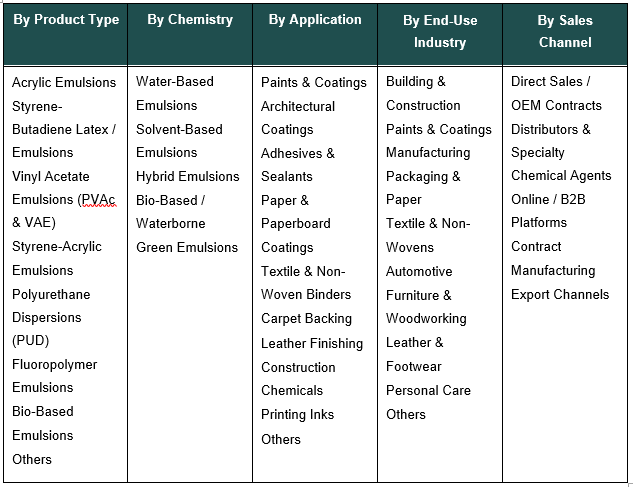

India Emulsion Polymers Market, By Product Type (Acrylic Emulsions, Styrene-Butadiene Latex / Emulsions, Vinyl Acetate Emulsions (PVAc & VAE), Styrene-Acrylic Emulsions, Polyurethane Dispersions (PUD), Fluoropolymer Emulsions, Bio-Based Emulsions, Others); By Chemistry (Water-Based Emulsions, Solvent-Based Emulsions, Hybrid Emulsions, Bio-Based / Waterborne Green Emulsions); By Monomer (Acrylics, Styrene-Butadiene, Vinyl Acetate, Vinyl Versatate, Styrene-Acrylic, Urethane, Others); By Solid Content (Below 30%, 30–50%, 50–60%, Above 60%); By Application (Paints & Coatings, Architectural Coatings, Adhesives & Sealants, Paper & Paperboard Coatings, Textile & Non-Woven Binders, Carpet Backing, Leather Finishing, Construction Chemicals, Printing Inks, Others); By End-Use Industry (Building & Construction, Paints & Coatings Manufacturing, Packaging & Paper, Textile & Non-Wovens, Automotive, Furniture & Woodworking, Leather & Footwear, Personal Care, Others); By Sales Channel (Direct Sales / OEM Contracts, Distributors & Specialty Chemical Agents, Online / B2B Platforms, Contract Manufacturing, Export Channels); By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Chemicals & Advanced Materials

- Apr 2026

- Pages 170

- Report Format: pdf

- Report Price: $1800 USD

India Emulsion Polymers Market: Waterborne Coatings & Construction Chemicals Shift Powers Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

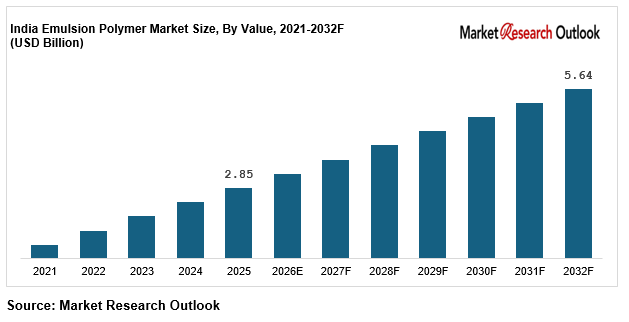

| Market Size (2025) | USD 2.85 Billion |

| CAGR (2026-2032) | 10.2% |

| Leading Segment | Acrylic Emulsion Polymers |

| Fastest Growing Segment | Water-Based & Bio-Based Emulsion Polymers |

| Market Size (2032) | USD 5.64 Billion |

Source: Market Research Outlook

Market Overview — India Emulsion Polymers Market

The India emulsion polymers market is moving through a structural growth phase, supported by strong expansion across paints, construction chemicals, adhesives, and packaging applications. What was once largely tied to decorative coatings is now evolving into a broader, application-driven market with deeper industrial linkages.

The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 5.64 billion by 2032, growing at a CAGR of around 10.2 %. This growth is not just volume-led, but also driven by a gradual shift toward higher-value formulations, particularly water-based and bio-based emulsions.

