India Baby Food Market, By Product Type (Infant Milk Formula, Baby Cereals, Dried Baby Food, Prepared Baby Food, Ready-to-Feed Baby Food, Baby Snacks & Finger Foods, Others); By Category (Organic, Conventional); By Age Group (0 to 6 Months, 6 to 12 Months, 12 to 24 Months, Above 24 Months); By Packaging Type (Tin Cans, Pouches, Glass Jars, Cartons & Tetra Packs, Plastic Bottles); By Product Format (Powder, Liquid, Solid / Semi-Solid); By Distribution Channel (Supermarkets & Hypermarkets, Pharmacies & Drug Stores, Convenience Stores, Online Retail, Specialty Baby Stores); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Food, Beverage & Nutrition

- May 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Baby Food Market: Urbanisation, Working Mothers and Premiumisation Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

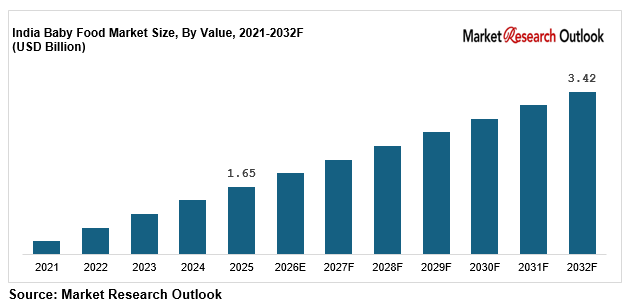

| Market Size (2025) | USD 1.65 Billion |

| CAGR (2026-2032) | 10.9% |

| Leading Segment | Infant Milk Formula (Powder Format) |

| Fastest Growing Segment | Organic & Millet-Based Baby Food |

| Market Size (2032) | USD 3.42 Billion |

Source: Market Research Outlook

Market Overview: India Baby Food Market

India baby food market size is witnessing rapid expansion, driven by rising urbanisation, increasing dual-income households, growing women workforce participation, expanding nuclear family structures, accelerated e-commerce penetration, and major capacity additions by global and Indian infant nutrition majors. Valued at USD 1.65 billion in 2025 and projected to reach USD 3.42 billion by 2032, growing at a CAGR of 10.9%, the India baby food market growth is being fuelled by strong demand for infant milk formula, rising adoption of fortified baby cereals, growing interest in organic and millet-based weaning food, and rising premium product uptake across metro and Tier II cities. Infant milk formula leads consumption, while the organic and millet-based baby food segment is emerging as the fastest growing category. Tightening FSSAI infant food regulations, rising parental focus on clean-label nutrition, and growing paediatric outreach are reshaping the supply landscape. As global majors including Nestle India, Danone, Abbott, Mead Johnson, and Hindustan Unilever expand their fortified baby food portfolios, and emerging Indian brands such as Slurrp Farm, Happa Foods, Early Foods, Timios, and Pristine Organics scale millet-based and organic baby food, the India baby food market is evolving into a science-led, consumer-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Baby Food Market

- India baby food market size is projected to grow from USD 1.65 billion in 2025 to USD 3.42 billion by 2032, registering a strong CAGR of 10.9%, driven by accelerated urban-led infant formula adoption, rising fortified baby cereal demand, and the structural shift toward packaged, science-based infant nutrition.

- Infant milk formula dominates the India baby food market, accounting for over 60% of total value in 2025, driven by rising demand for stage-specific formula in 0 to 6 months and 6 to 12 months age groups, urbanisation, and growing acceptance of formula feeding among working mothers in metro and Tier I cities.

- Organic and millet-based baby food is emerging as the fastest growing segment in the India baby food market, expected to grow at 15% to 18% annually as parental focus on clean-label nutrition, food safety concerns, and rising premium positioning by Slurrp Farm, Happa Foods, Early Foods, and Timios reshape sourcing strategies.

- Online retail and D2C platforms have become the fastest-growing distribution channel for the India baby food market, with e-commerce expected to grow at 17% to 20% annually, supported by Amazon, Flipkart, FirstCry, and BigBasket expanding baby nutrition assortments and subscription delivery models.

- Rising investments by global majors such as Nestle India, Danone, Abbott, Mead Johnson, and Hindustan Unilever in HMO-fortified infant formula, A2 milk-based products, and fortified baby cereals, alongside capacity expansion by Indian players, are strengthening domestic supply and supporting the India baby food market forecast 2032.

