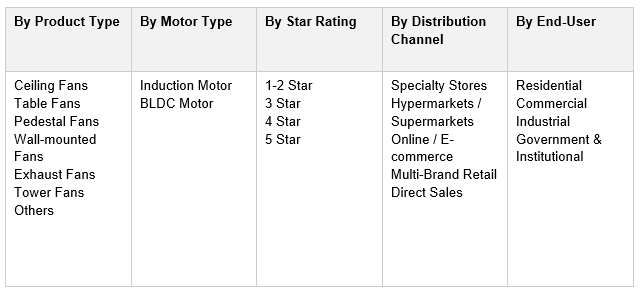

India Electric Fans Market, By Product Type (Ceiling, Table, Pedestal/Stand, Wall-mounted, Exhaust, Tower, Others); By Motor Type (Induction Motor, BLDC Motor); By Blade Material (Plastic, Aluminium, Wood, Metal, Others); By Sweep Size (Below 900mm, 900-1200mm, Above 1200mm); By Star Rating (1-2 Star, 3 Star, 4 Star, 5 Star); By Price Range (Economy, Mid-Range, Premium, Luxury/Designer); By Distribution Channel (Specialty Stores, Hypermarkets/Supermarkets, Online/E-commerce, Multi-Brand Retail, Direct Sales); By End-User (Residential, Commercial, Industrial, Government & Institutional); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Electric Fans Market: BLDC Adoption, BEE Star Labelling, and Smart Cooling Demand Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

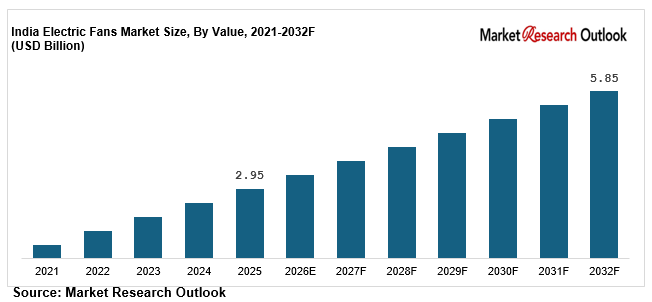

| Market Size (2025) | USD 2.95 Billion |

| CAGR (2026-2032) | 10.2% |

| Leading Segment | Ceiling Fans (Induction Motor) |

| Fastest Growing Segment | BLDC / Smart Ceiling Fans |

| Market Size (2032) | USD 5.85 Billion |

Source: Market Research Outlook

Market Overview: India Electric Fans Market

The India electric fans market size is witnessing steady expansion, driven by rising ambient temperatures, accelerating urbanization across Tier-I, Tier-II, and Tier-III cities, expanding rural electrification reach, mandatory BEE (Bureau of Energy Efficiency) star labelling norms effective January 2023, and rapid penetration of energy-efficient BLDC motor technology. Valued at USD 2.95 billion in 2025 and projected to reach USD 5.85 billion by 2032, growing at a CAGR of 10.2%, the India electric fans market growth is being fuelled by strong residential adoption supported by PMAY housing schemes, rising mid-range and premium ceiling fan demand among urban households, growing commercial procurement from hotels, offices, hospitals, and educational institutions, and the rapid scaling of online and D2C distribution platforms. Ceiling fans lead consumption with over 75% category share, while BLDC ceiling fans are emerging as the fastest growing category. Strengthening BEE 2023 star rating norms, smart home adoption, and aspirational interior preferences by Indian consumers, alongside aggressive new product launches by leading brands, are reshaping the supply landscape. As domestic majors including Havells, Crompton Greaves, Orient Electric, Bajaj Electricals, Usha International, and Atomberg scale BLDC, smart, and premium designer fan portfolios, and global majors including Panasonic and Schneider Electric deepen India-specific innovation, the India electric fans market is evolving into a technology-led, brand-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Electric Fans Market

- The India electric fans market size is projected to grow from USD 2.95 billion in 2025 to USD 5.85 billion by 2032, registering a strong CAGR of 10.2%, driven by accelerated BLDC fan adoption, rising BEE star-rated fan demand, climate-driven cooling consumption, and the structural shift toward energy-efficient ceiling, table, pedestal, and exhaust fans across Indian homes.

