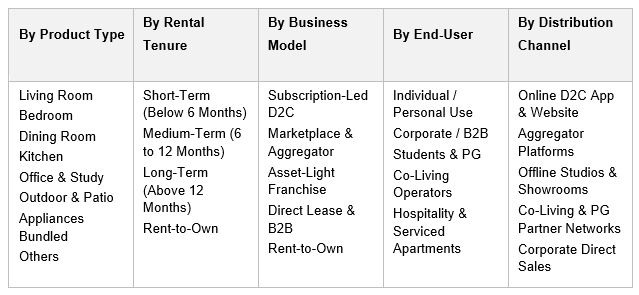

India Furniture Rental Market, By Product Type (Living Room Furniture, Bedroom Furniture, Dining Room Furniture, Kitchen Furniture, Office & Study Furniture, Outdoor & Patio Furniture, Appliances & Bundled Goods, Others); By Rental Tenure (Short-Term Below 6 Months, Medium-Term 6 to 12 Months, Long-Term Above 12 Months, Rent-to-Own); By Material (Solid Wood, Engineered Wood, Metal, Plastic & Composite, Upholstery & Fabric); By Pricing Tier (Premium, Mid-Range, Economy); By Business Model (Subscription-Led D2C, Marketplace & Aggregator, Asset-Light Franchise, Direct Lease & B2B, Rent-to-Own); By End-User (Individual / Personal Use, Corporate / B2B, Students & PG, Co-Living Operators, Hospitality & Serviced Apartments); By Distribution Channel (Online D2C App & Website, Aggregator Platforms, Offline Studios & Showrooms, Co-Living & PG Partner Networks, Corporate Direct Sales); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Furniture Rental Market: Subscription-Led D2C, Co-Living Demand, and Hybrid Work Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

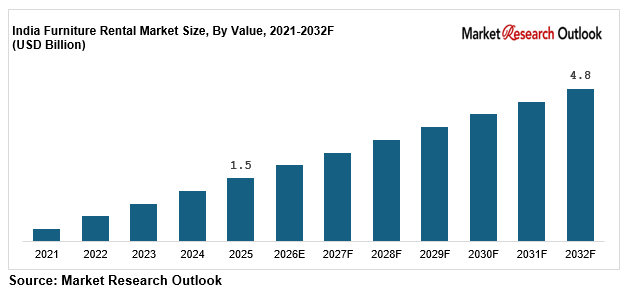

| Market Size (2025) | USD 1.5 Billion |

| CAGR (2026-2032) | 18.0% |

| Leading Segment | Living Room Furniture Rental (Subscription) |

| Fastest Growing Segment | Home Office & Work-from-Home Furniture Rental |

| Market Size (2032) | USD 4.8 Billion |

Source: Market Research Outlook

Market Overview: India Furniture Rental Market

The India furniture rental market size is witnessing rapid expansion, driven by rapid urban migration of young professionals and millennials, accelerating adoption of co-living, paying-guest, and student housing formats, rising preference for subscription-led consumption over upfront ownership, expanding corporate and B2B furniture rental demand from offices, hotels, and serviced apartments, and growing investments by domestic and global consumer-tech majors in India-specific furniture rental platforms, refurbishment hubs, and reverse-logistics capability. Valued at USD 1.5 Billion in 2025 and projected to reach USD 4.8 Billion by 2032, growing at a CAGR of 18.0%, the Indian furniture rental industry is being fuelled by strong demand for living-room and bedroom furniture rental, accelerating uptake of home-office and work-from-home furniture, and growing institutional adoption across co-living operators, PG aggregators, hotels, and serviced-apartment chains. Living-room and bedroom furniture lead consumption, while home-office and work-from-home furniture is emerging as the fastest growing category. Tightening GST, e-invoicing, and state-level commercial-leasing compliance, growing ESG and circular-economy commitments by Indian corporates, and the structural premiumisation of subscription tiers are reshaping the supply landscape. As domestic majors including Furlenco (House of Kieraya, Sheela Foam group), Rentomojo, CityFurnish, RentSher, Cherrypick India, Pepperfry Rentals, Urban Ladder Rentals, Guarented, GrabOnRent, and HouseProud expand integrated rental platforms, refurbishment infrastructure, and reverse-logistics capability, the India furniture rental market is evolving into a consumer-led, subscription-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Furniture Rental Market