Acrylic emulsions continue to dominate due to their versatility across paints and coatings, while water-based systems are increasingly becoming the standard across multiple applications. The shift is being reinforced by tightening VOC regulations, green building requirements, and growing awareness around indoor air quality.

At the same time, the supply landscape is becoming more competitive. Global players such as BASF, Dow, Arkema, and Wacker are expanding India-focused capacity, while domestic companies like Pidilite Industries, Jubilant Ingrevia, and GFL are scaling up specialty polymer capabilities. This is gradually transforming India from a demand-heavy market into a more balanced production and innovation hub.

What stands out is that this is no longer a cyclical growth story tied only to construction or paints. It is increasingly a structural shift toward waterborne chemistries, application-specific formulations, and sustainability-led demand, which will continue to shape the market through 2032.

Key Report Takeaways — India Emulsion Polymers Market

- The India emulsion polymers market is expected to grow from USD 2.85 billion in 2025 to around USD 5.64 billion by 2032, at a CAGR of about 10.2 percent. This growth is largely coming from steady expansion in paints and coatings, increasing construction activity, and a clear shift toward water-based chemistries across applications.

- Acrylic emulsion polymers continue to lead the market, accounting for over 40 percent of total demand. Their widespread use in decorative paints, exterior coatings, and pressure-sensitive adhesives makes them the preferred choice, especially as paint manufacturers focus on improving durability and finish quality.

- Water-based and bio-based emulsions are the fastest-growing segment, typically expanding in the range of 13 to 16 percent annually. This is being driven by stricter VOC norms and growing adoption of green building standards, particularly in urban residential and commercial projects.

- The rapid scale-up of the Indian paints industry, led by players such as Asian Paints, Berger Paints, Kansai Nerolac, and newer entrants like Birla Opus and JSW Paints, is creating consistent upstream demand. For example, capacity additions in decorative paints are directly increasing the consumption of acrylic and styrene-acrylic binders.

- Ongoing investments by global companies including BASF, Dow, Arkema, Wacker, and Synthomer are strengthening local manufacturing and technical capabilities. Expansion of application labs and India-focused product development is helping move the market beyond commodity supply toward more customised and performance-driven solutions.

Key Market Drivers — India Emulsion Polymers Market

Rapid Expansion of Paints, Coatings, and Decorative Demand in India

The expansion of the paints and coatings industry remains the single largest driver of demand in the India emulsion polymers market. The sector is currently growing at around 11 to 13 percent annually, comfortably outpacing most other chemical end-use segments.

Decorative coatings account for close to 75 percent of total paint consumption in India, and emulsion polymers sit at the centre of these formulations, acting as the primary binder in both interior and exterior paints. As a result, any increase in paint production directly translates into higher polymer consumption.

India still has relatively low per capita paint consumption at around 4.5 to 5 kilograms, compared to 15 to 25 kilograms in developed markets. This gap reflects a long runway for growth, especially as urban housing, repainting cycles, and premiumisation trends continue to strengthen.

The supply side is also expanding rapidly. Leading companies such as Asian Paints, Berger Paints, Kansai Nerolac, and Akzo Nobel, along with newer entrants like Birla Opus and JSW Paints, have collectively announced investments exceeding USD 2 billion in new capacity. These expansions are already starting to translate into sustained upstream demand for acrylic and styrene-acrylic emulsions.

In practical terms, even incremental improvements in paint performance, such as better washability, durability, or finish, require higher binder content. This means that growth in the paints industry does not just increase volumes, but also raises the intensity of emulsion polymer usage over time.

Structural Shift Toward Water-Based and Bio-Based Emulsion Polymers

A clear shift toward water-based and bio-based emulsion polymers is underway in India, and this is becoming one of the most important structural drivers of market growth. These systems are currently expanding at around 13 to 16 percent annually, significantly faster than traditional solvent-based alternatives.

This transition is being shaped by tighter VOC emission norms under CPCB regulations, increasing adoption of green building certifications such as IGBC and LEED, and growing sustainability commitments from both manufacturers and end users. As a result, formulation strategies across paints, adhesives, and construction chemicals are gradually moving toward waterborne systems.

