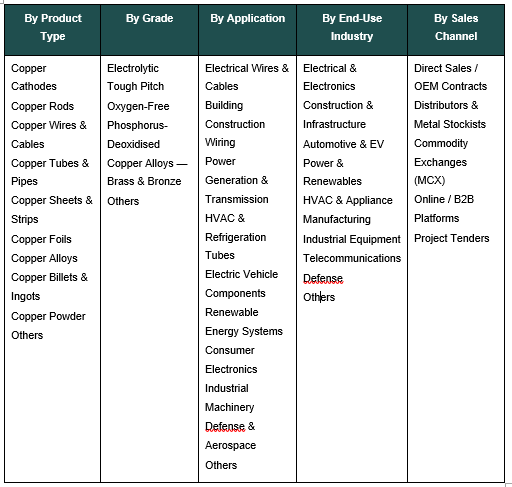

India Copper Market, By Product Type (Copper Cathodes, Copper Rods, Copper Wires & Cables, Copper Tubes & Pipes, Copper Sheets & Strips, Copper Foils, Copper Alloys, Copper Billets & Ingots, Copper Powder, Others); By Form (Solid, Liquid / Molten, Powder, Granular, Wire & Strand); By Grade (Electrolytic Tough Pitch, Oxygen-Free, Phosphorus-Deoxidised, Copper Alloys — Brass & Bronze, Others); By Production Process (Primary / Mined Copper, Secondary / Recycled Copper, Electrolytic Refining); By Application (Electrical Wires & Cables, Building Construction Wiring, Power Generation & Transmission, HVAC & Refrigeration Tubes, Electric Vehicle Components, Renewable Energy Systems, Consumer Electronics, Industrial Machinery, Defense & Aerospace, Others); By End-Use Industry (Electrical & Electronics, Construction & Infrastructure, Automotive & EV, Power & Renewables, HVAC & Appliance Manufacturing, Industrial Equipment, Telecommunications, Defense, Others); By Sales Channel (Direct Sales / OEM Contracts, Distributors & Metal Stockists, Commodity Exchanges (MCX), Online / B2B Platforms, Project Tenders); By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Chemicals & Advanced Materials

- Jan 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Copper Market: EV, Renewables & Electrification Megatrend Drive Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

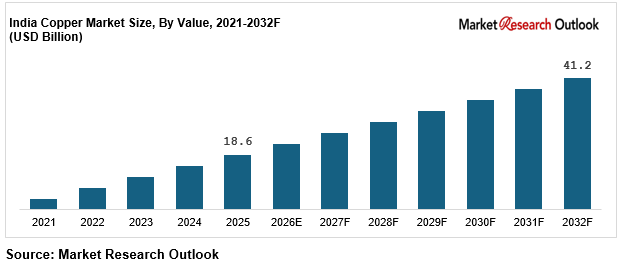

| Market Size (2025) | USD 18.6 Billion |

| CAGR (2026-2032) | 12.0% |

| Leading Segment | Refined Copper / Copper Rods |

| Fastest Growing Segment | Copper for EV & Renewable Energy |

| Market Size (2032) | USD 41.2 Billion |

Source: Market Research Outlook

Market Overview — India Copper Market

The India copper market is expanding at a steady pace, supported by structural growth across electrification, renewable energy, and infrastructure development. Valued at around USD 18.6 billion in 2025, the market is projected to reach nearly USD 41.2 billion by 2032, reflecting a CAGR of about 12.0 percent.

Demand is being led by sectors that are becoming increasingly copper-intensive. Electrical wires and cables continue to account for more than 50 percent of total consumption, while newer segments such as electric vehicles and renewable energy are growing at a much faster pace. For instance, EVs require roughly 3 to 4 times more copper than conventional vehicles, while solar and wind installations use approximately 3 to 4 tonnes of copper per megawatt.

