Global Facility Management Market, By Service Type (Hard Services, Soft Services, Integrated Facility Management, Energy Management, Others); By Deployment Model (In-House, Outsourced); By Facility Type (Commercial Buildings, Industrial Facilities, Healthcare Facilities, Educational Institutions, Government & Public Infrastructure, Residential & Mixed-Use, Data Centers & Critical Infrastructure, Others); By End-Use Industry (IT & Telecom, Manufacturing & Industrial, Healthcare & Life Sciences, Retail & Hospitality, BFSI & Corporate Offices, Education, Government & Public Sector), Trend Analysis, Competitive Landscape & Forecast, 2021–2031

- ICT

- Jan 2026

- Pages 300

- Report Format: pdf

- Report Price: $3500 USD

Global Facility Management Market Trends & Forecast, 2021–2031

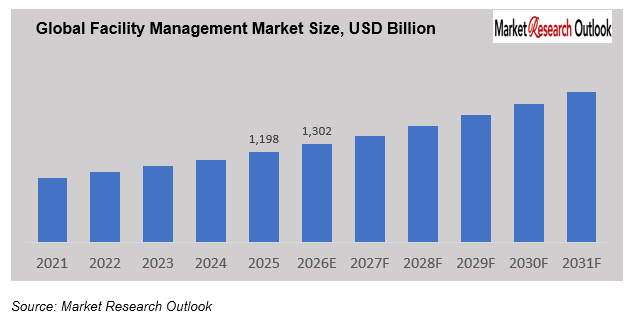

The Global Facility Management Market was estimated at around USD 1.3 trillion in 2025 and is projected to reach over USD 2 trillion by 2031. Market growth is primarily driven by increasing outsourcing of non-core operations, rising focus on cost optimization and operational efficiency, and growing adoption of integrated facility management (IFM) models across commercial, industrial, and institutional facilities.

Demand for facility management services is accelerating across commercial buildings, industrial facilities, healthcare institutions, educational campuses, data centers, and public infrastructure, as organizations seek reliable, compliant, and technology-enabled solutions to manage complex assets and operations. Growing emphasis on workplace safety, service quality, energy efficiency, and asset lifecycle management is further reinforcing this trend.

In addition, corporate ESG commitments, sustainability mandates, and increasing deployment of digital tools such as IoT-enabled monitoring, predictive maintenance, and energy management platforms are transforming service delivery models. These factors, combined with expanding real estate and infrastructure development and tightening regulatory and compliance requirements, are expected to sustain strong growth in the Global Facility Management Market between 2026 and 2031.

Facility Management – Overview

Facility management refers to the integrated management of people, processes, and physical assets within buildings and infrastructure to ensure safe, efficient, and sustainable operations. It encompasses a wide range of services, including hard services (such as HVAC, electrical, plumbing, and fire safety), soft services (such as cleaning, security, catering, and landscaping), and integrated facility management (IFM), which combines multiple services under a single delivery model.

Facility management solutions are designed to enhance operational efficiency, ensure regulatory compliance, improve occupant comfort and safety, and optimize asset lifecycle performance. By leveraging standardized processes, skilled workforce management, and increasingly digital tools such as IoT, building management systems, and data analytics, facility management supports sustainable building operations, energy efficiency, and cost optimization across commercial buildings, industrial facilities, healthcare institutions, educational campuses, data centers, and public infrastructure.

Global Facility Management Market

Growth Drivers

Increasing Outsourcing and Focus on Operational Efficiency

Rising pressure on organizations to optimize costs, improve service quality, and focus on core business activities is a key factor driving the growth of the Global Facility Management Market. Corporates, industrial operators, and public-sector entities across North America, Europe, and Asia-Pacific are increasingly outsourcing facility operations to specialized service providers to achieve efficiency, standardization, and regulatory compliance. Growing emphasis on workplace safety, energy efficiency, sustainability, and service-level accountability is accelerating the adoption of integrated facility management (IFM) models across diverse end-use sectors. These trends are creating a supportive ecosystem for the expansion of professional facility management services globally.