- Ceiling fans dominate the India electric fans market, accounting for over 75% of total category value in 2025, driven by mass-market price points of INR 1,200 to INR 4,500, daily-use cooling behaviour, and strong distribution across modern trade, electrical retail, pharmacies, and online platforms across urban and semi-urban India.

- BLDC and smart ceiling fans are emerging as the fastest growing segment in the India electric fans market, expected to grow at 22% to 26% annually as energy-conscious consumers, BEE 2023 mandatory star rating norms, and rising electricity tariffs accelerate the shift from traditional induction motor fans to BLDC fans offering 50% to 65% power savings.

- Rapid scaling of e-commerce platforms such as Amazon, Flipkart, Tata Cliq, and quick-commerce channels Blinkit and Zepto, with online electric fan sales crossing 18% to 22% of category value by mid-2025, is structurally expanding the India electric fans market across residential, commercial, and Tier-II city consumption.

- Rising investments by domestic majors such as Havells, Crompton Greaves, Orient Electric, Atomberg, Polycab, and V-Guard in BLDC motor manufacturing, premium designer fan launches, and Make-in-India PLI scheme commitments are strengthening domestic supply and supporting the India electric fans market forecast 2032.

Key Market Drivers: India Electric Fans Market

Rising Temperatures, Climate Change, and Urbanization Driving Sustained Electric Fan Demand

Growth in the India electric fans market is being driven by rising ambient temperatures, accelerating climate change impact, and structural urbanization across Indian metros and Tier-II cities. India recorded over 540 heatwave days across 2024 and 2025 according to IMD data, with peak summer temperatures in North and Central India crossing 47 to 49 degrees Celsius, structurally increasing cooling appliance demand. Per-capita ambient cooling consumption in India remains well below global benchmarks of USD 14 to 22, while electric fan household penetration has crossed 84% in 2025, up from 72% in 2018, supported by rising electrification and PMAY housing rollouts. India’s per-capita disposable income has grown at over 9% annually between 2020 and 2025, supporting discretionary spend on premium and BLDC fans. Cooling appliance demand among the 25 to 45 age cohort, supported by work-from-home culture, growing apartment supply, and longer summers, is structurally pulling demand into the India electric fans market. Mass-priced ceiling fans between INR 1,200 and INR 4,500, available across modern trade, electrical retail, and online platforms, continue to drive high-volume penetration across the country.

Mandatory BEE Star Labelling and Energy Efficiency Norms Boosting BLDC Fan Adoption

The India electric fans market is benefiting from a structural regulatory push under the Bureau of Energy Efficiency (BEE), with mandatory star labelling for ceiling fans implemented from January 2023, accelerating consumer shift toward energy-efficient BLDC fans. 5-star rated BLDC ceiling fans consume only 28 to 35 watts compared to 70 to 80 watts for traditional induction motor fans, delivering 50% to 65% power savings and electricity bill reductions of INR 1,500 to INR 2,200 per fan annually. Domestic BLDC ceiling fan capacity has scaled rapidly, with Indian manufacturing exceeding 18 million BLDC units annually by 2025, led by Atomberg, Havells, Crompton, Orient Electric, Polycab, and Superfan. The Production Linked Incentive (PLI) scheme for White Goods, BEE 2023 star rating norms, and Basic Customs Duty on cheap fan imports have further strengthened domestic BLDC supply, supporting price competitiveness across the India electric fans market. Average BLDC ceiling fan prices have compressed from INR 3,800 to INR 4,500 in 2020 to INR 2,800 to INR 3,800 in 2025, accelerating mass-market adoption.

E-commerce Expansion, D2C Brands, PMAY Housing Scheme, and Rural Electrification Accelerating Category Growth

Rapid growth in online and D2C distribution is a major catalyst for the India electric fans market, with the e-commerce channel projected to grow at 18% to 22% annually through 2032. Online electric fan sales now account for an estimated 18% to 22% of total category value, led by platforms such as Amazon, Flipkart, Tata Cliq, Croma Online, and Reliance Digital. Quick-commerce platforms including Blinkit, Zepto, Swiggy Instamart, and BigBasket Now have emerged as new growth engines for table fans, pedestal fans, and replacement ceiling fans in urban markets. The Pradhan Mantri Awas Yojana (PMAY) housing scheme, which targets construction of over 4 crore homes by 2027, alongside Saubhagya and DDUGJY rural electrification programs delivering electricity access to over 99.5% of Indian households, has structurally expanded the residential electric fan addressable market. Leading D2C and digital-first brands such as Atomberg, Superfan, and Crompton Insta have scaled aggressive influencer, content, and performance marketing pipelines, supporting structural expansion of the India electric fans market across all major end-user categories through 2032.