Beyond industrial demand, rising urbanisation and infrastructure expansion are reinforcing baseline consumption. Growth in Tier I and Tier II cities, combined with increasing penetration of HVAC systems and digital infrastructure, is creating consistent demand across applications. At the same time, capacity expansion by domestic smelters and growing adoption of recycled copper are improving supply-side stability, positioning India as a more self-reliant copper ecosystem.

Key Report Takeaways — India Copper Market

- The market is expected to grow from USD 18.6 billion in 2025 to around USD 41.2 billion by 2032, supported by strong demand across electrification and infrastructure.

- Electric vehicle adoption is a key growth driver, with copper consumption per EV ranging between 60 and 85 kilograms.

- Renewable energy expansion is creating incremental demand, with each megawatt of solar or wind capacity requiring 3 to 4 tonnes of copper.

- Domestic smelting capacity expansion and policy support are gradually reducing import dependence, particularly across refined copper.

- Recycled copper currently accounts for nearly 30 to 35 percent of consumption and is expected to increase further over the forecast period.

Key Market Drivers — India Copper Market

Electrification and Renewable Energy Expansion Driving Demand

Electrification and Renewable Energy Expansion Driving Structural Demand

Copper demand in India is increasingly linked to the country’s electrification and energy transition agenda. Electric vehicles require significantly higher copper content, typically ranging between 60 and 85 kilograms per unit, across motors, wiring systems, and charging infrastructure. With EV adoption accelerating at over 30 percent annually, this is creating a strong and sustained demand base.

At the same time, India’s renewable energy capacity is targeted to reach around 500 GW by 2030. Solar and wind installations require approximately 3 to 4 tonnes of copper per megawatt, while transmission infrastructure adds further demand. This combination of transport electrification and clean energy deployment is establishing long-term structural consumption for copper.

Rising Construction, Power Transmission, and HVAC Demand Supporting Core Copper Consumption

The accelerating pace of construction, real estate, and infrastructure development is a major catalyst for the India copper market, with housing demand growing at 9 to 11 percent annually across Tier I and Tier II cities. Premium residential projects, commercial real estate, and data centers increasingly specify copper wiring, copper plumbing, and antimicrobial copper for longevity and safety compliance. Power transmission and distribution (T&D) modernisation, including smart grid build-out and high-voltage DC transmission corridors, is adding substantial copper demand across cables, busbars, and transformers. The rapid expansion of room air-conditioning, where each AC unit uses 2 to 4 kilograms of copper, along with commercial HVAC in hospitals, malls, and metros, is creating additional pull-through demand. Government infrastructure programs including Smart Cities, Bharatmala, and metro rail expansion are further reinforcing structural copper consumption across the India copper market forecast 2032.

Government-Led PLI Support and Domestic Smelting Capacity Expansion Reducing Import Dependence

Domestic copper smelting and refining capacity in India is entering a significant expansion phase, with Adani Group’s Kutch Copper plant commissioning 500,000 tonnes per annum greenfield capacity, Hindalco expanding its Dahej operations, and discussions around the potential revival of Vedanta’s Sterlite Copper facility in Tuticorin. Combined India-focused investment announcements in copper smelting, refining, and downstream fabrication have exceeded USD 4 billion across 2023 to 2025, reflecting strong confidence in long-term India copper market growth. Government support through the Production Linked Incentive (PLI) scheme for advanced chemistry cells, telecom equipment, and white goods, combined with anti-dumping duties on select imports and Quality Control Orders, is creating a favourable environment for domestic capacity expansion. Rising adoption of secondary / recycled copper, currently at around 35 percent of total consumption, is further strengthening supply security and aligning with circular-economy targets across the India copper market.