Challenges

Cost Sensitivity and Service Standardization Concerns

Cost sensitivity remains a key challenge restraining the growth of the Global Facility Management Market, particularly in price-sensitive regions and sectors. While outsourcing offers long-term efficiency gains, concerns around service costs, contract rigidity, and transition complexity can delay adoption. In addition, ensuring consistent service quality across geographically dispersed facilities and managing skilled workforce availability continue to pose operational challenges for facility management providers.

Impact of Escalating Geopolitical Tensions on Global Facility Management Market

Escalating geopolitical tensions across regions can have a notable impact on the growth of the Global Facility Management Market. Macroeconomic uncertainty, inflationary pressures, and disruptions in construction and infrastructure investments can slow the development of new facilities and expansion projects. Rising energy costs, labor shortages, and regulatory uncertainty may increase operating expenses for facility management providers and clients. Furthermore, currency fluctuations and trade restrictions can affect procurement of equipment and services. Prolonged geopolitical instability could therefore pose challenges to sustained market growth.

Global Facility Management Market

Segmental Coverage

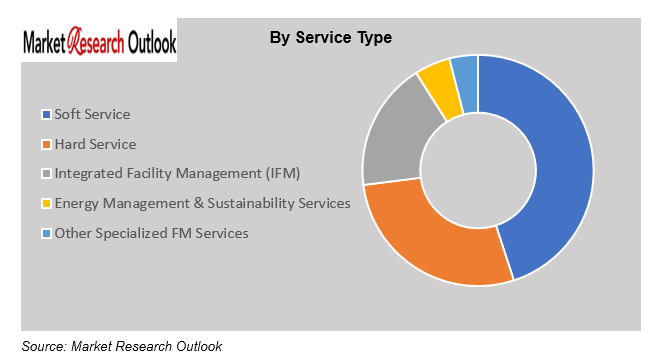

Global Facility Management Market – By Service Type

Based on service type, the Global Facility Management Market is segmented into Hard Services, Soft Services, Integrated Facility Management (IFM), Energy Management Services, and other specialized services. Integrated facility management and soft services account for a significant share of the market, driven by increasing preference for bundled service offerings that deliver cost efficiency, operational transparency, and single-point accountability. IFM models enable centralized management of multiple services such as maintenance, cleaning, security, and energy management, improving asset performance and service consistency. Continuous adoption of digital tools, smart building technologies, and data-driven maintenance practices is further strengthening demand across end-use industries.

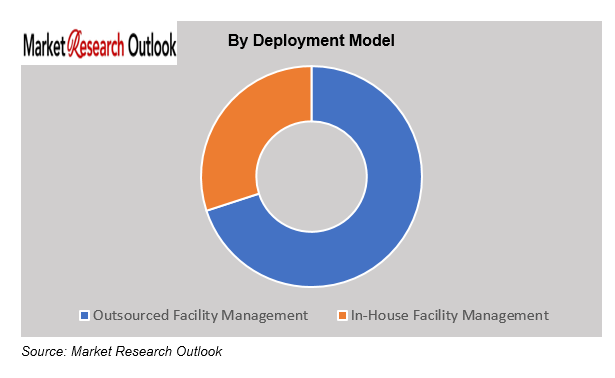

Global Facility Management Market – By Deployment Model

Based on deployment model, the Global Facility Management Market is divided into In-House and Outsourced segments. The outsourced segment holds a dominant share of the market, supported by growing preference among organizations to focus on core business activities while transferring non-core facility operations to specialized service providers. Increasing emphasis on cost optimization, service standardization, regulatory compliance, and access to skilled workforce is driving adoption of outsourced facility management models. Additionally, rising demand for integrated facility management (IFM), scalability across multi-site portfolios, and alignment with sustainability and ESG objectives is expected to further strengthen the growth of the outsourced segment during the forecast period.