Key Market Challenges: India Electric Fans Market

Strong Unorganized Market and Counterfeit / Cheap Imported Fan Products

The India electric fans market continues to face challenges around the strong presence of an unorganized local assembly economy and a large counterfeit and cheap imported fan segment. The unorganized and regional fan economy, estimated at 28% to 32% of total category volume in 2025, undermines brand-building investments by leading players such as Havells, Crompton, Orient Electric, and Bajaj Electricals. Look-alike packaging, imitation Usha, Crompton, Havells, and Orient variants, and unauthorised online listings continue to challenge category economics. Cheap Chinese and ASEAN-imported table and exhaust fans, priced 25% to 40% below organized brands, continue to penetrate the economy segment despite increased Basic Customs Duty and BIS quality enforcement. Strengthening enforcement under the Bureau of Indian Standards (BIS), mandatory BIS certification under IS 374, and tighter e-commerce listing policies are gradually easing these pressures, but unorganized and grey-market penetration remains a structural concern across the India electric fans market.

Raw Material Price Volatility for Copper, Aluminium, Steel, and Engineering Plastics

The India electric fans market faces structural complexity from raw material price volatility, particularly for copper, aluminium, steel, engineering plastics, and electronic components used in BLDC controllers. Global copper prices have fluctuated by 18% to 28% between 2022 and 2025, while aluminium prices have moved within a 14% to 22% range, directly impacting motor and blade manufacturing economics. India imports a significant share of high-grade copper winding wire, neodymium magnets for BLDC motors, and electronic controller components, exposing manufacturers to currency volatility and global supply chain risks. Steel, used in chassis and brackets, has seen sustained inflation, while ABS and polypropylene plastic prices have risen by 8% to 16% over 2023 to 2025, compressing gross margins for mass-market fan manufacturers. While leading domestic players such as Havells, Crompton, Polycab, and Atomberg are localising motor manufacturing and electronic controller assembly under the PLI scheme, raw material volatility remains a near-term challenge for the India electric fans market.

Low Replacement Cycle and Price Sensitivity in Mass-Market Segments

The India electric fans market faces practical constraints around a long replacement cycle and high price sensitivity in mass-market segments. Indian ceiling fans typically have a replacement cycle of 8 to 12 years, well above global benchmarks of 5 to 7 years, driven by consumer perception of fans as durable goods rather than upgradeable appliances. This long replacement cycle limits BLDC fan upgrade demand, particularly among middle-income and rural households where traditional induction motor fans continue to operate. Average mass-market ceiling fan prices of INR 1,200 to INR 2,200 remain significantly below BLDC entry pricing of INR 2,800 to INR 3,800, creating affordability gaps despite long-term energy savings. After-sales service gaps, including capacitor replacement, regulator servicing, and blade replacement, remain a key consumer pain point across Tier-II and rural markets. While leading brands such as Havells, Crompton, Orient, and Atomberg have built service networks of 400 to 1,000 cities, smaller and regional players continue to face execution gaps across the India electric fans market.

Key Market Trends: India Electric Fans Market

Rapid Adoption of BLDC Motor Technology and Smart, IoT-Enabled Ceiling Fans

The India electric fans market is undergoing a clear technology shift toward BLDC (brushless DC) motors and smart, IoT-enabled ceiling fans, with these advanced categories expected to capture over 35% of new ceiling fan installations by 2027. BLDC ceiling fans deliver power consumption of 28 to 35 watts compared to 70 to 80 watts for traditional induction motor fans, with longevity exceeding 15 years and quieter operation. Smart ceiling fans with Wi-Fi connectivity, voice control via Amazon Alexa and Google Assistant, remote control via mobile apps, temperature-sensing auto-speed adjustment, and integration with smart home ecosystems are increasingly preferred by metro and Tier-I urban consumers. Leading domestic manufacturers including Atomberg, Havells, Crompton (Crompton SilentPro), Orient Electric (Aeroquiet), Polycab, and Superfan have scaled BLDC and smart fan production capacity through 2024 and 2025. Premium designer aesthetic ceiling fans with anti-dust coating, decorative finishes, wooden blades, and ultra-silent operation are also gaining strong consumer traction. This technology transition is reinforcing the India electric fans market forecast 2032 across both mid-range and premium categories.

