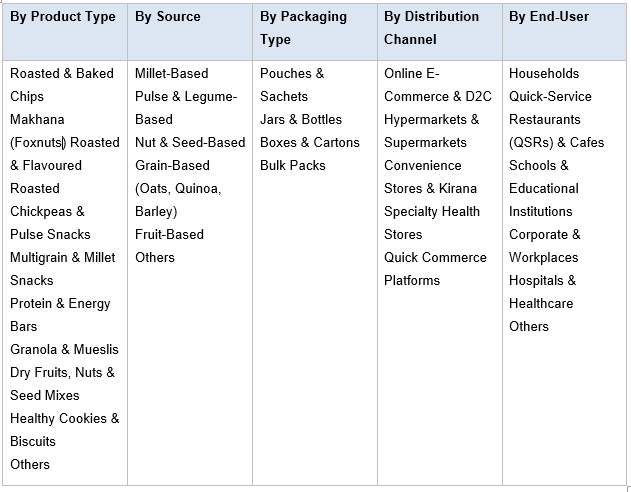

India Healthy Snacks Market, By Product Type (Roasted & Baked Chips, Makhana / Foxnuts, Roasted Chickpeas & Pulse Snacks, Multigrain & Millet Snacks, Protein & Energy Bars, Granola & Mueslis, Dry Fruits, Nuts & Seed Mixes, Healthy Cookies & Biscuits, Others); By Source (Millet-Based, Pulse & Legume-Based, Nut & Seed-Based, Grain-Based, Fruit-Based, Others); By Packaging Type (Pouches & Sachets, Jars & Bottles, Boxes & Cartons, Bulk Packs); By Distribution Channel (Online E-Commerce & D2C, Hypermarkets & Supermarkets, Convenience Stores & Kirana, Specialty Health Stores, Quick Commerce Platforms); By End-User (Households, Quick-Service Restaurants & Cafes, Schools & Educational Institutions, Corporate & Workplaces, Hospitals & Healthcare); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Food, Beverage & Nutrition

- May 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Healthy Snacks Market: Rising Health Awareness, Millet Mission, and Quick Commerce Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

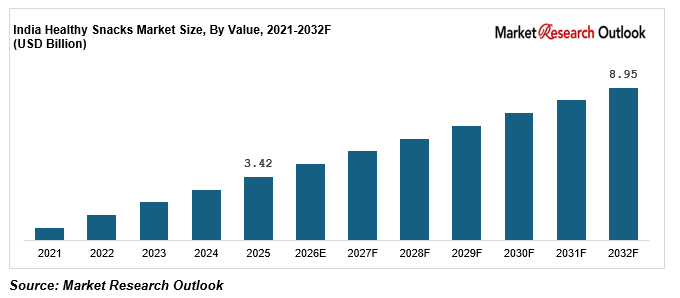

| Market Size (2025) | USD 3.42 Billion |

| CAGR (2026-2032) | 14.7% |

| Leading Segment | Makhana, Roasted Chickpeas & Dry Fruit Snacks |

| Fastest Growing Segment | Millet-Based and High-Protein Functional Healthy Snacks |

| Market Size (2032) | USD 8.95 Billion |

Source: Market Research Outlook

Market Overview: India Healthy Snacks Market

The India healthy snacks market size is witnessing rapid expansion, driven by rising health consciousness, accelerating lifestyle disease awareness, government-led millet promotion, expanding D2C and quick commerce distribution, and major capacity additions by Indian FMCG majors and emerging D2C startups. Valued at USD 3.42 Billion in 2025 and projected to reach USD 8.95 Billion by 2032, growing at a CAGR of 14.7%, the India healthy snacks market growth is being fuelled by strong household demand under metros and tier-1 cities, rising tier-2 city procurement tied to growing health awareness and disposable income, and accelerating modern trade and quick commerce shelf expansion. Roasted makhana, roasted chickpeas, dry fruit mixes, multigrain biscuits, and baked chips lead consumption, while millet-based snacks, protein bars, and functional fortified healthy snacks are emerging as the fastest growing category. Tightening FSSAI Front-of-Pack Labelling requirements, Eat Right India movement, and growing quick commerce penetration are reshaping the supply landscape. As branded players including ITC, Britannia, PepsiCo, Marico, and Tata Consumer Products expand integrated healthy snacks portfolios, and D2C disruptors including The Whole Truth Foods, Open Secret, Farmley, True Elements, and Happilo scale premium product pipelines, the India healthy snacks market is evolving into a consumer-led, innovation-driven, and digitally distributed ecosystem with strong long-term growth potential.