Key Market Challenges — India Copper Market

LME Copper Price Volatility and Currency Exposure Pressuring Working Capital

Copper, being a globally traded commodity, makes the India copper market highly sensitive to volatility on the London Metal Exchange (LME) and to USD-INR currency movements. LME copper prices have moved in a wide USD 7,500 to USD 10,500 per tonne range over the past 24 months, creating significant working capital pressure, especially for mid-sized fabricators and wire-drawing units. Extended inventory cycles of 45 to 60 days, combined with India’s dependence on imported copper concentrate for primary smelting, further compound margin volatility. This pricing instability makes long-term OEM contracts with EV manufacturers, cable makers, and HVAC producers challenging to structure, pushing leading players to invest in hedging infrastructure, LME-linked pricing clauses, and scrap-based supply diversification across the India copper market.

Heavy Import Dependence for Copper Concentrate and Refined Copper Creating Supply Risk

India remains structurally import-dependent for copper raw materials, with over 90 percent of copper concentrate sourced from overseas mines in Chile, Peru, Indonesia, and Australia, and with refined copper imports meeting a meaningful portion of downstream demand. The prolonged shutdown of Vedanta’s Sterlite Copper Tuticorin plant has tilted India further toward refined copper imports, primarily from Japan, Tanzania, and the UAE. Geopolitical tensions, logistics disruptions, and shifts in global mining capex have exposed domestic cable makers, wire producers, and EV component manufacturers to supply disruption risk. While Adani’s Kutch Copper and Hindalco’s expansion plans are expected to reduce this dependence materially by 2027 to 2030, the India copper market will remain exposed to global concentrate pricing and availability in the near term, making supply security a critical strategic challenge.

Environmental, Pollution Control, and Land Acquisition Challenges for New Smelting Capacity

The India copper market faces significant challenges around environmental clearances, pollution control norms, and land acquisition for new primary smelting and refining capacity. The 2018 shutdown of Vedanta’s Sterlite Copper Tuticorin plant, which previously accounted for nearly 40 percent of India’s primary refined copper output, highlighted the complex interplay between community concerns, environmental regulation, and industrial capacity needs. New smelter projects require rigorous compliance with CPCB standards, emission control, sulphur dioxide capture, effluent management, and rehabilitation commitments, extending commissioning timelines by 18 to 24 months. Smaller downstream fabricators also face tightening compliance around scrap sourcing, e-waste recycling, and occupational health standards, increasing compliance costs by 8 to 12 percent and reshaping the competitive landscape across the India copper market.

Key Market Trends — India Copper Market

Rapid Shift Toward EV-Linked Copper Demand Reshaping the India Copper Market

The India copper market is undergoing a structural shift toward EV-linked copper demand, with electric vehicles, battery packs, charging infrastructure, and traction motors emerging as the fastest-growing demand category. Copper consumption per electric vehicle is 3 to 4 times higher than in internal combustion engine vehicles, with BEVs requiring 60 to 85 kilograms per unit. India’s electric vehicle penetration is expected to cross 30 percent of new sales by 2030, driven by FAME-II, PLI support for advanced chemistry cells, and state-level EV policies. In 2025, OEMs such as Tata Motors, Mahindra Electric, Ola Electric, Ather Energy, and TVS Motor scaled up India-specific EV production, reinforcing structural copper demand across wire, cable, busbar, and specialty alloy categories in the India copper market.

Accelerated Adoption of Secondary / Recycled Copper and Circular-Economy Supply Models

Secondary or recycled copper is playing an increasingly critical role in the India copper market, currently accounting for approximately 35 percent of total copper consumption and expected to grow to over 45 percent by 2032. This shift is driven by rising ESG and sustainability mandates from global OEMs, supply security concerns around concentrate imports, and favourable economics as refined copper prices remain structurally elevated. Leading players including Hindalco’s Birla Copper, Vedanta, and organised scrap processors are expanding recycling capacity, while Extended Producer Responsibility (EPR) norms under e-waste and battery waste management rules are strengthening organised scrap supply. This circular-economy transition is reshaping cost structures and supply chains across the India copper market forecast 2032.