The difference in emission levels is substantial. Water-based emulsions typically contain less than 50 g/L of VOC, compared to 400 to 600 g/L in solvent-based products. This makes them far more suitable for indoor applications where low odour and better air quality are critical.

In practice, this shift is already visible in the market. Most interior wall paints used in urban housing are now water-based, and similar transitions are happening in tile adhesives, sealants, and construction chemicals used in residential and commercial projects.

On the supply side, global players such as BASF, Dow, and Arkema have expanded their waterborne product portfolios in India over the past two years. At the same time, domestic manufacturers are increasing investments in bio-based monomers and environmentally compliant emulsions, supporting the long-term transition toward more sustainable chemistries.

Overall, this is not just a regulatory adjustment. It reflects a broader change in how products are being designed and used, with water-based systems gradually becoming the default across multiple end-use applications.

Growth in Construction Chemicals, Adhesives, and Infrastructure-Led Demand

Expansion in construction activity, real estate development, and infrastructure projects is emerging as a major growth driver for the India emulsion polymers market. The construction chemicals segment is currently growing at around 12 to 14 percent annually, while adhesives and sealants are expanding at 10 to 12 percent, creating steady downstream demand for emulsion polymers.

These polymers act as key binders across a wide range of applications, including tile adhesives, waterproofing systems, sealants, concrete admixtures, and wood adhesives. As construction practices evolve toward ready-to-use and performance-enhanced materials, the role of polymers in improving flexibility, bonding strength, and durability has become more critical.

For example, tile adhesives used in modern residential and commercial projects are increasingly polymer-modified, replacing traditional cement-based applications. Similarly, waterproofing solutions used in basements, terraces, and bathrooms now rely heavily on emulsion-based systems to improve long-term performance.

Demand is being supported by a mix of residential housing growth, commercial real estate expansion, and large-scale infrastructure programs such as metro rail projects, Smart Cities initiatives, and highway development under Bharatmala. These projects are not only increasing construction volumes but also driving the adoption of higher-quality materials.

On the supply side, companies such as Pidilite Industries, BASF, Sika, and MYK Laticrete have expanded capacity and introduced broader product portfolios tailored to these applications. At the same time, the gradual formalisation of the construction chemicals market is encouraging the shift from unorganised, low-cost materials toward branded and performance-driven solutions.

As a result, this segment is moving from being a secondary demand source to a more consistent and structurally important contributor to overall emulsion polymer consumption in India.

Key Market Challenges — India Emulsion Polymers Market

Volatility in Monomer Feedstock Prices

The India emulsion polymers market remains highly sensitive to fluctuations in key raw materials such as acrylic acid, butyl acrylate, styrene, butadiene, and vinyl acetate monomer (VAM). These inputs typically account for around 60 to 75 percent of total production cost, making pricing closely linked to global crude oil and petrochemical movements.

Over the past two years, crude oil prices moving within the USD 70 to USD 95 per barrel range have led to 20 to 35 percent variation in monomer costs. This has made it difficult for manufacturers to maintain stable margins, particularly when supplying large paint and adhesive companies under fixed or quarterly pricing contracts.

In practice, producers often face delays in passing on cost increases, especially during periods of sudden price spikes. This creates short-term margin pressure and adds uncertainty to contract negotiations. To manage this, companies are increasingly exploring backward integration, long-term sourcing agreements, and formulation adjustments that reduce exposure to volatile feedstocks.

Dependence on Imported Specialty Monomers and High-Performance Grades

India continues to depend on imports for a large share of specialty monomers and advanced emulsion polymer grades. In several high-performance categories, over 55 to 65 percent of demand is still met through imports, particularly for high-purity acrylic derivatives, vinyl-versatate, and specialty dispersions.

This dependence exposes manufacturers to supply disruptions, currency fluctuations, and longer lead times, which can extend to 8 to 14 weeks depending on global shipping conditions.

For instance, delays in sourcing vinyl acetate or specialty acrylates can directly impact production cycles for adhesives and coatings, especially during peak construction periods when demand is already elevated.