Key Market Drivers: India Baby Food Market

Rising Urbanisation, Dual-Income Households, and Growing Women Workforce Driving Convenient Baby Food Demand

Growth in the India baby food market is being driven by rapid urbanisation, with over 35% of India’s population now residing in urban areas, alongside rising female workforce participation, which reached 41.7% in FY24 according to the Periodic Labour Force Survey. Nuclear family structures, expanding dual-income households, and longer working hours among urban mothers are accelerating shifts away from traditional home-cooked weaning food toward packaged infant milk formula, fortified baby cereals, and ready-to-feed baby food. India records nearly 25 million annual births, accounting for almost 17% of global births, creating a large addressable base for the India baby food market. Convenience-led consumption among young parents, growing acceptance of stage-specific baby food, and rising disposable incomes of INR 1.5 lakh to 4 lakh per household across metro and Tier I cities are creating strong structural pull-through demand across the India baby food market.

Increasing Parental Awareness of Infant Nutrition and Growing Preference for Fortified and Premium Baby Food

India baby food market is benefiting from sustained improvement in parental awareness of infant nutrition, with nearly 68% to 70% of urban parents now actively evaluating nutritional labels, micronutrient fortification, and ingredient quality before selecting baby food, according to industry consumer surveys. Paediatric outreach by Nestle India, Danone, Abbott, and Mead Johnson, alongside growing online infant nutrition content, has accelerated premium baby food adoption across the 0 to 24 months age group. Demand is rising for fortified infant formula with HMOs, DHA, ARA, prebiotics, and probiotics, while baby cereals enriched with iron, zinc, vitamin D, and millet bases are gaining strong traction. Premium baby food now accounts for an estimated 35% to 40% of urban consumption, with average household monthly spend on packaged baby food ranging between INR 1,500 and INR 4,500. Rising health-conscious purchasing behaviour continues to support price competitiveness across the India baby food market.

E-commerce Expansion, Rising Disposable Incomes, and Tier II / Tier III City Penetration Accelerating Market Reach

Rapid e-commerce expansion is a major catalyst for the India baby food market, with online channels projected to grow at 17% to 20% annually through 2032. Online platforms including Amazon, Flipkart, FirstCry, BigBasket, and brand-owned D2C portals have made stage-specific infant milk formula, fortified baby cereals, organic baby purees, and millet-based baby snacks accessible across over 19,000 PIN codes. According to industry data, online retail contributed over 15% to 17% of India baby food market sales in 2025, up from below 5% in 2019. Rising household disposable incomes, growing Tier II and Tier III city consumption (where average urban household incomes have crossed INR 80,000 monthly), and aggressive digital marketing by Nestle, Danone, Slurrp Farm, Happa Foods, and Timios are deepening market penetration. Combined with subscription-based delivery and paediatrician-led product recommendations, e-commerce is structurally expanding the India baby food market across all major age groups through 2032.

Key Market Challenges: India Baby Food Market

Strong Cultural Preference for Breastfeeding and IMS Act Restrictions Limiting Marketing of Infant Milk Substitutes

India baby food market continues to face challenges around strong cultural and policy support for breastfeeding, with the World Health Organization and Indian Academy of Paediatrics recommending exclusive breastfeeding for the first 6 months and continued breastfeeding up to 24 months. India’s exclusive breastfeeding rate among 0 to 6 month infants stands at around 64%, according to the National Family Health Survey-5, structurally limiting the addressable infant milk formula market. The Infant Milk Substitutes, Feeding Bottles, and Infant Foods (IMS) Act, 1992 imposes strict restrictions on advertising, promotion, and incentivising the use of infant milk substitutes for children under 24 months, with violations attracting imprisonment of up to 3 years. FSSAI has further reinforced compliance, including on e-commerce platforms, restricting surrogate marketing of infant nutrition products. While these regulations protect infant health, they limit brand-building flexibility for baby food companies operating across the India baby food market.

Premium Pricing of Organic and Imported Baby Food Limiting Affordability for Lower-Income Households

India baby food market faces structural complexity from premium pricing of organic, imported, and specialty baby food products, with typical organic baby food priced 40% to 70% higher than conventional alternatives. Average pricing for a 400 gram pack of premium infant milk formula ranges between INR 750 and INR 1,400, while organic baby cereals and purees are priced between INR 350 and INR 600 per pack. Per-capita disposable income limitations across India’s lower-middle and lower-income households, which constitute over 60% of total population, continue to restrict deep adoption of premium baby food products. Differential pricing between metro, Tier II, and Tier III cities creates affordability gaps for players such as Nestle India, Danone, and Abbott operating pan-India. While entry-price baby food products under INR 300 are gaining traction, premium pricing remains a near-term challenge for the India baby food market.

