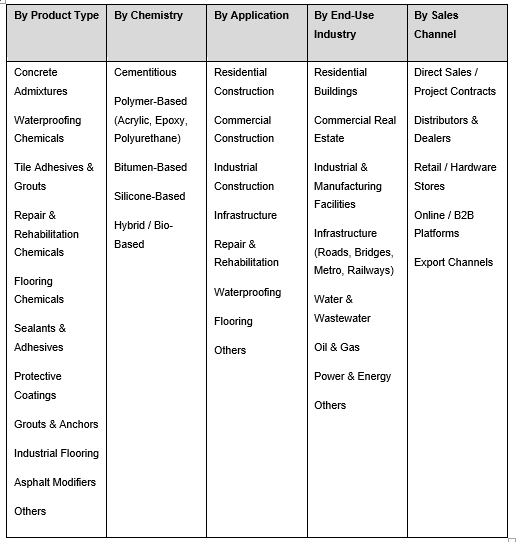

India Construction Chemicals Market, By Product Type (Concrete Admixtures, Waterproofing Chemicals, Tile Adhesives & Grouts, Repair & Rehabilitation Chemicals, Flooring Chemicals, Sealants & Adhesives, Protective Coatings, Grouts & Anchors, Industrial Flooring, Asphalt Modifiers, Others); By Chemistry (Cementitious, Polymer-Based (Acrylic, Epoxy, Polyurethane), Bitumen-Based, Silicone-Based, Hybrid / Bio-Based); By Application (Residential Construction, Commercial Construction, Industrial Construction, Infrastructure, Repair & Rehabilitation, Waterproofing, Flooring, Others); By Form (Liquid, Powder, Paste / Gel, Pre-Mixed / Ready-to-Use); By End-Use Industry (Residential Buildings, Commercial Real Estate, Industrial & Manufacturing Facilities, Infrastructure (Roads, Bridges, Metro, Railways), Water & Wastewater, Oil & Gas, Power & Energy, Others); By Sales Channel (Direct Sales / Project Contracts, Distributors & Dealers, Retail / Hardware Stores, Online / B2B Platforms, Export Channels); By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Chemicals & Advanced Materials

- Apr 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Construction Chemicals Market: Infrastructure Boom & Green Building Shift Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

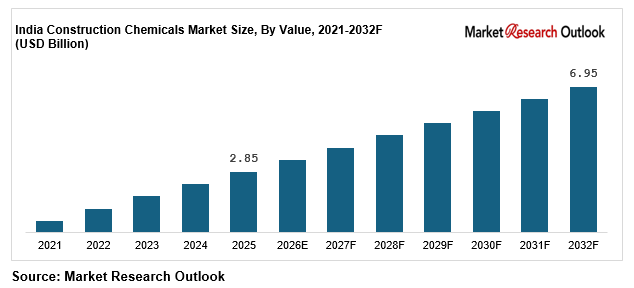

| Market Size (2025) | USD 2.85 Billion |

| CAGR (2026-2032) | 13.6% |

| Leading Segment | Concrete Admixtures |

| Fastest Growing Segment | Waterproofing Chemicals & Tile Adhesives |

| Market Size (2032) | USD 6.95 Billion |

Source: Market Research Outlook

The India construction chemicals market size is expanding rapidly, supported by strong growth in real estate and infrastructure, rising demand for waterproofing chemicals and tile adhesives, and the shift toward high-performance polymer-modified and green construction chemicals. Valued at USD 2.85 billion in 2025 and expected to reach USD 6.95 billion by 2032 at a CAGR of 13.6 %, the India construction chemicals market growth is driven by increasing adoption across builders, developers, EPC contractors, and repair and rehabilitation projects.

Concrete admixtures continue to lead the India construction chemicals market, while waterproofing chemicals and tile adhesives are emerging as the fastest-growing segments due to higher usage in residential and infrastructure applications. Growing adoption of green building standards such as IGBC and LEED, along with CPCB VOC regulations and ESG commitments, is reshaping product demand toward sustainable and low-VOC construction chemicals.