- The India furniture rental market size is projected to grow from USD 1.5 Billion in 2025 to USD 4.8 Billion by 2032, registering a strong CAGR of 18.0%, driven by rapid urban migration, co-living expansion, hybrid-work adoption, and the structural shift toward subscription-led consumption.

- Living-room and bedroom furniture together dominate the Indian furniture rental industry, accounting for over 58% to 62% of total revenue in 2025, supported by anchor demand from urban tenants and co-living operators across Bengaluru, Mumbai, Delhi NCR, Hyderabad, Pune, and Chennai.

- Home-office and work-from-home furniture is the fastest growing rental category, expected to expand at 22% to 26% annually as hybrid work scales and Indian IT and services employers offer remote-employee allowances of INR 5,000 to 15,000 per month for furniture and equipment.

- Co-living and PG operators are anchoring institutional demand, with organised co-living bed capacity expected to exceed 6.5 lakh beds by 2026; multi-thousand-bed bulk rental contracts between operators and branded furniture rental partners are expanding the institutional opportunity.

- Rising investments by domestic furniture rental majors such as Furlenco (Sheela Foam group), Rentomojo, CityFurnish, RentSher, Cherrypick India, Pepperfry Rentals, Urban Ladder Rentals, Guarented, GrabOnRent, and HouseProud in subscription platforms, refurbishment hubs, and reverse-logistics infrastructure are supporting the India furniture rental market forecast 2032.

Key Market Drivers: India Furniture Rental Market

Rapid Urban Migration of Young Professionals and Millennials Driving Demand for Flexible Furniture Rental

Growth in the India furniture rental market is being driven by rapid urban migration of young professionals, millennials, and Gen-Z workers into Tier I metros such as Bengaluru, Mumbai, Delhi NCR, Hyderabad, Pune, and Chennai. India’s urban population is projected to cross 600 million by 2031, with over 14 million Indians changing cities annually for work, education, or family relocation, according to the World Bank and the Ministry of Housing and Urban Affairs. Indian millennials and Gen-Z workers, who form the largest single demographic cohort in metro India, increasingly prefer subscription-led furniture rental over capital-intensive ownership, with average rental tenures of 12 to 24 months and monthly rentals starting at INR 1,500 to 2,500 for a basic bedroom package. The Indian furniture rental segment is also benefiting from rapid hybrid-work adoption, with over 38% of Indian metro workers now requiring home-office furniture, including ergonomic chairs, study tables, and bookcases. These trends are creating strong, multi-year structural pull-through demand across the India furniture rental market through 2032.

Source: Market Research Outlook

Rise of Co-Living, Paying-Guest, and Student Housing Formats Driving Institutional Furniture Rental Demand

A clear shift toward organised co-living, paying-guest (PG), and student housing in Indian cities is a major catalyst for the India furniture rental market. Organised co-living bed capacity in India is estimated to exceed 6.5 lakh beds by 2026, growing at over 25% annually, led by operators such as Stanza Living, Colive, Zolo Stays, Your-Space, OYO Life, Settl., and HelloWorld. Student housing demand alone, anchored in Bengaluru, Hyderabad, Pune, Delhi NCR, Indore, and Coimbatore, is projected to reach an addressable opportunity of 1.5 million paid beds by 2030, with each bed requiring an estimated INR 18,000 to 25,000 of furniture and appliances on average. Co-living and PG operators are increasingly partnering with furniture rental players to convert capital expenditure into operating expenditure, accelerating multi-year B2B contracts of 24 to 36 months. The Indian furniture rental industry is also winning serviced-apartment, hotel, and corporate-transferee mandates, structurally widening institutional demand.

