Global Aerospace Plastics Market Size- By Plastic Type (Polyether Ether Ketone (PEEK), Polyetherimide (PEI), Polyamide (PA), Polycarbonate (PC), Polymethyl Methacrylate (PMMA), Others), By Aircraft Type (Commercial Aircraft, Military Aircraft, General Aviation, Helicopters, Spacecraft), By Manufacturing Process (Injection Molding, Extrusion, Thermoforming, Compression Molding, 3D Printing), By Application (Cabin Interiors, Aerostructures, Windows & Windshields, Electrical & Electronics, Insulation Components), By End Use (OEM (Original Equipment Manufacturer), Aftermarket), By Geography (North America, Asia Pacific, Europe, Latin America and Middle East and Africa), By Trend Analysis, Competitive Landscape & Forecast, 2026–2032– Industry Trends and Forecast to 2032

- Chemicals & Advanced Materials

- Mar 2026

- Pages 400

- Report Format: pdf

- Report Price: $3500 USD

Global Aerospace Plastics Market Analysis

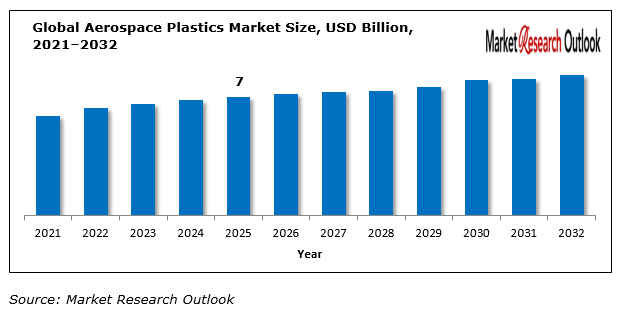

The global aerospace plastics market is expected to grow steadily from USD 7 billion in 2025 and is projected to reach approximately USD 12.8 billion by 2032, growing at a CAGR of around 10.20% during the forecast period. The aerospace plastics market is growing due to the increasing demand for lightweight materials to improve fuel efficiency and lower costs in aircraft. Aviation sector is always looking for ways to lower carbon emissions, and aerospace plastics are playing a significant role in this direction by lowering aircraft weights substantially compared to materials like aluminum and steel. In addition, the increasing production of commercial aircraft, passenger traffic, and low-cost carriers are further boosting market growth. Furthermore, advancements in high-performance plastics like PEEK, PEI, and PPS are allowing companies to produce aircraft components that can withstand high temperatures and pressures. In addition, government support for sustainable aviation technologies and constant investment in R&D activities will create tremendous opportunities for market growth during the forecast period.

Global Aerospace Plastics Market Overview

Market Trends

- One of the major factors contributing to the growth of the aerospace plastics market is the increasing demand for lightweight and fuel-efficient aircraft. Airlines and manufacturers are trying their best to reduce fuel consumption, and this is contributing to the increasing demand for advanced plastic materials.

- The increasing demand for high-performance thermoplastics and composite materials is creating new opportunities in the aerospace plastics market. The use of these materials is becoming more popular in the manufacturing of aircraft due to their strength and lightweight properties.

- The expansion of the global aviation sector, particularly in the emerging economies of the world, is contributing to the growth of the aerospace plastics market. The increase in air traffic and the defense budgets of these countries is contributing to the growth of the market.

- However, the aerospace plastics market is expected to face some challenges in the coming years, and these challenges include the high costs of raw materials, certification requirements, and the challenges faced in recycling these materials. The fluctuation in the prices of crude oil is affecting the supply of these materials.

Geopolitical Impact on Global Aerospace Plastics Market

The aerospace market, when viewed from a global perspective, is affected by various geopolitical factors like trade policies, defense budgets, and regulations of various regions. Regions like North America and Europe have well-established aerospace industries, manufacturing facilities, and regulations from governments, which play a vital role in the growth of the aerospace market. Regions like Asia Pacific are also becoming prominent players in the growth of the aerospace market, driven by increasing aircraft production, growth of the aviation fleet, and investments in aerospace infrastructure. Regions like Latin America, Middle East, and Africa are also growing, driven by increasing aviation demands and regulations from governments. However, the availability of raw materials might be affected due to trade policies, which might have a negative impact on the aerospace market. However, the aerospace market has a bright future, driven by the need for modernization and sustainability across the globe.