Global players including BASF, Sika, Fosroc, Mapei, and Saint-Gobain Weber are expanding India-focused manufacturing and technical capabilities, while domestic companies such as Pidilite Industries, MYK Laticrete, Asian Paints, Berger Paints, Ardex Endura, and Kryton Buildmat are strengthening their presence across waterproofing, tile adhesives, and repair chemicals. This is positioning the India construction chemicals market as a high-growth, innovation-driven, and sustainability-focused segment within the broader construction ecosystem.

Key Report Takeaways — India Construction Chemicals Market

- The India construction chemicals market is expected to grow from USD 2.85 billion in 2025 to USD 6.95 billion by 2032, at a CAGR of 13.6 percent, driven by rapid infrastructure development, urbanisation, and rising demand for high-performance construction chemicals.

- Concrete admixtures dominate the India construction chemicals market with a 30 to 33 percent share, supported by strong usage in ready-mix concrete, precast construction, and large-scale residential and infrastructure projects.

- Waterproofing chemicals and tile adhesives are the fastest-growing segments in the India construction chemicals market, expanding at 15 to 18 percent annually as premium housing, green building standards, and modern construction practices gain traction.

- Growth in real estate and infrastructure, led by developers such as DLF, Godrej Properties, and Prestige Estates, along with EPC players like Larsen & Toubro and Tata Projects, is driving consistent demand for construction chemicals across applications.

- Global companies including BASF, Sika, Fosroc, and Mapei are increasing investments in India-focused manufacturing and training, strengthening innovation and supporting long-term growth in the India construction chemicals market.

Key Market Drivers — India Construction Chemicals Market

Rapid Urbanisation and Infrastructure Investment Driving India Construction Chemicals Market Growth

The India construction chemicals market is growing strongly, supported by rapid urbanisation and large-scale government infrastructure programs such as Smart Cities Mission, Bharatmala, PMAY, and metro rail expansion. These initiatives are significantly increasing construction activity and driving demand for construction chemicals across residential, commercial, and infrastructure projects.

Construction contributes around 9 percent to India’s GDP, with construction chemicals becoming essential inputs in modern building practices. Per capita consumption remains low at nearly USD 2 compared to USD 15 to 25 in developed markets, highlighting strong long-term growth potential for the India construction chemicals market.

Leading companies such as Pidilite, BASF, Sika, Fosroc, MYK Laticrete, and Saint-Gobain Weber are expanding capacity and strengthening distribution, supporting rising demand for concrete admixtures, waterproofing chemicals, and tile adhesives across India.

Shift Toward High-Performance and Sustainable Construction Chemicals in India

The India construction chemicals market is witnessing a strong shift toward high-performance polymer-modified, green, and sustainable construction chemicals, growing at 15 to 18 percent annually and outpacing conventional cement-based solutions.

Stricter green building standards such as IGBC and LEED, along with CPCB VOC norms and ESG commitments, are driving demand for low-VOC, durable, and application-specific construction chemicals across residential, commercial, and infrastructure projects. Polymer-modified construction chemicals offer significantly higher durability and lower emissions, making them the preferred choice for premium and long-life construction.

Global companies including BASF, Sika, Fosroc, and Mapei, along with leading domestic manufacturers, are expanding polymer-modified and green construction chemical portfolios, reinforcing the shift toward sustainable and performance-driven solutions in the India construction chemicals market.

Premium Real Estate and Repair Activity Driving India Construction Chemicals Market

The India construction chemicals market is gaining strong momentum from the expansion of premium real estate, rising repair and rehabilitation activity, and the adoption of modern construction practices. The real estate sector is growing at around 10 to 12 percent annually, while repair and rehabilitation is expanding at 14 to 16 percent, creating sustained demand for construction chemicals.

Construction chemicals such as waterproofing membranes, tile adhesives, concrete admixtures, epoxy flooring, sealants, and protective coatings are becoming essential across residential, commercial, and infrastructure projects. Demand is being driven by premium housing, metro rail, Smart Cities Mission, Bharatmala, and the need to upgrade aging infrastructure.

Leading developers including DLF, Godrej Properties, and Lodha, along with EPC contractors such as Larsen & Toubro and Tata Projects, are increasingly specifying high-performance construction chemicals. This trend, combined with sector formalisation and infrastructure investment, is strengthening long-term growth in the India construction chemicals market.