Stringent FSSAI Regulations and Infant Food Labelling Norms Creating Compliance Complexity

India baby food market faces practical constraints around stringent FSSAI regulations, infant food labelling norms, and quality compliance. The Food Safety and Standards (Foods for Infant Nutrition) Regulations, 2020, alongside the IMS Act, 1992, mandate detailed labelling on ingredients, nutritional information, mother’s milk superiority statements, and prohibition of misleading claims. Recurring scrutiny on added sugar in infant cereals, contamination concerns, and quality recalls have raised compliance pressure on baby food manufacturers, with key brands facing periodic regulatory action. Approval timelines for new infant food products range between 6 and 12 months, while imported baby food faces strict customs clearance and Basic Customs Duty exposure. Domestic clean-label baby food brands such as Slurrp Farm, Early Foods, Happa Foods, Timios, and Pristine Organics, while well positioned to capture trust-led demand, must also navigate ongoing compliance overheads across the India baby food market.

Key Market Trends: India Baby Food Market

Rapid Adoption of Organic, Clean-Label, and Millet-Based Baby Food in India

India baby food market is undergoing a clear product shift toward organic, clean-label, and millet-based baby food, with these advanced categories expected to capture over 25% to 28% of new baby food launches by 2027. Organic baby food, free from synthetic pesticides, artificial preservatives, and added sugar, is growing at 15% to 18% annually, while millet-based baby food using ragi, jowar, bajra, and foxtail millet is gaining strong traction among urban paediatric-aware parents. Domestic clean-label baby food brands including Slurrp Farm, Happa Foods, Early Foods, Timios, and Pristine Organics have scaled organic and millet-based product portfolios through 2024 and 2025, supported by Government of India’s millet promotion policies and the International Year of Millets framework. Global majors such as Nestle, Danone, and Mead Johnson are also expanding clean-label and reduced-sugar baby food variants in India. This product transition is reinforcing the India baby food market forecast 2032 across both metro and Tier II city categories.

Growth of E-commerce, D2C Platforms, and Subscription-Based Baby Food Delivery

A clear shift toward e-commerce, D2C platforms, and subscription-based delivery is reshaping the India baby food market, particularly in the urban premium segment. Online retail has emerged as the fastest growing distribution channel, growing at 17% to 20% annually, with Amazon, Flipkart, FirstCry, BigBasket, and brand-owned D2C portals together accounting for over 15% to 17% of total India baby food market sales in 2025. Leading brands have built combined direct-to-consumer subscription portfolios serving over 5 lakh households nationally. Online aggregators and digital platforms such as FirstCry parenting community, paediatrician-led recommendation platforms, and EMI-linked baby care subscriptions are also reducing customer acquisition costs and accelerating baby food adoption across both metro and Tier II city segments of the India baby food market. Brands such as Slurrp Farm, Happa Foods, Timios, Early Foods, and Pristine Organics are scaling D2C operations rapidly.

Capacity Expansion by Domestic and Global Baby Food Manufacturers

A wave of domestic and global capacity expansion is reshaping the India baby food market supply landscape. Combined India-focused capital expenditure announcements in infant nutrition, baby cereal, and ready-to-feed baby food capacity exceeded USD 600 million across 2023 to 2025. Nestle India expanded Cerelac manufacturing with no-refined-sugar variants in October 2024, Danone India launched AptaGrow toddler nutrition in January 2024, Abbott scaled Similac and PediaSure offerings, and Mead Johnson expanded Enfamil and Enfagrow portfolios. Indian players including Amul (GCMMF) strengthened Amulspray infant milk substitute, while Slurrp Farm, Happa Foods, Timios, Early Foods, and Pristine Organics scaled millet-based and organic baby food production. FSSAI compliance reforms, alongside government support for organic farming under the National Programme for Organic Production (NPOP), have structurally favoured domestic supply. Combined with rising urbanisation driving infant formula demand and clean-label baby food scaling rapidly, these developments are reinforcing the India baby food market forecast 2032 across the entire value chain.