Key Report Takeaways: India Healthy Snacks Market

- The India healthy snacks market size is projected to grow from USD 3.42 Billion in 2025 to USD 8.95 Billion by 2032, registering a strong CAGR of 14.7%, driven by accelerated health consciousness, government-led millet adoption, rising D2C brand penetration, and the structural shift toward clean-label nutritious snacking across the India healthy snacks market.

- Roasted makhana, roasted chickpeas, dry fruit mixes, multigrain biscuits, and baked chips dominate the India healthy snacks market, accounting for over 58% of total revenues in 2025, driven by traditional consumer familiarity, mass affordability, and broad distribution reach across modern trade and kirana channels.

- Millet-based snacks, high-protein bars, and functional fortified healthy snacks are emerging as the fastest growing categories in the India healthy snacks market, expected to grow at 24 to 30% annually as government millet promotion, premium D2C brands, and quick commerce shelf expansion reshape sourcing priorities.

- Rapid scaling of quick commerce and D2C platforms, with Blinkit, Zepto, Swiggy Instamart, BB Now, Amazon India, and brand websites contributing 22 to 26% of total healthy snacks sales, is structurally expanding the India healthy snacks market across metros, tier-1, and emerging tier-2 cities.

- Rising investments by Indian FMCG majors and D2C disruptors such as ITC, Tata Consumer Products, Marico, The Whole Truth Foods, Farmley, and Open Secret in product innovation, manufacturing capacity, and millet-based snack ranges are strengthening domestic supply and supporting the India healthy snacks market forecast 2032.

Key Market Drivers: India Healthy Snacks Market

Rising Health Consciousness, Lifestyle Disease Awareness, and Diabetes-Obesity Concerns Driving India Healthy Snacks Market Adoption

Growth in the India healthy snacks market is being driven by rapidly rising health awareness, lifestyle disease prevalence, and growing consumer concern around diabetes, obesity, hypertension, and cardiovascular health. The International Diabetes Federation (IDF) estimates over 101 million Indians lived with diabetes in 2024, with another 136 million pre-diabetic, while the National Family Health Survey (NFHS-5) reports that approximately 24% of urban adults are overweight or obese. Urban Indian consumers are increasingly substituting traditional fried namkeen, biscuits, and namkeen mixtures with baked chips, roasted makhana, roasted chickpeas, multigrain biscuits, protein bars, and granola across the India healthy snacks market. According to the Indian Council of Medical Research (ICMR), per-capita salt and sugar intake among urban Indians exceeds WHO daily recommendations by 50 to 70%, fuelling consumer interest in low-sodium, low-sugar, and reduced-fat snack alternatives. Premium urban households now allocate 12 to 18% of grocery basket spend on healthy snacks, supported by paediatrician and nutritionist endorsements, growing wellness culture, post-pandemic immunity focus, and millennial-led parent preferences for nutritious mid-meal snacking options across the India healthy snacks market through 2032.

Government-Led International Year of Millets, FSSAI Eat Right Initiative, and Shree Anna Yojana Boosting India Healthy Snacks Market Demand

The India healthy snacks market is benefiting from sustained policy push around millet adoption, healthy eating, and food labelling reforms. The United Nations declared 2023 as the International Year of Millets, an initiative championed by India, and the Government of India launched the National Year of Millets in 2018 along with the National Mission on Millets and Shree Anna Yojana. The Ministry of Food Processing Industries has approved the Production Linked Incentive (PLI) scheme for the food processing sector with an outlay of INR 10,900 crore, prioritising millet-based ready-to-eat foods and innovative healthy snack products across the India healthy snacks market. The Food Safety and Standards Authority of India (FSSAI) introduced the Eat Right India movement, mandatory Front-of-Pack Labelling (FOPL) regulations, and Indian Nutrition Rating star ratings to guide consumer choices toward healthier processed foods. ITC, Tata Consumer Products, Britannia, PepsiCo, and Marico have launched millet-based snack ranges including Tata Soulfull Ragi Bites, ITC Sunfeast Yippee Millet Mix, and Quaker Oats Millet variants, accelerating mainstream adoption across the India healthy snacks market through 2032.