Although domestic players such as Jubilant Ingrevia and GFL are expanding capacity, and global companies are strengthening local manufacturing, reducing this dependence will take time. Until then, supply reliability remains a key concern across the market.

Rising Environmental Compliance and Regulatory Complexity

Environmental compliance is becoming more demanding across the value chain, adding both cost and operational complexity. Emulsion polymer manufacturing requires significant water and energy input, along with strict wastewater treatment and emission control systems.

Compliance with CPCB norms, including Zero Liquid Discharge (ZLD) and air emission standards, can add approximately 8 to 12 percent to operating costs, particularly for smaller or less integrated manufacturers.

Export-oriented players face additional requirements such as REACH and other international regulatory frameworks, which increase documentation, testing, and process compliance efforts.

At the same time, downstream industries such as paints and coatings are facing tighter VOC limits and green certification requirements. This pressure flows upstream, requiring polymer manufacturers to continuously adapt formulations and improve environmental performance.

While these regulations increase complexity, they are also gradually favouring organised players with stronger R&D capabilities and better compliance infrastructure.

Key Market Trends — India Emulsion Polymers Market

Rapid Adoption of Water-Based, Low-VOC, and Bio-Based Emulsion Polymers in India

The India emulsion polymers market is undergoing a clear shift toward water-based, low-VOC, and bio-based emulsion systems, with waterborne emulsion polymers growing at 13 to 16 percent annually, significantly outpacing solvent-based alternatives. Tightening VOC norms under CPCB, green building certifications such as IGBC and LEED, and corporate ESG commitments are reshaping formulation strategies across paints, adhesives, and construction chemicals. Bio-based monomers derived from renewable feedstocks are gaining traction as downstream brands commit to Scope 3 emission reductions. In 2025, global majors including BASF, Dow, Arkema, Wacker, and Synthomer launched expanded waterborne and bio-based portfolios for the Indian market, reinforcing the structural shift across the India emulsion polymers market.

Capacity Expansion by Global Majors and Domestic Producers in the India Emulsion Polymers Market

A wave of domestic capacity expansion and global major investment is reshaping the India emulsion polymers market supply landscape. Combined India-focused capital expenditure announcements in emulsion polymers and waterborne chemistries exceeded USD 1.5 billion across 2023 to 2025. BASF expanded its Dahej complex, Arkema commissioned acrylic monomer and emulsion capacity, Wacker scaled VAE dispersions in Pune, and Synthomer strengthened SBR latex for paper coatings. Domestic players including Pidilite Industries, Jubilant Ingrevia, GFL Limited, and BASF India expanded emulsion polymer and specialty monomer capacity. PM MITRA-linked supply to new textile clusters and downstream paint capacity additions by Asian Paints, Berger, Kansai Nerolac, Grasim’s Birla Opus, and JSW Paints are structurally reinforcing demand growth in the India emulsion polymers market.

Rising Role of Construction Chemicals, Adhesives, and Packaging in Emulsion Polymer Demand

Construction chemicals, adhesives and sealants, and packaging applications are emerging as high-growth pull-through segments for the India emulsion polymers market, collectively expected to account for over 35 percent of total emulsion polymer demand by 2032. The Indian construction chemicals market is growing at 12 to 14 percent annually, while adhesives and sealants are expanding at 10 to 12 percent, with emulsion polymers used extensively in tile adhesives, waterproofing membranes, pressure-sensitive adhesives, wood glues, and packaging laminates. Leading players including Pidilite Industries (Fevicol, Dr. Fixit), BASF, Sika, MYK Laticrete, 3M India, and Henkel India have scaled capacity and launched premium waterborne product ranges. This structural pull-through is reinforcing India emulsion polymers market forecast 2032 across both domestic and export-oriented segments.

Segmental Insights — India Emulsion Polymers Market

By Application — Paints and Coatings Remain the Core Consumption Segment

Paints and coatings continue to account for the largest share of emulsion polymer consumption in India, contributing roughly 52 to 55 percent of total demand. This dominance comes from the extensive use of emulsion binders in decorative interior and exterior paints, as well as in architectural and selected industrial coatings.

Within this segment, acrylic and styrene-acrylic emulsions remain the preferred chemistries due to their balance of durability, adhesion, and finish quality. Water-based systems are now widely used across decorative coatings, particularly in urban housing and commercial projects.

