India Air Conditioners Market, By Product Type (Split Air Conditioners, Window Air Conditioners, Inverter Air Conditioners, Cassette Air Conditioners, Floor Standing Air Conditioners, Portable Air Conditioners, Others); By Capacity (Up to 1 Ton, 1–1.5 Ton, 1.5–2 Ton, Above 2 Ton); By End User (Residential, Commercial, Industrial); By Distribution Channel (Multi-Brand Stores, Exclusive Brand Outlets, Online Channels, Institutional Sales, Others); By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Consumer Goods & Retail

- Apr 2026

- Pages 170

- Report Format: pdf

- Report Price: $1800 USD

India Air Conditioners Market, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

| Market Size (2025) | USD 6.51 Billion |

| CAGR (2026-2032) | 15% |

| Leading Segment | Split AC |

| Fastest Growing Segment | Commercial |

| Market Size (2032) | USD 16.14 Billion |

MARKET OVERVIEW

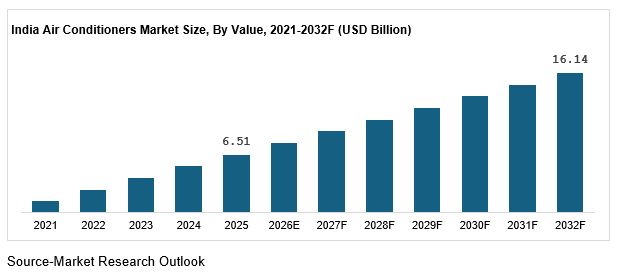

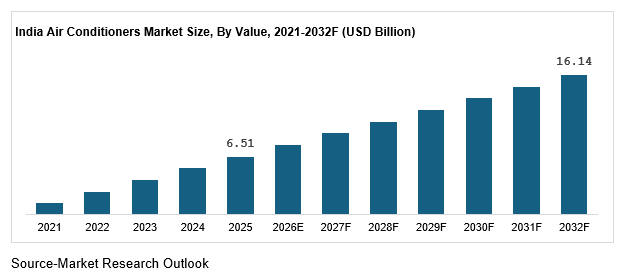

The India Air Conditioners Market is valued at USD 6.51 billion in 2025 and is expected to reach USD 16.14 billion by 2032, growing at a CAGR of 15.0 percent. In volume terms, annual sales are estimated at around 14.2 million units in 2025 and are projected to exceed 32 million units by 2032. Despite this growth, penetration remains below 10 percent, indicating a large untapped opportunity.

Pricing varies across segments, with entry level models starting around INR 25000 and premium inverter units reaching up to INR 65000. Inverter ACs carry a price premium of 18 to 25 percent but deliver energy savings of 25 to 30 percent. Split air conditioners dominate with 68 percent market share, while window units contribute around 21 percent.

Residential demand accounts for 72 percent of total consumption, supported by income growth of 10 to 11 percent annually. The 1.5 ton segment leads with 52 percent share, driven by typical household requirements. Tier II and Tier III cities contribute 46 percent of incremental demand, while online sales account for 28 percent, up from 21 percent in 2023. Rising temperatures of 0.6 to 0.8 degrees Celsius over the past decade continue to drive structural demand.

KEY REPORT TAKEAWAYS

- India Air Conditioners Market is projected to grow from USD 6.51 billion in 2025 to USD 16.14 billion by 2032, reflecting a strong 15.0 percent CAGR

- Penetration remains below 10 percent, indicating a large untapped opportunity across over 250 million households

- Split air conditioners dominate with 68 percent share, while inverter ACs are growing at 18 percent CAGR driven by energy efficiency demand

- Tier II and Tier III cities contribute 46 percent of incremental demand, supported by income growth of 10 to 11 percent annually

- Online sales account for 28 percent of total market, up from 21 percent in 2023, with digital channels growing at over 22 percent annually

KEY MARKET DRIVERS

Rising Temperature and Structural Cooling Demand Shift

Cooling demand in India is shifting from seasonal to structural. Over the past decade, average temperatures have increased by around 0.7 degree Celsius, while the number of heatwave days has risen by nearly 22 percent. This has directly increased usage intensity, which is now growing at 12 to 15 percent annually across multiple regions. North and West India together contribute more than 55 percent of total demand, with temperatures regularly exceeding 40 degrees Celsius for extended periods. Replacement cycles are also shortening from around 8 years to 6 to 7 years, indicating faster product turnover. In 2025, a prolonged summer led to more than 20 percent growth in AC sales during peak months, confirming that rising temperatures are not a temporary factor but a long term demand driver.

