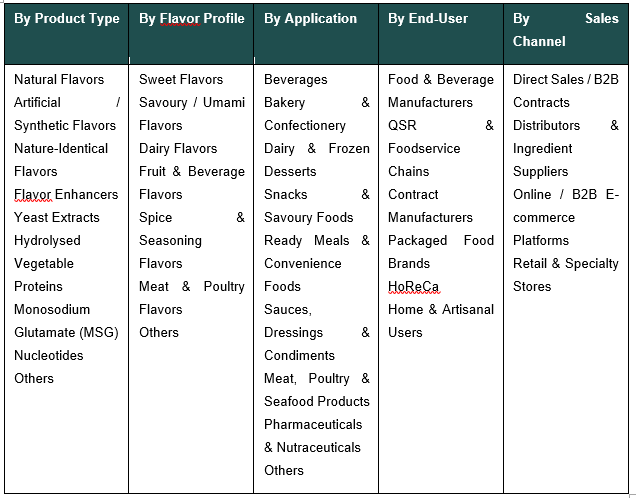

India Food Flavor and Enhancer Market, By Product Type (Natural Flavors, Artificial / Synthetic Flavors, Nature-Identical Flavors, Flavor Enhancers, Yeast Extracts, Hydrolysed Vegetable Proteins, Monosodium Glutamate (MSG), Nucleotides, Others); By Form (Liquid, Powder, Paste, Granular, Emulsion); By Flavor Profile (Sweet Flavors, Savoury / Umami Flavors, Dairy Flavors, Fruit & Beverage Flavors, Spice & Seasoning Flavors, Meat & Poultry Flavors, Others); By Application (Beverages, Bakery & Confectionery, Dairy & Frozen Desserts, Snacks & Savoury Foods, Ready Meals & Convenience Foods, Sauces, Dressings & Condiments, Meat, Poultry & Seafood Products, Pharmaceuticals & Nutraceuticals, Others); By End-User (Food & Beverage Manufacturers, QSR & Foodservice Chains, Contract Manufacturers, Packaged Food Brands, HoReCa, Home & Artisanal Users); By Sales Channel (Direct Sales / B2B Contracts, Distributors & Ingredient Suppliers, Online / B2B E-commerce Platforms, Retail & Specialty Stores); By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Food, Beverage & Nutrition

- Apr 2026

- Pages 170

- Report Format: pdf

- Report Price: $1800 USD

India Food Flavor and Enhancer Market: Natural & Clean-Label Shift Meets Packaged Food Boom, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

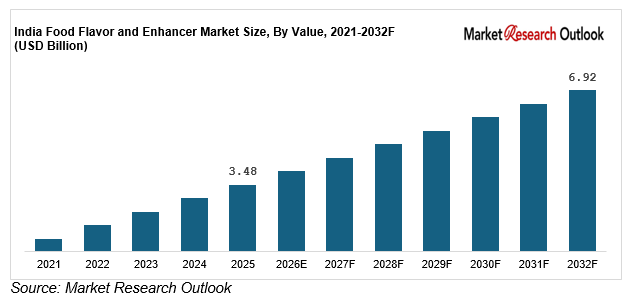

| Market Size (2025) | USD 3.48 Billion |

| CAGR (2026-2032) | 10.3% |

| Leading Segment | Savoury Flavors |

| Fastest Growing Segment | Natural & Clean-Label Flavors |

| Market Size (2032) | USD 6.92 Billion |

Source: Market Research Outlook

Market Overview — India Food Flavor and Enhancer Market

The India food flavor and enhancer market is expanding at a strong pace, supported by rising packaged food consumption, increasing demand for clean-label ingredients, and growing preference for Indian regional taste profiles. Valued at USD 3.48 billion in 2025 and projected to reach USD 6.92 billion by 2032 at a CAGR of 10.3 percent, the market is being driven by strong demand from food and beverage manufacturers, QSR chains, cloud kitchens, and packaged food brands.

