India Footwear Market, By Product Type (Casual Footwear, Formal Footwear, Sports & Athletic Footwear, Sandals, Flip-Flops & Slippers, Boots & Others); By Material (Leather, Rubber, Plastic & PVC, Textile & Fabric, EVA & Foam, Synthetic, Others); By Price Range (Luxury, Premium, Mid-Range, Mass, Economy); By Distribution Channel (Exclusive Brand Outlets, Multi-Brand Outlets, Supermarkets & Hypermarkets, Online Retail & E-Commerce, Independent & Kirana Retailers, Direct-to-Consumer); By Application (Men, Women, Children, Unisex); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- Jul 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Footwear Market: Urbanization, Athleisure Demand and E-Commerce Expansion Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

| Market Size (2025) | USD 20.7 Billion |

| CAGR (2026-2032) | 10.5% |

| Leading Segment | Non-Athletic Footwear |

| Fastest Growing Segment | Athletic & Athleisure Footwear |

| Market Size (2032) | USD 41.7 Billion |

Source: Market Research Outlook

Market Overview: India Footwear Market

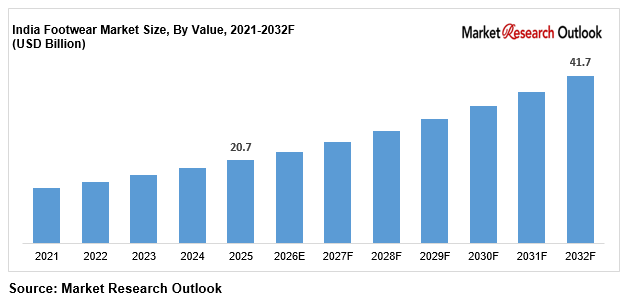

The India footwear market size is witnessing rapid expansion, driven by accelerating urbanization, rising disposable incomes, growing fashion and fitness consciousness, expanding organized retail, the shift toward branded and athletic footwear, and major capacity additions by domestic and global players. Valued at USD 20.7 billion in 2025 and projected to reach USD 41.7 billion by 2032, growing at a CAGR of 10.5%, the India Footwear Market growth is being fuelled by strong demand from young urban consumers, rising premiumization, and the rapid scaling of e-commerce and D2C platforms across metro and Tier-2 cities. Non-athletic footwear leads consumption, while athletic and athleisure footwear is emerging as the fastest growing category. Shifting consumer preferences toward branded, stylish, and performance-driven footwear, growing fitness culture, and rising demand for premium products are reshaping the supply landscape of the India footwear market. As domestic and global majors including Bata, Relaxo, Campus Activewear, Nike, and Adidas expand integrated manufacturing and retail capacity, and specialty players including Metro Brands, Mirza International, and Woodland scale branded pipelines, the market is evolving into a consumer-led, innovation-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Footwear Market

- The India footwear market size is projected to grow from USD 20.7 billion in 2025 to USD 41.7 billion by 2032, registering a strong CAGR of 10.5%, driven by accelerated athletic and athleisure adoption, rising premiumization, and the structural shift toward branded footwear across urban India.

- Non-athletic footwear dominates the India footwear market, accounting for 68% of total value in 2025, driven by deeply entrenched demand for casual, formal, and traditional styles, the deep presence of brands such as Bata, Relaxo, and Metro Brands, and rising urban demand across organized retail and e-commerce channels.

- Athletic and athleisure footwear are emerging as the fastest growing segments in the India footwear market, expected to grow at 12% annually as fitness culture, sneaker adoption, and hybrid lifestyles reshape purchasing strategies across metro and Tier-2 markets.

- Rapid scaling of organized retail and e-commerce, with 28,000 organized footwear outlets across India by 2025 and projected expansion to 42,000 by 2030, is structurally expanding the market across modern retail, exclusive outlets, and online delivery categories.

- Rising investments by domestic and global majors such as Bata, Relaxo, Campus Activewear, and Nike in manufacturing capacity, D2C channels, and premium variants are strengthening local supply and supporting the market forecast 2032.