Expansion of Quick Commerce, D2C Platforms, and Modern Trade Channels Strengthening India Healthy Snacks Market Reach

Rapid expansion of quick commerce, D2C platforms, and modern trade is a major catalyst for the India healthy snacks market, with online channels now contributing an estimated 22 to 26% of total healthy snacks sales. Quick commerce platforms including Blinkit, Zepto, Swiggy Instamart, BB Now, and Dunzo have scaled assortment across roasted makhana, protein bars, baked chips, multigrain biscuits, and granola, with average delivery times under 15 minutes driving impulse purchase conversion across the India healthy snacks market. D2C brand websites including Farmley, The Whole Truth Foods, Open Secret, True Elements, and Happilo have built strong digital-first brand equity, with cumulative D2C healthy snacks funding crossing USD 280 million between 2022 and 2025. Modern trade chains including Reliance Smart, DMart, Spencer’s, More Retail, and Nature’s Basket have expanded dedicated healthy snacks sections, while Amazon India and Flipkart Grocery contribute substantial recurring volumes. Subscription-based health snack boxes, brand-led D2C apps, and quick commerce dark stores are accelerating customer acquisition and broadening the India healthy snacks market reach across metros, tier-1, and emerging tier-2 cities through 2032.

Key Market Challenges: India Healthy Snacks Market

Price Premium of Healthy Snacks Compared to Traditional Snacks Restricting Mass-Market Penetration of India Healthy Snacks Market

The India healthy snacks market continues to face significant pricing barriers, particularly for premium D2C and clean-label products. Premium healthy snack brands including The Whole Truth Foods, Open Secret, Yoga Bar, Farmley, and True Elements typically retail at INR 60 to 250 per 100 grams, representing a 2 to 4 times price premium over traditional namkeen, biscuits, chips, and savouries from Haldiram’s, Bikaji, Lays, Bingo, and Parle. Middle-class and lower-middle-class Indian households remain highly price-sensitive on impulse-purchase categories, restricting adoption of premium healthy snacks beyond metros and tier-1 cities of the India healthy snacks market. Production costs for healthy snacks are structurally higher due to premium ingredients including almonds, dates, makhana, millets, jaggery, and cold-pressed oils, smaller batch sizes, FSSAI-compliant certifications, sustainable packaging requirements, and frequent product reformulations. Distribution costs through quick commerce and D2C also remain elevated relative to traditional FMCG margins. While the introduction of smaller pack sizes priced INR 10 to 30 by Farmley, Tata Soulfull, and Open Secret are gradually addressing affordability barriers, the persistent cost gap continues to be a central commercial constraint across the India healthy snacks market through 2032.

Misleading Health Claims, Healthy-Halo Marketing, and Regulatory Scrutiny on Front-of-Pack Labelling Constraining India Healthy Snacks Market

A growing regulatory and consumer trust challenge facing the India healthy snacks market is the prevalence of misleading health claims, healthy-halo marketing, and inconsistent product labelling, prompting tightening oversight from FSSAI and the Advertising Standards Council of India (ASCI). FSSAI introduced Front-of-Pack Labelling (FOPL) regulations and the Indian Nutrition Rating star-rating system in 2022 to bring transparency to processed food nutrition profiles, with full mandatory rollout expected through 2026 across the India healthy snacks market. ASCI has issued multiple advisories against misleading low-fat, sugar-free, all-natural, no-preservative, and 100% healthy claims in the snack and FMCG sector, with several leading brands facing public complaints during 2023 and 2024. The Whole Truth Foods has built brand differentiation around transparent ingredient positioning, but smaller and unbranded healthy snacks producers continue to make exaggerated nutritional claims, eroding consumer trust. The FSSAI Eat Right India initiative requires reformulation, transparent ingredient labelling, and reduced sugar, salt, and fat content, raising compliance and reformulation costs across the India healthy snacks market and creating execution complexity for category players through 2032.

