lithium Manganese Oxide, Lithium Nickel Manganese Cobalt Oxide, Lithium Nickel Cobalt Aluminium Oxide, Others); By Source (Electric Vehicles, Consumer Electronics, Industrial Equipment, Energy Storage Systems, Others); By Recycling Process (Hydrometallurgy, Pyrometallurgy, Direct Recycling, Mechanical Processing, Others); By Material Recovered (Lithium, Cobalt, Nickel, Manganese, Copper, Aluminium, Others); By Application (Electric Vehicles & Automotive, Consumer Electronics, Renewable Energy Storage, Industrial Applications, Others); By Distribution Channel (Direct Sales, Third-Party Recyclers, Government Collection Centers, Online Platforms, Others); By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Chemicals & Advanced Materials

- Apr 2026

- Pages 120

- Report Format: pdf

- Report Price: $2500 USD

India Lithium-Ion Battery Recycling Market, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

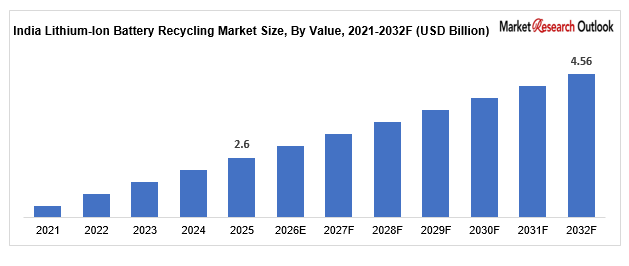

| Market Size (2025) | USD 2.6 Billion |

| CAGR (2026-2032) | 9.80% |

| Leading Segment | Lithium Nickel Manganese |

| Fastest Growing Segment | Lithium Iron Phosphate (LFP) batteries |

| Market Size (2032) | USD 4.56 Billion |

Market Overview

The India Lithium-Ion Battery Recycling market has transitioned from a specialized dietary niche into a commercially significant USD 2.6 Billion industrial segment by the end of the 2032 strategic horizon. Having established a baseline valuation of USD 4.56 Billion in 2025, the market is currently expanding at a robust and consistent CAGR of 9.80%. The accelerated growth process is occurring because people are adopting electric vehicles (EVs) at a fast pace while they consume more consumer electronics and need to obtain critical battery materials through domestic sources. Battery recycling has become a essential element for India to establish itself as a worldwide clean energy center because it enables resource protection and environmental regulation compliance.

NMC batteries which contain Lithium Nickel Manganese and Cobalt serve as the primary recycled product because they are widely used in electric vehicles and their metal content can be recovered. The fastest growing battery segment is Lithium Iron Phosphate (LFP) batteries because their cost advantages and safety features have led to increased implementation in electric vehicles and energy storage systems. The development of new recycling technologies through hydrometallurgy and direct recycling methods brings about substantial improvements in both recovery rates and the financial performance of recycling operations.

The competitive landscape is evolving, with startups and metal recovery companies and large industrial companies have begun operating within the industry market. Regulatory authorities have increased their monitoring activities to guarantee proper material handling and material tracking and material recovery processes. The market development until 2032 will lead to closed-loop recycling systems becoming the primary focus of research and development because these systems enable manufacturers to reuse their recovered materials directly for battery production. The combination of rising investments and backing from legislation and advancements in technology will enable the market to maintain its continuous high-growth period.

Market Drivers

The EV Revolution: Surge in Battery Waste Generation

India’s increasing electric vehicle usage leads to a corresponding rise in lithium-ion battery waste. The need for effective recycling systems starts to become essential when EV batteries enter their final phase. The increasing volume of waste requires recycling to become a fundamental industrial process which results in major financial investments and facility growth.

Resource Security: Reducing Import Dependence

India currently depends primarily on foreign markets to obtain essential battery materials which include lithium and cobalt and nickel. The process of recycling enables countries to extract valuable resources from their waste materials which helps them to maintain stable supply chains while decreasing price fluctuations. The strategic benefit of advanced recycling technologies is driving governments and businesses to invest in these technologies.

Market Challenges

Collection Inefficiencies: Fragmented Supply Chain

The Indian market faces its main challenge because there is no efficient system to collect batteries. The informal scrap dealers handle most of the used batteries which results in poor recycling practices and creates environmental hazards. The industry needs to establish a formal collection system which allows for complete tracking of collected materials as its main obstacle to business expansion.

High Capital and Technological Barriers

The advanced recycling processes which include hydrometallurgy and direct recycling require both substantial financial backing and specialized technical knowledge. The absence of unified technological standards together with restricted national capabilities causes operational expenses to increase, which hinders new companies from achieving successful expansion.