Key Market Challenges — India Construction Chemicals Market

Raw Material Price Volatility — India Construction Chemicals Market Challenge

The India construction chemicals market faces significant pressure from raw material price volatility, particularly in cement, polymers, epoxy resins, bitumen, and specialty additives, which account for nearly 55 to 70 percent of total input costs. These materials are closely linked to crude oil and global petrochemical cycles, leading to frequent cost fluctuations.

Crude oil movements in the USD 70 to USD 95 per barrel range have resulted in 20 to 30 percent swings in polymer and bitumen prices, impacting margins and making long-term pricing contracts difficult for construction chemical manufacturers.

Dependence on imported raw materials from China, Germany, the US, Japan, and South Korea further increases exposure to supply disruptions and currency risks. In response, companies in the India construction chemicals market are focusing on backward integration, long-term sourcing agreements, and formulation improvements to manage cost volatility.

Import Dependence — India Construction Chemicals Market Challenge

The India construction chemicals market remains heavily dependent on imports for specialty polymers, intermediates, and high-performance additives, with nearly 55 to 65 percent of demand met through imports from China, Germany, the US, Japan, and South Korea.

Critical product categories such as epoxy resins, acrylic polymers, polyurethane systems, silicone sealants, and advanced concrete admixtures continue to see high import intensity, exposing manufacturers to supply disruptions and extended lead times of up to 8 to 14 weeks.

Geopolitical risks and global supply chain shifts have further highlighted vulnerabilities in sourcing. While companies such as Pidilite, BASF India, Asian Paints, and Berger Paints are expanding domestic capabilities, reducing import dependence will take time, making supply security a key near-term challenge in the India construction chemicals market.

Environmental Compliance and VOC Regulations — India Construction Chemicals Market Challenge

The India construction chemicals market is facing increasing pressure from environmental compliance, VOC regulations, and green building mandates. Strict CPCB norms, including wastewater treatment and Zero Liquid Discharge requirements, are raising compliance costs by 7 to 12 percent for manufacturers.

Green building certifications such as IGBC, LEED, and GRIHA are further driving demand for low-VOC, sustainable, and compliant construction chemicals across residential, commercial, and infrastructure projects.

At the same time, ESG commitments from builders, developers, and EPC contractors are pushing stricter sustainability requirements across the value chain. While this adds operational complexity, it also favours organised, R&D-driven players, strengthening quality standards in the India construction chemicals market.

Key Market Trends — India Construction Chemicals Market

Adoption of Waterproofing and Polymer-Modified Solutions — India Construction Chemicals Market

The India construction chemicals market is witnessing rapid adoption of waterproofing chemicals, tile adhesives, and polymer-modified construction chemicals, with these segments growing at 15 to 18 percent annually, outpacing traditional cement-based solutions.

Stricter green building standards such as IGBC and LEED, along with CPCB VOC regulations and ESG commitments, are driving demand for high-performance, durable, and low-emission construction chemicals across residential, commercial, and infrastructure projects.

Polymer-modified construction chemicals based on acrylics, epoxies, and polyurethanes are gaining traction as builders prioritise longer lifecycle performance and reduced maintenance costs. Global companies including BASF, Sika, Fosroc, and Mapei are expanding waterproofing and tile adhesive portfolios in India, reinforcing this structural shift in the India construction chemicals market.

Capacity Expansion — India Construction Chemicals Market

The India construction chemicals market is witnessing strong capacity expansion, with global and domestic players investing over USD 800 million between 2023 and 2025 in construction chemicals and polymer-modified solutions.

Global companies such as BASF, Sika, Fosroc, Mapei, and MC-Bauchemie are expanding manufacturing across waterproofing chemicals, tile adhesives, and concrete admixtures, while domestic players including Pidilite Industries, MYK Laticrete, Asian Paints, Berger Paints, and Ardex Endura are scaling capacity across key product segments.

This expansion is aligned with rising demand from infrastructure and real estate projects under PMAY, Smart Cities Mission, Bharatmala, and metro rail development, along with increased activity from developers and EPC contractors. These trends are strengthening supply capabilities and supporting long-term growth in the India construction chemicals market.

Infrastructure, Repair and DIY Demand — India Construction Chemicals Market

The India construction chemicals market is seeing strong growth from infrastructure projects, repair and rehabilitation activity, and DIY retail, which together are expected to account for over 40 percent of total demand by 2032.