Short Shelf Life of Preservative-Free Healthy Snacks and Cold-Chain Distribution Challenges Constraining India Healthy Snacks Market

The India healthy snacks market faces structural distribution challenges related to short shelf life of preservative-free products, complex cold-chain logistics, and uneven temperature-controlled retail infrastructure across tier-2 and tier-3 cities. Premium clean-label healthy snacks, particularly fresh granola, no-preservative protein bars, fresh fruit-based snacks, low-sugar jaggery cookies, and dairy-based makhana variants, typically have shelf lives of 60 to 120 days, compared to 6 to 9 months for conventional snacks with preservatives. India’s cold-chain infrastructure remains underdeveloped, with only 30 to 35% of perishable food production routed through temperature-controlled storage according to NCCD (National Centre for Cold-Chain Development) estimates, limiting reach across the India healthy snacks market. Distribution wastage rates for healthy snacks range between 8 and 14%, materially higher than conventional snacks, eroding producer margins and constraining national rollout. Quick commerce dark stores, while expanding rapidly, are concentrated in top 20 to 25 metros, limiting deeper tier-2 city penetration. Brands such as Farmley, Open Secret, True Elements, and Wingreens are investing in modified atmosphere packaging, nitrogen-flushed pouches, and resealable jars to extend shelf life, but logistics challenges continue to be a near-term execution constraint across the India healthy snacks market through 2032.

Key Market Trends: India Healthy Snacks Market

Rapid Adoption of Millet-Based, High-Protein, and Functional Healthy Snacks Across Premium Indian Consumers

The India healthy snacks market is undergoing a clear product shift toward millet-based, high-protein, functional, and fortified snack categories, with these segments expected to capture over 38% of new healthy snacks launches by 2028. Millet-based snacks including jowar chips, ragi puffs, bajra-based mixtures, and foxtail millet bars are gaining strong traction across Tata Soulfull Ragi Bites, Slurrp Farm, Bagrry’s Millet Mueslis, and ITC Sunfeast Yippee Millet variants. High-protein snacks including The Whole Truth Foods protein bars, Yoga Bar Multigrain bars (now under ITC), and Open Secret protein-fortified cookies are scaling rapidly across metros of the India healthy snacks market. Functional snacks targeting immunity (ashwagandha, tulsi, turmeric infused), gut health (prebiotic, probiotic), and diabetes management (low-GI, sugar-free) are gaining premium positioning. According to industry estimates, millet-based snacks alone grew at over 30% annually during 2023 to 2025, accelerated by the International Year of Millets in 2023. This product mix shift, combined with rising health-conscious urban demand, is reinforcing the India healthy snacks market forecast 2032 across premium urban and metro consumer segments.

Growth of D2C Brands, Subscription-Based Healthy Snack Boxes, and Quick Commerce Dark Stores Reshaping India Healthy Snacks Market

A clear shift toward D2C brands, subscription-based healthy snack boxes, and quick commerce dark stores is reshaping the India healthy snacks market, particularly in metros and tier-1 cities. D2C-first brands including The Whole Truth Foods, Open Secret, Farmley, True Elements, Happilo, and EAT Anytime have built combined annualised revenue exceeding INR 1,500 crore by 2025, with online and quick commerce contributing 60 to 75% of category sales. Subscription-based healthy snack boxes from Open Secret, EAT Anytime, and various direct-to-home services are accelerating customer retention and repeat purchase frequency across the India healthy snacks market. Quick commerce platforms including Blinkit (Zomato), Zepto, Swiggy Instamart, BB Now, and Dunzo have expanded dedicated healthy snacks shelves, with category contribution often exceeding 8% of total grocery orders. Branded D2C apps and digital service platforms are also reducing customer acquisition costs and accelerating healthy snacks adoption across both impulse and planned purchase moments in the India healthy snacks market.