Key Market Drivers: India Footwear Market

Rapid Urbanization, Rising Disposable Incomes, and Growing Fashion Consciousness Driving Branded Footwear Demand

Growth in the market is being driven by rapid urbanization, rising disposable incomes, and growing fashion consciousness across metro, Tier-1, and Tier-2 cities. India’s urban population crossed 510 million in 2025, with urbanization rates climbing to 36% and projected to reach 40% by 2030. Per-capita income reached USD 3,200 in 2024, expanding the middle class and accelerating demand for branded and premium footwear. With more than 50% of India’s population under 25 years of age, young consumers are driving strong demand for stylish, branded, and aspirational footwear. India is the second-largest producer and consumer of footwear globally, producing nearly 2.6 billion pairs annually, with per-capita consumption rising to 2.5 pairs per person per year. The premium segment now accounts for 54% of the India footwear market, reflecting rising brand consciousness, higher disposable incomes, and social media influence, creating strong structural pull-through demand across the market.

E-Commerce, D2C, and Quick-Commerce Expansion, Plus Organized Retail Penetration Strengthening Footwear Distribution

The India footwear market is benefiting from rapid e-commerce, D2C, and organized retail expansion. India’s e-commerce industry, valued at USD 125 billion in 2024, is projected to reach USD 345 billion by 2030 at a CAGR of 15%, rapidly expanding digital footwear distribution. Online channels are projected to account for over 30% of footwear sales by 2030, up sharply from current levels, driven by platforms such as Myntra, Ajio, Amazon India, and Flipkart. D2C-first brands including Campus Activewear have scaled rapidly through digital-first models, while quick-commerce platforms are beginning to stock everyday footwear. Domestic manufacturing and retail capacity has scaled rapidly, led by Bata, Relaxo, Campus Activewear, Metro Brands, and Liberty. Expanding exclusive brand outlets, multi-brand retail, and omnichannel networks have further strengthened organized supply, supporting value realisation across the market. Virtual try-on tools, AI-driven recommendations, and digital-first collections are increasingly shaping how young consumers discover and purchase footwear in India.

Athleisure, Sports, and Fitness Trends, Plus a Young Demographic, Driving Athletic Footwear Consumption

Strong athleisure, sports, and fitness trends, combined with a young demographic, are major catalysts for the India footwear market, with the athletic and athleisure segment projected to grow at 12% annually through 2032. Athletic footwear currently accounts for 32% of the India footwear market, growing faster than the non-athletic segment as fitness culture, sneaker adoption, and hybrid work lifestyles reshape consumption. Rising participation in sports, gyms, and outdoor activities, combined with the convergence of athletic and casual styles, is driving strong demand for sneakers, running shoes, and athleisure footwear. Global brands including Nike, Adidas, and Puma, alongside domestic players such as Campus Activewear and Relaxo, have scaled athletic and athleisure pipelines, with the athletic footwear segment representing an estimated USD 6.6 billion addressable opportunity in India. Rising fitness consciousness combined with corporate investment is structurally expanding India footwear market growth across all major categories through 2032.

Key Market Challenges: India Footwear Market

Fragmented, MSME-Dominated Manufacturing, Capacity Stagnation, and Import Dependence

The India footwear market continues to face challenges around fragmented, MSME-dominated manufacturing, capacity stagnation, and import dependence. MSMEs account for over 95% of India’s footwear production units, creating a fragmented and largely unorganized manufacturing base. Domestic production capacity has remained near 2.6 billion pairs annually, and stagnation in organized capacity, combined with a heavy compliance burden, has constrained the industry’s ability to meet rising demand. As demand accelerates, India risks growing reliance on imports, particularly from China, which benefits from an organized industry, ample capacity, and low production costs. India’s continued dependence on fragmented manufacturing and the slow modernization of organized capacity limit predictable branded supply across the market.