Domestic Capacity Expansion, PLI Support, and Reduced Import Dependence in the India Copper Market

A wave of domestic capacity expansion, supported by government PLI incentives and favourable trade policy, is reshaping the India copper market supply landscape. Adani Group’s Kutch Copper has commissioned 500,000 tonnes per annum greenfield smelter capacity, Hindalco is expanding its Dahej operations, and multiple downstream fabricators are scaling copper rod, wire, and tube production. The PLI scheme for advanced chemistry cells, telecom equipment, and white goods is indirectly accelerating copper demand localisation, while anti-dumping duties and Quality Control Orders (QCOs) are supporting domestic producers. In 2025, combined capacity additions exceeded 1.5 million tonnes per annum of downstream copper output, reinforcing India’s emergence as a competitive copper manufacturing hub and strengthening the India copper market forecast 2032.

Segmental Insights — India Copper Market

By Application — Electrical Wires & Cables Dominate the India Copper Market

The electrical wires and cables segment dominates the India copper market, accounting for an estimated 50 to 55 percent of total copper consumption, driven by construction wiring, power transmission and distribution, and rapidly expanding renewable energy projects. Copper’s superior conductivity, ductility, and thermal performance make it the material of choice for low-voltage wiring, high-voltage cables, and specialty cables used in data centers, EV charging, and solar and wind installations. Leading cable manufacturers including Polycab, KEI Industries, Havells, Finolex Cables, and RR Kabel have scaled capacity in 2024 and 2025 to meet structural demand. Power transmission modernisation, smart grid build-out, and high-voltage DC corridors are further reinforcing the segment’s dominance in the India copper market.

By End-Use Industry — Electrical & Electronics Leads the India Copper Market

Electrical and electronics leads the India copper market end-use landscape, contributing approximately 55 to 60 percent of total consumption, driven by strong demand from cable manufacturing, consumer appliances, transformers, motors, and electronics assembly. Construction and infrastructure follows with 15 to 18 percent share, supported by residential and commercial wiring, plumbing, and HVAC tubes. Automotive and EV, though a smaller base today, is the fastest-growing end-use segment, expected to grow at over 25 percent annually through 2032 as EV adoption accelerates. Power and renewables, along with HVAC and appliance manufacturing, remain critical incremental demand engines, reinforcing copper’s role as a foundational material for India’s electrification economy.

Regional Insights — India Copper Market

Regional analysis of the India copper market shows that West India and South India collectively account for approximately 55 to 60 percent of total copper consumption, driven by the concentration of copper smelting and refining hubs in Gujarat (Hindalco Dahej, Adani Kutch Copper), downstream fabrication clusters in Maharashtra, and strong electrical, cable, and HVAC manufacturing across Tamil Nadu, Karnataka, and Telangana. North India contributes around 20 to 23 percent of demand, led by Delhi NCR, Haryana, Uttar Pradesh, and Rajasthan, supported by cable and wire manufacturing hubs, metro rail expansion, and growing EV and appliance production. East and Central India together account for 18 to 22 percent, supported by Odisha’s integrated copper capacity, industrial corridor development, and rising demand in cities such as Kolkata, Bhubaneswar, Raipur, and Indore. In 2025, capacity additions by Adani Kutch Copper in Gujarat and Hindalco Birla Copper in Dahej reinforced regional supply hubs, supporting closer collaboration with cable makers, EV OEMs, and HVAC manufacturers across the India copper market.

Recent Developments — India Copper Market

- The India copper market has witnessed strong momentum in greenfield smelting and refining capacity expansion during 2024 and 2025. Adani Group’s Kutch Copper commissioned its 500,000 tonnes per annum greenfield smelter, making it one of the largest single-location copper complexes in the country. Hindalco Industries expanded its Birla Copper operations at Dahej with additional downstream copper rod and wire capacity, while Vedanta continued discussions around the potential revival of its Sterlite Copper facility, reflecting strong confidence in long-term India copper market growth.