Segmental Analysis

The Indian lithium-ion battery recycling market shows dominance of NMC battery types because these batteries contain valuable metals and they are widely used in electric vehicle applications. The recycling stream receives substantial contributions from LCO batteries which function as the primary power source in consumer electronics. The fastest growth of LFP batteries occurs because they receive wider adoption in electric vehicles and energy storage systems. The niche applications of LMO and NCA battery chemistries receive support from their smaller yet essential functions.

By recycling process, Hydrometallurgy leads the market due to its higher recovery rates and environmental efficiency compared to traditional methods. Pyrometallurgy maintains its importance for extensive industrial processes while Direct Recycling has developed into an advanced technology that maintains battery material structure yet boosts overall efficiency. The material separation process begins with the application of Mechanical and Physical processes which serve as initial stages.

Regional Analysis

The Indian lithium-ion battery recycling market operates from its core industrial and urban centers. The market in West India centers on Maharashtraand Gujarat because of its industrial baseand port facilities and major recycling centers. The region also benefits from proximity to automotive manufacturing clusters. South India has become a major growth area because of its expanding electric vehicle production and technology centers in Tamil Naduand Karnataka. The existence of electronics manufacturing clusters creates additional demand for battery recycling operations.

Recent Developments

- Policy Push & EPR Implementation: The Battery Waste Management Rules 2022 together with Extended Producer Responsibility frameworks establish formal procedures which require battery recycling operations to demonstrate their responsibility for recycling activities.

- Strategic Investments & Capacity Expansion: Startups and traditional companies are raising funds for scaling and implementing recycling plants using refined means of technology.

- OEM Partnerships: Almost all automotive and battery producers are exploring partnerships with recyclers to work together to ensure closed-loop supply chains.

Key Market Players

- Attero Recycling Pvt. Ltd.

- Lohum Cleantech Pvt. Ltd.

- Gravita India Ltd.

- Exigo Recycling Pvt. Ltd.

- RecycleKaro India Pvt. Ltd.

- Metastable Materials Pvt. Ltd.

- BatX Energies Pvt. Ltd.

- E-Parisaraa Pvt. Ltd.

- TES-AMM India Pvt. Ltd.

- SungEel India Recycling Pvt. Ltd.

Segmentation

- Battery Type

- Lithium Cobalt Oxide (LCO)

- Lithium Iron Phosphate (LFP)

- Lithium Manganese Oxide (LMO)

- Lithium Nickel Manganese Cobalt (NMC)

- Lithium Nickel Cobalt Aluminum Oxide (NCA)

- Others

- Recycling Process

- Hydrometallurgy

- Pyrometallurgy

- Direct Recycling

- Mechanical / Physical Process

- Others

- Recovered Material

- Lithium

- Cobalt

- Nickel

- Manganese

- Graphite

- Aluminium & Copper

- Others

- Source

- Electric Vehicles (EV) Batteries

- Consumer Electronics Batteries

- Industrial & Energy Storage Batteries

- Others

- End Use Industry

- Automotive & Electric Vehicles

- Consumer Electronics

- Energy Storage Systems (ESS)

- Industrial Manufacturing

- Others

- Distribution Channel

- OEM & Battery Manufacturers (Direct Tie-ups)

- Authorized Collection & Aggregation Centers

- Third-Party Recyclers & Scrap Dealers

- Government & Municipal Collection Programs

- Online / Digital B2B Platforms

- Region

- East India

- West India

- North India

- South India

Table of Contents:

- Executive Summary

- Research Methodology

- Report Scope

- Market Definition

- Inclusions & Exclusions

- Research Methodology

- India Lithium-Ion Battery Recycling Market Overview

- Market Evolution in India

- Industry Value Chain Overview

- Ecosystem Mapping

- Pricing Analysis Overview

- Market Dynamics

- Drivers

- Challenges

- Opportunities

- Emerging Trends

- Market Attractiveness Index

- Consumer Behaviour Analysis

- Buying Patterns

- Price Sensitivity

- Urban vs Tier 2 Demand

- Policy & Regulatory Landscape

- India Lithium-Ion Battery Recycling Market Outlook

- Market Size & Forecast, 2021-2032

- By Value

- By Volume

- Market Share & Forecast by Battery Type

- Lithium Cobalt Oxide (LCO)

- Lithium Iron Phosphate (LFP)

- Lithium Manganese Oxide (LMO)

- Lithium Nickel Manganese Cobalt (NMC)

- Lithium Nickel Cobalt Aluminum Oxide (NCA)