Capacity Expansion by FMCG Majors, D2C Acquisitions, and Vertical Integration of Healthy Snacks Manufacturing in India

A wave of FMCG mergers and acquisitions, D2C deals, and vertical integration is reshaping the India healthy snacks market supply landscape. Combined India-focused acquisition and capital expenditure announcements by ITC, Tata Consumer Products, Marico, Britannia, and PepsiCo exceeded USD 480 million between 2022 and 2025. ITC acquired Yoga Bar (Sprout Life Foods) in 2023 for approximately INR 350 to 400 crore, Marico acquired Plix (vegan nutrition brand) and made strategic investments in True Elements, Tata Consumer Products acquired Soulfull for millet-based snacks, Britannia expanded NutriChoice and Pro range, and PepsiCo scaled Quaker Oats and lower-sodium Doritos across the India healthy snacks market. Domestic manufacturing capacity expansion across millet snacks, makhana processing, oats milling, and protein bar production is rising under Production Linked Incentive (PLI) scheme allocations for the food processing sector. Combined with rising urban premium demand, expanding tier-2 city penetration, and quick commerce-led distribution acceleration, these developments are reinforcing the India healthy snacks market forecast 2032 across the entire value chain.

Segmental Insights: India Healthy Snacks Market

By Product Type: Makhana, Roasted Chickpeas, and Dry Fruit Mixes Dominate the India Healthy Snacks Market

Roasted makhana, roasted chickpeas, dry fruit and nut mixes, multigrain biscuits, and baked chips lead the India healthy snacks market product landscape, accounting for an estimated 58 to 62% of total revenues, driven by mass-market familiarity, broad price accessibility, and deep distribution reach across modern trade, kirana, and quick commerce channels. Makhana has emerged as a particularly strong category, with Farmley, Too Yumm!, and ITC leading branded packaging volumes across the India healthy snacks market. Protein and energy bars contribute another 12 to 14% of the India healthy snacks market, primarily through The Whole Truth Foods, Yoga Bar (ITC), Open Secret, and EAT Anytime in metros and tier-1 cities. Granola, mueslis, and oat-based healthy snacks account for 10 to 12%, led by Bagrry’s, True Elements, Marico Saffola Oats, and PepsiCo Quaker. Multigrain and millet-based snacks together capture another 14 to 16% of the India healthy snacks market, with Tata Soulfull Ragi Bites, ITC Sunfeast Yippee Millet variants, and Slurrp Farm scaling rapidly under millet mission tailwinds. In 2025, leading healthy snacks players scaled up product assortment and innovation pipelines across the India healthy snacks market.

By Distribution Channel: Quick Commerce Grows Fastest While Modern Trade and Kirana Lead Volume

Convenience stores, kirana outlets, and modern trade together continue to lead the India healthy snacks market by total volume, accounting for approximately 52 to 56% of total healthy snacks sales, driven by traditional FMCG distribution depth of ITC, Britannia, PepsiCo, Marico, and Tata Consumer Products across Indian cities and towns. Online e-commerce and D2C is the fastest growing distribution channel within the India healthy snacks market, expanding at 28 to 34% annually, with Amazon India, Flipkart Grocery, and brand D2C platforms now contributing 14 to 18% of total sales. Quick commerce platforms including Blinkit, Zepto, Swiggy Instamart, BB Now, and Dunzo account for another 8 to 10% of the India healthy snacks market, scaling rapidly with dedicated healthy snacks shelves and dark-store assortment. Hypermarkets and supermarkets such as Reliance Smart, DMart, Spencer’s, and Nature’s Basket contribute another 14 to 16% of category sales. Leading brands have aligned omni-channel strategies, driving premium healthy snacks adoption across the India healthy snacks market.

Regional Insights: India Healthy Snacks Market

Regional analysis of the India healthy snacks market shows that West India and South India collectively account for approximately 56 to 60% of total healthy snacks sales, driven by Maharashtra, Gujarat, Karnataka, Tamil Nadu, Telangana, Andhra Pradesh, and Kerala, supported by high urbanisation, premium consumer demographics, strong modern trade depth, and concentrated D2C and quick commerce activity. North India contributes around 24 to 27% of demand, led by Delhi NCR, Punjab, Haryana, Uttar Pradesh, and Rajasthan, supported by growing health awareness, rising tier-1 and tier-2 city affluence, and strong makhana production base in Bihar feeding north Indian markets. Central and East India together account for 16 to 18% of demand, supported by Madhya Pradesh, Chhattisgarh, West Bengal, Bihar (the largest makhana producing state), and Odisha, where tier-2 city consumption and millet adoption are accelerating. In 2025, capacity additions and distribution expansion by ITC across pan-India FMCG channels, Tata Consumer Products across South and West India, Britannia across modern trade, Farmley across quick commerce, and The Whole Truth Foods across D2C reinforced regional supply hubs, supporting closer execution of healthy snacks offerings across the India healthy snacks market.