- Downstream fabricators and global OEMs have deepened India sourcing of copper-intensive products, with cable manufacturers including Polycab, KEI Industries, and Havells scaling long-term supply contracts with domestic smelters in 2025. EV OEMs such as Tata Motors, Mahindra Electric, Ola Electric, and Ather Energy scaled India-specific production, driving demand for copper busbars, wire harnesses, and specialty alloys. Renewable energy EPC players and solar module manufacturers also standardised copper-based interconnections, reinforcing demand across premium copper applications.

- Secondary and recycled copper has gained strong traction in the India copper market. In 2025, organised scrap processors and recyclers expanded capacity, supported by Extended Producer Responsibility (EPR) norms under e-waste and battery waste management rules. Strategic tie-ups between Indian copper companies and global OEMs are positioning India as an emerging copper manufacturing and recycling hub, strengthening long-term competitive positioning in the India copper market forecast 2032.

Key Market Players — India Copper Market

- Hindalco Industries Limited (Birla Copper)

- Vedanta Limited (Sterlite Copper)

- Adani Group (Kutch Copper)

- Hindustan Copper Limited

- Polycab India Limited

- KEI Industries Limited

- Havells India Limited

- Finolex Cables Limited

- RR Kabel Limited

- Mehta Tubes Limited

- Multimetals Ltd.

- Arcotech Ltd.

Report Scope

In this report, the India Copper Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Copper Cathodes

- Copper Rods

- Copper Wires & Cables

- Copper Tubes & Pipes

- Copper Sheets & Strips

- Copper Foils

- Copper Alloys

- Copper Billets & Ingots

- Copper Powder

- Others

- By Form

- Solid

- Liquid / Molten

- Powder

- Granular

- Wire & Strand

- By Grade

- Electrolytic Tough Pitch

- Oxygen-Free

- Phosphorus-Deoxidised

- Copper Alloys — Brass & Bronze

- Others

- By Production Process

- Primary / Mined Copper

- Secondary / Recycled Copper

- Electrolytic Refining

- By Application

- Electrical Wires & Cables

- Building Construction Wiring

- Power Generation & Transmission

- HVAC & Refrigeration Tubes

- Electric Vehicle Components

- Renewable Energy Systems

- Consumer Electronics

- Industrial Machinery

- Defense & Aerospace

- Others

- By End-Use Industry

- Electrical & Electronics

- Construction & Infrastructure

- Automotive & EV

- Power & Renewables

- HVAC & Appliance Manufacturing

- Industrial Equipment

- Telecommunications

- Defense

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Metal Stockists

- Commodity Exchanges (MCX)

- Online / B2B Platforms

- Project Tenders

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Copper Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic copper smelters, downstream fabricators, global entrants, or niche segment leaders.

The India Copper Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021–2032

- By Product Type

- By Application

- By End-Use Industry

- By Production Process

- By Sales Channel

- By Region

- Analyst Recommendations

- Market Overview, 2021–2032

- Geopolitical Impact on India Copper Market

- India Copper Market Insights

- Market Dynamics

- Growth Drivers

- Accelerated EV adoption and renewable energy build-out driving structural copper demand across India.

- Rising construction, power transmission, and HVAC demand supporting core copper consumption across India.

- Government-led PLI support and domestic smelting capacity expansion reducing copper import dependence.

- Restraints

- LME copper price volatility and currency exposure pressuring working capital across the copper value chain.

- Heavy import dependence for copper concentrate and refined copper creating long-term supply risk.

- Environmental clearance, pollution control, and land acquisition challenges constraining new smelting capacity.

- Opportunities

- Massive copper demand opportunity from EV battery, motor, and charging infrastructure build-out through 2032.

- Rapid scale-up of secondary / recycled copper processing aligned with circular-economy and ESG targets.

- Emerging copper demand from green hydrogen electrolysers, 5G telecom, and data center infrastructure build-out.

- Challenges

- Intense price-led competition between organised smelters and unorganised copper fabricators compressing margins.

- Shortage of skilled metallurgists, electro-refining technicians, and extrusion specialists limiting scale-up speed.