Infrastructure construction chemicals are growing at 13 to 15 percent annually, while repair and rehabilitation and DIY retail segments are expanding at 14 to 16 percent and 16 to 20 percent respectively. Demand is driven by applications such as highways, bridges, metro projects, structural repair, crack injection, waterproofing, and tile fixing.

Companies including Pidilite, BASF, Sika, Fosroc, MYK Laticrete, Asian Paints, and Saint-Gobain Weber are expanding product portfolios and launching applicator-friendly and DIY-focused solutions. This trend is strengthening both project-led and retail-led growth in the India construction chemicals market.

Segmental Insights — India Construction Chemicals Market

By Application — India Construction Chemicals Market

The India construction chemicals market is led by residential and commercial construction, which together account for 55 to 60 percent of total demand, driven by strong growth in housing, commercial real estate, and urban infrastructure. High demand for waterproofing chemicals, tile adhesives, concrete admixtures, flooring systems, and protective coatings continues to support this segment.

Within the India construction chemicals market, concrete admixtures and waterproofing chemicals remain the most widely used products across residential and commercial projects, while polymer-modified construction chemicals and green construction chemicals are rapidly gaining share due to durability and compliance requirements.

Infrastructure construction contributes 20 to 23 percent of the India construction chemicals market, supported by highways, metro rail, and smart city projects, while repair and rehabilitation accounts for 12 to 15 percent, driven by aging buildings and asset maintenance. Industrial construction contributes 8 to 10 percent, with demand linked to manufacturing and warehousing expansion.

Leading developers such as DLF, Godrej Properties, Prestige Estates, and Lodha are increasing adoption of high-performance construction chemicals, reinforcing the dominance of residential and commercial applications in the India construction chemicals market.

By Product Type — India Construction Chemicals Market

Concrete admixtures dominate the India construction chemicals market, accounting for 30 to 33 percent of total consumption, driven by strong demand from ready-mix concrete, precast construction, and large-scale infrastructure projects. Waterproofing chemicals hold a 22 to 25 percent share, followed by tile adhesives and grouts at 16 to 18 percent, and repair and rehabilitation chemicals at 10 to 12 percent.

Within the India construction chemicals market, waterproofing chemicals, tile adhesives, and polymer-modified flooring systems are the fastest-growing segments, expanding at 15 to 18 percent annually. This growth is supported by premium real estate development, increasing adoption of green building standards, rising DIY retail demand, and the shift toward modern construction practices.

The increasing use of high-performance construction chemicals across residential, commercial, and industrial projects is driving demand for durable, low-maintenance, and application-specific solutions, strengthening product innovation and value growth in the India construction chemicals market.

Regional Insights — India Construction Chemicals Market

The India construction chemicals market is concentrated in West and South India, which together account for 58 to 62 percent of total production and consumption, driven by strong manufacturing clusters in Maharashtra, Gujarat, Karnataka, and Tamil Nadu, along with high construction activity in cities such as Mumbai, Pune, Bengaluru, Hyderabad, and Chennai.

North India contributes 22 to 25 percent of the India construction chemicals market, supported by demand from Delhi NCR, Haryana, Uttar Pradesh, and Rajasthan, with growth driven by residential and commercial real estate, metro expansion, and increasing adoption of waterproofing chemicals and tile adhesives.

East and Central India account for 14 to 18 percent of demand, led by infrastructure development and emerging real estate markets in Kolkata, Odisha, Jharkhand, Bihar, and Madhya Pradesh.

Capacity expansions by BASF, Sika, Pidilite, Mapei, MYK Laticrete, and Fosroc are strengthening regional supply chains and enabling faster adoption of construction chemicals across builders, developers, and EPC contractors, reinforcing growth in the India construction chemicals market.

Recent Developments — India Construction Chemicals Market

- The India construction chemicals market has witnessed strong momentum in capacity expansion and polymer-modified product innovation during 2024 and 2025. BASF expanded its Mangalore and Thane construction chemical facilities, Sika commissioned additional tile adhesives and waterproofing capacity at Pune, Fosroc strengthened concrete admixtures at Taloja, Mapei expanded its Andheri plant, and MC-Bauchemie scaled specialty concrete admixture capacity. Domestic players including Pidilite Industries (Dr. Fixit), MYK Laticrete, Asian Paints (Smartcare), Berger Paints (Home Shield), Ardex Endura, Saint-Gobain Weber, and Kryton Buildmat announced capacity additions for waterproofing, tile adhesives, and specialty construction chemicals, reinforcing India as a globally competitive construction chemicals manufacturing hub.