Recent Developments: India Healthy Snacks Market

- The India healthy snacks market witnessed strong momentum in M&A activity, product launches, and category innovation during 2024 and 2025. ITC acquired Yoga Bar (Sprout Life Foods) in 2023 for approximately INR 350 to 400 crore, integrating premium protein and multigrain bars into ITC’s portfolio. Marico expanded into healthy snacks through True Elements and Plix investments. Tata Consumer Products scaled Tata Soulfull Ragi Bites and other millet-based snacks under the Shree Anna Yojana tailwind. Combined product launches and brand integration are strengthening the India healthy snacks market across the premium segment.

- Domestic healthy snacks brands have deepened India-focused capacity expansion. In 2025, ITC expanded Yoga Bar and Sunfeast Yippee millet variants production, Britannia scaled NutriChoice and Pro range manufacturing, PepsiCo expanded Quaker Oats and lower-sodium Doritos operations, Marico scaled Saffola FITTIFY and Plix capacity, and D2C players including Farmley, The Whole Truth Foods, Open Secret, and True Elements expanded co-packing partnerships under FSSAI-licensed facilities. Domestic manufacturing of makhana processing, oat milling, and millet snack production under Production Linked Incentive scheme allocations is rising rapidly, strengthening domestic supply and supporting the India healthy snacks market forecast 2032.

- Quick commerce and D2C momentum gained strong traction across the India healthy snacks market. In 2025, leading brands including ITC, Britannia, Farmley, The Whole Truth Foods, Open Secret, True Elements, and Happilo expanded shelf presence on Blinkit, Zepto, Swiggy Instamart, and BB Now, with dedicated healthy snacks categories on each platform. Strategic partnerships between FMCG majors, D2C disruptors, quick commerce platforms such as Blinkit and Zepto, and modern trade chains including Reliance Smart and DMart are positioning India as one of the most actively scaling healthy snacks markets in Asia, strengthening long-term competitive positioning in the India healthy snacks market forecast 2032.

Key Market Players: India Healthy Snacks Market

- ITC Limited (Sunfeast, Yoga Bar)

- Britannia Industries Limited (NutriChoice)

- PepsiCo India Holdings Pvt. Ltd. (Quaker)

- Marico Limited (Saffola FITTIFY)

- Tata Consumer Products Limited (Tata Soulfull)

- The Whole Truth Foods (And Nothing Else Pvt. Ltd.)

- Open Secret (Open Secret Pvt. Ltd.)

- Farmley (Hyfun Foods Pvt. Ltd.)

- True Elements (Wholsum Foods Pvt. Ltd.)

- Wingreens Farms Pvt. Ltd.

- Bagrry’s India Limited

- Happilo International Pvt. Ltd.

- Guiltfree Industries Ltd. (Too Yumm! / RPG Group)

Report Scope

In this report, the India Healthy Snacks Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Roasted & Baked Chips

- Makhana (Foxnuts) Roasted & Flavoured

- Roasted Chickpeas & Pulse Snacks

- Multigrain & Millet Snacks

- Protein & Energy Bars

- Granola & Mueslis

- Dry Fruits, Nuts & Seed Mixes

- Healthy Cookies & Biscuits

- Others

- By Source

- Millet-Based

- Pulse & Legume-Based

- Nut & Seed-Based

- Grain-Based (Oats, Quinoa, Barley)

- Fruit-Based

- Others

- By Packaging Type

- Pouches & Sachets

- Jars & Bottles

- Boxes & Cartons

- Bulk Packs

- By Distribution Channel

- Online E-Commerce & D2C

- Hypermarkets & Supermarkets

- Convenience Stores & Kirana

- Specialty Health Stores

- Quick Commerce Platforms

- By End-User

- Households

- Quick-Service Restaurants (QSRs) & Cafes

- Schools & Educational Institutions

- Corporate & Workplaces

- Hospitals & Healthcare

- Others

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Healthy Snacks Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging D2C healthy snacks startups, specialty millet and pulse-based snack producers, functional and fortified snacks developers, organic and clean-label brands, or niche regional makhana and dry fruit suppliers operating across the India healthy snacks market.