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | · North America (U.S. and Canada)

· Asia Pacific (China, India, Indonesia, Japan, South Korea, Australia, Malaysia, Rest of Asia Pacific) · Europe (Germany, United Kingdom, France, Italy, Russia, Spain, NORDIC, Rest of Europe) · Latin America (Mexico, Argentina, Brazil, Rest of Latin America) · Middle East and Africa (Israel, GCC, North Africa, South Africa, Rest of the Middle East and Africa) |

| Segmentation | By Plastic Type, By Aircraft Type, By Manufacturing Process, By Application, By End Use |

Global Aerospace Plastics Market: Segmentation Coverage

By Plastic Type

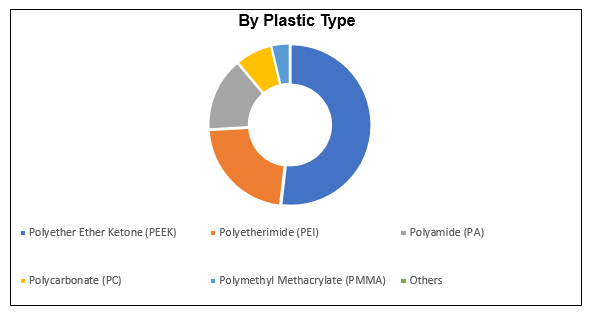

The plastics used in the aerospace industry are classified into high-performance plastics such as Polyether Ether Ketone (PEEK), Polyetherimide (PEI), Polyamide (PA), Polycarbonate (PC), and Polymethyl Methacrylate (PMMA), among others. Out of these plastics, PEEK is used because of its mechanical strength, high-temperature properties, and light weight. On the other hand, PEI is also increasingly used because of its flame retardancy and dimensional stability. Polyamide plastics are also used for aircraft components because of their durability and cost-effectiveness. Polycarbonate and PMMA plastics are also used for aircraft windows and canopies because of their optical clarity and toughness. The constant development of new plastics and reinforced plastics is also contributing to the growth and popularity of plastics in the aerospace industry.

By Aircraft Type

Based on type, the market can be segmented into commercial aircraft, military aircraft, general aircraft, helicopters, and spacecraft. The market share of commercial aircraft is high owing to the increasing air passengers and the fleet size of airlines. The need for lightweight materials in the commercial aircraft industry is high, as airlines are looking for reducing fuel costs. The military aircraft segment is also high, owing to the increasing defense budgets and the need for lightweight and high-performance materials in military aircraft. The general aircraft and helicopter segments are growing, and the spacecraft segment is emerging rapidly owing to the increasing need for space exploration and satellite deployment, where lightweight and high-performance materials are used.

Regional Analysis

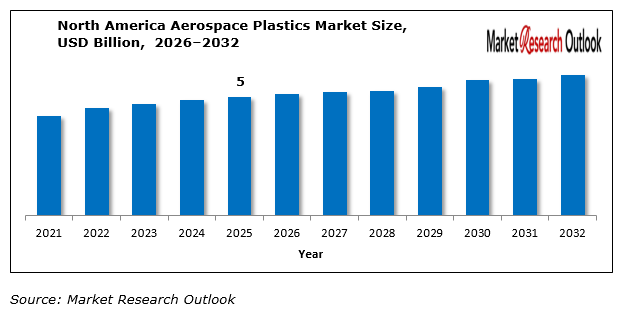

The market for aerospace plastics is divided into various geographic regions, namely North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. North America leads in this market because of the presence of key players in this region and high investment in aerospace R&D activities. Europe ranks second in this market, owing to stringent environmental regulations and high emphasis on sustainable aviation technology. Asia Pacific is also growing rapidly in this market because of increased air travel demand, expansion in airline fleet size, and development in aerospace manufacturing in this region, especially in Asia-based countries like China and India. Latin America and Middle East and Africa are also showing moderate growth in this market because of infrastructure development and increased investments in aviation in these regions. However, these regions are also facing challenges in this market because of economic and technology-related issues.

Recent Developments

- In August 2024, Pexco acquired Precise Aerospace Manufacturing, a move aimed at enhancing its capabilities in the aerospace sector. This acquisition allows Pexco to expand its product offerings and improve its service to customers in the aerospace industry. The deal is expected to strengthen Pexco’s position in the market by leveraging Precise Aerospace’s expertise and resources.

- In August 2024, Trelleborg Group acquired Magee Plastics, a U.S. company specializing in high-performance thermoplastic and composite materials for the aerospace industry. This move enhances Trelleborg’s Sealing Solutions business unit and strengthens its presence in the aerospace sector.

Competitive Landscape

In the competitive landscape of the global aerospace plastics market, the organisation has covered major players of the market and their details.

Here are some of the leading players that are playing a major role in the global Aerospace Plastics market:

- Victrex plc

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- Swot Analysis

**(Same Data Pointers Will Be Provided for The Below Companies)

- Ensinger

- SABIC

- Solvay

- BASF SE

- Evonik Industries AG

- Toray Advanced Composites

- Saint Gobain Aerospace

- DuPont

- Celanese Corporation

- Sumitomo Chemical Co., Ltd.