Source: Market Research Outlook

Affordability, Hassle-Free Relocation, and Subscription Economy Fuelling Furniture Rental Growth in India

Rapid adoption of subscription-led consumption, EMI-style monthly payments, and asset-light living among Indian urban consumers is a major driver of the India furniture rental market. The total upfront cost of furnishing a 1 BHK home in metro India typically ranges from INR 1.5 lakh to 3.5 lakh, while comparable subscription furniture rental packages start at INR 2,499 to 4,999 per month, with free delivery, installation, swap, and return options. Furniture rental players such as Furlenco, Rentomojo, CityFurnish, RentSher, Cherrypick India, Pepperfry Rentals, Guarented, and GrabOnRent are scaling subscription-led D2C apps and websites with seamless KYC, online payments, and 48-hour delivery across 25+ Indian cities. Quick-relocation use cases, frequent inter-city job changes, sabbatical living, and short-term project-based work are reinforcing demand for flexible rental tenures of 3, 6, 12, and 24 months. These dynamics are structurally expanding the India furniture rental market across both individual and corporate end-user categories.

Key Market Challenges: India Furniture Rental Market

Low Consumer Awareness of Organised Furniture Rental Beyond Tier I Metros Limiting Near-Term Penetration

The India furniture rental market remains heavily concentrated in Tier I metros, with over 78% of organised rental revenue in 2025 generated across Bengaluru, Delhi NCR, Mumbai, Hyderabad, Pune, and Chennai. Awareness of branded furniture rental subscriptions remains low in Tier II and Tier III Indian cities, where ownership-led consumption, hand-me-down furniture, and unorganised local rental shops continue to dominate household furnishing decisions. Cultural preference for owning long-life household assets, particularly in joint-family setups across smaller Indian cities, also slows down trial of subscription-led furniture rental. Marketing-to-acquisition costs for digital-first furniture rental brands in Tier I metros remain high, with average customer-acquisition cost in the range of INR 4,500 to 7,500 per subscriber, while equivalent acquisition economics in non-metro India are still unproven. Expanding the Indian furniture rental industry beyond top metros will require targeted awareness building, regional pricing innovation, and partnerships with local distribution, real estate, and PG ecosystems.

High Logistics, Refurbishment, and Reverse-Logistics Costs Squeezing Unit Economics

The India furniture rental market is exposed to significant logistics, refurbishment, and reverse-logistics cost pressures. Last-mile delivery, installation, swap, pickup, and warehousing together account for an estimated 22% to 28% of furniture rental revenue, materially affecting unit economics. Refurbishment of returned furniture typically involves deep cleaning, polish, upholstery repair, and minor part replacement, adding INR 600 to 1,500 of cost per asset per cycle for Indian furniture rental players. Warehousing and storage costs in Indian metros remain elevated, with industrial real estate rents in Bengaluru and Mumbai growing by over 9% to 12% annually. Damage, theft, and disputed-condition write-offs at end of rental tenure further pressure margins, with damage-related write-offs ranging between 4% and 8% of inventory value per year. Cost engineering, route optimisation, third-party logistics partnerships, and centralised refurbishment hubs are emerging as critical responses for the Indian furniture rental industry.

Long Payback Cycles and Capital-Intensive Inventory Limiting Scalability for Furniture Rental Players

Scalability in the India furniture rental market is constrained by long payback cycles on capital-intensive inventory. A typical furniture rental SKU in India takes 24 to 36 months of utilisation to recover its acquisition cost, with utilisation rates of 70% to 85% needed for healthy returns. Building diversified inventory across living room, bedroom, dining, kitchen, office, and outdoor categories requires substantial upfront capital, with leading furniture rental players such as Furlenco, Rentomojo, and CityFurnish having collectively raised over USD 200 million in equity funding to date. Inventory financing remains challenging, given limited bank appetite for asset-backed rental inventory loans in India, and the relatively young vintage of organised furniture rental as a category. Demand seasonality across Indian academic and corporate cycles also creates utilisation volatility, with spikes around July to September and dips between January and March. These dynamics make capital allocation, inventory mix, and utilisation discipline critical levers in the India furniture rental market.