Growth of Premium Designer, Anti-Dust, and Decorative Aesthetic Ceiling Fans

A clear shift toward premium designer, anti-dust, and decorative aesthetic ceiling fans is reshaping the India electric fans market, particularly across the premium and luxury segments. Premium designer fan launches grew by over 32% in 2024 and 2025, with leading players including Havells (Stealth Air, Carlos), Crompton (Avancer Magic), Orient Electric (i-Tome, Aeroquiet), Atomberg (Renesa, Aris), Luminous, and Anchor scaling premium aesthetic portfolios. Decorative finishes including matte black, brushed bronze, walnut wood, and lacquered white are increasingly central to premium fan brand positioning, especially among urban millennial and Gen-Z homeowners. Anti-dust coating technology, which reduces dust accumulation on blades by 50% to 70% and supports easy cleaning, is seeing structural demand across urban India. Underlight ceiling fans, BLDC fans with integrated LED lighting, and ultra-silent fans operating below 30 decibels are gaining traction across premium apartment and villa installations. This premiumization momentum is supporting category value growth and is reinforcing structural growth across the India electric fans market.

Capacity Expansion by Domestic Manufacturers, PLI Scheme, and Make-in-India Push

A wave of domestic capacity expansion and vertical integration is reshaping the India electric fans market supply landscape. Combined India-focused capital expenditure announcements in electric fan and BLDC motor manufacturing exceeded INR 4,200 crore across 2023 to 2025 under the Production Linked Incentive (PLI) scheme for White Goods. Havells expanded its Ghiloth, Rajasthan, and Neemrana plants for BLDC manufacturing, Crompton scaled Vadodara and Goa fan capacity, Orient Electric expanded its Faridabad facility, Atomberg added new BLDC manufacturing in Maharashtra, and Polycab commissioned new fan production lines. PLI scheme allocations exceeding INR 6,238 crore for the White Goods sector, mandatory BIS certification under IS 374, and Basic Customs Duty on imports have structurally favoured domestic supply. Combined with BEE 2023 star labelling driving BLDC demand and PMAY housing rollouts expanding the residential fan addressable market, these developments are reinforcing the India electric fans market forecast 2032 across the entire value chain.

Segmental Insights: India Electric Fans Market

By Product Type: Ceiling Fans Segment Dominates the India Electric Fans Market

The ceiling fans segment dominates the India electric fans market, accounting for an estimated 74% to 78% of total category value, driven by ubiquitous residential adoption, mandatory BEE star labelling from January 2023, rising electricity tariffs, and improving BLDC fan economics. Induction motor ceiling fans currently lead with over 65% of ceiling fan volumes, while BLDC ceiling fans capture 35% of category volume and over 45% of category value in 2025. Pedestal and stand fans contribute another 9% to 11% of demand, driven by mass-market summer cooling adoption. Table fans account for 7% to 9%, led by economy and Tier-II city consumption. Wall-mounted fans contribute 4% to 5%, supported by commercial and small-room applications, while exhaust fans capture 3% to 4%, driven by kitchen and bathroom installations. Tower fans, a premium emerging category, contribute 1% to 2% of category value but are growing at over 25% annually. In 2025, leading players including Havells, Crompton, Orient Electric, Bajaj, Usha, Atomberg, and Polycab scaled up ceiling fan and BLDC fan deployment under BEE 2023 norms, reinforcing segment dominance in the India electric fans market.