Adhesives and sealants represent the next major application, contributing around 20 to 22 percent of demand, followed by construction chemicals at 12 to 15 percent, including tile adhesives, waterproofing systems, and concrete admixtures.

Recent capacity additions by leading paint manufacturers have further strengthened this segment. Increased production of decorative paints is translating directly into higher and more consistent offtake of emulsion polymers, reinforcing its position as the primary demand centre.

By Product Type — Acrylic Emulsions Lead, While Specialty and Bio-Based Systems Gain Momentum

Acrylic emulsions hold the leading position in the product mix, accounting for approximately 40 to 42 percent of total consumption. Their widespread use is linked to strong performance across a range of applications, including paints, adhesives, and coatings that require weather resistance and long-term durability.

Styrene-acrylic emulsions contribute another 22 to 25 percent, offering a cost-performance balance for mid-range applications. Vinyl acetate-based emulsions, including PVAc and VAE, account for 18 to 20 percent, particularly in adhesives and paper coatings, while styrene-butadiene latex represents 10 to 12 percent, largely used in paper and packaging applications.

At the same time, higher-value categories such as bio-based emulsions and polyurethane dispersions (PUD) are gradually gaining traction. These products are being adopted in applications where performance requirements are more specific, such as flexibility, chemical resistance, or environmental compliance.

This shift indicates a gradual move in the market mix, where standard emulsions continue to dominate volumes, but specialty products are contributing a growing share of value.

Regional Insights — India Emulsion Polymers Market

West and South India together account for the majority of production and consumption, contributing approximately 58 to 62 percent of total demand. This concentration is supported by well-established chemical manufacturing clusters in Gujarat, Maharashtra, and Tamil Nadu, along with proximity to major paint and coatings production hubs.

Industrial zones such as Dahej, Ankleshwar, Vapi, Pune, and Chennai play a key role in both production and distribution, enabling efficient supply to large downstream customers.

North India contributes around 20 to 24 percent of demand, driven by construction activity, adhesive manufacturing, and expanding packaging applications across states such as Haryana, Rajasthan, and Uttar Pradesh.

East and Central India together account for roughly 14 to 18 percent, with demand supported by regional paints manufacturing and gradual growth in construction chemicals usage.

Recent capacity additions by both global and domestic players have further strengthened these regional clusters. Expanding local production has improved supply responsiveness and enabled closer alignment with customer requirements across paints, adhesives, and construction applications.

Recent Developments — India Emulsion Polymers Market

- The India emulsion polymers market has seen steady activity in capacity expansion and product innovation during 2024 and 2025. BASF expanded its emulsion polymer capacity at Dahej, Arkema added new acrylic monomer and emulsion lines, Wacker scaled VAE dispersion output at its Pune facility, and Synthomer increased styrene-butadiene latex capacity for paper and packaging applications. Domestic players such as Pidilite Industries, Jubilant Ingrevia, and GFL Limited have also announced new investments in specialty emulsions, strengthening India’s position as a more competitive manufacturing base.

- Paint and coating companies are increasingly strengthening local sourcing of emulsion polymers. Leading players such as Asian Paints, Berger Paints, Kansai Nerolac, and Akzo Nobel expanded long-term supply arrangements with both domestic and global suppliers in 2025. At the same time, new entrants like Birla Opus and JSW Paints have commissioned large decorative paint capacities, which is already translating into higher upstream demand. In parallel, construction chemical and adhesive companies including Pidilite, Sika, MYK Laticrete, and Henkel India have broadened their product portfolios, particularly in water-based systems, reinforcing stronger linkages across the value chain.

- Sustainability-led product development is becoming more visible across the market. During 2025, companies such as BASF, Dow, Arkema, and Wacker introduced expanded ranges of water-based, low-VOC, and bio-based emulsions tailored for Indian applications. In several cases, these developments are supported by closer collaboration between polymer producers and downstream manufacturers, especially in paints and construction chemicals. This is gradually positioning India not just as a manufacturing location, but also as a development hub for environmentally compliant and application-focused emulsion systems

Key Market Players — India Emulsion Polymers Market

- BASF India Limited

- Dow Chemical International Pvt. Ltd.