Key Market Trends: India Furniture Rental Market

Surge in Subscription-Led Rental Models, EMI-Style Monthly Plans, and Rent-to-Own Programs

The India furniture rental market is undergoing a clear shift toward subscription-led rental, EMI-style monthly plans, and rent-to-own programs, with subscription-led furniture rental expected to account for over 70% of organised rental revenue by 2030. Indian D2C furniture rental brands such as Furlenco, Rentomojo, CityFurnish, RentSher, Cherrypick India, Guarented, and GrabOnRent have built propositions around flexible 3, 6, 12, 24, and 36-month subscription tenures, with free swap, free relocation, and free maintenance options bundled into monthly plans. Rent-to-own programs, which convert a portion of monthly rental into ownership equity at the end of the tenure, are gaining traction with first-time Indian urban migrants, paying-guest tenants, and young couples. Premium tiered subscriptions covering designer furniture, smart-home appliances, work-from-home setups, and kids’ furniture are also scaling, reinforcing the structural premiumisation of the Indian furniture rental industry through 2032.

Asset-Light, Marketplace, and Franchise Models Scaling India Furniture Rental Market Footprint

A clear move toward asset-light marketplace, franchise, and partner-network models is reshaping the India furniture rental market. Aggregator platforms now match independent furniture rental operators, refurbishers, and warehousing partners with end-users, reducing the capital intensity of network expansion. Franchise-led furniture rental, where regional partners deploy inventory under a national brand, is enabling rapid expansion into Tier II and Tier III Indian cities such as Jaipur, Lucknow, Indore, Coimbatore, Bhubaneswar, Visakhapatnam, Surat, and Kochi. Strategic partnerships with co-living operators, PG aggregators, hotel chains, and serviced-apartment brands are converting rental into multi-year B2B contracts. Co-living players such as Stanza Living, Colive, Zolo Stays, OYO Life, Settl., and Your-Space have anchored multi-thousand-bed furniture rental deals with branded furniture rental partners, reinforcing institutional scaling of the segment.

Curated, Designer, and Category-Specialised Rental Gaining Traction in India

A wave of curated, designer, and category-specialised rental innovation is reshaping the India furniture rental market. Specialised rental categories including work-from-home furniture, baby and kids’ furniture, fitness equipment, smart-home appliances, designer outdoor furniture, and ergonomic office chairs are scaling fast. Furniture rental players are tying up with Indian designers and home brands to launch curated, design-led rental capsules. Pet-friendly upholstery, modular furniture for compact 1 BHK apartments, and bundled appliances-plus-furniture packages are also gaining traction. Ingredient-led storytelling around solid-wood sourcing, eco-friendly polish, low-VOC paints, and FSC-certified engineered wood is driving consumer education across the Indian furniture rental industry. These developments are reinforcing the India furniture rental market forecast 2032 across both residential and commercial end-user categories.

Segmental Insights: India Furniture Rental Market

By Product Type: Living Room and Bedroom Furniture Lead, Home Office Grows Fastest

Living-room furniture (sofa, coffee table, TV unit, recliner) and bedroom furniture (bed, mattress, wardrobe, bedside table) together account for an estimated 58% to 62% of total revenue in the India furniture rental market in 2025, supported by anchor demand from urban tenants and co-living operators. Dining-room furniture contributes another 8% to 10%, while kitchen and storage units add 4% to 6%. Home-office and study furniture, including ergonomic chairs, study tables, bookcases, and standing desks, is the fastest growing furniture rental product category, expanding at 22% to 26% annually, driven by hybrid-work adoption and remote-employee allowances of INR 5,000 to 15,000 per month from Indian IT and services employers. Outdoor and patio furniture rental is a niche but growing category in apartments, hotels, and serviced apartments. Appliances bundled with furniture rental, including refrigerator, washing machine, microwave, and smart TV, are scaling rapidly across Indian metros.

