India Branded Sugar Market, By Product Type (White Refined Sugar, Brown Sugar, Raw Sugar, Organic Sugar, Icing Sugar, Jaggery & Jaggery Powder, Others); By Packaging Type (Pouches, Bags, Jars, Sachets, Bulk Packaging, Others); By Application (Household Consumption, Food Processing Industry, Beverages Industry, Confectionery & Bakery, Foodservice/HoReCa, Others); By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Traditional Retail/Kirana Stores, Online Platforms, Others); By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Food, Beverage & Nutrition

- Apr 2026

- Pages 120

- Report Format: pdf

- Report Price: $2500 USD

India Branded Sugar Market, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

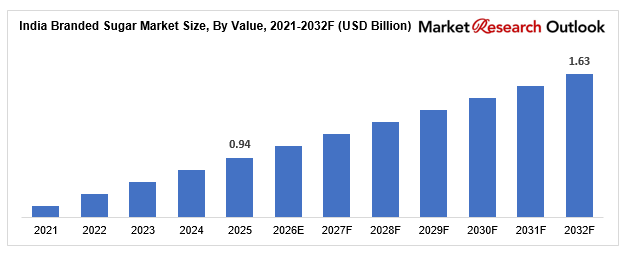

| Market Size (2025) | USD 0.94 Billion |

| CAGR (2026-2032) | 9.56% |

| Leading Segment | White / Refined Sugar |

| Fastest Growing Segment | Organic Sugar, Jaggery-based / Khandsari Sugar |

| Market Size (2032) | USD 1.63 Billion |

Market Overview

The India Branded Sugar market has transitioned from a specialized dietary niche into a commercially significant USD 1.63 Billion industrial segment by the end of the 2032 strategic horizon. Having established a baseline valuation of USD 0.94 Billion in 2025, the market is currently expanding at a robust and consistent CAGR of 9.56%. The growth is occurring because the market has transitioned from selling unbranded loose sugar through mandis to selling certified hygienic packaged sugar through branded products. Urbanization together with health awareness and organized retail formats has developed new consumer preferences that now define sugar consumption patterns throughout India.

White / Refined Sugar remains the leading market product which serves as the primary kitchen essential because it can be used in all types of drinks and cooking and packaged food items. However, Organic Sugar and Jaggery-based / Khandsari Sugar have become the most rapidly expanding market segments because consumers prefer natural sweeteners that contain no chemical additives and have been processed at the lowest level. The urban population in India shows growing interest in wellness which leads them to choose these alternatives because they think these products offer better health benefits than refined sugar. India’s high per capita sugar consumption together with its development of official retail supply chains functions as the main driver for this USD 8.6 billion estimate. In contrast to previous decades when sugar functioned as a basic need item that people bought in bulk, modern consumers now demand proof that sugar products maintain their natural purity and consistent grain size while being free from any form of tampering.

The competitive landscape is witnessing gradual consolidation because major fast-moving consumer goods companies and sugar manufacturers are establishing their own branded products to increase profits while developing direct connections with customers. The authorities now exercise tighter control over labeling requirements because they demand standardized labeling and sulfur content information and established quality assessment methods. The market will reach its mature state by 2032 which will lead to the development of new fortified and specialty sugar products that include low-GI sugar and mineral-infused jaggery blends. The market will maintain its growth rate for the next ten years because of increased digital commerce adoption and the expansion of businesses into Tier-2 and Tier-3 cities.

Market Drivers

The Trust Shift: From Loose to Branded Consumption

The Indian sugar market is undergoing a fundamental trust transition. The category used to be dominated by loose unpackaged sugar which people purchased from local kirana stores but now consumers strongly prefer branded products which provide hygienic standards and accurate weight measurements and uniform quality assurance. People in urban and semi-urban areas select branded sugar because they are worried about adulteration and contamination. The consumer trust assurance is strengthened by aggressive branding methods and new packaging designs and quality certification programs.

The Wellness Wave: Rise of Natural and Alternative Sweeteners

Health consciousness is changing sugar consumption patterns throughout India. The market currently prefers refined sugar yet there exists increasing demand for natural sweeteners which includes jaggery and khandsari and organic sugar. The products are viewed as more natural because they contain fewer artificial ingredients and their health benefits match the current trend of clean-label products and traditional food restoration. The rising incidence of diabetes and other lifestyle diseases drives consumers to reduce their refined sugar consumption while trying new healthier alternatives that create growth in the premium market segment.