- Arkema India Pvt. Ltd.

- Wacker Chemie India Pvt. Ltd.

- Synthomer Specialty Chemicals (India)

- Pidilite Industries Limited

- Jubilant Ingrevia Limited

- GFL Limited (Gujarat Fluorochemicals)

- Asian Paints Limited (captive emulsion polymers)

- Celanese India Pvt. Ltd.

- Trinseo India Pvt. Ltd.

- Specialty Polymers Pvt. Ltd.

Report Scope

In this report, the India Emulsion Polymers Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Acrylic Emulsions

- Styrene-Butadiene Latex / Emulsions

- Vinyl Acetate Emulsions (PVAc & VAE)

- Styrene-Acrylic Emulsions

- Polyurethane Dispersions (PUD)

- Fluoropolymer Emulsions

- Bio-Based Emulsions

- Others

- By Chemistry

- Water-Based Emulsions

- Solvent-Based Emulsions

- Hybrid Emulsions

- Bio-Based / Waterborne Green Emulsions

- By Monomer

- Acrylics

- Styrene-Butadiene

- Vinyl Acetate

- Vinyl Versatate

- Styrene-Acrylic

- Urethane

- Others

- By Solid Content

- Below 30%

- 30–50%

- 50–60%

- Above 60%

- By Application

- Paints & Coatings

- Architectural Coatings

- Adhesives & Sealants

- Paper & Paperboard Coatings

- Textile & Non-Woven Binders

- Carpet Backing

- Leather Finishing

- Construction Chemicals

- Printing Inks

- Others

- By End-Use Industry

- Building & Construction

- Paints & Coatings Manufacturing

- Packaging & Paper

- Textile & Non-Wovens

- Automotive

- Furniture & Woodworking

- Leather & Footwear

- Personal Care

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Specialty Chemical Agents

- Online / B2B Platforms

- Contract Manufacturing

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Emulsion Polymers Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic emulsion polymer producers, specialty waterborne chemistry specialists, global entrants, or niche segment leaders.

The India Emulsion Polymers Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021–2032

- By Product Type

- By Application

- By End-Use Industry

- By Feedstock

- By Sales Channel

- By Region

- Analyst Recommendations

- Market Overview, 2021–2032

- Geopolitical Impact on India Emulsion Polymers Market

- India Emulsion Polymers Market Insights

- Market Dynamics

- Growth Drivers

- Rapid expansion of paints, coatings, and architectural decorative demand driving core emulsion polymer consumption.

- Structural shift toward water-based and bio-based emulsion polymers driven by VOC regulations and green building norms.

- Accelerated construction chemicals, adhesives, and infrastructure-led demand for emulsion polymers.

- Restraints

- Monomer feedstock price volatility linked to crude oil and global supply disruptions pressuring producer margins.

- Heavy import dependence for specialty monomers and high-performance emulsion grades creating supply risk.

- Environmental compliance, effluent management, and tightening VOC regulatory complexity raising compliance costs.

- Opportunities

- Rapid scale-up of waterborne, bio-based, and low-VOC emulsion polymers aligned with green building and sustainability mandates.

- High-growth demand from construction chemicals, waterproofing membranes, tile adhesives, and concrete admixtures supporting infrastructure build-out.

- Emerging export opportunity for specialty emulsion polymers to Middle East, Southeast Asia, and African markets with growing paint and packaging industries.

- Challenges

- Intense price-led competition between global emulsion polymer majors and domestic producers compressing margins.

- Shortage of skilled polymer chemists, formulation scientists, and reactor operators limiting scale-up speed of new capacity.