- Stringent BIS, CPCB, and export compliance requirements raising quality, environmental, and investment standards.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Dynamics

- Industry Value Chain & Entry Points

- Copper Mines & Concentrate Suppliers (domestic and imported from Chile, Peru, Indonesia, Australia)

- Copper Smelters & Refineries (Hindalco Dahej, Adani Kutch, Hindustan Copper, Sterlite Copper)

- Secondary / Recycled Copper Processors (organised scrap, e-waste, battery recycling)

- Copper Rod, Billet & Ingot Manufacturers

- Downstream Fabrication (wires, cables, tubes, sheets, foils, alloys)

- Quality Control & Certification (BIS, ISO 9001, IS 191, ASTM, CPCB, export QCOs)

- Distributors, Stockists & Metal Exchanges (MCX, commodity markets)

- OEM Direct Supply (cable makers, EV OEMs, HVAC, appliance, electronics, defense)

- Installation & Fabrication Contractors (power, telecom, construction, MEP)

- End-Use Industries & Recycling Loop (electrical, automotive, construction, renewables, telecom)

- India Copper Market: Regulatory Framework

- India Copper Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (‘000 Tons)

- Market Share & Forecast

- By Product Type

- Copper Cathodes

- Copper Rods

- Copper Wires & Cables

- Copper Tubes & Pipes

- Copper Sheets & Strips

- Copper Foils

- Copper Alloys

- Copper Billets & Ingots

- Copper Powder

- Others

- By Form

- Solid

- Liquid / Molten

- Powder

- Granular

- Wire & Strand

- By Grade

- Electrolytic Tough Pitch

- Oxygen-Free

- Phosphorus-Deoxidised

- Copper Alloys — Brass & Bronze

- Others

- By Production Process

- Primary / Mined Copper

- Secondary / Recycled Copper

- Electrolytic Refining

- By Application

- Electrical Wires & Cables

- Building Construction Wiring

- Power Generation & Transmission

- HVAC & Refrigeration Tubes

- Electric Vehicle Components

- Renewable Energy Systems

- Consumer Electronics

- Industrial Machinery

- Defense & Aerospace

- Others

- By End-Use Industry

- Electrical & Electronics

- Construction & Infrastructure

- Automotive & EV

- Power & Renewables

- HVAC & Appliance Manufacturing

- Industrial Equipment

- Telecommunications

- Defense

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Metal Stockists

- Commodity Exchanges (MCX)

- Online / B2B Platforms

- Project Tenders

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Market Size & Forecast, 2021-2032

- Competitive Landscape

- India Copper Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Hindalco Industries Limited (Birla Copper)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Hindalco Industries Limited (Birla Copper)

*(Same Data Pointers Will Be Provided for The Below Companies)

- Vedanta Limited (Sterlite Copper)

- Adani Group (Kutch Copper)

- Hindustan Copper Limited

- Polycab India Limited

- KEI Industries Limited

- Havells India Limited

- Finolex Cables Limited

- RR Kabel Limited

- Mehta Tubes Limited

- Multimetals Ltd.

- Arcotech Ltd.

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India copper market and what is its growth forecast?

Ans: The India copper market size is valued at USD 18.6 billion in 2025 and is projected to reach USD 41.2 billion by 2032, growing at a CAGR of around 12.0 percent. This strong India copper market growth is driven by accelerated electric vehicle adoption, rapid renewable energy capacity additions, rising construction and HVAC demand, and government-led PLI support for domestic smelting and refining capacity. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India copper market?

Ans: The India copper market segmentation shows that electrical wires and cables dominate with approximately 50 to 55 percent market share, supported by construction wiring, power transmission, and renewable energy projects. Copper for EV and renewable energy applications is the fastest-growing segment, expected to grow at over 25 percent annually through 2032. The report breaks down demand across product types, forms, grades, production processes, applications, end-use industries, and sales channels, helping businesses identify where growth is accelerating across the India copper market.