The India Healthy Snacks Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Source

- By Packaging Type

- By Distribution Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Healthy Snacks Market

- India Healthy Snacks Market Insights

- Market Dynamics

- Growth Drivers

- Rising health consciousness, diabetes-obesity concerns, and lifestyle disease awareness driving India healthy snacks market adoption.

- Government-led International Year of Millets, FSSAI Eat Right initiative, and Shree Anna Yojana boosting India healthy snacks market demand.

- Expansion of quick commerce, D2C platforms, and modern trade channels strengthening India healthy snacks market reach.

- Restraints

- Price premium of healthy snacks vs. traditional snacks restricting mass-market penetration in India.

- Misleading health claims, healthy-halo marketing, and regulatory scrutiny on Front-of-Pack Labelling (FOPL) under FSSAI.

- Short shelf life of preservative-free snacks and underdeveloped cold-chain distribution infrastructure across India.

- Opportunities

- Tier-2, tier-3, and rural India penetration with affordable smaller pack sizes creating long-term mass-market healthy snacks opportunity.

- Functional, fortified, and diabetic-friendly healthy snacks including protein-fortified, prebiotic, and immunity-boosting variants opening new value pools.

- Plant-based, vegan, gluten-free, and keto-friendly healthy snacks driven by millennial and Gen Z demand supporting next-generation growth.

- Challenges

- Slow tier-2 and tier-3 city adoption of premium clean-label healthy snacks restricting near-term mass-market reach.

- Limited cold-chain and modified atmosphere packaging infrastructure across rural and semi-urban India healthy snacks market.

- Inconsistent FSSAI Front-of-Pack Labelling enforcement and proliferation of misleading health claims across smaller brands.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (millets, makhana, oats, pulses, dry fruits, jaggery, cold-pressed oils, sustainable packaging)

- Ingredient & Source Suppliers (millet aggregators, makhana FPOs in Bihar, dry fruit importers, oat millers)

- Healthy Snack Manufacturers & Co-Packers (contract manufacturers, FSSAI-licensed facilities)

- Functional Ingredient & Fortification Suppliers (protein isolates, prebiotics, ashwagandha, vitamin premixes)

- Quality Control, R&D & Food Testing Laboratories (FSSAI, NABL accredited, Eat Right India certified)

- Distributors, Dealers & Online Aggregators (Amazon India, Flipkart Grocery, Blinkit, Zepto, Swiggy Instamart, BB Now)

- Branded Healthy Snacks OEMs (ITC, Britannia, PepsiCo, Marico, Tata Consumer Products)

- D2C Healthy Snack Brands (The Whole Truth Foods, Open Secret, Farmley, True Elements, Happilo)

- Modern Trade & Quick Commerce (Reliance Smart, DMart, Spencer’s, More Retail, Nature’s Basket)

- End-Users (Households, QSRs & Cafes, Schools, Corporate, Hospitals)

- India Healthy Snacks Market: Regulatory Framework

- India Healthy Snacks Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Million Units Sold)

- Market Share & Forecast

- By Product Type

- Roasted & Baked Chips

- Makhana (Foxnuts) Roasted & Flavoured

- Roasted Chickpeas & Pulse Snacks

- Multigrain & Millet Snacks

- Protein & Energy Bars

- Granola & Mueslis

- Dry Fruits, Nuts & Seed Mixes

- Healthy Cookies & Biscuits

- Others

- By Source

- Millet-Based

- Pulse & Legume-Based

- Nut & Seed-Based

- Grain-Based (Oats, Quinoa, Barley)