Savoury and umami flavor systems continue to dominate consumption, accounting for nearly 40–45 percent of total demand, while natural and clean-label flavors are emerging as the fastest-growing segment, expanding at 14–18 percent annually. Per capita packaged food consumption in India is increasing at 8–10 percent annually, with Tier II and Tier III cities contributing over 50 percent of incremental growth. The rise of D2C food brands, which have grown by over 25 percent annually in the past three years, is further accelerating demand for differentiated flavor systems.

As global and domestic players expand application capabilities and production capacity, the India food flavor and enhancer market is evolving into a more innovation-led, application-focused, and regulation-driven ecosystem with strong long-term growth visibility.

Key Report Takeaways — India Food Flavor and Enhancer Market

- The India food flavor and enhancer market size is projected to grow from USD 3.48 billion in 2025 to USD 6.92 billion by 2032, registering a CAGR of 10.3 percent. This growth is supported by accelerating packaged food consumption (12–14 percent annually), rising clean-label demand, and rapid expansion of QSR chains across Tier I and Tier II cities.

- The rapid expansion of natural and clean-label flavors is reshaping the India food flavor and enhancer market, with this segment growing at 14–18 percent annually—nearly twice the pace of synthetic alternatives. Leading food and beverage manufacturers are actively reformulating products using botanical extracts, fermentation-derived flavors, and yeast-based enhancers.

- Rising demand for Indian regional and ethnic flavor profiles is creating high-growth opportunities for domestic flavor manufacturers. Categories such as ready meals, snacks, and QSR menus are witnessing double-digit growth, driven by demand for authentic biryani, masala, chaat, South Indian, and regional curry-based flavor systems.

- QSR chains, cloud kitchens, and quick commerce platforms are emerging as key demand drivers, collectively influencing over 60–65 percent of incremental flavor consumption in urban markets. These channels are accelerating product innovation cycles and increasing demand for scalable and consistent flavor systems.

- Increasing investments by global flavor houses such as Givaudan, IFF, Symrise, and Firmenich—exceeding USD 250 million across 2024–2025—are strengthening India-specific innovation capabilities. Expansion of application laboratories, sensory testing facilities, and manufacturing capacity is accelerating product development and supporting long-term growth of the India food flavor and enhancer market.

Key Market Drivers — India Food Flavor and Enhancer Market

Rapid Expansion of Packaged Foods, QSR Chains, and Processed Food Consumption Driving Core Flavor Demand

Growth in the India food flavor and enhancer market is closely linked to the expansion of packaged and processed food consumption, which is growing at 12–14 percent annually. Per capita packaged food spending is increasing at 8–10 percent annually, supported by urbanisation, nuclear households, and rising disposable incomes. QSR and cloud kitchen outlets are expanding at 18–22 percent annually, creating consistent demand for savoury, dairy, and seasoning-based flavor systems. The Indian snacks segment is adding approximately 2–3 million new consumers every month, reinforcing sustained demand across applications including snacks, ready meals, and sauces.

Rising Demand for Natural, Clean-Label, and Regional Indian Flavors Driving Premium Reformulation

The India food flavor and enhancer market is witnessing strong momentum in natural and clean-label flavors, growing at 14–18 percent annually, nearly twice the pace of artificial alternatives. Products positioned as “natural” or “no added MSG” command a price premium of 15–25 percent, particularly in urban markets. At the same time, Indian regional and ethnic flavor profiles such as biryani, chaat, sambar, and regional curry bases are witnessing double-digit growth across packaged foods and QSR menus. More than 60 percent of urban consumers actively check ingredient labels, directly influencing reformulation strategies across food manufacturers.

Accelerated Investments by Global Flavor Houses in India-Specific Innovation and Manufacturing Capacity

Global flavor companies including Givaudan, IFF, Symrise, and Firmenich have collectively invested over USD 250 million across India in 2024 and 2025. These investments focus on application laboratories, sensory testing capabilities, and localised production facilities. Domestic companies are also expanding aggressively, with capacity increases of 20–30 percent in natural extracts and oleoresins. Government initiatives such as PLI schemes for food processing are further strengthening downstream demand, reinforcing long-term growth across the India food flavor and enhancer market.