By Motor Type and Price Range: Induction Leads While BLDC and Premium Grow Fastest

Induction motor fans lead the India electric fans market motor landscape, accounting for approximately 65% to 68% of total category volume, driven by their lower price points of INR 1,200 to INR 2,500 and strong distribution across mass-market and rural channels. BLDC motor fans contribute another 32% to 35% of category volume but over 45% of category value, driven by superior efficiency, 50% to 65% power savings, and growing adoption in urban and premium residential installations. By price range, mass-priced fans below INR 2,500 lead with 58% to 62% share, supported by daily-use replacement and PMAY-driven new housing demand. Mid-range fans priced between INR 2,500 and INR 5,000 contribute another 25% to 28%, primarily BLDC and 4-5 star rated models. Premium and luxury designer fans priced above INR 5,000 account for 10% to 14% of category value, led by Havells Stealth, Crompton Avancer, Orient i-Tome, and Atomberg Renesa. Leading domestic manufacturers including Havells, Crompton, Orient, Bajaj, Polycab, and Atomberg have aligned product portfolios to this motor and price-tier mix, driving BLDC and premium fan adoption across the India electric fans market.

Regional Insights: India Electric Fans Market

Regional analysis of the India electric fans market shows that North India and Central India collectively account for approximately 48% to 52% of total category value, driven by Uttar Pradesh, Delhi NCR, Punjab, Haryana, Rajasthan, Madhya Pradesh, and Bihar, supported by extreme summer temperatures crossing 47 degrees Celsius, large household base, and strong PMAY housing rollouts. West India contributes around 22% to 24% of demand, led by Maharashtra (Mumbai, Pune urban consumption belt), Gujarat (Ahmedabad, Surat), and parts of Madhya Pradesh, supported by urban apartment growth and premium BLDC fan adoption. South India contributes around 20% to 22% of demand, led by Tamil Nadu (Chennai), Karnataka (Bengaluru), Andhra Pradesh, Telangana (Hyderabad), and Kerala, supported by industrial commercial demand and an established Atomberg, Crompton, and Superfan consumer base. East India together accounts for 8% to 10% of demand, supported by West Bengal (Kolkata), Odisha, and the Northeast, where rural electrification under DDUGJY and Saubhagya is accelerating ceiling fan penetration. In 2025, capacity additions and brand activity by Havells across Rajasthan, Crompton in Vadodara and Goa, Atomberg in Maharashtra, Orient Electric in Faridabad, and Polycab across pan-India reinforced regional supply hubs, supporting closer execution of residential and commercial fan deployment across the India electric fans market.

Recent Developments: India Electric Fans Market

- The India electric fans market witnessed strong momentum in BLDC adoption, new product launches, and channel expansion during 2024 and 2025. The category grew by an estimated 11% to 13% in value terms in 2025, supported by extreme summer heatwave demand, BEE 2023 star rating compliance, festive season activations, and quick-commerce expansion. Online and D2C sales crossed 18% to 22% of total category value, with BLDC ceiling fan sales growing by over 32% year-on-year, according to leading industry trackers. Cumulative BLDC fan penetration is projected to expand from 35% in 2025 to 55% to 60% by FY32, growing at an average 22% to 26% annually.

- Domestic electric fan manufacturers have deepened India-focused capacity expansion and BLDC technology investment. In 2025, Havells expanded BLDC manufacturing at its Ghiloth and Neemrana plants and launched new Stealth Air premium designer variants, Crompton scaled Vadodara and Goa BLDC capacity with new Avancer Magic launches, Orient Electric expanded Faridabad production and introduced i-Tome smart BLDC fans, Atomberg scaled Maharashtra BLDC manufacturing and launched Renesa and Aris series, and Polycab expanded fan production lines under the PLI scheme. Bajaj Electricals and Usha International also expanded BLDC and designer fan portfolios. These developments are strengthening domestic supply and supporting the India electric fans market forecast 2032.

- Premium and D2C electric fan momentum has gained strong traction in the India electric fans market. In 2025, leading premium and digital-first players including Atomberg, Superfan, Havells Stealth, Crompton SilentPro, Orient Aeroquiet, and Luminous scaled premium BLDC, designer aesthetic, anti-dust, and smart fan portfolios. Strategic partnerships between domestic fan manufacturers, e-commerce platforms such as Amazon, Flipkart, Croma, and Reliance Digital, and quick-commerce platforms Blinkit, Zepto, and Instamart are positioning India as one of the most actively scaling BLDC fan markets globally, strengthening long-term competitive positioning in the India electric fans market forecast 2032.