Competitive Landscape

Major players operating in the Global Facility Management Market include multinational facility management service providers, integrated FM companies, and regional service specialists. To strengthen their market position, these companies are adopting strategies such as mergers and acquisitions, strategic partnerships, geographic expansion, long-term outsourcing contracts, and expansion of integrated facility management (IFM) offerings. Continuous investment in digital platforms, workforce training, ESG-aligned service delivery, and smart building capabilities remains central to maintaining a competitive advantage in the global facility management industry.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2026 Estimated Year – 2027 Forecast Period – 2028–2031 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | Global |

| Product/ Service Segmentation | Service Type, Deployment Model, Facility Type, End-Use Industry |

| Key Players | ISS A/S, Sodexo, CBRE Group, Jones Lang LaSalle (JLL), Compass Group, Cushman & Wakefield, Engie Solutions, Mitie Group, Serco Group, G4S, Apleona Group, Dussmann Group, Aramark, OCS Group |

- By Service Type

o Hard Services (HVAC, Electrical, Plumbing, Fire Safety)

o Soft Services (Cleaning, Security, Catering, Landscaping)

o Integrated Facility Management (IFM)

o Energy Management Services

o Other Specialized Facility Services - By Deployment Model

o In-House

o Outsourced - By Facility Type

o Commercial Buildings

o Industrial Facilities

o Healthcare Facilities

o Educational Institutions

o Government & Public Infrastructure

o Residential & Mixed-Use Properties

o Data Centers & Critical Infrastructure

o Others - By End-Use Industry

o IT & Telecom

o Manufacturing & Industrial

o Healthcare & Life Sciences

o Retail & Hospitality

o BFSI & Corporate Offices

o Education

o Government & Public Sector

Global Facility Management Market – Table of Contents

- Introduction

- Market Overview

- Facility Management Definition & Classification

- Research Methodology

- Key Assumptions

- Executive Summary

- Market Snapshot (2025)

- Key Insights & Emerging Trends

- Strategic Takeaways

- Regulatory, ESG & Sustainability Landscape

- Facility Management Ecosystem & Value Chain Analysis

- Market Dynamics

- Growth Drivers

- Market Challenges

- Emerging Opportunities

- Regional Demand Hotspots

- Key Market Trends & Developments

- Global Facility Management Market Outlook (2026–2030)

- Market Size & Forecast (USD Million)

- Historical Analysis (2020–2025) vs Forecast (2026–2030)

- By Service Type

- Hard Services (HVAC, Electrical, Plumbing, Fire Safety)

- Soft Services (Cleaning, Security, Catering, Landscaping)

- Integrated Facility Management (IFM)

- Energy Management Services

- Other Specialized FM Services

- By Deployment Model

- In-House

- Outsourced

- By Facility Type

- Commercial Buildings

- Industrial Facilities

- Healthcare Facilities

- Educational Institutions

- Government & Public Infrastructure

- Residential & Mixed-Use Properties

- Data Centers & Critical Infrastructure

- Others

- By End-Use Industry

- IT & Telecom

- Manufacturing & Industrial

- Healthcare & Life Sciences

- Retail & Hospitality

- BFSI & Corporate Offices

- Education

- Government & Public Sector

- By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

- Asia-Pacific Facility Management Market Outlook (2026–2030)

- Market Size & Forecast (USD Million)

- Historical Analysis (2020–2025) vs Forecast (2026–2030)

- By Service Type

- Hard Services (HVAC, Electrical, Plumbing, Fire Safety)

- Soft Services (Cleaning, Security, Catering, Landscaping)

- Integrated Facility Management (IFM)

- Energy Management Services

- Other Specialized FM Services

- By Deployment Model

- In-House

- Outsourced

- By Facility Type

- Commercial Buildings

- Industrial Facilities

- Healthcare Facilities

- Educational Institutions

- Government & Public Infrastructure

- Residential & Mixed-Use Properties

- Data Centers & Critical Infrastructure

- Others

- By End-Use Industry

- IT & Telecom

- Manufacturing & Industrial

- Healthcare & Life Sciences

- Retail & Hospitality

- BFSI & Corporate Offices

- Education

- Government & Public Sector

- By Country

- North America Facility Management Market Outlook (2026–2030)