Key Market Challenges — India Food Flavor and Enhancer Market

MSG Stigma and Consumer Skepticism Toward Synthetic Flavor Enhancers Pressuring Legacy Products

Consumer skepticism toward monosodium glutamate (MSG) and synthetic flavor enhancers remains a structural challenge. Over 60 percent of urban consumers actively read ingredient labels, and “no added MSG” has become a common claim across packaged foods. While MSG is scientifically considered safe within regulated limits, perception-driven demand shifts are forcing manufacturers to move toward yeast extracts, hydrolysed vegetable proteins, and nucleotide-based alternatives. This transition is increasing formulation complexity and R&D costs across the India food flavor and enhancer market.

Regulatory Complexity and FSSAI Compliance Around Flavors, Additives, and Labeling Requirements

Regulatory compliance remains a key challenge, with FSSAI continuously updating permissible ingredient lists, usage limits, and labeling requirements. Compliance costs have increased by 8–12 percent for flavor manufacturers due to stricter labeling norms and documentation requirements. Export-focused players face additional certification requirements such as Halal, Kosher, and FSSC 22000, extending approval timelines by 6–12 months. Smaller players face greater pressure due to limited regulatory infrastructure.

Volatile Agri-Raw Material Prices and Supply Chain Fragmentation for Natural Flavor Inputs

The India food flavor and enhancer market is highly sensitive to fluctuations in agri-based raw materials such as spices, herbs, and essential oils. Price volatility of 25–40 percent annually is common for inputs such as cardamom, pepper, and citrus oils, driven by monsoon variability and global demand shifts. Fragmented supply chains and inconsistent quality further complicate procurement. In response, leading companies are investing in contract farming and backward integration, although short-term margin volatility remains a challenge.

Key Market Trends — India Food Flavor and Enhancer Market

Rapid Shift Toward Natural, Clean-Label, and Fermentation-Derived Flavors

The India food flavor and enhancer market is witnessing a strong shift toward natural and clean-label formulations, with natural flavors growing at 14–18 percent annually compared to 7–9 percent for synthetic alternatives. Fermentation-derived flavors, including yeast extracts and microbial aroma compounds, are emerging as premium substitutes for synthetic enhancers. In 2025, leading companies expanded clean-label portfolios, with natural SKUs increasing by over 30 percent across key packaged food categories.

Rising Adoption of Indian Regional and Ethnic Flavor Profiles Across Packaged Foods and QSR Menus

Indian regional flavor systems such as biryani, Punjabi masala, South Indian sambar, and chaat are gaining strong traction. Regional flavor SKUs have increased by 30–40 percent across major food manufacturers over the past two years. QSR chains and cloud kitchens are actively leveraging these flavors to drive differentiation and repeat consumption. This trend is also enabling premium pricing and stronger brand positioning across urban markets.

Expansion of Digital, E-commerce, and Quick Commerce Channels Influencing Flavor Innovation Cycles

Digital channels now influence over 40 percent of packaged food purchase decisions in Tier I cities. Quick commerce platforms are growing at 30–40 percent annually, significantly accelerating product innovation cycles. Brands are launching new flavor variants 20–30 percent faster compared to traditional retail cycles. This shift is enabling rapid experimentation with niche and regional flavor profiles, directly impacting demand patterns in the India food flavor and enhancer market.

Segmental Insights — India Food Flavor and Enhancer Market

By Flavor Profile — Savoury / Umami Flavors Dominate the India Food Flavor and Enhancer Market

The savoury and umami flavor segment dominates the India food flavor and enhancer market, accounting for an estimated 40–45 percent of total market share. This dominance is driven by strong and consistent demand from snacks, instant noodles, seasonings, sauces, and QSR applications, where taste intensity and repeatability are critical.