Key Market Players: India Electric Fans Market

- Havells India Limited

- Crompton Greaves Consumer Electricals Limited

- Orient Electric Limited (CK Birla Group)

- Bajaj Electricals Limited

- Usha International Limited

- V-Guard Industries Limited

- Polycab India Limited

- Atomberg Technologies Pvt. Ltd.

- Khaitan Electricals Limited

- Luminous Power Technologies Pvt. Ltd. (Schneider Electric)

- Anchor by Panasonic India

- Surya Roshni Limited

- Almonard Pvt. Ltd.

- GM Modular Pvt. Ltd.

- Superfan (Versa Drives Pvt. Ltd.)

Report Scope

In this report, the India Electric Fans Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Ceiling Fans

- Table Fans

- Pedestal / Stand Fans

- Wall-mounted Fans

- Exhaust Fans

- Tower Fans

- Others

- By Motor Type

- Induction Motor

- BLDC (Brushless DC) Motor

- By Blade Material

- Plastic

- Aluminium

- Wood

- Metal

- Others

- By Sweep Size

- Below 900mm

- 900mm to 1200mm

- Above 1200mm

- By Star Rating

- 1-2 Star

- 3 Star

- 4 Star

- 5 Star

- By Price Range

- Economy

- Mid-Range

- Premium

- Luxury / Designer

- By Distribution Channel

- Specialty Stores

- Hypermarkets / Supermarkets

- Online / E-commerce

- Multi-Brand Retail

- Direct Sales

- By End-User

- Residential

- Commercial (Hotels, Offices, Restaurants)

- Industrial

- Government & Institutional

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Electric Fans Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic BLDC fan manufacturers, specialty smart and designer fan brands, premium D2C fan players, or niche regional fan installers.

The India Electric Fans Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Motor Type

- By Blade Material

- By Sweep Size

- By Star Rating

- By Price Range

- By Distribution Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Electric Fans Market

- India Electric Fans Market Insights

- Market Dynamics

- Growth Drivers

- Rising temperatures, climate change, and urbanization driving sustained electric fan demand.

- Mandatory BEE star labelling and energy efficiency norms boosting BLDC fan adoption.

- E-commerce growth, D2C brands, PMAY housing scheme, and rural electrification accelerating category penetration.

- Restraints

- Strong unorganized market and counterfeit / cheap imported fan products limiting branded penetration.

- Raw material price volatility for copper, aluminium, steel, and engineering plastics impacting margins.

- Low replacement cycle of 8 to 12 years and high price sensitivity in mass-market segments.

- Opportunities

- Rural India and Tier-III city electrification creating a large untapped electric fan demand base.

- Smart, IoT-enabled, voice-controlled, and energy-efficient BLDC fan solutions opening new premium value pools.

- Designer, decorative, and premium aesthetic ceiling fan adoption supporting next-generation growth.

- Challenges

- Cheap Chinese fan imports and unbranded local assembly limiting organized brand market share.

- Limited consumer awareness of BLDC technology, energy savings, and star rating benefits.

- After-sales service gaps and warranty fulfilment challenges across Tier-II and rural India.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (copper, aluminium, steel, engineering plastics, electronic components)

- Motor & Component Manufacturers (BLDC motors, induction motors, capacitors, blades, regulators)

- Smart Electronics & Controller Suppliers (IoT modules, remote controllers, IR sensors)

- Contract Manufacturers & Original Design Manufacturers (Make-in-India PLI partners)

- Quality Control, R&D & Testing Laboratories (BIS, BEE, IS 374 standards)

- Distributors, Wholesalers, Dealers & Online Aggregators

- Electric Fan Brand Owners (Havells, Crompton, Orient, Bajaj, Usha, Atomberg, Polycab)

- Retailers, Specialty Stores, Hypermarkets, D2C Platforms & Quick-commerce

- Installation, After-Sales Service & Authorized Service Centres

- End-Users (residential households, hotels, offices, factories, schools, hospitals)

- India Electric Fans Market: Regulatory Framework

- India Electric Fans Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Million Units)