Price Sensitivity, Unorganized Competition, and Counterfeits Restricting Branded Penetration

The India footwear market faces structural complexity from price sensitivity, unorganized competition, and counterfeits across different cities. While metros such as Delhi, Mumbai, Bengaluru, Chennai, and Hyderabad have well-established branded retail and organized outlets, smaller cities remain dominated by unorganized and local manufacturers. The unorganized sector still accounts for a large share of the India footwear market, with local players and counterfeits holding significant volumes, creating price competition. Households outside metro cities continue to prioritise price over brand, limiting branded adoption among middle-income and rural consumers. Differential availability of branded outlets, organized retail, and authentic products across states creates operational complexity for players such as Bata, Relaxo, Campus Activewear, and Metro Brands operating pan-India. While premiumization supports growth, unorganized competition remains a near-term challenge for the India footwear market.

Raw Material Volatility, BIS Quality-Compliance Costs, and Margin Pressure

The India footwear market faces practical constraints around raw material volatility, BIS quality-compliance costs, and margin pressure across the value chain. Volatility in leather, rubber, EVA, and synthetic material prices raises overall production costs and squeezes margins. The implementation of mandatory BIS Quality Control Orders for footwear has increased compliance requirements and costs, particularly for smaller MSME manufacturers. Average gross margins for branded footwear in India stand near 38%, reducing the effective profitability of new launches amid rising input and compliance costs. Manufacturing modernization, design and technology investment, and government schemes supporting quality and capacity are emerging as solutions to differentiate, but input volatility and compliance costs remain barriers to widespread branded adoption across the market.

Key Market Trends: India Footwear Market

Rapid Shift to Athleisure, Sneakers, and Casual Hybrid Footwear in India

The India footwear market is undergoing a clear shift toward athleisure, sneakers, and casual hybrid footwear, with these variants expected to capture 40% of new footwear launches by 2027. Sneakers, running shoes, and athleisure styles deliver strong value and appeal to young consumers, while comfort and performance designs serve fitness-focused buyers. Leading brands including Nike, Adidas, Puma, Campus Activewear, and Bata have scaled athletic and athleisure production and design capacity through 2024 and 2025. Premium, sustainable, and performance-driven footwear with modern styling is also gaining traction, particularly in metro cities such as Mumbai and Bengaluru where young consumers are rising, with brands like Metro Brands, Mirza International, and Woodland offering aspirational footwear variants. This product transition is reinforcing the market forecast 2032 across both retail and e-commerce categories.

Growth of E-Commerce, D2C, Omnichannel, and Digital Distribution in the India Footwear Market

A clear shift toward e-commerce, D2C, omnichannel, and digital distribution models is reshaping the India footwear market, particularly in the urban and metro segment. Leading e-commerce platforms including Myntra, Ajio, Amazon India, and Flipkart have built combined operational reach across more than 100 Indian cities, with footwear ranking among the fastest-growing fashion categories ordered online. D2C-first brands such as Campus Activewear have scaled rapidly through digital models, while virtual try-on tools and AI-driven recommendations enhance the online shopping experience. Bata deployed generative AI on its e-commerce platform in 2025 to improve online discovery, reflecting rising digital investment. Digital platforms are also reducing customer acquisition costs and accelerating branded adoption across both retail and online segments of the India footwear market. Online channels are projected to account for over 30% of footwear sales by 2030, with metro buyers increasingly preferring digital-first shopping over in-store purchase.

Premiumization, Sustainability, Domestic Manufacturing, and Quality Standards Across India

A wave of premiumization, sustainability, domestic manufacturing investment, and rising quality standards is reshaping the market supply landscape. Combined India-focused capital and capacity activity in footwear exceeded USD 500 million across 2023 to 2025. Bata launched its global ‘Make Your Way’ campaign to appeal to younger, style-conscious consumers, Campus Activewear expanded athletic capacity, and brands such as Relaxo and Metro Brands deepened premium portfolios. The implementation of mandatory BIS Quality Control Orders, the Focus Product Scheme announced in Budget 2025, and 100% FDI in footwear retail have structurally favoured organized and quality-led supply. Combined with rising manufacturing FDI, export promotion, and D2C expansion, these developments are reinforcing the market forecast 2032 across the entire value chain.