Umami-rich flavor systems, including yeast extracts, hydrolysed vegetable proteins, and nucleotides, are increasingly preferred as natural alternatives to MSG, particularly in clean-label product formulations. Indian consumer preference for spicy, bold, and layered taste profiles continues to reinforce demand for masala-based and seasoning-driven flavor systems across both packaged foods and foodservice channels.

In 2025, leading Indian snack and seasoning brands such as Haldiram’s, Bikaji, Balaji, and Too Yumm expanded their savoury flavor portfolios with regionally inspired masala variants, further strengthening the segment’s leadership position in the India food flavor and enhancer market.

By Application — Beverages and Snacks Emerge as High-Growth Demand Centers

The application segmentation highlights beverages and snacks as two of the most dynamic segments in the India food flavor and enhancer market. Beverages account for over 25 percent of total demand and are growing at 12–14 percent annually, driven by flavored water, ready-to-drink beverages, and functional drinks. The snacks and savoury foods segment continues to be a major volume contributor, supported by strong urban consumption and frequent product innovation. Ready meals and convenience foods are also expanding rapidly, driven by busy lifestyles and rising demand for packaged meal solutions.

Regional Insights — India Food Flavor and Enhancer Market

Regional analysis of the India food flavor and enhancer market indicates that West and South India together account for approximately 55–60 percent of total demand. This concentration is driven by the presence of major packaged food manufacturing hubs across Maharashtra, Gujarat, Tamil Nadu, and Karnataka, along with a strong QSR footprint in key urban centres such as Mumbai, Pune, Bengaluru, Chennai, and Hyderabad.

North India contributes around 22–25 percent of total demand, led by Delhi NCR, Haryana, and Uttar Pradesh. The region benefits from well-established dairy, bakery, and traditional sweets ecosystems, which continue to generate steady demand for flavour systems across both organised and unorganised segments.

East and Central India together account for 15–20 percent of the market, but represent the fastest-growing regional clusters. Growth in these regions is supported by increasing packaged food penetration, expansion of organised retail, and rising urbanisation across cities such as Kolkata, Bhubaneswar, Raipur, and Indore.

In 2025, capacity expansions by global and domestic players further strengthened regional supply capabilities. Givaudan and IFF expanded operations in Maharashtra, Symrise increased capacity in Tamil Nadu, and Kancor scaled operations in Kerala. These developments are improving supply chain responsiveness, enabling faster flavour development cycles, and supporting closer collaboration with regional food and beverage manufacturers across the India food flavor and enhancer market.

Recent Developments — India Food Flavor and Enhancer Market

- The India food flavor and enhancer market has witnessed strong momentum in natural and clean-label innovation during 2024 and 2025. Global flavor majors including Givaudan, IFF, Symrise, and Firmenich have launched dedicated natural flavor portfolios for the Indian market, targeting key applications such as beverages, dairy, and snacks. Domestic players including Kancor Ingredients, Synthite, and Keva Flavours have expanded their capabilities in natural extracts and oleoresins, while emerging startups are introducing fermentation-derived umami solutions as clean-label alternatives to MSG.

- Strategic capacity expansions and India-focused laboratory investments are reshaping the competitive landscape. In 2025, Givaudan inaugurated a new flavor creation centre in Mumbai, IFF expanded its innovation hub in Bengaluru, and Symrise announced a capacity expansion in Chennai. Domestic companies such as Oriental Aromatics and Kancor have added new manufacturing lines focused on Indian regional flavor systems, including biryani, masala, and South Indian taste profiles, targeting both packaged food manufacturers and QSR chains.

- Partnership activity between flavor houses, QSR chains, and cloud kitchens is accelerating the co-development of India-specific flavor systems. In 2025, leading QSR brands including Rebel Foods, Box8, and Wow! Momo partnered with flavor companies to develop exclusive regional taste variants. At the same time, e-commerce and quick commerce platforms such as Blinkit, Zepto, and Swiggy Instamart expanded their private-label, flavor-led product portfolios, reflecting strong digital-driven demand for rapid flavor innovation across the India food flavor and enhancer market.