By Rental Tenure: Medium-Term and Long-Term Rentals Anchor Furniture Rental Demand

Medium-term rental tenures of 6 to 12 months and long-term tenures of 12 to 36 months together represent over 68% of total subscriptions in the India furniture rental market in 2025, driven by Indian working professionals, young couples, and inter-city transferees who typically rent furniture for the duration of an employment contract. Short-term rentals below 6 months contribute another 18% to 22% of subscriptions, anchored in students, project-based consultants, and short-term corporate deputations. Rent-to-own packages, where a portion of monthly rental converts to ownership equity, are emerging as a high-growth tenure, expanding at over 24% annually as Indian urban consumers seek hybrid models that combine flexibility with eventual ownership. Average monthly furniture rental subscription value in India ranges from INR 1,500 for basic bedroom packages to INR 12,000 for premium full-home bundles, with premium tiers growing fastest in the Indian furniture rental industry.

By End-User and Distribution Channel: D2C Apps and Co-Living Tie-Ups Outpace Offline Retail

Individual and personal-use customers account for an estimated 55% to 58% of total revenue in the India furniture rental market, supported by young Indian professionals, students, and inter-city migrants. Corporate and B2B customers, including IT and services employers, hotels, co-working operators, and serviced-apartment chains, contribute another 22% to 25% of revenue, with multi-year leasing contracts of 24 to 36 months. Co-living and PG operators contribute 14% to 17%, anchored by multi-thousand-bed bulk furniture rental deals. Distribution-wise, online D2C apps and websites lead with over 55% to 60% share of furniture rental subscriptions, followed by aggregator platforms at 18% to 22%, offline studios and showrooms at 8% to 10%, and direct corporate sales contracts at 12% to 14%. Co-living and PG partner channels are the fastest-growing distribution route for the Indian furniture rental industry, expanding at over 30% annually.

Regional Insights: India Furniture Rental Market

Regional analysis of the India furniture rental market shows that South India and West India collectively account for approximately 56% to 60% of total subscriptions, driven by Bengaluru, Hyderabad, Chennai, Pune, and Mumbai, supported by large IT and services employer concentrations, dense co-living and student-housing inventory, and higher per-capita disposable income. North India contributes around 25% to 28% of demand, led by Delhi NCR (Gurugram, Noida, Greater Noida), Chandigarh, and Jaipur, supported by inter-state migration, corporate transferee mandates, and growing co-living deployment. East and Central India together account for 12% to 17% of demand, led by Kolkata, Bhubaneswar, Indore, Lucknow, Bhopal, and Patna, where furniture rental is scaling through asset-light franchise and aggregator models. Tier II and Tier III cities including Coimbatore, Mysuru, Visakhapatnam, Surat, Ahmedabad, Kochi, Vadodara, Nagpur, Vijayawada, Madurai, and Mangaluru are emerging as the next growth frontier, supported by IT-services satellite hubs and university clusters. In 2025, Furlenco, Rentomojo, CityFurnish, RentSher, Cherrypick India, Guarented, GrabOnRent, and Pepperfry Rentals expanded regional distribution, reverse-logistics, and refurbishment infrastructure across Indian states, reinforcing regional supply hubs and supporting closer execution of consumer and corporate furniture rental orders across the country.

Recent Developments: India Furniture Rental Market

- The India furniture rental market witnessed strong momentum across funding, consolidation, and digital-first expansion during 2024 and 2025. Sheela Foam, the parent of Sleepwell mattresses, completed the acquisition of a majority stake in Furlenco’s parent House of Kieraya, strengthening Furlenco’s furniture rental, refurbishment, and mattress capabilities and structurally consolidating one of India’s largest organised furniture rental platforms. Rentomojo, CityFurnish, and RentSher expanded their digital-first furniture rental subscription portfolios, deepened metro coverage, and launched home-office and rent-to-own programs aligned to hybrid-work demand.