Segmental Insights: India Footwear Market

By Application: Men’s Segment Dominates the India Footwear Market

The men’s application segment dominates the India footwear market, accounting for 52% of total consumption, driven by strong demand across formal, casual, sports, and everyday footwear categories. Men’s footwear captures the majority of branded and athletic purchases, supported by workwear, sports, and lifestyle demand. The women’s segment contributes 30% of demand, driven by rising fashion consciousness, growing workforce participation, and expanding stylish and premium ranges. Children’s footwear accounts for 15%, supported by school, sports, and casual demand, while unisex footwear accounts for 3%, driven by athleisure and sneaker styles. In 2025, leading players including Bata, Relaxo, Campus Activewear, and Metro Brands scaled up men’s and women’s footwear deployment under modern retail and e-commerce expansion, reinforcing segment dominance in the India footwear market.

By Product Type: Non-Athletic Leads While Athletic and Athleisure Grow Fastest

Non-athletic footwear leads the market product landscape, accounting for 68% of total value, driven by deeply entrenched demand for casual, formal, and traditional styles across household and everyday use. Casual and formal footwear, sandals, flip-flops, and slippers capture the majority of non-athletic demand, supported by mass and premium ranges. Athletic and athleisure footwear are the fastest growing categories within the India footwear market, expanding at 12% annually, driven by fitness culture, sneaker adoption, and hybrid lifestyles in metro and premium urban segments. Leather remains the leading material with a 45% share, while rubber, EVA, and synthetic materials support mass and sports categories. Leading manufacturers including Bata, Relaxo, Campus Activewear, Nike, and Adidas have aligned product portfolios to this product mix, driving branded and athletic adoption across the market.

Regional Insights: India Footwear Market

Regional analysis of the market shows that North India and South India collectively account for 60% of total footwear value, driven by Delhi NCR, Punjab, Uttar Pradesh (Agra manufacturing belt), Tamil Nadu, Karnataka, and Telangana, supported by higher disposable incomes, established manufacturing clusters, and strong retail infrastructure. North India alone contributes 35% of demand, led by Delhi NCR, Punjab, Haryana, and Uttar Pradesh, supported by Agra’s manufacturing clusters and strong branded retail adoption. South India contributes 25% of demand, anchored by Tamil Nadu, Karnataka, and Telangana, which also serve as major footwear manufacturing and export hubs. West India adds 22%, anchored by Maharashtra and Gujarat, while East and Central India together account for 18%, supported by West Bengal, Odisha, and Madhya Pradesh, where organized retail adoption is accelerating. In 2025, capacity and distribution operations by Bata and Relaxo across North India, and manufacturing hubs in Tamil Nadu, reinforced regional supply, supporting closer execution of retail and export projects across the market.

Recent Developments: India Footwear Market

- The India footwear market witnessed strong momentum in launches and capacity progress during 2024 and 2025. India produced nearly 2.6 billion pairs of footwear in 2025, retaining its position as the world’s second-largest producer and consumer. E-commerce platforms recorded strong double-digit growth in branded footwear orders, with the athletic and athleisure segment accounting for a rising share of new online purchases. India’s footwear exports contributed a significant share of the country’s USD 4.68 billion leather and footwear exports.

- Domestic and global majors have deepened India-focused capacity and investment. In 2025, Bata launched its ‘Make Your Way’ global campaign and deployed generative AI on its e-commerce platform, Campus Activewear expanded athletic capacity, and Relaxo and Metro Brands deepened premium portfolios. These developments are strengthening domestic supply and supporting the market forecast 2032.

- E-commerce, D2C, and organized retail momentum has gained strong traction in the India footwear market. In 2025, leading players including Bata, Relaxo, Campus Activewear, Nike, and Adidas expanded branded offerings and digital distribution across Myntra, Ajio, and Amazon. Strategic investments in manufacturing and D2C are positioning India as one of the fastest scaling footwear markets globally, strengthening long-term competitive positioning in the market forecast 2032.