Market Challenges

The Commodity Trap: Thin Margins and Price Sensitivity

The Indian market continues to treat sugar as a price-sensitive commodity despite its branding efforts. The existence of major cooperative companies together with government-controlled price systems creates ongoing challenges for businesses to maintain their profit margins. Consumers in rural areas who belong to lower-income groups tend to choose products based on their price rather than brand recognition which creates challenges for companies to achieve high product prices. The “commodity trap” restricts market profits while it prevents fast premium market development in mass market products.

Supply Volatility: Dependence on Agricultural Cycles

The sugar industry depends on sugarcane production, which government policies, monsoon patterns, and water availability determine. Sugar prices and supply stability experience direct effects from changes in crop yield. Branded sugar companies face challenges in maintaining consistent pricing and supply chains because of export restrictions and minimum selling price controls and ethanol blending policies.

Segmental Analysis

White and refined sugar products serve as the mainstay of Indian branded sugar market because they function as essential items for both homes and industrial facilities. The product becomes the standard selection for widespread use because of its consistent crystal dimensions and simple dissolving properties and low cost. Urban customers who want healthier food options that require less processing are increasingly choosing Brown Sugar and Raw and Unrefined Sugar products.

By nature, Conventional sugar dominates the market due to its affordability and large-scale availability. The Organic and Natural and Minimally Processed product categories show increased market growth because consumers prefer clean-label products. The packaging market shows high demand for Pouches and Sachets together with small Bags that weigh 1 kilogram because these products meet daily household needs while Bulk and Institutional Packaging serves B2B markets in food processing and HoReCa establishments.

Regional Analysis

The Indian branded sugar market exhibits a regionally diversified consumption pattern, with North India leading production and consumption due to its extensive sugarcane cultivation belt, particularly in Uttar Pradesh and Haryana. The region functions as a supply center while serving as a market that exhibits high demand which exists because of traditional dietary practices that use sugar as a primary ingredient. The Maharashtra and Gujarat states of West India create an advanced and structured market which has developed strong cooperative sugar companies alongside widespread availability of branded items. The area emerges as the main driver of premiumization trends because its residents have achieved higher income levels and urbanization rates continue to rise.

Recent Developments

- Strategic Expansion by FMCG Players: The leading FMCG companies developed their product lines to include branded sugar products while using their current distribution systems to gain market share in the organized market.

- Regulatory Strengthening by FSSAI: Updated quality and labeling standards have created better product transparency through their requirements of sulfur content and grain size and purity measurements, which enables consumers to trust branded sugar products more.

- E-commerce Penetration: E-commerce platforms may have played a significant role in the search of an increased range of premium organic sugar, particularly in the middle-levels of these cities.

Key Market Players

- Balrampur Chini Mills Ltd.

- Triveni Engineering & Industries Ltd.

- DCM Shriram Ltd.

- EID Parry (India) Ltd.

- Shree Renuka Sugars Ltd.

- Bajaj Hindusthan Sugar Ltd.

- Dhampur Sugar Mills Ltd.

- Uttam Sugar Mills Ltd.

- Mawana Sugars Ltd.

- NSL Sugars Ltd.

Segmentation

- Product Type

- White / Refined Sugar

- Brown Sugar

- Raw / Unrefined Sugar

- Organic Sugar

- Powdered / Icing Sugar

- Jaggery-based / Khandsari Sugar

- Others

- Nature

- Conventional

- Organic

- Natural / Minimally Processed

- Packaging Type

- Pouches & Sachets

- Bags (1 kg, 5 kg, 10 kg)

- Boxes & Cartons

- Bulk / Institutional Packaging

- Others

- Price Range

- Economy / Mass Market

- Mid-range

- Premium & Super Premium

- End Use Industry

- Household / Retail Consumers

- Food & Beverage Manufacturers

- Bakery & Confectionery

- Foodservice & HoReCa

- Pharmaceuticals & Nutraceuticals

- Others

- Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores & Kirana Stores

- Wholesale & Cash-and-Carry

- Online Retail / E-commerce

- Foodservice / Institutional Sales

- Region

- East India

- West India

- North India

- South India

Table of Contents

- Executive Summary

- Research Methodology

- Report Scope

- Market Definition

- Inclusions & Exclusions

- Research Methodology

- India Branded Sugar Market Overview

- Market Evolution in India

- Industry Value Chain Overview

- Ecosystem Mapping

- Pricing Analysis Overview

- Market Dynamics

- Drivers

- Challenges

- Opportunities

- Emerging Trends

- Market Attractiveness Index

- Consumer Behaviour Analysis

- Buying Patterns

- Price Sensitivity

- Urban vs Tier 2 Demand

- Policy & Regulatory Landscape

- India Branded Sugar Market Outlook

- Market Size & Forecast, 2021-2032

- By Value

- By Volume

- Market Share & Forecast by Product Type

- White / Refined Sugar

- Brown Sugar

- Raw / Unrefined Sugar

- Organic Sugar

- Powdered / Icing Sugar

- Jaggery-based / Khandsari Sugar

- Others

- Market Share & Forecast by Nature

- Conventional

- Organic

- Natural / Minimally Processed

- Market Share & Forecast by Packaging Type

- Pouches & Sachets

- Bags (1 kg, 5 kg, 10 kg)