Rising Affordability and Financing Driven Adoption

Affordability is improving steadily, supported by income growth of around 10 to 11 percent annually and increased access to financing. Currently, nearly 42 percent of AC purchases are financed, compared to less than 30 percent three years ago. Financing reduces upfront burden by approximately 20 to 25 percent, making higher priced models more accessible. Residential demand dominates with 72 percent share, supported by housing growth of around 8 percent annually. Inverter ACs, despite being priced 25 percent higher, are growing at around 18 percent CAGR, reflecting a clear shift toward efficiency and premiumization. In 2025, festive season sales increased by over 15 percent, largely driven by financing schemes and bundled offers, showing that credit availability is directly accelerating market expansion.

Expansion of Distribution and Digital Sales Channels

The way consumers purchase air conditioners is evolving rapidly. Offline retail continues to dominate with around 72 percent share, but online channels have scaled to 28 percent and are growing at 20 to 22 percent annually. Internet penetration has crossed 52 percent, while smartphone usage exceeds 60 percent, supporting digital commerce growth. Tier II and Tier III cities now contribute nearly 46 percent of incremental demand, driven by improved logistics and wider product access. Delivery timelines have improved by approximately 15 percent, making online purchases more reliable. In 2025, ecommerce platforms recorded over 25 percent growth in AC sales during peak summer campaigns, highlighting the increasing role of digital channels in market expansion.

KEY MARKET CHALLENGES

Raw Material Cost Volatility and Margin Pressure

Raw material cost volatility continues to impact profitability across the air conditioners market. Copper and aluminum together account for nearly 35 percent of manufacturing costs, and their prices have increased by around 9 to 11 percent over the past two years. Logistics costs have also risen by approximately 5 to 6 percent, further increasing overall production expenses. As a result, operating margins have declined by around 3 to 4 percent, particularly for mid tier players competing in price sensitive segments. In 2025, several manufacturers reported margin pressure despite strong sales volumes, as competitive pricing limited their ability to pass on cost increases. This ongoing imbalance between input cost inflation and pricing pressure continues to challenge long term profitability and pricing strategies.

Energy Cost Sensitivity and Regulatory Compliance Pressure

Energy consumption remains a key concern for both consumers and manufacturers. Air conditioners can account for up to 40 percent of household electricity usage during peak summer months. Electricity tariffs are increasing at around 6 to 8 percent annually, raising the total cost of ownership and impacting purchase decisions. At the same time, stricter energy efficiency regulations have increased compliance costs by 5 to 7 percent, requiring investment in technology upgrades and product redesign. In 2025, updated efficiency norms led to product revisions and re certification requirements, increasing costs and delaying launches. While these regulations improve long term efficiency, they also create short term pricing pressure and adoption challenges, particularly in cost sensitive segments.

KEY MARKET TRENDS

Shift Toward Energy Efficient and Inverter Technology

The market is witnessing a clear shift toward energy efficient air conditioners, with inverter models accounting for approximately 58 percent of total sales and growing at around 18 percent annually. These systems offer energy savings of up to 25 percent, making them attractive despite being priced around 25 percent higher than conventional models. Consumers are increasingly prioritizing long term savings over upfront cost. In 2025, several leading brands reported that more than 60 percent of their sales came from inverter ACs, confirming strong adoption across urban markets. This trend is expected to continue as energy costs rise and awareness increases.

Rapid Growth of Online and Omnichannel Sales

Digital channels are becoming a key growth driver, with online sales accounting for around 28 percent of total demand and growing at 20 to 22 percent annually. Price transparency, wider product selection, and financing options are driving this shift. In 2025, ecommerce platforms reported over 25 percent growth in AC sales during peak summer campaigns, reflecting strong seasonal demand. Brands are increasingly adopting omnichannel strategies, combining online discovery with offline fulfillment, which has improved conversion rates by around 10 to 12 percent. This integrated approach is helping brands expand reach and improve customer experience.