- Indian furniture rental majors have deepened B2B and institutional pipelines. Co-living operators including Stanza Living, Colive, Zolo Stays, Your-Space, OYO Life, Settl., and HelloWorld scaled bulk furniture rental contracts with branded rental partners, anchoring multi-thousand-bed institutional deployments. Corporate-transferee and serviced-apartment furniture rental contracts also expanded across Bengaluru, Hyderabad, Pune, and Delhi NCR, while hotel and budget-hospitality operators began piloting branded furniture rental for select properties in 2025.

- Digital-first and asset-light momentum has gained strong traction in the Indian furniture rental industry. Aggregator platforms, marketplace listings, and franchise-led expansion are scaling rental footprint into Tier II and Tier III Indian cities such as Jaipur, Lucknow, Indore, Coimbatore, Surat, Vadodara, Kochi, Bhubaneswar, Visakhapatnam, Nagpur, and Mangaluru. Pepperfry Rentals, Urban Ladder, Guarented, GrabOnRent, and HouseProud expanded subscription-led furniture rental, while smaller regional players continued to scale rent-to-own and category-specialised rental, reinforcing the India furniture rental market forecast 2032 across the entire value chain.

Key Market Players: India Furniture Rental Market

- Furlenco (House of Kieraya Furnishing Solutions Pvt. Ltd. / Sheela Foam Group)

- Rentomojo (Edunetwork Pvt. Ltd.)

- CityFurnish (Bedotchi Internet Pvt. Ltd.)

- RentSher (RentSher Online Services Pvt. Ltd.)

- Cherrypick India (Cherrypick Lifestyle Pvt. Ltd.)

- The Furniture Library

- Pepperfry Rentals (Trendsutra Platform Services Pvt. Ltd.)

- Urban Ladder Rentals (Urban Ladder Home Decor Solutions Pvt. Ltd.)

- Guarented

- GrabOnRent

- HouseProud Lifestyle Pvt. Ltd.

- Voylla Home Furnishings

- Geekay Furniture Rentals

Report Scope

In this report, the India Furniture Rental Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Living Room Furniture (Sofa, Coffee Table, TV Unit, Recliner)

- Bedroom Furniture (Bed, Mattress, Wardrobe, Bedside Table)

- Dining Room Furniture (Dining Table & Chairs, Bar Stools)

- Kitchen Furniture (Kitchen Cabinets, Storage Units)

- Office & Study Furniture (Ergonomic Chair, Study Table, Bookcase, Standing Desk)

- Outdoor & Patio Furniture

- Appliances & Bundled Goods (Refrigerator, Washing Machine, Smart TV, Microwave)

- Others

- By Rental Tenure

- Short-Term (Below 6 Months)

- Medium-Term (6 to 12 Months)

- Long-Term (Above 12 Months)

- Rent-to-Own

- By Material

- Solid Wood

- Engineered Wood

- Metal

- Plastic & Composite

- Upholstery & Fabric

- By Pricing Tier

- Premium

- Mid-Range

- Economy

- By Business Model

- Subscription-Led D2C

- Marketplace & Aggregator

- Asset-Light Franchise

- Direct Lease & B2B

- Rent-to-Own

- By End-User

- Individual / Personal Use

- Corporate / B2B

- Students & PG

- Co-Living Operators

- Hospitality & Serviced Apartments

- By Distribution Channel

- Online D2C App & Website

- Aggregator Platforms

- Offline Studios & Showrooms

- Co-Living & PG Partner Networks

- Corporate Direct Sales

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the Indian furniture rental industry, including business overview, rental product portfolio (living-room, bedroom, dining, kitchen, office, outdoor, appliances), strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional furniture rental players (up to five companies), including emerging Indian D2C rental brands, asset-light franchise operators, co-living-aligned rental specialists, or niche state-level rental aggregators.