Key Market Players — India Food Flavor and Enhancer Market

- Givaudan India Pvt. Ltd.

- International Flavors & Fragrances (IFF) India

- Symrise Pvt. Ltd.

- Firmenich Aromatics (India) Pvt. Ltd.

- Kancor Ingredients Limited

- Synthite Industries Ltd.

- Keva Flavours Pvt. Ltd.

- Oriental Aromatics Ltd.

- S H Kelkar and Company Ltd.

- Döhler India Pvt. Ltd.

- Ajinomoto India Pvt. Ltd.

- Mane Kancor (Kerry Group–associated)

Report Scope

In this report, the India Food Flavor and Enhancer Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Natural Flavors

- Artificial / Synthetic Flavors

- Nature-Identical Flavors

- Flavor Enhancers

- Yeast Extracts

- Hydrolysed Vegetable Proteins

- Monosodium Glutamate (MSG)

- Nucleotides

- Others

- By Form

- Liquid

- Powder

- Paste

- Granular

- Emulsion

- By Flavor Profile

- Sweet Flavors

- Savoury / Umami Flavors

- Dairy Flavors

- Fruit & Beverage Flavors

- Spice & Seasoning Flavors

- Meat & Poultry Flavors

- Others

- By Application

- Beverages

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Savoury Foods

- Ready Meals & Convenience Foods

- Sauces, Dressings & Condiments

- Meat, Poultry & Seafood Products

- Pharmaceuticals & Nutraceuticals

- Others

- By End-User

- Food & Beverage Manufacturers

- QSR & Foodservice Chains

- Contract Manufacturers

- Packaged Food Brands

- HoReCa

- Home & Artisanal Users

- By Sales Channel

- Direct Sales / B2B Contracts

- Distributors & Ingredient Suppliers

- Online / B2B E-commerce Platforms

- Retail & Specialty Stores

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Food Flavor and Enhancer Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic flavor manufacturers, global entrants, or niche segment leaders.

The India Food Flavor and Enhancer Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021–2032

- By Product Type

- By Flavor Profile

- By Application

- By End-User

- By Sales Channel

- By Region

- Analyst Recommendations

- Market Overview, 2021–2032

- Geopolitical Impact on India Food Flavor and Enhancer Market

- India Food Flavor and Enhancer Market Insights

- Market Dynamics

- Growth Drivers

- Rapid expansion of packaged foods, QSR chains, and processed food consumption driving core flavor demand.

- Rising demand for natural, clean-label, and regional Indian flavors driving premium reformulation activity.

- Accelerated investments by global flavor houses in India-specific innovation laboratories and manufacturing capacity.

- Restraints

- MSG stigma and consumer skepticism toward synthetic flavor enhancers pressuring legacy product portfolios.

- Regulatory complexity and FSSAI compliance requirements around flavors, additives, and ingredient labeling.

- Volatile agri-raw material prices and fragmented supply chains for natural flavor inputs constraining margins.

- Opportunities

- Rising export opportunities in ethnic Indian flavor systems to US, UK, Middle East, and ASEAN markets with growing South Asian diaspora.

- Fermentation and biotechnology-derived flavors opening new high-margin categories in natural savoury, dairy, and umami segments.

- Partnerships between flavor houses, QSR chains, and cloud kitchens accelerating co-development of India-specific signature flavor systems.

- Challenges

- Intense price-led competition between domestic flavor companies and global flavor majors compressing margins.

- Shortage of specialist flavorists, sensory scientists, and application technologists limiting scale-up speed.