Segmental Insights: India Baby Food Market

By Product Type: Infant Milk Formula Dominates the India Baby Food Market

Infant milk formula segment dominates the India baby food market, accounting for an estimated 60% to 62% of total market value, driven by rapid urbanisation, rising working mothers, growing acceptance of stage-specific formula, and aggressive product innovation in HMO, DHA, and A2 milk-based formula. Powder-format infant formula is the dominant technology within this segment, with stage 1 (0 to 6 months) and stage 2 (6 to 12 months) capturing over 75% of formula sales. Baby cereals contribute another 18% to 20% of demand, driven by Nestle Cerelac, Amulspray, and millet-based weaning options from Slurrp Farm and Happa Foods. Ready-to-feed baby food, baby snacks, and finger foods together account for 12% to 14%, led by urban convenience-oriented consumption. In 2025, leading baby food players including Nestle India, Danone, Abbott, Mead Johnson, and Hindustan Unilever scaled up premium and fortified baby food deployment under FSSAI compliance frameworks, reinforcing segment dominance in the India baby food market.

By Category: Conventional Leads While Organic Grows Fastest

Conventional baby food leads the India baby food market category landscape, accounting for approximately 88% to 90% of total baby food sales, driven by mass-market affordability, wider availability through general trade, and deep brand recognition of Nestle, Danone, Abbott, and Amul. Organic baby food is the fastest growing category within the India baby food market, expanding at 15% to 18% annually, driven by rising parental focus on clean-label, pesticide-free, and minimally processed infant nutrition. Organic baby food currently accounts for 10% to 12% of the market, with this share expected to cross 18% by 2032 in metro and Tier I cities. Leading domestic clean-label players including Slurrp Farm, Happa Foods, Early Foods, Timios, and Pristine Organics have aligned product portfolios to this category, while global majors are also expanding organic baby food variants, driving high-quality product adoption across the India baby food market.

Regional Insights: India Baby Food Market

Regional analysis of the India baby food market shows that West India and North India collectively account for approximately 55% to 58% of total baby food consumption, driven by Maharashtra (Mumbai, Pune metropolitan belt), Gujarat (Ahmedabad, Surat), Delhi NCR, Punjab, Haryana, and Uttar Pradesh urban clusters, supported by high urbanisation rates, strong dual-income households, and aggressive distribution by Nestle India, Danone, and Abbott. South India contributes around 25% to 28% of demand, led by Karnataka, Tamil Nadu, Telangana, and Kerala, supported by premium baby food adoption in IT-driven urban clusters around Bengaluru, Chennai, Hyderabad, and Kochi. Central and East India together account for 14% to 17% of demand, supported by Madhya Pradesh, Chhattisgarh, West Bengal, and Odisha, where Tier II city baby food adoption is accelerating through e-commerce. In 2025, distribution expansion by Nestle India across Tamil Nadu and Karnataka, Danone in Maharashtra and Gujarat, Abbott across Delhi NCR and Punjab, and Slurrp Farm and Happa Foods through D2C across pan-India reinforced regional supply hubs, supporting closer execution of premium and clean-label baby food projects across the India baby food market.

Recent Developments: India Baby Food Market

- India baby food market witnessed strong momentum in product launches and capacity expansion during 2024 and 2025. India added over USD 200 million in new baby food product launches in calendar year 2025, representing a strong increase from 2024. Online retail penetration in baby food crossed 17% by mid-2025, while urban premium baby food adoption grew at 14% to 16% annually, with the infant milk formula segment accounting for 60% to 62% of new launches. Cumulative urban baby food penetration in India is projected to reach 28% to 32% of urban infant households by FY27 from 22% in FY25, growing at an average 12% to 14% annually.

- Domestic and global baby food manufacturers have deepened India-focused capacity expansion. In 2024, Nestle SA launched new no-refined-sugar Cerelac variants in October, Danone India launched AptaGrow toddler nutrition in January with 100% milk protein, calcium, prebiotics, vitamin A, C, D, iron, folic acid, and iodine. In 2025, Abbott expanded Similac and PediaSure portfolios, Mead Johnson scaled Enfamil and Enfagrow ranges, Amul strengthened Amulspray distribution, and Slurrp Farm, Happa Foods, Timios, Early Foods, and Pristine Organics expanded millet-based and organic baby food production. These developments are strengthening domestic supply and supporting the India baby food market forecast 2032.