3. What are the key drivers of growth in the India copper market?

Ans: Key India copper market drivers include accelerated electric vehicle adoption, rapid build-out of renewable energy capacity targeting 500 GW by 2030, rising construction and real estate demand, and domestic smelting capacity expansion by Hindalco, Adani Group, and Hindustan Copper. Government support through the PLI scheme, FAME-II, Green Hydrogen Mission, and power transmission modernisation are further catalysing copper demand. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends, enabling better strategic decision-making across the India copper market.

4. Which regions are driving growth in the India copper market?

Ans: Regional analysis of the India copper market shows that West and South India together account for nearly 55 to 60 percent of total demand, driven by copper smelting hubs in Gujarat and strong downstream manufacturing in Maharashtra, Tamil Nadu, Karnataka, and Telangana. North India contributes around 20 to 23 percent of demand, supported by cable manufacturing clusters and metro rail expansion. East and Central India together account for 18 to 22 percent, led by Odisha’s integrated capacity and industrial corridor development. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India copper market?

Ans: The latest India copper market trends include rapid growth of EV-linked copper demand, accelerated adoption of secondary and recycled copper aligned with circular-economy targets, and significant domestic smelting capacity expansion supported by PLI and favourable trade policy. EV-linked copper demand is expected to grow 5 to 6 times by 2032, while recycled copper share is projected to rise from 35 percent to over 45 percent of total consumption. The report provides detailed insights into emerging trends, innovation pipelines, and future demand shifts, helping businesses stay ahead of competition and capture new growth opportunities in the India copper market.

Frequently Asked Questions

1. How large is the India copper market and what is its growth forecast?

Ans: The India copper market size is valued at USD 18.6 billion in 2025 and is projected to reach USD 41.2 billion by 2032, growing at a CAGR of around 12.0 percent. This strong India copper market growth is driven by accelerated electric vehicle adoption, rapid renewable energy capacity additions, rising construction and HVAC demand, and government-led PLI support for domestic smelting and refining capacity. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India copper market?

Ans: The India copper market segmentation shows that electrical wires and cables dominate with approximately 50 to 55 percent market share, supported by construction wiring, power transmission, and renewable energy projects. Copper for EV and renewable energy applications is the fastest-growing segment, expected to grow at over 25 percent annually through 2032. The report breaks down demand across product types, forms, grades, production processes, applications, end-use industries, and sales channels, helping businesses identify where growth is accelerating across the India copper market.

3. What are the key drivers of growth in the India copper market?

Ans: Key India copper market drivers include accelerated electric vehicle adoption, rapid build-out of renewable energy capacity targeting 500 GW by 2030, rising construction and real estate demand, and domestic smelting capacity expansion by Hindalco, Adani Group, and Hindustan Copper. Government support through the PLI scheme, FAME-II, Green Hydrogen Mission, and power transmission modernisation are further catalysing copper demand. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends, enabling better strategic decision-making across the India copper market.

4. Which regions are driving growth in the India copper market?

Ans: Regional analysis of the India copper market shows that West and South India together account for nearly 55 to 60 percent of total demand, driven by copper smelting hubs in Gujarat and strong downstream manufacturing in Maharashtra, Tamil Nadu, Karnataka, and Telangana. North India contributes around 20 to 23 percent of demand, supported by cable manufacturing clusters and metro rail expansion. East and Central India together account for 18 to 22 percent, led by Odisha’s integrated capacity and industrial corridor development. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India copper market?

Ans: The latest India copper market trends include rapid growth of EV-linked copper demand, accelerated adoption of secondary and recycled copper aligned with circular-economy targets, and significant domestic smelting capacity expansion supported by PLI and favourable trade policy. EV-linked copper demand is expected to grow 5 to 6 times by 2032, while recycled copper share is projected to rise from 35 percent to over 45 percent of total consumption. The report provides detailed insights into emerging trends, innovation pipelines, and future demand shifts, helping businesses stay ahead of competition and capture new growth opportunities in the India copper market.