- High dependence on imported specialty aroma chemicals and encapsulation ingredients creating supply risks.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Dynamics

- Industry Value Chain & Entry Points

- Agri-Raw Material Suppliers (spices, herbs, fruits, aromatic crops)

- Essential Oil, Oleoresin & Aroma Chemical Manufacturers

- Flavor Houses & Formulation Laboratories (natural and synthetic flavor creation)

- Fermentation and Biotech-Derived Flavor Producers

- Quality Control, Sensory Testing & Regulatory Certification (FSSAI, Halal, Kosher, FSSC 22000)

- Packaging and Encapsulation Suppliers

- Distributors and Ingredient Specialty Suppliers

- Food & Beverage Manufacturers, QSR Chains, and Cloud Kitchens

- Retail, HoReCa, E-commerce and Quick Commerce Channels

- End Consumers (household, institutional, and foodservice)

- India Food Flavor and Enhancer Market: Regulatory Framework

- India Food Flavor and Enhancer Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (‘000 Tons)

- Market Share & Forecast

- By Product Type

- Natural Flavors

- Artificial / Synthetic Flavors

- Nature-Identical Flavors

- Flavor Enhancers

- Yeast Extracts

- Hydrolysed Vegetable Proteins

- Monosodium Glutamate (MSG)

- Nucleotides

- Others

- By Form

- Liquid

- Powder

- Paste

- Granular

- Emulsion

- By Flavor Profile

- Sweet Flavors

- Savoury / Umami Flavors

- Dairy Flavors

- Fruit & Beverage Flavors

- Spice & Seasoning Flavors

- Meat & Poultry Flavors

- Others

- By Application

- Beverages

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Savoury Foods

- Ready Meals & Convenience Foods

- Sauces, Dressings & Condiments

- Meat, Poultry & Seafood Products

- Pharmaceuticals & Nutraceuticals

- Others

- By End-User

- Food & Beverage Manufacturers

- QSR & Foodservice Chains

- Contract Manufacturers

- Packaged Food Brands

- HoReCa

- Home & Artisanal Users

- By Sales Channel

- Direct Sales / B2B Contracts

- Distributors & Ingredient Suppliers

- Online / B2B E-commerce Platforms

- Retail & Specialty Stores

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Market Size & Forecast, 2021-2032

- Competitive Landscape

- India Food Flavor and Enhancer Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Givaudan India Pvt. Ltd.

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Givaudan India Pvt. Ltd.

*(Same Data Pointers Will Be Provided for The Below Companies)

- International Flavors & Fragrances (IFF) India

- Symrise Pvt. Ltd.

- Firmenich Aromatics (India) Pvt. Ltd.

- Kancor Ingredients Limited

- Synthite Industries Ltd.

- Keva Flavours Pvt. Ltd.

- Oriental Aromatics Ltd.

- S H Kelkar and Company Ltd.

- Döhler India Pvt. Ltd.

- Ajinomoto India Pvt. Ltd.

- Mane Kancor (Kerry Group–associated)

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India food flavor and enhancer market and what is its growth forecast?

Ans: The India food flavor and enhancer market is valued at USD 3.48 billion in 2025 and is projected to reach USD 6.92 billion by 2032, growing at a CAGR of around 10.3 percent. This growth is supported by rising packaged food consumption, increasing demand for natural and clean-label flavors, and the rapid expansion of QSR chains and cloud kitchens. The report provides detailed market sizing, forecast modelling, and segment-level insights to help businesses identify high-growth opportunities and plan long-term strategies.

2. Which segments are driving demand in the India food flavor and enhancer market?

Ans: Savoury and umami flavors dominate the market, accounting for approximately 40–45 percent of total demand, driven by strong consumption in snacks, instant noodles, seasonings, and QSR applications. The beverages segment is the fastest-growing application, expanding at 12–14 percent annually, supported by demand for flavored water, functional beverages, and ready-to-drink products. The report offers detailed segmentation across product types, forms, flavor profiles, applications, end-users, and sales channels to highlight where growth is accelerating.