- Fragmented downstream paint and adhesive customer base with diverse specifications increasing formulation and inventory complexity.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Dynamics

- Industry Value Chain & Entry Points

- Upstream Petrochemical Feedstock (crude oil, naphtha, propylene, ethylene, benzene)

- Monomer Producers (acrylic acid, butyl acrylate, styrene, butadiene, VAM, acrylates)

- Bio-Based Monomer Producers (renewable feedstock, fermentation-derived monomers)

- Emulsion Polymerisation & Reactor Operations (batch, semi-batch, continuous)

- Quality Control, R&D & Application Laboratories (BIS, REACH, TSCA, ecolabels)

- Distributors, Specialty Chemical Agents & B2B Marketplaces

- Downstream Formulators (paints, adhesives, construction chemicals, paper, textiles)

- Brand Owners & Manufacturers (paint companies, adhesive brands, construction chemical brands)

- Installation & Retail Channels (painters, contractors, DIY retail, project tenders)

- End-Use Industries (construction, packaging, automotive, textiles, personal care)

- India Emulsion Polymers Market: Regulatory Framework

- India Emulsion Polymers Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (‘000 Tons)

- Market Share & Forecast

- By Product Type

- Acrylic Emulsions

- Styrene-Butadiene Latex / Emulsions

- Vinyl Acetate Emulsions (PVAc & VAE)

- Styrene-Acrylic Emulsions

- Polyurethane Dispersions (PUD)

- Fluoropolymer Emulsions

- Bio-Based Emulsions

- Others

- By Chemistry

- Water-Based Emulsions

- Solvent-Based Emulsions

- Hybrid Emulsions

- Bio-Based / Waterborne Green Emulsions

- By Monomer

- Acrylics

- Styrene-Butadiene

- Vinyl Acetate

- Vinyl Versatate

- Styrene-Acrylic

- Urethane

- Others

- By Solid Content

- Below 30%

- 30–50%

- 50–60%

- Above 60%

- By Application

- Paints & Coatings

- Architectural Coatings

- Adhesives & Sealants

- Paper & Paperboard Coatings

- Textile & Non-Woven Binders

- Carpet Backing

- Leather Finishing

- Construction Chemicals

- Printing Inks

- Others

- By End-Use Industry

- Building & Construction

- Paints & Coatings Manufacturing

- Packaging & Paper

- Textile & Non-Wovens

- Automotive

- Furniture & Woodworking

- Leather & Footwear

- Personal Care

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Specialty Chemical Agents

- Online / B2B Platforms

- Contract Manufacturing

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Market Size & Forecast, 2021-2032

- Competitive Landscape

- India Emulsion Polymers Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- BASF India Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- BASF India Limited

*(Same Data Pointers Will Be Provided for The Below Companies)

- Dow Chemical International Pvt. Ltd.

- Arkema India Pvt. Ltd.

- Wacker Chemie India Pvt. Ltd.

- Synthomer Specialty Chemicals (India)

- Pidilite Industries Limited

- Jubilant Ingrevia Limited

- GFL Limited (Gujarat Fluorochemicals)

- Asian Paints Limited (captive emulsion polymers)

- Celanese India Pvt. Ltd.

- Trinseo India Pvt. Ltd.

- Specialty Polymers Pvt. Ltd.

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India emulsion polymers market and what is its growth forecast?

Ans: The India emulsion polymers market size is valued at USD 2.85 billion in 2025 and is projected to reach USD 5.64 billion by 2032, growing at a CAGR of around 10.2 percent. This strong India emulsion polymers market growth is driven by accelerated paints and coatings demand, rising construction chemicals and adhesives consumption, structural shift toward waterborne and bio-based chemistries, and major domestic and global capacity expansions. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India emulsion polymers market?

Ans: The India emulsion polymers market segmentation shows that paints and coatings dominate with approximately 52 to 55 percent share, followed by adhesives and sealants at 20 to 22 percent and construction chemicals at 12 to 15 percent. Acrylic emulsions lead by product type with 40 to 42 percent share, while water-based and bio-based emulsion polymers are the fastest-growing segment, expanding at 13 to 16 percent annually. The report breaks down demand across product types, chemistries, monomers, applications, end-use industries, and sales channels, helping businesses understand where growth is accelerating across the India emulsion polymers market.

3. What are the key drivers of growth in the India emulsion polymers market?

Ans: Key India emulsion polymers market drivers include rapid expansion of the Indian paints and coatings industry growing at 11 to 13 percent annually, structural shift toward water-based and bio-based emulsion chemistries driven by VOC regulations and green building norms, and accelerated construction chemicals, adhesives, and infrastructure-led demand. Global emulsion polymer majors such as BASF, Dow, Arkema, Wacker, and Synthomer are investing in India-specific manufacturing capacity and application laboratories. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends shaping the India emulsion polymers market.