The India Furniture Rental Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Rental Tenure

- By Material

- By Pricing Tier

- By Business Model

- By End-User

- By Distribution Channel

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Furniture Rental Market

- India Furniture Rental Market Insights

- Market Dynamics

- Growth Drivers

- Rapid urban migration of young professionals and millennials driving demand for flexible furniture rental.

- Rise of co-living, paying-guest, and student housing formats creating institutional furniture rental demand.

- Affordability, hassle-free relocation, and subscription-economy adoption fuelling furniture rental growth in India.

- Restraints

- Low consumer awareness of organised furniture rental beyond Tier I metros limiting near-term penetration.

- High logistics, refurbishment, and reverse-logistics costs squeezing unit economics for rental operators.

- Long payback cycles and capital-intensive inventory limiting scalability for furniture rental players.

- Opportunities

- Corporate B2B furniture rental opportunity across offices, co-working hubs, hotels, and serviced apartments in India.

- Tier II and Tier III city expansion through digital channels and asset-light franchise furniture rental models.

- Sustainability and circular-economy positioning unlocking ESG-aligned consumer and corporate cohorts.

- Challenges

- Damage, depreciation, and asset write-offs across multi-tenant rental cycles affecting furniture rental returns.

- Fragmented unorganised resale and local rental competition pressuring branded furniture rental pricing.

- GST, e-invoicing, and state-level commercial-leasing compliance creating regulatory complexity for furniture rental.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (solid wood, engineered wood, MDF, plywood, metal, upholstery fabric, polyurethane foam)

- Furniture Manufacturers & OEMs (modular furniture, designer furniture, contract furniture)

- Furniture Rental Operators (subscription-led D2C, marketplace, asset-light franchise)

- Quality Control, R&D & Refurbishment Hubs (cleaning, polish, upholstery repair, certification)

- Distributors, Aggregator Platforms & D2C Apps (online rental portals, B2B aggregators)

- Co-Living, PG & Hospitality Partner Networks (Stanza Living, Colive, Zolo Stays, OYO Life)

- Corporate & Serviced Apartment Buyers (IT employers, co-working operators, transferee programs)

- Last-Mile Delivery, Installation & Reverse-Logistics Providers

- Insurance, Damage-Cover & Financing Partners (rent-to-own, EMI providers, asset-backed lenders)

- End-Users (Individual / Personal Use, Corporate / B2B, Students & PG, Co-Living, Hospitality)

- India Furniture Rental Market: Regulatory Framework

- India Furniture Rental Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Thousand Active Subscriptions)

- Market Share & Forecast

- By Product Type

- Living Room Furniture (Sofa, Coffee Table, TV Unit, Recliner)

- Bedroom Furniture (Bed, Mattress, Wardrobe, Bedside Table)

- Dining Room Furniture (Dining Table & Chairs, Bar Stools)

- Kitchen Furniture (Kitchen Cabinets, Storage Units)

- Office & Study Furniture (Ergonomic Chair, Study Table, Bookcase, Standing Desk)

- Outdoor & Patio Furniture

- Appliances & Bundled Goods (Refrigerator, Washing Machine, Smart TV, Microwave)

- Others

- By Rental Tenure

- Short-Term (Below 6 Months)

- Medium-Term (6 to 12 Months)

- Long-Term (Above 12 Months)

- Rent-to-Own

- By Material

- Solid Wood

- Engineered Wood

- Metal

- Plastic & Composite

- Upholstery & Fabric

- By Pricing Tier

- Premium

- Mid-Range

- Economy

- By Business Model

- Subscription-Led D2C

- Marketplace & Aggregator

- Asset-Light Franchise

- Direct Lease & B2B

- Rent-to-Own

- By End-User

- Individual / Personal Use

- Corporate / B2B

- Students & PG

- Co-Living Operators

- Hospitality & Serviced Apartments

- By Distribution Channel

- Online D2C App & Website

- Aggregator Platforms

- Offline Studios & Showrooms

- Co-Living & PG Partner Networks

- Corporate Direct Sales

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Furniture Rental Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Furlenco (House of Kieraya Furnishing Solutions Pvt. Ltd. / Sheela Foam Group)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- Rentomojo (Edunetwork Pvt. Ltd.)