3. What are the key drivers of growth in the India food flavor and enhancer market?

Ans: Key growth drivers include the rapid expansion of packaged foods and QSR chains, growing at 12–22 percent annually, rising demand for natural and clean-label ingredients, and increasing investments by global flavor companies such as Givaudan, IFF, Symrise, and Firmenich in India-specific innovation and manufacturing capacity. In addition, demand for Indian regional and ethnic flavor profiles is supporting premium product development across ready meals, snacks, and foodservice channels.

4. Which regions are driving growth in the India food flavor and enhancer market?

Ans: West and South India together account for approximately 55–60 percent of total demand, supported by strong packaged food manufacturing ecosystems and a high concentration of QSR outlets. North India contributes around 22–25 percent, driven by established dairy, bakery, and traditional food segments. East and Central India together account for 15–20 percent and represent emerging high-growth regions due to increasing packaged food penetration and expanding organised retail. The report provides detailed regional insights to support targeted expansion strategies.

5. What are the latest trends in the India food flavor and enhancer market?

Ans: Key trends include the rapid shift toward natural, clean-label, and fermentation-derived flavors, growing at 14–18 percent annually, significantly outpacing synthetic alternatives. Demand for Indian regional and ethnic flavor profiles is rising across ready meals, snacks, and QSR menus. In parallel, digital channels, e-commerce, and quick commerce platforms are reshaping flavor innovation cycles and product distribution. The report provides in-depth analysis of emerging trends, innovation pipelines, and future demand patterns.

Frequently Asked Questions

1. How large is the India food flavor and enhancer market and what is its growth forecast?

Ans: The India food flavor and enhancer market is valued at USD 3.48 billion in 2025 and is projected to reach USD 6.92 billion by 2032, growing at a CAGR of around 10.3 percent. This growth is supported by rising packaged food consumption, increasing demand for natural and clean-label flavors, and the rapid expansion of QSR chains and cloud kitchens. The report provides detailed market sizing, forecast modelling, and segment-level insights to help businesses identify high-growth opportunities and plan long-term strategies.

2. Which segments are driving demand in the India food flavor and enhancer market?

Ans: Savoury and umami flavors dominate the market, accounting for approximately 40–45 percent of total demand, driven by strong consumption in snacks, instant noodles, seasonings, and QSR applications. The beverages segment is the fastest-growing application, expanding at 12–14 percent annually, supported by demand for flavored water, functional beverages, and ready-to-drink products. The report offers detailed segmentation across product types, forms, flavor profiles, applications, end-users, and sales channels to highlight where growth is accelerating.

3. What are the key drivers of growth in the India food flavor and enhancer market?

Ans: Key growth drivers include the rapid expansion of packaged foods and QSR chains, growing at 12–22 percent annually, rising demand for natural and clean-label ingredients, and increasing investments by global flavor companies such as Givaudan, IFF, Symrise, and Firmenich in India-specific innovation and manufacturing capacity. In addition, demand for Indian regional and ethnic flavor profiles is supporting premium product development across ready meals, snacks, and foodservice channels.

4. Which regions are driving growth in the India food flavor and enhancer market?

Ans: West and South India together account for approximately 55–60 percent of total demand, supported by strong packaged food manufacturing ecosystems and a high concentration of QSR outlets. North India contributes around 22–25 percent, driven by established dairy, bakery, and traditional food segments. East and Central India together account for 15–20 percent and represent emerging high-growth regions due to increasing packaged food penetration and expanding organised retail. The report provides detailed regional insights to support targeted expansion strategies.

5. What are the latest trends in the India food flavor and enhancer market?

Ans: Key trends include the rapid shift toward natural, clean-label, and fermentation-derived flavors, growing at 14–18 percent annually, significantly outpacing synthetic alternatives. Demand for Indian regional and ethnic flavor profiles is rising across ready meals, snacks, and QSR menus. In parallel, digital channels, e-commerce, and quick commerce platforms are reshaping flavor innovation cycles and product distribution. The report provides in-depth analysis of emerging trends, innovation pipelines, and future demand patterns.