- Others

- Market Share & Forecast by Recycling Process

- Hydrometallurgy

- Pyrometallurgy

- Direct Recycling

- Mechanical / Physical Process

- Others

- Market Share & Forecast by Recovered Material

- Lithium

- Cobalt

- Nickel

- Manganese

- Graphite

- Aluminium & Copper

- Others

- Market Share & Forecast by Source

- Electric Vehicles (EV) Batteries

- Consumer Electronics Batteries

- Industrial & Energy Storage Batteries

- Others

- Market Share & Forecast by End Use Industry

- Automotive & Electric Vehicles

- Consumer Electronics

- Energy Storage Systems (ESS)

- Industrial Manufacturing

- Others

- Market Share & Forecast by Distribution Channel

- OEM & Battery Manufacturers (Direct Tie-ups)

- Authorized Collection & Aggregation Centers

- Third-Party Recyclers & Scrap Dealers

- Government & Municipal Collection Programs

- Online / Digital B2B Platforms

- Market Share & Forecast by Region

- East India

- West India

- North India

- South India

- Market Size & Forecast, 2021-2032

- Competitive Landscape

- Market Share Analysis

- Competitive Benchmarking

- Company Profiles

- Product Portfolio Comparison

- Strategic Developments

- Strategic Recommendations

- Growth Strategies for New Entrants

- Expansion Strategies for Existing Players

- Investment Opportunities

Frequently Asked Questions

1. What is the projected market size of the India Lithium-Ion Battery Recycling Market in 2025?

Ans: The India Lithium-Ion Battery Recycling market is estimated to be valued at approximately USD 2.6 Billion in 2025.

2. What is the expected growth rate (CAGR) of the India Lithium-Ion Battery Recycling Market during the forecast period?

Ans: The market is expected to exhibit a robust CAGR of 9.80% during the forecast period between 2026 and 2032.

3. What is the forecast value of the India Lithium-Ion Battery Recycling Market by 2032?

Ans: By the end of the strategic horizon in 2032, the India Lithium-Ion Battery Recycling market is projected to reach a valuation of approximately USD 4.56 Billion.

4. What are the major factors driving the growth of the India Lithium-Ion Battery Recycling Market?

Ans: The accelerated growth process is occurring because people are adopting electric vehicles (EVs) at a fast pace while they consume more consumer electronics and need to obtain critical battery materials through domestic sources.

5. Name the key players operating in the India Lithium-Ion Battery Recycling Market.

Ans: Prominent players shaping the Indian landscape include Attero Recycling Pvt. Ltd., Lohum Cleantech Pvt. Ltd., Gravita India Ltd., Exigo Recycling Pvt. Ltd., RecycleKaro India Pvt. Ltd., Metastable Materials Pvt. Ltd., BatX Energies Pvt. Ltd., E-Parisaraa Pvt. Ltd., TES-AMM India Pvt. Ltd., SungEel India Recycling Pvt. Ltd., and other prominent players.

6. Which regions/cities are expected to lead the growth in the India Lithium-Ion Battery Recycling Market?

Ans: The market in West India centers on Maharashtraand Gujarat because of its industrial baseand port facilities and major recycling centers.

Frequently Asked Questions

1. What is the projected market size of the India Lithium-Ion Battery Recycling Market in 2025?

Ans: The India Lithium-Ion Battery Recycling market is estimated to be valued at approximately USD 2.6 Billion in 2025.

2. What is the expected growth rate (CAGR) of the India Lithium-Ion Battery Recycling Market during the forecast period?

Ans: The market is expected to exhibit a robust CAGR of 9.80% during the forecast period between 2026 and 2032.

3. What is the forecast value of the India Lithium-Ion Battery Recycling Market by 2032?

Ans: By the end of the strategic horizon in 2032, the India Lithium-Ion Battery Recycling market is projected to reach a valuation of approximately USD 4.56 Billion.

4. What are the major factors driving the growth of the India Lithium-Ion Battery Recycling Market?

Ans: The accelerated growth process is occurring because people are adopting electric vehicles (EVs) at a fast pace while they consume more consumer electronics and need to obtain critical battery materials through domestic sources.

5. Name the key players operating in the India Lithium-Ion Battery Recycling Market.

Ans: Prominent players shaping the Indian landscape include Attero Recycling Pvt. Ltd., Lohum Cleantech Pvt. Ltd., Gravita India Ltd., Exigo Recycling Pvt. Ltd., RecycleKaro India Pvt. Ltd., Metastable Materials Pvt. Ltd., BatX Energies Pvt. Ltd., E-Parisaraa Pvt. Ltd., TES-AMM India Pvt. Ltd., SungEel India Recycling Pvt. Ltd., and other prominent players.

6. Which regions/cities are expected to lead the growth in the India Lithium-Ion Battery Recycling Market?

Ans: The market in West India centers on Maharashtraand Gujarat because of its industrial baseand port facilities and major recycling centers.