- Covestro AG

- Other Prominent Players

Segments

- By Plastic Type

- Polyether Ether Ketone (PEEK)

- Unfilled PEEK

- Carbon-Filled PEEK

- Glass-Filled PEEK

- Others

- Polyetherimide (PEI)

- Unfilled PEI

- Glass-Filled PEI

- Flame-Retardant PEI

- Others

- Polyamide (PA)

- PA6

- PA66

- Bio-based Polyamide

- Others

- Polycarbonate (PC)

- Standard PC

- Flame-Retardant PC

- Glass-Filled PC

- Others

- Polymethyl Methacrylate (PMMA)

- General Purpose PMMA

- Impact-Modified PMMA

- UV-Resistant PMMA

- Others

- Others

- Polyether Ether Ketone (PEEK)

- By Aircraft Type

- Commercial Aircraft

- Military Aircraft

- General Aviation

- Helicopters

- Spacecraft

- By Manufacturing Process

- Injection Molding

- Extrusion

- Thermoforming

- Compression Molding

- 3D Printing

- By Application

- Cabin Interiors

- Aerostructures

- Windows & Windshields

- Electrical & Electronics

- Insulation Components

- By End Use

- OEM (Original Equipment Manufacturer)

- Aftermarket

By Geography

- North America

- S.

- Canada

- Asia Pacific

- China

- India

- Australia

- Indonesia

- Japan

- South Korea

- Malaysia

- Thailand

- Rest of Asia Pacific

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Netherlands

- Rest of Europe

- Latin America

- Mexico

- Argentina

- Brazil

- Rest of Latin America

- Middle East and Africa

- Israel

- Saudi Arabia

- UAE

- Qatar

- North Africa

- South Africa

- Rest of the Middle East and Africa

Global Aerospace Plastics Market, 2032

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Breakdown Of Primary Research Respondents, By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

- Assumption & Limitation

- Qualitative Research

- Executive Summary

- Market Overview, 2021–2032

- By Plastic Type

- By Aircraft Type

- By Manufacturing Process

- By Application

- By End Use

- Analyst Recommendations

- Market Overview, 2021–2032

- Geopolitical Impact on Global Aerospace Plastics Market

- Global Aerospace Plastics Market Insights

- Market Dynamics

- Growth Drivers

- Increasing demand for lightweight and fuel-efficient aircraft

- Growth in commercial aviation and rising air passenger traffic

- Rising focus on carbon emission reduction and sustainability

- Expansion of aircraft production and fleet modernization

- Restraints

- High cost of advanced aerospace-grade plastics

- Complex manufacturing and processing requirements

- Stringent regulatory and certification procedures

- Opportunities

- Growing adoption of 3D printing and additive manufacturing

- Development of bio-based and recyclable plastics

- Expansion of aerospace industry in emerging markets

- Challenges

- Strict safety and performance standards compliance

- Competition from traditional materials like metals and alloys

- High initial investment and long certification timeline

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Trade Analysis

- Top 3 Importing Countries

- Top 3 Exporting Countries

- Growth Drivers

- Market Dynamics

- Industry Value Chain & Entry Points

- Raw Material Suppliers

- Polymer Production

- Plastic Compounding & Formulation

- Component Manufacturing & Processing

- Aerospace OEMs (Aircraft Manufacturers)

- Tier 1 & Tier 2 Suppliers

- Distribution & Supply Chain

- Maintenance, Repair, and Overhaul (MRO)

- End Users

- Global Aerospace Plastics Market: Regulatory Framework

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

- Global Aerospace Plastics Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Plastic Type

- Polyether Ether Ketone (PEEK)

- Unfilled PEEK

- Carbon-Filled PEEK

- Glass-Filled PEEK

- Others

- Polyetherimide (PEI)

- Unfilled PEI

- Glass-Filled PEI

- Others

- Polyamide (PA)

- PA6

- PA66

- Bio-based Polyamide

- Others

- Polycarbonate (PC)

- Standard PC

- Flame-Retardant PC

- Glass-Filled PC

- Others

- Polymethyl Methacrylate (PMMA)

- General Purpose PMMA

- Impact-Modified PMMA

- UV-Resistant PMMA

- Others

- Others

- Polyether Ether Ketone (PEEK)

- By Aircraft Type

- Commercial Aircraft

- Military Aircraft

- General Aviation

- Helicopters

- Spacecraft

- By Manufacturing Process

- Injection Molding

- Extrusion

- Thermoforming

- Compression Molding

- 3D Printing

- By Application

- Cabin Interiors

- Aerostructures

- Windows & Windshields

- Electrical & Electronics

- Insulation Components

- By End Use

- OEM (Original Equipment Manufacturer)

- Aftermarket

- By Geography

- North America

- S.