Premiumization and Smart Feature Adoption

There is a growing shift toward premium air conditioners equipped with advanced features such as smart connectivity, AI based cooling, and app control. Premium models, typically priced 25 to 30 percent higher, are growing at around 17 percent annually, especially in metro cities where penetration exceeds 30 percent. Consumers are increasingly focusing on comfort, automation, and energy optimization rather than just basic cooling. In 2025, multiple brands launched smart AC models with sensor based and remote access capabilities, indicating rising demand for connected home solutions.

SEGMENTAL INSIGHTS

Product Type and Technology Mix

Split air conditioners dominate the market with approximately 68 percent share, driven by efficiency and suitability for urban housing. Window ACs contribute around 18 percent, primarily in price sensitive segments. Inverter ACs account for nearly 58 percent of total demand and are growing at around 18 percent annually, supported by energy savings of up to 25 percent. In 2025, leading brands reported that inverter models contributed over 60 percent of their total sales, highlighting a clear shift toward efficient and premium products.

Capacity and End User Demand Distribution

Air conditioners between 1 ton and 1.5 ton account for around 52 percent of total demand, making them the most widely used segment. The 1.5 to 2 ton segment holds around 30 percent share and is growing at approximately 16 percent annually. Units below 1 ton contribute around 10 percent, mainly in compact residential spaces. Residential users account for 72 percent of demand, while the commercial segment contributes 28 percent and is growing faster at around 19 percent CAGR. In 2025, commercial demand increased significantly across retail and office spaces, reflecting broader usage beyond households.

Distribution Channel and Sales Dynamics

Offline retail continues to dominate with around 72 percent share, supported by dealer networks and installation services. Online channels account for 28 percent and are growing at 20 to 22 percent annually. Tier II and Tier III cities contribute nearly 46 percent of incremental demand, supported by improved logistics and digital access. In 2025, online platforms recorded more than 25 percent growth in AC sales during peak summer, highlighting the increasing importance of digital channels. Omnichannel strategies are improving conversion rates by around 10 to 12 percent, strengthening overall sales performance.

REGIONAL INSIGHTS

Demand remains concentrated in North and West India, which together account for nearly 55 percent of total market share, driven by prolonged summers and high temperature levels. South India contributes around 25 percent, supported by stable demand, while East India holds approximately 20 percent share with emerging growth potential. Growth rates are highest in Central and Eastern regions at around 18 to 20 percent annually, compared to 13 to 14 percent in metro markets. Metro cities contribute around 54 percent of demand, while non metro regions account for 46 percent and are growing at approximately 19 percent annually. In 2025, cities such as Lucknow, Indore, and Bhubaneswar recorded growth above 20 percent, highlighting the shift toward emerging markets.

KEY MARKET PLAYERS

- Voltas Limited

- Daikin Airconditioning India Pvt Ltd

- LG Electronics India Pvt Ltd

- Samsung India Electronics Pvt Ltd

- Blue Star Limited

- Johnson Controls Hitachi Air Conditioning India Ltd

- Panasonic India Pvt Ltd

- Carrier Midea India Pvt Ltd

- Whirlpool of India Ltd

- Haier Appliances India Pvt Ltd

Report Scope:

In this report, the India Air Conditioners Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

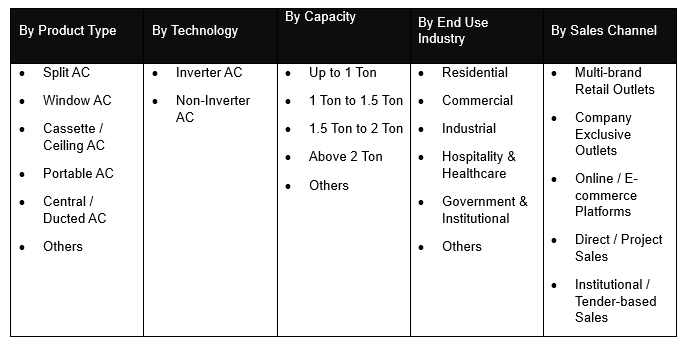

- By Product Type

- Split AC

- Window AC

- Cassette / Ceiling AC

- Portable AC

- Central / Ducted AC

- Others

- By Technology

- Inverter AC

- Non-Inverter AC

- By Capacity

- Up to 1 Ton

- 1 Ton to 1.5 Ton

- 5 Ton to 2 Ton

- Above 2 Ton

- Others

- By End Use Industry

- Residential

- Commercial

- Industrial

- Hospitality & Healthcare

- Government & Institutional

- Others

- By Sales Channel

- Multi-brand Retail Outlets

- Company Exclusive Outlets

- Online / E-commerce Platforms

- Direct / Project Sales

- Institutional / Tender-based Sales

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the India Air Conditioners Market, covering product portfolio, strategic initiatives, financial performance, and recent developments.