- Market Size & Forecast (USD Million)

- Historical Analysis (2020–2025) vs Forecast (2026–2030)

- By Service Type

- Hard Services (HVAC, Electrical, Plumbing, Fire Safety)

- Soft Services (Cleaning, Security, Catering, Landscaping)

- Integrated Facility Management (IFM)

- Energy Management Services

- Other Specialized FM Services

- By Deployment Model

- In-House

- Outsourced

- By Facility Type

- Commercial Buildings

- Industrial Facilities

- Healthcare Facilities

- Educational Institutions

- Government & Public Infrastructure

- Residential & Mixed-Use Properties

- Data Centers & Critical Infrastructure

- Others

- By End-Use Industry

- IT & Telecom

- Manufacturing & Industrial

- Healthcare & Life Sciences

- Retail & Hospitality

- BFSI & Corporate Offices

- Education

- Government & Public Sector

- By Country

- Europe Facility Management Market Outlook (2026–2030)

- Market Size & Forecast (USD Million)

- Historical Analysis (2020–2025) vs Forecast (2026–2030)

- By Service Type

- Hard Services (HVAC, Electrical, Plumbing, Fire Safety)

- Soft Services (Cleaning, Security, Catering, Landscaping)

- Integrated Facility Management (IFM)

- Energy Management Services

- Other Specialized FM Services

- By Deployment Model

- In-House

- Outsourced

- By Facility Type

- Commercial Buildings

- Industrial Facilities

- Healthcare Facilities

- Educational Institutions

- Government & Public Infrastructure

- Residential & Mixed-Use Properties

- Data Centers & Critical Infrastructure

- Others

- By End-Use Industry

- IT & Telecom

- Manufacturing & Industrial

- Healthcare & Life Sciences

- Retail & Hospitality

- BFSI & Corporate Offices

- Education

- Government & Public Sector

- By Country

- South America Facility Management Market Outlook (2026–2030)

- Market Size & Forecast (USD Million)

- Historical Analysis (2020–2025) vs Forecast (2026–2030)

- By Service Type

- Hard Services (HVAC, Electrical, Plumbing, Fire Safety)

- Soft Services (Cleaning, Security, Catering, Landscaping)

- Integrated Facility Management (IFM)

- Energy Management Services

- Other Specialized FM Services

- By Deployment Model

- In-House

- Outsourced

- By Facility Type

- Commercial Buildings

- Industrial Facilities

- Healthcare Facilities

- Educational Institutions

- Government & Public Infrastructure

- Residential & Mixed-Use Properties

- Data Centers & Critical Infrastructure

- Others

- By End-Use Industry

- IT & Telecom

- Manufacturing & Industrial

- Healthcare & Life Sciences

- Retail & Hospitality

- BFSI & Corporate Offices

- Education

- Government & Public Sector

- By Country

- Middle East & Africa Facility Management Market Outlook (2026–2030)

- Market Size & Forecast (USD Million)

- Historical Analysis (2020–2025) vs Forecast (2026–2030)

- By Service Type

- Hard Services (HVAC, Electrical, Plumbing, Fire Safety)

- Soft Services (Cleaning, Security, Catering, Landscaping)

- Integrated Facility Management (IFM)