4. Which regions are driving growth in the India emulsion polymers market?

Ans: Regional analysis of the India emulsion polymers market shows that West and South India together account for nearly 58 to 62 percent of total demand, driven by specialty chemical clusters in Gujarat, Maharashtra, and Tamil Nadu, along with strong paints and coatings manufacturing. North India contributes around 20 to 24 percent, supported by construction chemicals and tile adhesive manufacturing. East and Central India together account for 14 to 18 percent, supported by West Bengal’s paints industry and growing construction activity. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India emulsion polymers market?

Ans: The latest India emulsion polymers market trends include rapid adoption of water-based, low-VOC, and bio-based emulsion polymers, major capacity expansion by global majors and domestic producers, and the rising role of construction chemicals, adhesives, and packaging in emulsion polymer demand. Waterborne emulsion polymers are growing at 13 to 16 percent annually, nearly twice the pace of solvent-based alternatives, while capacity additions exceeded USD 1.5 billion across 2023 to 2025. The report provides detailed insights into emerging trends, innovation pipelines, and future demand shifts, helping businesses stay ahead of competition and capture new growth opportunities in the India emulsion polymers market.

Frequently Asked Questions

1. How large is the India emulsion polymers market and what is its growth forecast?

Ans: The India emulsion polymers market size is valued at USD 2.85 billion in 2025 and is projected to reach USD 5.64 billion by 2032, growing at a CAGR of around 10.2 percent. This strong India emulsion polymers market growth is driven by accelerated paints and coatings demand, rising construction chemicals and adhesives consumption, structural shift toward waterborne and bio-based chemistries, and major domestic and global capacity expansions. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India emulsion polymers market?

Ans: The India emulsion polymers market segmentation shows that paints and coatings dominate with approximately 52 to 55 percent share, followed by adhesives and sealants at 20 to 22 percent and construction chemicals at 12 to 15 percent. Acrylic emulsions lead by product type with 40 to 42 percent share, while water-based and bio-based emulsion polymers are the fastest-growing segment, expanding at 13 to 16 percent annually. The report breaks down demand across product types, chemistries, monomers, applications, end-use industries, and sales channels, helping businesses understand where growth is accelerating across the India emulsion polymers market.

3. What are the key drivers of growth in the India emulsion polymers market?

Ans: Key India emulsion polymers market drivers include rapid expansion of the Indian paints and coatings industry growing at 11 to 13 percent annually, structural shift toward water-based and bio-based emulsion chemistries driven by VOC regulations and green building norms, and accelerated construction chemicals, adhesives, and infrastructure-led demand. Global emulsion polymer majors such as BASF, Dow, Arkema, Wacker, and Synthomer are investing in India-specific manufacturing capacity and application laboratories. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends shaping the India emulsion polymers market.

4. Which regions are driving growth in the India emulsion polymers market?

Ans: Regional analysis of the India emulsion polymers market shows that West and South India together account for nearly 58 to 62 percent of total demand, driven by specialty chemical clusters in Gujarat, Maharashtra, and Tamil Nadu, along with strong paints and coatings manufacturing. North India contributes around 20 to 24 percent, supported by construction chemicals and tile adhesive manufacturing. East and Central India together account for 14 to 18 percent, supported by West Bengal’s paints industry and growing construction activity. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India emulsion polymers market?

Ans: The latest India emulsion polymers market trends include rapid adoption of water-based, low-VOC, and bio-based emulsion polymers, major capacity expansion by global majors and domestic producers, and the rising role of construction chemicals, adhesives, and packaging in emulsion polymer demand. Waterborne emulsion polymers are growing at 13 to 16 percent annually, nearly twice the pace of solvent-based alternatives, while capacity additions exceeded USD 1.5 billion across 2023 to 2025. The report provides detailed insights into emerging trends, innovation pipelines, and future demand shifts, helping businesses stay ahead of competition and capture new growth opportunities in the India emulsion polymers market.