- Market Share & Forecast

- By Product Type

- Ceiling Fans

- Table Fans

- Pedestal / Stand Fans

- Wall-mounted Fans

- Exhaust Fans

- Tower Fans

- Others

- By Motor Type

- Induction Motor

- BLDC (Brushless DC) Motor

- By Blade Material

- Plastic

- Aluminium

- Wood

- Metal

- Others

- By Sweep Size

- Below 900mm

- 900mm to 1200mm

- Above 1200mm

- By Star Rating

- 1-2 Star

- 3 Star

- 4 Star

- 5 Star

- By Price Range

- Economy

- Mid-Range

- Premium

- Luxury / Designer

- By Distribution Channel

- Specialty Stores

- Hypermarkets / Supermarkets

- Online / E-commerce

- Multi-Brand Retail

- Direct Sales

- By End-User

- Residential

- Commercial (Hotels, Offices, Restaurants)

- Industrial

- Government & Institutional

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Electric Fans Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Havells India Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- Crompton Greaves Consumer Electricals Limited

- Orient Electric Limited (CK Birla Group)

- Bajaj Electricals Limited

- Usha International Limited

- V-Guard Industries Limited

- Polycab India Limited

- Atomberg Technologies Pvt. Ltd.

- Khaitan Electricals Limited

- Luminous Power Technologies Pvt. Ltd. (Schneider Electric)

- Anchor by Panasonic India

- Surya Roshni Limited

- Almonard Pvt. Ltd.

- GM Modular Pvt. Ltd.

- Superfan (Versa Drives Pvt. Ltd.)

- Other Prominent Players

- Havells India Limited

- By Product Type

- Market Size & Forecast, 2021-2032

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India electric fans market and what is its growth forecast?

Ans: The India electric fans market is valued at USD 2.95 billion in 2025 and is projected to reach USD 5.85 billion by 2032, growing at a CAGR of 10.2%, supported by BLDC adoption, BEE star labelling, and rising summer cooling demand.

2. Which segments are driving demand in the India electric fans market?

Ans: Ceiling fans dominate the India electric fans market with over 75% value share, while BLDC and smart ceiling fans are the fastest growing segments, supported by BEE 2023 star rating norms and aspirational urban consumption.

3. What are the key drivers of growth in the India electric fans market?

Ans: Key drivers include rising temperatures, urbanization, mandatory BEE star labelling, BLDC technology adoption, PMAY housing rollouts, rural electrification, e-commerce expansion, and growing premium designer fan demand across India's electric fans market.

4. Which regions are driving growth in the India electric fans market?

Ans: Uttar Pradesh, Delhi NCR, Maharashtra, Gujarat, Tamil Nadu, and Karnataka lead the India electric fans market, supported by extreme summer temperatures, large household base, PMAY housing rollouts, and strong urban BLDC fan penetration.

5. What are the latest trends in the India electric fans market?

Ans: Latest trends include rapid BLDC motor adoption, smart Wi-Fi-enabled ceiling fans, premium designer aesthetic fans, anti-dust coating technology, voice-controlled appliances, quick-commerce expansion, and Make-in-India PLI scheme manufacturing across India's electric fans market.

Frequently Asked Questions

1. How large is the India electric fans market and what is its growth forecast?

Ans: The India electric fans market is valued at USD 2.95 billion in 2025 and is projected to reach USD 5.85 billion by 2032, growing at a CAGR of 10.2%, supported by BLDC adoption, BEE star labelling, and rising summer cooling demand.

2. Which segments are driving demand in the India electric fans market?

Ans: Ceiling fans dominate the India electric fans market with over 75% value share, while BLDC and smart ceiling fans are the fastest growing segments, supported by BEE 2023 star rating norms and aspirational urban consumption.

3. What are the key drivers of growth in the India electric fans market?

Ans: Key drivers include rising temperatures, urbanization, mandatory BEE star labelling, BLDC technology adoption, PMAY housing rollouts, rural electrification, e-commerce expansion, and growing premium designer fan demand across India's electric fans market.

4. Which regions are driving growth in the India electric fans market?

Ans: Uttar Pradesh, Delhi NCR, Maharashtra, Gujarat, Tamil Nadu, and Karnataka lead the India electric fans market, supported by extreme summer temperatures, large household base, PMAY housing rollouts, and strong urban BLDC fan penetration.

5. What are the latest trends in the India electric fans market?

Ans: Latest trends include rapid BLDC motor adoption, smart Wi-Fi-enabled ceiling fans, premium designer aesthetic fans, anti-dust coating technology, voice-controlled appliances, quick-commerce expansion, and Make-in-India PLI scheme manufacturing across India's electric fans market.