- Downstream builders, developers, and EPC contractors have deepened India sourcing of construction chemicals, with DLF, Godrej Properties, Prestige Estates, Lodha, Oberoi Realty, Brigade Group, Sobha, Larsen & Toubro, Shapoorji Pallonji, and Tata Projects scaling long-term supply contracts with domestic and global construction chemical producers in 2025. New infrastructure projects under Bharatmala, Smart Cities Mission, PMAY, and metro rail drove further structural construction chemical demand. DIY retail channels including homecentres, hardware chains, and online B2B platforms also expanded construction chemical visibility, reinforcing downstream linkage across the India construction chemicals market.

- Sustainability-led innovation has gained strong traction in the India construction chemicals market. In 2025, global majors including BASF, Sika, Fosroc, Mapei, MC-Bauchemie, and Saint-Gobain Weber launched expanded low-VOC, polymer-modified, and bio-based construction chemical portfolios targeted at Indian builders, developers, and EPC customers. Strategic partnerships between construction chemical producers, builders, and EPC contractors are positioning India as an emerging hub for sustainable construction chemistries, strengthening long-term competitive positioning in the India construction chemicals market forecast 2032.

Key Market Players — India Construction Chemicals Market

- Pidilite Industries Limited (Dr. Fixit)

- BASF India Limited

- Sika India Pvt. Ltd.

- MYK Laticrete India Pvt. Ltd.

- MC-Bauchemie (India) Pvt. Ltd.

- Fosroc Chemicals (India) Pvt. Ltd.

- Mapei Construction Products India Pvt. Ltd.

- Asian Paints Limited (Smartcare)

- Berger Paints India Limited (Home Shield)

- Saint-Gobain Weber India Pvt. Ltd.

- Ardex Endura India Pvt. Ltd.

- Kryton Buildmat Co. Pvt. Ltd.

- CICO Technologies Limited

- Choksey Chemicals Pvt. Ltd.

Report Scope

In this report, the India Construction Chemicals Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Concrete Admixtures

- Waterproofing Chemicals

- Tile Adhesives & Grouts

- Repair & Rehabilitation Chemicals

- Flooring Chemicals

- Sealants & Adhesives

- Protective Coatings

- Grouts & Anchors

- Industrial Flooring

- Asphalt Modifiers

- Others

- By Chemistry

- Cementitious

- Polymer-Based (Acrylic, Epoxy, Polyurethane)

- Bitumen-Based

- Silicone-Based

- Hybrid / Bio-Based

- By Application

- Residential Construction

- Commercial Construction

- Industrial Construction

- Infrastructure

- Repair & Rehabilitation

- Waterproofing

- Flooring

- Others

- By Form

- Liquid

- Powder

- Paste / Gel

- Pre-Mixed / Ready-to-Use

- By End-Use Industry

- Residential Buildings

- Commercial Real Estate

- Industrial & Manufacturing Facilities

- Infrastructure (Roads, Bridges, Metro, Railways)

- Water & Wastewater

- Oil & Gas

- Power & Energy

- Others

- By Sales Channel

- Direct Sales / Project Contracts

- Distributors & Dealers

- Retail / Hardware Stores

- Online / B2B Platforms

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Construction Chemicals Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic construction chemical producers, green building specialists, global entrants, or niche segment leaders.

The India Construction Chemicals Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021–2032

- By Product Type

- By Application

- By End-Use Industry

- By Chemistry

- By Sales Channel

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Construction Chemicals Market

- India Construction Chemicals Market Insights

- Market Dynamics

- Growth Drivers

- Rapid urbanization and government-led infrastructure investment under Smart Cities, Bharatmala, PMAY, and metro rail programs driving construction chemicals consumption.

- Growing adoption of waterproofing, tile adhesives, and repair chemicals driven by premium real estate and modern construction practices.

- Structural shift toward high-performance, sustainable, and green construction chemistries aligned with IGBC, LEED, and ESG mandates.