- Online retail and D2C momentum has gained strong traction in the India baby food market. In 2025, leading online and D2C players including Amazon, Flipkart, FirstCry, BigBasket, and brand-owned platforms expanded baby food assortments and subscription delivery models. Strategic partnerships between domestic baby food manufacturers, online aggregators, paediatric communities, and influencer-led parenting platforms are positioning India as one of the most actively scaling baby food markets globally, strengthening long-term competitive positioning in the India baby food market forecast 2032.

Key Market Players: India Baby Food Market

- Nestle India Limited

- Danone India Pvt. Ltd. (Nutricia)

- Abbott India Limited

- Mead Johnson Nutrition India (Reckitt Benckiser Group plc)

- Hindustan Unilever Limited

- Amway India Enterprises Pvt. Ltd.

- Raptakos, Brett & Co. Ltd.

- Gujarat Cooperative Milk Marketing Federation Ltd. (Amul)

- Wholesum Foods Pvt. Ltd. (Slurrp Farm)

- Early Foods Pvt. Ltd.

- Happa Foods Pvt. Ltd.

- Timios Nutrition Pvt. Ltd.

- Pristine Organics Pvt. Ltd.

Report Scope

In this report, the India Baby Food Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Infant Milk Formula

- Baby Cereals

- Dried Baby Food

- Prepared Baby Food / Purees

- Ready-to-Feed Baby Food

- Baby Snacks & Finger Foods

- Others

- By Category

- Organic

- Conventional

- By Age Group

- 0 to 6 Months

- 6 to 12 Months

- 12 to 24 Months

- Above 24 Months

- By Packaging Type

- Tin Cans

- Pouches

- Glass Jars

- Cartons & Tetra Packs

- Plastic Bottles

- By Product Format

- Powder

- Liquid

- Solid / Semi-Solid

- By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Convenience Stores & Kirana

- Online Retail / E-commerce

- Specialty Baby Stores

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Baby Food Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic organic and millet-based baby food brands, specialty toddler nutrition firms, D2C-model players, or niche regional baby food brands.

The India Baby Food Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Category

- By Age Group

- By Distribution Channel

- By Packaging Type

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Baby Food Market

- India Baby Food Market Insights

- Market Dynamics

- Growth Drivers

- Rising urbanisation, dual-income households, and growing women workforce driving demand for convenient baby food.

- Increasing parental awareness of infant nutrition and growing preference for fortified and premium baby food products.

- E-commerce expansion, rising disposable incomes, and Tier II and Tier III city penetration accelerating market reach.

- Restraints

- Strong cultural preference for breastfeeding and IMS Act restrictions limiting marketing of infant milk substitutes.

- Premium pricing of organic and imported baby food limiting affordability across lower-income consumer segments.

- Stringent FSSAI regulations and infant food labelling norms creating compliance complexity for manufacturers.

- Opportunities

- Rising demand for organic, clean-label, and millet-based baby food creating premium product opportunity pools.

- E-commerce, D2C platforms, and subscription-based baby food delivery expanding national distribution reach.

- Functional baby food with HMOs, probiotics, DHA, and ARA fortification opening next-generation growth opportunities.

- Challenges

- Persistent quality and contamination concerns affecting consumer trust across leading baby food brands.

- Limited cold chain and last-mile distribution infrastructure restricting penetration in rural and semi-urban India.

- Counterfeit infant formula and unregulated local baby food brands creating market integrity risks.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (dairy milk, cereals, fruits, vegetables, millets, vitamins, minerals, prebiotics)

- Ingredient Processors & Nutritional Premix Manufacturers (whey, lactose, DHA, ARA, HMOs, probiotics)

- Baby Food Manufacturers (infant formula, baby cereals, purees, snacks, ready-to-feed)

- Packaging & Cold Chain Solution Providers (aseptic packs, pouches, jars, tetra cartons)

- Quality Control, R&D & Testing Laboratories (FSSAI, BIS, Codex Alimentarius standards)

- Distributors, Dealers & Online Aggregators (B2B and B2C platforms)

- Modern Trade & General Trade Retailers (supermarkets, pharmacies, kirana stores)

- Brand Owners & Baby Nutrition Companies (Nestle, Danone, Abbott, Reckitt, Amul, Slurrp Farm)

- E-commerce & D2C Platforms (Amazon, Flipkart, FirstCry, BigBasket, brand-owned platforms)

- End-Users (parents, infants, toddlers, hospitals, day-care centres, paediatric clinics)

- India Baby Food Market: Regulatory Framework

- India Baby Food Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Kilo Tonnes)