AVAILABLE CUSTOMIZATIONS

India Air Conditioners Market report, with the given market data, Market Research Outlook offers customizations based on specific business requirements. The following customization options are available for the report:

Company Information

Detailed analysis and profiling of additional market players up to five companies can be included as per client requirements.

The India Air Conditioners Market report is part of an upcoming release. For early access to this report or to confirm the expected release timeline, please connect with our team at sarita@marketresearchoutlook.com

Table of contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Qualitative Research

- Executive Summary

- Market Overview, 2021–2032

- By Product Type

- By Technology

- By Capacity

- By End Use Industry

- By Sales Channel

- Analyst Recommendations

- Market Overview, 2021–2032

- Geopolitical Impact on India Air Conditioners Market

- India Air Conditioners Market Insights

- Market Dynamics

- Growth Drivers

- Rising ambient temperatures and increasing frequency of heat waves across India.

- Growing urbanization, expanding middle class, and rising disposable incomes.

- Rapid expansion of commercial real estate, hospitality, and retail sectors.

- Restraints

- High energy consumption and rising electricity tariffs limiting affordability of ACs.

- Seasonal and cyclical demand patterns leading to inventory buildup risks for manufacturers.

- Price sensitivity in semi-urban and rural markets restraining overall volume growth.

- Opportunities

- Strong government push for energy efficiency through the BEE star rating system.

- Growing demand for inverter ACs and smart, IoT-enabled connected home solutions.

- Expanding market penetration in Tier-2 and Tier-3 cities and rural areas.

- Challenges

- Intense price competition and margin pressure among domestic and global brands.

- Supply chain vulnerabilities for key components such as compressors and refrigerants.

- Regulatory transitions related to refrigerant phase-out (R-22) and adoption of R-32, R-290.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Growth Drivers

- Market Dynamics

- Industry Value Chain & Entry Points

- Raw Material Suppliers (steel, copper, aluminum, refrigerants, plastics)

- Component Manufacturers (compressors, heat exchangers, PCBs, motors)

- AC Manufacturers / OEM Assemblers (branded & contract manufacturing)

- Quality Control & Testing (BEE star rating, BIS & IS certification)

- Packaging & Logistics (carton packaging, cold-chain where needed)

- Distributors, Dealers & Retailers

- End Users (residential, commercial, industrial & institutional)

- After-sales Support & Compliance Services

- India Air Conditioners Market: Regulatory Framework

- India Air Conditioners Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- Market Share & Forecast

- By Product Type

- Split AC

- Window AC

- Cassette / Ceiling AC

- Portable AC

- Central / Ducted AC

- Others

- By Technology

- Inverter AC

- Non-Inverter AC

- By Capacity

- Up to 1 Ton

- 1 Ton to 1.5 Ton

- 5 Ton to 2 Ton

- Above 2 Ton

- Others

- By End Use Industry

- Residential

- Commercial

- Industrial

- Hospitality & Healthcare

- Government & Institutional

- Others

- By Sales Channel

- Multi-brand Retail Outlets

- Company Exclusive Outlets

- Online / E-commerce Platforms

- Direct / Project Sales

- Institutional / Tender-based Sales

- By Product Type

- Market Size & Forecast, 2021-2032

- Competitive Landscape

- India Air Conditioners Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging players

- Company Profile

- Voltas Limited (Tata Group)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Voltas Limited (Tata Group)

**(Same Data Pointers Will Be Provided for The Below Companies)

- Daikin Airconditioning India Pvt. Ltd.

- Blue Star Limited

- LG Electronics India Pvt. Ltd.

- Samsung India Electronics Pvt. Ltd.

- Hitachi Cooling & Heating India Pvt. Ltd.

- Panasonic India Pvt. Ltd.

- Godrej & Boyce Mfg. Co. Ltd.

- Carrier Midea India Pvt. Ltd.

- Whirlpool of India Ltd.