- Boxes & Cartons

- Bulk / Institutional Packaging

- Others

- Market Share & Forecast by Price Range

- Economy / Mass Market

- Mid-range

- Premium & Super Premium

- Market Share & Forecast by End Use Industry

- Household / Retail Consumers

- Food & Beverage Manufacturers

- Bakery & Confectionery

- Foodservice & HoReCa

- Pharmaceuticals & Nutraceuticals

- Others

- Market Share & Forecast by Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores & Kirana Stores

- Wholesale & Cash-and-Carry

- Online Retail / E-commerce

- Foodservice / Institutional Sales

- Market Share & Forecast by Region

- East India

- West India

- North India

- South India

- Market Size & Forecast, 2021-2032

- Competitive Landscape

- Market Share Analysis

- Competitive Benchmarking

- Company Profiles

- Product Portfolio Comparison

- Strategic Developments

- Strategic Recommendations

- Growth Strategies for New Entrants

- Expansion Strategies for Existing Players

- Investment Opportunities

Frequently Asked Questions

1. What is the projected market size of the India Branded Sugar Market in 2025?

Ans: The India Branded Sugar market is estimated to be valued at approximately USD 0.94 Billion in 2025.

2. What is the expected growth rate (CAGR) of the India Branded Sugar Market during the forecast period?

Ans: The market is expected to exhibit a robust CAGR of 9.56% during the forecast period between 2026 and 2032.

3. What is the forecast value of the India Branded Sugar Market by 2032?

Ans: By the end of the strategic horizon in 2032, the India Branded Sugar market is projected to reach a valuation of approximately USD 1.63 Billion.

4. What are the major factors driving the growth of the India Branded Sugar Market?

Ans: The growth is occurring because the market has transitioned from selling unbranded loose sugar through mandis to selling certified hygienic packaged sugar through branded products.

5. Name the key players operating in the India Branded Sugar Market.

Ans: Prominent players shaping the Indian landscape include Balrampur Chini Mills Ltd., Triveni Engineering & Industries Ltd., DCM Shriram Ltd., EID Parry (India) Ltd., Shree Renuka Sugars Ltd., Bajaj Hindusthan Sugar Ltd., Dhampur Sugar Mills Ltd., Uttam Sugar Mills Ltd., Mawana Sugars Ltd., NSL Sugars Ltd., and other prominent players.

6. Which regions/cities are expected to lead the growth in the India Branded Sugar Market?

Ans: The Indian branded sugar market exhibits a regionally diversified consumption pattern, with North India leading production and consumption due to its extensive sugarcane cultivation belt, particularly in Uttar Pradesh and Haryana.

Frequently Asked Questions

1. What is the projected market size of the India Branded Sugar Market in 2025?

Ans: The India Branded Sugar market is estimated to be valued at approximately USD 0.94 Billion in 2025.

2. What is the expected growth rate (CAGR) of the India Branded Sugar Market during the forecast period?

Ans: The market is expected to exhibit a robust CAGR of 9.56% during the forecast period between 2026 and 2032.

3. What is the forecast value of the India Branded Sugar Market by 2032?

Ans: By the end of the strategic horizon in 2032, the India Branded Sugar market is projected to reach a valuation of approximately USD 1.63 Billion.

4. What are the major factors driving the growth of the India Branded Sugar Market?

Ans: The growth is occurring because the market has transitioned from selling unbranded loose sugar through mandis to selling certified hygienic packaged sugar through branded products.

5. Name the key players operating in the India Branded Sugar Market.

Ans: Prominent players shaping the Indian landscape include Balrampur Chini Mills Ltd., Triveni Engineering & Industries Ltd., DCM Shriram Ltd., EID Parry (India) Ltd., Shree Renuka Sugars Ltd., Bajaj Hindusthan Sugar Ltd., Dhampur Sugar Mills Ltd., Uttam Sugar Mills Ltd., Mawana Sugars Ltd., NSL Sugars Ltd., and other prominent players.

6. Which regions/cities are expected to lead the growth in the India Branded Sugar Market?

Ans: The Indian branded sugar market exhibits a regionally diversified consumption pattern, with North India leading production and consumption due to its extensive sugarcane cultivation belt, particularly in Uttar Pradesh and Haryana.