- Market Share & Forecast

- By Product Type

- Infant Milk Formula

- Baby Cereals

- Dried Baby Food

- Prepared Baby Food / Purees

- Ready-to-Feed Baby Food

- Baby Snacks & Finger Foods

- Others

- By Category

- Organic

- Conventional

- By Age Group

- 0 to 6 Months

- 6 to 12 Months

- 12 to 24 Months

- Above 24 Months

- By Packaging Type

- Tin Cans

- Pouches

- Glass Jars

- Cartons & Tetra Packs

- Plastic Bottles

- By Product Format

- Powder

- Liquid

- Solid / Semi-Solid

- By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Convenience Stores & Kirana

- Online Retail / E-commerce

- Specialty Baby Stores

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Baby Food Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Nestle India Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- Danone India Pvt. Ltd. (Nutricia)

- Abbott India Limited

- Mead Johnson Nutrition India (Reckitt Benckiser Group plc)

- Hindustan Unilever Limited

- Amway India Enterprises Pvt. Ltd.

- Raptakos, Brett & Co. Ltd.

- Gujarat Cooperative Milk Marketing Federation Ltd. (Amul)

- Wholesum Foods Pvt. Ltd. (Slurrp Farm)

- Early Foods Pvt. Ltd.

- Happa Foods Pvt. Ltd.

- Timios Nutrition Pvt. Ltd.

- Pristine Organics Pvt. Ltd.

- Other Prominent Players

- Nestle India Limited

- By Product Type

- Market Size & Forecast, 2021-2032

Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India baby food market and what is its growth forecast?

Ans: India baby food market is valued at USD 1.65 billion in 2025 and is projected to reach USD 3.42 billion by 2032, registering a CAGR of 10.9% during 2026-2032, supported by rising urbanisation, working mothers, and growing e-commerce-led baby nutrition adoption.

2. Which segments are driving demand in the India baby food market?

Ans: Infant milk formula leads with over 60% share, while organic and millet-based baby food is the fastest growing category at 15% to 18% annually, supported by clean-label parental focus and premiumisation trends.

3. What are the key drivers of growth in the India baby food market?

Ans: Rising urbanisation, dual-income households, growing women workforce, increasing parental awareness of infant nutrition, accelerated e-commerce penetration, and premium product adoption are the key drivers fuelling India baby food market growth.

4. Which regions are driving growth in the India baby food market?

Ans: West and North India lead with 55% to 58% share, driven by Maharashtra, Gujarat, Delhi NCR, Punjab, and Uttar Pradesh, while South India contributes 25% to 28%, led by Karnataka, Tamil Nadu, Telangana, and Kerala urban clusters.

5. What are the latest trends in the India baby food market?

Ans: Key trends include rapid organic and millet-based baby food adoption, HMO-fortified infant formula growth, expanding e-commerce and D2C distribution, subscription-based delivery models, and premium fortified baby cereal launches by Nestle, Danone, and Slurrp Farm.

Frequently Asked Questions

1. How large is the India baby food market and what is its growth forecast?

Ans: India baby food market is valued at USD 1.65 billion in 2025 and is projected to reach USD 3.42 billion by 2032, registering a CAGR of 10.9% during 2026-2032, supported by rising urbanisation, working mothers, and growing e-commerce-led baby nutrition adoption.

2. Which segments are driving demand in the India baby food market?

Ans: Infant milk formula leads with over 60% share, while organic and millet-based baby food is the fastest growing category at 15% to 18% annually, supported by clean-label parental focus and premiumisation trends.

3. What are the key drivers of growth in the India baby food market?

Ans: Rising urbanisation, dual-income households, growing women workforce, increasing parental awareness of infant nutrition, accelerated e-commerce penetration, and premium product adoption are the key drivers fuelling India baby food market growth.

4. Which regions are driving growth in the India baby food market?

Ans: West and North India lead with 55% to 58% share, driven by Maharashtra, Gujarat, Delhi NCR, Punjab, and Uttar Pradesh, while South India contributes 25% to 28%, led by Karnataka, Tamil Nadu, Telangana, and Kerala urban clusters.

5. What are the latest trends in the India baby food market?

Ans: Key trends include rapid organic and millet-based baby food adoption, HMO-fortified infant formula growth, expanding e-commerce and D2C distribution, subscription-based delivery models, and premium fortified baby cereal launches by Nestle, Danone, and Slurrp Farm.