Key Market Players: India Footwear Market

- Bata India Ltd.

- Relaxo Footwears Ltd.

- Campus Activewear Ltd.

- Metro Brands Ltd.

- Liberty Shoes Ltd.

- Khadim India Ltd.

- Paragon Polymer Products Pvt. Ltd.

- Mirza International Ltd. (Red Tape)

- Woodland (Aero Club)

- Nike India Pvt. Ltd.

- Adidas India Marketing Pvt. Ltd.

- Puma Sports India Pvt. Ltd.

- Action Footwear Pvt. Ltd.

Report Scope

In this report, the India Footwear Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

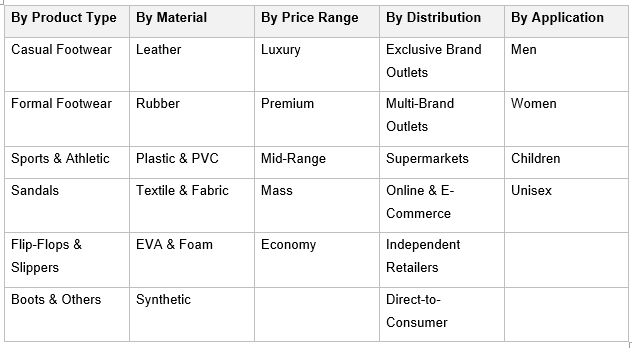

- By Product Type

- Casual Footwear

- Formal Footwear

- Sports & Athletic Footwear

- Sandals

- Flip-Flops & Slippers

- Boots & Others

- By Material

- Leather

- Rubber

- Plastic & PVC

- Textile & Fabric

- EVA & Foam

- Synthetic

- Others

- By Price Range

- Luxury

- Premium

- Mid-Range

- Mass

- Economy

- By Distribution Channel

- Exclusive Brand Outlets

- Multi-Brand Outlets

- Supermarkets & Hypermarkets

- Online Retail & E-Commerce

- Independent & Kirana Retailers

- Direct-to-Consumer

- By Application

- Men

- Women

- Children

- Unisex

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Footwear Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging footwear brands, specialty athletic producers, regional players, or niche direct-to-consumer footwear brands.

The India Footwear Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Material

- By Price Range

- By Distribution Channel

- By Application

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Footwear Market

- India Footwear Market Insights

- Market Dynamics

- Growth Drivers

- Rapid urbanization, rising disposable incomes, and growing fashion consciousness driving branded footwear demand across India.

- E-commerce, D2C, and quick-commerce expansion, plus organized retail penetration strengthening footwear distribution.

- Athleisure, sports, and fitness trends, plus a young demographic, driving athletic footwear consumption.

- Restraints

- Fragmented, MSME-dominated manufacturing, capacity stagnation, and import dependence limiting organized footwear growth.

- Price sensitivity, unorganized competition, and counterfeits restricting branded footwear penetration across smaller cities.

- Raw material volatility, BIS quality-compliance costs, and margin pressure impacting overall footwear profitability.

- Opportunities

- Athletic, athleisure, and premium branded footwear innovation for young urban consumers.

- E-commerce, D2C, quick-commerce, and modern retail expansion unlocking Tier-2 and Tier-3 footwear reach.

- Export growth, manufacturing FDI, and government schemes positioning India as a global footwear hub.

- Challenges

- Intense competition from unorganized players, local manufacturers, and low-cost imports across price-sensitive markets.

- Limited design, technology, and quality infrastructure across smaller footwear clusters.