- CityFurnish (Bedotchi Internet Pvt. Ltd.)

- RentSher (RentSher Online Services Pvt. Ltd.)

- Cherrypick India (Cherrypick Lifestyle Pvt. Ltd.)

- The Furniture Library

- Pepperfry Rentals (Trendsutra Platform Services Pvt. Ltd.)

- Urban Ladder Rentals (Urban Ladder Home Decor Solutions Pvt. Ltd.)

- Guarented

- GrabOnRent

- HouseProud Lifestyle Pvt. Ltd.

- Voylla Home Furnishings

- Geekay Furniture Rentals

- Other Prominent Players

- Furlenco (House of Kieraya Furnishing Solutions Pvt. Ltd. / Sheela Foam Group)

- Market Size & Forecast, 2021-2032

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India furniture rental market and what is its growth forecast?

Ans: India furniture rental market is projected to grow from USD 1.5 Billion in 2025 to USD 4.8 Billion by 2032, at 18.0% CAGR, driven by urban migration, co-living, hybrid work, and subscription-led D2C adoption.

2. Which segments are driving demand in the India furniture rental market?

Ans: Living-room and bedroom furniture lead with 58% to 62% revenue share, anchored by urban tenants and co-living operators. Home-office and work-from-home furniture grows fastest at 22% to 26% annually, driven by hybrid-work adoption.

3. What are the key drivers of growth in the India furniture rental market?

Ans: Key drivers include rapid urban migration of young professionals and millennials, rise of co-living, PG, and student housing formats, affordability and hassle-free relocation, subscription-economy adoption, and growing corporate B2B furniture rental demand across Indian metros.

4. Which regions are driving growth in the India furniture rental market?

Ans: South and West India lead with 56% to 60% of subscriptions, anchored by Bengaluru, Hyderabad, Chennai, Pune, and Mumbai. North India contributes 25% to 28%, led by Delhi NCR, Chandigarh, and Jaipur, supported by inter-state migration.

5. What are the latest trends in the India furniture rental market?

Ans: Latest trends include subscription-led rental, EMI-style plans, and rent-to-own programs, asset-light marketplace and franchise expansion, curated designer and category-specialised rental, hybrid-work home-office furniture, and growing co-living-led institutional contracts.

Frequently Asked Questions

1. How large is the India furniture rental market and what is its growth forecast?

Ans: India furniture rental market is projected to grow from USD 1.5 Billion in 2025 to USD 4.8 Billion by 2032, at 18.0% CAGR, driven by urban migration, co-living, hybrid work, and subscription-led D2C adoption.

2. Which segments are driving demand in the India furniture rental market?

Ans: Living-room and bedroom furniture lead with 58% to 62% revenue share, anchored by urban tenants and co-living operators. Home-office and work-from-home furniture grows fastest at 22% to 26% annually, driven by hybrid-work adoption.

3. What are the key drivers of growth in the India furniture rental market?

Ans: Key drivers include rapid urban migration of young professionals and millennials, rise of co-living, PG, and student housing formats, affordability and hassle-free relocation, subscription-economy adoption, and growing corporate B2B furniture rental demand across Indian metros.

4. Which regions are driving growth in the India furniture rental market?

Ans: South and West India lead with 56% to 60% of subscriptions, anchored by Bengaluru, Hyderabad, Chennai, Pune, and Mumbai. North India contributes 25% to 28%, led by Delhi NCR, Chandigarh, and Jaipur, supported by inter-state migration.

5. What are the latest trends in the India furniture rental market?

Ans: Latest trends include subscription-led rental, EMI-style plans, and rent-to-own programs, asset-light marketplace and franchise expansion, curated designer and category-specialised rental, hybrid-work home-office furniture, and growing co-living-led institutional contracts.