- Fruit-Based

- Others

- By Packaging Type

- Pouches & Sachets

- Jars & Bottles

- Boxes & Cartons

- Bulk Packs

- By Distribution Channel

- Online E-Commerce & D2C

- Hypermarkets & Supermarkets

- Convenience Stores & Kirana

- Specialty Health Stores

- Quick Commerce Platforms

- By End-User

- Households

- Quick-Service Restaurants (QSRs) & Cafes

- Schools & Educational Institutions

- Corporate & Workplaces

- Hospitals & Healthcare

- Others

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Healthy Snacks Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- ITC Limited (Sunfeast, Yoga Bar)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- Britannia Industries Limited (NutriChoice)

- PepsiCo India Holdings Pvt. Ltd. (Quaker)

- Marico Limited (Saffola FITTIFY)

- Tata Consumer Products Limited (Tata Soulfull)

- The Whole Truth Foods (And Nothing Else Pvt. Ltd.)

- Open Secret (Open Secret Pvt. Ltd.)

- Farmley (Hyfun Foods Pvt. Ltd.)

- True Elements (Wholsum Foods Pvt. Ltd.)

- Wingreens Farms Pvt. Ltd.

- Bagrry’s India Limited

- Happilo International Pvt. Ltd.

- Guiltfree Industries Ltd. (Too Yumm! / RPG Group)

- Other Prominent Players

- ITC Limited (Sunfeast, Yoga Bar)

Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India healthy snacks market and what is its growth forecast?

Ans: The India healthy snacks market is projected to grow from USD 3.42 billion in 2025 to USD 8.95 billion by 2032, at a CAGR of 14.7%, supported by rising health awareness, millet adoption, and quick commerce expansion.

2. Which segments are driving demand in the India healthy snacks market?

Ans: Makhana, roasted chickpeas, multigrain biscuits, baked chips, and dry fruits lead the India healthy snacks market by volume, while protein bars, millet-based snacks, and functional fortified snacks are emerging as the fastest-growing premium categories.

3. What are the key drivers of growth in the India healthy snacks market?

Ans: Key India healthy snacks market drivers include rising health awareness, diabetes-obesity concerns, government-led millet promotion, FSSAI Eat Right initiative, premium D2C brand growth, and rapid expansion of quick commerce and modern trade channels.

4. Which regions are driving growth in the India healthy snacks market?

Ans: Maharashtra, Karnataka, Delhi NCR, Tamil Nadu, Telangana, Gujarat, and Uttar Pradesh lead India healthy snacks market demand, while tier-2 cities including Pune, Jaipur, Lucknow, Indore, and Coimbatore are emerging fast.

5. What are the latest trends in the India healthy snacks market?

Ans: Latest India healthy snacks market trends include millet-based and high-protein snacks, functional immunity and gut-health products, D2C brand growth, subscription-based snack boxes, quick commerce expansion, and FSSAI Front-of-Pack Labelling adoption.

Frequently Asked Questions

1. How large is the India healthy snacks market and what is its growth forecast?

Ans: The India healthy snacks market is projected to grow from USD 3.42 billion in 2025 to USD 8.95 billion by 2032, at a CAGR of 14.7%, supported by rising health awareness, millet adoption, and quick commerce expansion.

2. Which segments are driving demand in the India healthy snacks market?

Ans: Makhana, roasted chickpeas, multigrain biscuits, baked chips, and dry fruits lead the India healthy snacks market by volume, while protein bars, millet-based snacks, and functional fortified snacks are emerging as the fastest-growing premium categories.

3. What are the key drivers of growth in the India healthy snacks market?

Ans: Key India healthy snacks market drivers include rising health awareness, diabetes-obesity concerns, government-led millet promotion, FSSAI Eat Right initiative, premium D2C brand growth, and rapid expansion of quick commerce and modern trade channels.

4. Which regions are driving growth in the India healthy snacks market?

Ans: Maharashtra, Karnataka, Delhi NCR, Tamil Nadu, Telangana, Gujarat, and Uttar Pradesh lead India healthy snacks market demand, while tier-2 cities including Pune, Jaipur, Lucknow, Indore, and Coimbatore are emerging fast.

5. What are the latest trends in the India healthy snacks market?

Ans: Latest India healthy snacks market trends include millet-based and high-protein snacks, functional immunity and gut-health products, D2C brand growth, subscription-based snack boxes, quick commerce expansion, and FSSAI Front-of-Pack Labelling adoption.