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

**The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India air conditioners market and what is its growth outlook?

Ans: 1. How large is the India air conditioners market and what is its growth outlook?

The India air conditioners market size is valued at USD 6.51 billion in 2025 and is projected to reach USD 16.14 billion by 2032, growing at a CAGR of around 15 percent during the forecast period. This strong growth outlook reflects increasing demand for cooling solutions, low penetration levels, and rising adoption across residential and commercial segments. You get detailed market sizing, year-on-year forecasts, and growth projections to identify where the biggest expansion opportunities will emerge.

2. Which segments are driving demand in the India air conditioners market?

Ans: Demand in the India air conditioners market is primarily driven by split air conditioners, accounting for approximately 68 percent of total market share, supported by higher efficiency and strong consumer preference. Inverter and energy-efficient air conditioners are also gaining traction as consumers prioritise lower electricity consumption and long-term savings. The report breaks down demand by product type, technology, and application, helping you pinpoint high-growth segments and investment focus areas.

3. What are the key drivers of India air conditioners market growth?

Ans: The India air conditioners market growth is driven by rising temperatures, longer summers, increasing disposable income growing at around 10 to 11 percent, and expanding access to consumer financing. These factors are making air conditioners more accessible across a wider consumer base. You’ll see a data-backed breakdown of each growth driver, including its impact across regions and segments, enabling more precise strategic planning.

4. Which regions offer the highest growth opportunities in India?

Ans: The India air conditioners market regional analysis shows that North and West India account for nearly 55 percent of total demand, driven by extreme climatic conditions and higher urbanisation. Meanwhile, Tier II and Tier III cities contribute around 46 percent of incremental demand, emerging as the next major growth centres. The report maps demand at regional and city level, helping you identify where to expand, invest, and scale distribution.

5. What are the emerging trends in the India air conditioners market?

Ans: The India air conditioners market is evolving with rising adoption of inverter ACs, smart and connected cooling systems, and eco-friendly refrigerants. Consumers are increasingly focused on energy efficiency, while brands are introducing AI-enabled and IoT-integrated solutions. You get insights into technology trends, product innovation, and competitive positioning shaping the future of the India air conditioners market.

Frequently Asked Questions

1. How large is the India air conditioners market and what is its growth outlook?

Ans: 1. How large is the India air conditioners market and what is its growth outlook?

The India air conditioners market size is valued at USD 6.51 billion in 2025 and is projected to reach USD 16.14 billion by 2032, growing at a CAGR of around 15 percent during the forecast period. This strong growth outlook reflects increasing demand for cooling solutions, low penetration levels, and rising adoption across residential and commercial segments. You get detailed market sizing, year-on-year forecasts, and growth projections to identify where the biggest expansion opportunities will emerge.

2. Which segments are driving demand in the India air conditioners market?

Ans: Demand in the India air conditioners market is primarily driven by split air conditioners, accounting for approximately 68 percent of total market share, supported by higher efficiency and strong consumer preference. Inverter and energy-efficient air conditioners are also gaining traction as consumers prioritise lower electricity consumption and long-term savings. The report breaks down demand by product type, technology, and application, helping you pinpoint high-growth segments and investment focus areas.

3. What are the key drivers of India air conditioners market growth?

Ans: The India air conditioners market growth is driven by rising temperatures, longer summers, increasing disposable income growing at around 10 to 11 percent, and expanding access to consumer financing. These factors are making air conditioners more accessible across a wider consumer base. You’ll see a data-backed breakdown of each growth driver, including its impact across regions and segments, enabling more precise strategic planning.

4. Which regions offer the highest growth opportunities in India?

Ans: The India air conditioners market regional analysis shows that North and West India account for nearly 55 percent of total demand, driven by extreme climatic conditions and higher urbanisation. Meanwhile, Tier II and Tier III cities contribute around 46 percent of incremental demand, emerging as the next major growth centres. The report maps demand at regional and city level, helping you identify where to expand, invest, and scale distribution.

5. What are the emerging trends in the India air conditioners market?

Ans: The India air conditioners market is evolving with rising adoption of inverter ACs, smart and connected cooling systems, and eco-friendly refrigerants. Consumers are increasingly focused on energy efficiency, while brands are introducing AI-enabled and IoT-integrated solutions. You get insights into technology trends, product innovation, and competitive positioning shaping the future of the India air conditioners market.