- Energy Management Services

- Other Specialized FM Services

- By Deployment Model

- In-House

- Outsourced

- By Facility Type

- Commercial Buildings

- Industrial Facilities

- Healthcare Facilities

- Educational Institutions

- Government & Public Infrastructure

- Residential & Mixed-Use Properties

- Data Centers & Critical Infrastructure

- Others

- By End-Use Industry

- IT & Telecom

- Manufacturing & Industrial

- Healthcare & Life Sciences

- Retail & Hospitality

- BFSI & Corporate Offices

- Education

- Government & Public Sector

- By Country

- Competitive Landscape

- Competitive Characteristics

- Market Share Analysis

- Company Benchmarking

- Competitive Strategies

- Company Profiles

- Business Overview

- Service Portfolio & Digital Capabilities

- Operational Footprint & Workforce Strength

- Geographic Presence

- Sustainability, ESG & Smart Building Initiatives

- Strategic Partnerships & Alliances

- Recent Developments

- Financial Overview

- Regulatory, Compliance & ESG Strategy

- Digitalization, Automation & Cost Optimization

- Workforce Management & Service Delivery Strategy

- Go-to-Market & Client Acquisition Strategy

- Conclusion & Key Takeaways

- Disclaimer

Frequently Asked Questions

1. What is the current market size of the Global Facility Management Market?

Ans: The Global Facility Management Market size by value was estimated at around USD 1.3 trillion in 2025.

2. What is the expected growth rate of the Global Facility Management Market by value during the forecast period?

Ans: The Global Facility Management Market is expected to grow at a CAGR of approximately 9% during the forecast period between 2026 and 2031.

3. What is the forecast value of the Global Facility Management Market size by the end of the forecast period?

Ans: By 2031, the Global Facility Management Market size is forecast to reach over USD 2 trillion.

4. What are the major factors driving the growth of the Global Facility Management Market?

Ans: The growth of the Global Facility Management Market is primarily driven by increasing outsourcing of non-core operations, rising focus on cost optimization and operational efficiency, growing adoption of integrated facility management (IFM) models, expanding commercial and industrial infrastructure, and increasing emphasis on ESG compliance, workplace safety, and energy efficiency.

5. Name the key players in the Global Facility Management Market.

Ans: Key players operating in the Global Facility Management Market include ISS A/S, Sodexo, CBRE Group, Jones Lang LaSalle (JLL), Compass Group, Cushman & Wakefield, Engie Solutions, Mitie Group, Serco Group, and Aramark, among others.

6. Which is a faster-growing segment in the Global Facility Management Market by deployment model?

Ans: The outsourced facility management segment is expected to grow at a faster CAGR during the forecast period, driven by rising preference for integrated service delivery, scalability across multi-site portfolios, access to specialized expertise, and long-term cost and compliance benefits.

Frequently Asked Questions

1. What is the current market size of the Global Facility Management Market?

Ans: The Global Facility Management Market size by value was estimated at around USD 1.3 trillion in 2025.

2. What is the expected growth rate of the Global Facility Management Market by value during the forecast period?

Ans: The Global Facility Management Market is expected to grow at a CAGR of approximately 9% during the forecast period between 2026 and 2031.

3. What is the forecast value of the Global Facility Management Market size by the end of the forecast period?

Ans: By 2031, the Global Facility Management Market size is forecast to reach over USD 2 trillion.

4. What are the major factors driving the growth of the Global Facility Management Market?

Ans: The growth of the Global Facility Management Market is primarily driven by increasing outsourcing of non-core operations, rising focus on cost optimization and operational efficiency, growing adoption of integrated facility management (IFM) models, expanding commercial and industrial infrastructure, and increasing emphasis on ESG compliance, workplace safety, and energy efficiency.

5. Name the key players in the Global Facility Management Market.

Ans: Key players operating in the Global Facility Management Market include ISS A/S, Sodexo, CBRE Group, Jones Lang LaSalle (JLL), Compass Group, Cushman & Wakefield, Engie Solutions, Mitie Group, Serco Group, and Aramark, among others.

6. Which is a faster-growing segment in the Global Facility Management Market by deployment model?

Ans: The outsourced facility management segment is expected to grow at a faster CAGR during the forecast period, driven by rising preference for integrated service delivery, scalability across multi-site portfolios, access to specialized expertise, and long-term cost and compliance benefits.