- Maintaining quality, durability, and consistency at scale across diverse footwear supply chains.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Inputs (leather, rubber, EVA, PVC, textile, soles, adhesives, components)

- Tanneries & Material Suppliers (leather processing, synthetic material makers)

- Component Manufacturers (soles, uppers, laces, insoles, hardware)

- Footwear Manufacturers & MSMEs (Agra, Kanpur, Chennai, Ambur, Ranipet clusters)

- Design, R&D & Product Development (design studios, comfort and technology engineering)

- Quality Control & Testing (BIS standards, durability testing, laboratories)

- Brand Owners & OEM / Contract Manufacturers (Bata, Relaxo, Campus, Nike, Adidas)

- Distribution, Wholesale & Modern Trade (distributors, multi-brand outlets)

- Retail, Exclusive Outlets & E-Commerce (EBOs, Amazon, Flipkart, Myntra, Ajio)

- End-Consumers (men, women, children, athletic, institutional buyers)

- India Footwear Market: Regulatory Framework

- India Footwear Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- By Volume (Billion Pairs)

- Market Share & Forecast

- By Product Type

- Casual Footwear

- Formal Footwear

- Sports & Athletic Footwear

- Sandals

- Flip-Flops & Slippers

- Boots & Others

- By Material

- Leather

- Rubber

- Plastic & PVC

- Textile & Fabric

- EVA & Foam

- Synthetic

- Others

- By Price Range

- Luxury

- Premium

- Mid-Range

- Mass

- Economy

- By Distribution Channel

- Exclusive Brand Outlets

- Multi-Brand Outlets

- Supermarkets & Hypermarkets

- Online Retail & E-Commerce

- Independent & Kirana Retailers

- Direct-to-Consumer

- By Application

- Men

- Women

- Children

- Unisex

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Footwear Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Bata India Ltd.

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

(Same Data Pointers Will Be Provided for The Below Companies)

- Relaxo Footwears Ltd.

- Campus Activewear Ltd.

- Metro Brands Ltd.

- Liberty Shoes Ltd.

- Khadim India Ltd.

- Paragon Polymer Products Pvt. Ltd.

- Mirza International Ltd. (Red Tape)

- Woodland (Aero Club)

- Nike India Pvt. Ltd.

- Adidas India Marketing Pvt. Ltd.

- Puma Sports India Pvt. Ltd.

- Action Footwear Pvt. Ltd.

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the market and what is its growth forecast?

Ans: The India footwear market is valued at USD 20.7 billion in 2025 and is projected to reach USD 41.7 billion by 2032, growing at a CAGR of 10.5%.

2. Which segments are driving demand in the market?

Ans: Non-athletic footwear leads with a 68% value share, while athletic and athleisure footwear are the fastest-growing segments, driven by fitness culture and sneaker adoption.

3. What are the key drivers of growth in the market?

Ans: Key drivers include rapid urbanization, rising incomes, fashion and fitness consciousness, e-commerce and D2C expansion, and a large young demographic.

4. Which regions are driving growth in the market?

Ans: North India and South India lead with around 60% of total value. North India alone contributes 35%, supported by Agra's manufacturing clusters and strong retail infrastructure.

5. What are the latest trends in the India footwear market?

Ans: Latest trends include the shift to athleisure and sneakers, e-commerce and D2C growth, virtual try-on and AI tools, and premium and sustainable footwear.

Frequently Asked Questions

1. How large is the market and what is its growth forecast?

Ans: The India footwear market is valued at USD 20.7 billion in 2025 and is projected to reach USD 41.7 billion by 2032, growing at a CAGR of 10.5%.

2. Which segments are driving demand in the market?

Ans: Non-athletic footwear leads with a 68% value share, while athletic and athleisure footwear are the fastest-growing segments, driven by fitness culture and sneaker adoption.

3. What are the key drivers of growth in the market?

Ans: Key drivers include rapid urbanization, rising incomes, fashion and fitness consciousness, e-commerce and D2C expansion, and a large young demographic.

4. Which regions are driving growth in the market?

Ans: North India and South India lead with around 60% of total value. North India alone contributes 35%, supported by Agra's manufacturing clusters and strong retail infrastructure.

5. What are the latest trends in the India footwear market?

Ans: Latest trends include the shift to athleisure and sneakers, e-commerce and D2C growth, virtual try-on and AI tools, and premium and sustainable footwear.