- Canada

- Asia Pacific

- China

- India

- Australia

- Indonesia

- Japan

- South Korea

- Malaysia

- Thailand

- Rest of Asia Pacific

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Netherlands

- Rest of Europe

- Latin America

- Mexico

- Argentina

- Brazil

- Rest of Latin America

- Middle East and Africa

- Israel

- Saudi Arabia

- UAE

- Qatar

- North Africa

- South Africa

- Rest of the Middle East and Africa

- North America

- By Plastic Type

- Market Size & Forecast, 2021-2032

- Competitive Landscape

- Global Aerospace Plastics Company Market Share Analysis, 2026

- By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging players

- By Region

- Global Aerospace Plastics Company Market Share Analysis, 2026

- Company Profile

- Victrex plc

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- Swot Analysis

- Victrex plc

**(Same Data Pointers Will Be Provided for The Below Companies)

- Ensinger

- SABIC

- Solvay

- BASF SE

- Evonik Industries AG

- Toray Advanced Composites

- Saint Gobain Aerospace

- DuPont

- Celanese Corporation

- Sumitomo Chemical Co., Ltd.

- Covestro AG

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

**The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. What is the expected growth rate of the Global Aerospace Plastics Market during the forecast period?

Ans: The Global Aerospace Plastics Market size was estimated at USD 10.6 billion in 2025.

2. What is the expected growth rate of the Global Aerospace Plastics Market during the forecast period?

Ans: Global Aerospace Plastics Market is expected to grow at a CAGR of around 7.9% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Global Aerospace Plastics Market by 2032?

Ans: The Global Aerospace Plastics Market is projected to reach a value of approximately USD 18.1 Billion by 2032.

4. What are the major factors driving the growth of the Global Aerospace Plastics Market?

Ans: The market expansion occurs because of two factors which include rising aircraft production and increasing demand for lightweight aerospace materials and the expansion of commercial aviation fleets.

5. Name the key players operating in the Global Aerospace Plastics Market.

Ans: The key players of Global Aerospace Plastics Market are Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, Intel Corporation, Micron Technology, SK Hynix, GlobalFoundries, United Microelectronics Corporation (UMC), Texas Instruments, Infineon Technologies, STMicroelectronics, Applied Materials, Lam Research and other prominent players.

6. Which is the fastest-growing plastic type segment in the Global Aerospace Plastics Market?

Ans: The PEEK market segment will achieve substantial market share because of its outstanding mechanical properties and thermal resistance and ability to withstand chemical and wear damage.

7. Which region contributes significantly to the growth of the Global Aerospace Plastics Market?

Ans: North America will experience substantial growth in the Global Aerospace Plastics Market throughout the forecast period because of its established major aircraft manufacturers and advanced aerospace supply chains and substantial funding dedicated to aviation technology development.

Frequently Asked Questions

1. What is the expected growth rate of the Global Aerospace Plastics Market during the forecast period?

Ans: The Global Aerospace Plastics Market size was estimated at USD 10.6 billion in 2025.

2. What is the expected growth rate of the Global Aerospace Plastics Market during the forecast period?

Ans: Global Aerospace Plastics Market is expected to grow at a CAGR of around 7.9% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Global Aerospace Plastics Market by 2032?

Ans: The Global Aerospace Plastics Market is projected to reach a value of approximately USD 18.1 Billion by 2032.

4. What are the major factors driving the growth of the Global Aerospace Plastics Market?

Ans: The market expansion occurs because of two factors which include rising aircraft production and increasing demand for lightweight aerospace materials and the expansion of commercial aviation fleets.

5. Name the key players operating in the Global Aerospace Plastics Market.

Ans: The key players of Global Aerospace Plastics Market are Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, Intel Corporation, Micron Technology, SK Hynix, GlobalFoundries, United Microelectronics Corporation (UMC), Texas Instruments, Infineon Technologies, STMicroelectronics, Applied Materials, Lam Research and other prominent players.

6. Which is the fastest-growing plastic type segment in the Global Aerospace Plastics Market?

Ans: The PEEK market segment will achieve substantial market share because of its outstanding mechanical properties and thermal resistance and ability to withstand chemical and wear damage.

7. Which region contributes significantly to the growth of the Global Aerospace Plastics Market?

Ans: North America will experience substantial growth in the Global Aerospace Plastics Market throughout the forecast period because of its established major aircraft manufacturers and advanced aerospace supply chains and substantial funding dedicated to aviation technology development.