- Restraints

- Raw material price volatility linked to cement, polymers, bitumen, and specialty chemicals pressuring producer margins.

- Heavy import dependence for specialty chemicals, polymer intermediates, and high-performance additives creating supply risk.

- Environmental compliance, VOC regulations, and tightening green building mandates raising compliance costs.

- Opportunities

- Rapid scale-up of waterproofing, tile adhesives, and repair chemicals aligned with premium housing and commercial real estate growth.

- High-growth demand from infrastructure projects including highways, metro rail, Smart Cities, PMAY, and airport expansions.

- Emerging opportunity in green and bio-based construction chemicals aligned with IGBC, LEED, and global sustainability mandates.

- Challenges

- Intense price-led competition between global majors and domestic producers compressing margins.

- Shortage of skilled applicators, formulation scientists, and field engineers limiting scale-up speed of new capacity.

- Fragmented retail distribution and informal sector presence creating quality and pricing complexity.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Material Feedstock (cement, polymers, bitumen, specialty chemicals, additives, pigments)

- Specialty Chemical & Polymer Intermediate Producers (acrylics, epoxies, polyurethanes, silicones, SBR latex)

- Bio-Based Feedstock Producers (renewable polymers, green additives, sustainable fillers)

- Construction Chemical Formulation & Blending Operations (batch, continuous, ready-mix)

- Quality Control, R&D & Application Laboratories (BIS, IS codes, IGBC, LEED ecolabels)

- Distributors, Dealers & B2B Marketplaces

- Downstream Applicators (waterproofing contractors, tile fixers, repair specialists, flooring contractors)

- Brand Owners & Manufacturers (Pidilite, BASF, Sika, MYK Laticrete, Fosroc, Mapei)

- Project Channels (builders, developers, EPC contractors, government tenders, DIY retail)

- End-Use Segments (residential, commercial, industrial, infrastructure, repair & rehabilitation)

- India Construction Chemicals Market: Regulatory Framework

- India Construction Chemicals Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (‘000 Tons)

- Market Share & Forecast

- By Product Type

- Concrete Admixtures

- Waterproofing Chemicals

- Tile Adhesives & Grouts

- Repair & Rehabilitation Chemicals

- Flooring Chemicals

- Sealants & Adhesives

- Protective Coatings

- Grouts & Anchors

- Industrial Flooring

- Asphalt Modifiers

- Others

- By Chemistry

- Cementitious

- Polymer-Based (Acrylic, Epoxy, Polyurethane)

- Bitumen-Based

- Silicone-Based

- Hybrid / Bio-Based

- By Application

- Residential Construction

- Commercial Construction

- Industrial Construction

- Infrastructure

- Repair & Rehabilitation

- Waterproofing

- Flooring

- Others

- By Form

- Liquid

- Powder

- Paste / Gel

- Pre-Mixed / Ready-to-Use

- By End-Use Industry

- Residential Buildings

- Commercial Real Estate

- Industrial & Manufacturing Facilities

- Infrastructure (Roads, Bridges, Metro, Railways)

- Water & Wastewater

- Oil & Gas

- Power & Energy

- Others

- By Sales Channel

- Direct Sales / Project Contracts

- Distributors & Dealers

- Retail / Hardware Stores

- Online / B2B Platforms

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Construction Chemicals Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Pidilite Industries Limited (Dr. Fixit)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Pidilite Industries Limited (Dr. Fixit)

- By Product Type

- Market Size & Forecast, 2021-2032

*(Same Data Pointers Will Be Provided for The Below Companies)

- BASF India Limited

- Sika India Pvt. Ltd.

- MYK Laticrete India Pvt. Ltd.

- MC-Bauchemie (India) Pvt. Ltd.

- Fosroc Chemicals (India) Pvt. Ltd.

- Mapei Construction Products India Pvt. Ltd.

- Asian Paints Limited (Smartcare)

- Berger Paints India Limited (Home Shield)

- Saint-Gobain Weber India Pvt. Ltd.

- Ardex Endura India Pvt. Ltd.

- Kryton Buildmat Co. Pvt. Ltd.

- CICO Technologies Limited

- Choksey Chemicals Pvt. Ltd.

- Other Prominent Players

** Financial information in case of non-listed companies will be provided as per availability

*** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable