Europe CCUS Market, By Technology (Pre-Combustion Capture, Post-Combustion Capture, Oxy-Fuel Combustion, Direct Air Capture (DAC)); By Service (Capture, Transportation, Utilization, Storage); By Deployment Type (Onshore CCUS Projects, Offshore CCUS Projects ); By Application (Oil & Gas, Power Generation, Cement, Steel & Metallurgy, Chemicals & Petrochemicals, Fertilizers, Hydrogen Production, Waste-to-Energy & Biomass); By Country (Germany, United Kingdom, Italy, France, Spain, Belgium, Russia, Netherlands, Rest of Europe); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Energy and Power

- Feb 2026

- Pages 250

- Report Format: pdf

- Report Price: $3000 USD

Europe CCUS Market, Size & Forecast 2021-2032

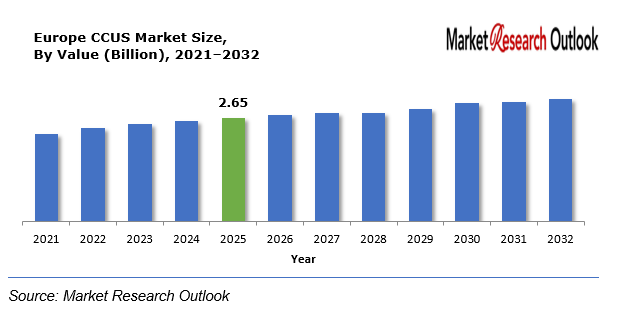

The Europe CCUS Market size was estimated at USD 2.65 Billion in 2025. During the forecast period, the Europe CCUS Market size is projected to grow at a CAGR of 48.2% reaching a value of USD 41.80 Billion by 2032. The Europe CCUS (Carbon Capture, Utilization, and Storage) market will show considerable expansion from 2026 until 2032 because European Union policies and national government backing will enforce more strict emission reduction requirements. The European Union climate neutrality commitment for 2050 drives investments in carbon capture technology development to create solutions for cement steel chemicals and power generation sectors which currently face difficulties in reducing emissions. The UK, Norway, Netherlands, and Germany implement major CCUS projects which create market opportunities through their development of CO₂ transportation and storage systems in the North Sea area. The European Union will become a top global CCUS market between 2026 and 2032 because the need for low-carbon hydrogen and industrial decarbonization efforts and public-private partnerships will drive CCUS technology adoption.

CCUS – Overview

CCUS (Carbon Capture, Utilization, and Storage) refers to a set of technologies which capture carbon dioxide (CO₂) emissions from industrial processes power plants and other sources and either use the captured carbon for different purposes or permanently store it underground to stop its atmospheric emission. CCUS plays a crucial role in reducing greenhouse gas emissions because it enables industrial decarbonization while helping countries achieve their net-zero climate targets through its protective measures against environmental damage caused by fossil fuel and heavy industry operations.

Europe CCUS Market

Growth Drivers

Growing Demand for Low-Carbon Hydrogen

The CCUS market in Europe grows because industries use blue hydrogen production to decrease carbon emissions while advancing their decarbonization goals which creates a growing need for low-carbon hydrogen. The CO₂ emissions which CCUS technologies capture and store during hydrogen production from fossil fuels create cleaner energy systems. The CCUS market for hydrogen production will experience substantial growth in upcoming years because of increased hydrogen infrastructure investments and European government backing for hydrogen initiatives.

Challenges

High Initial Capital Investment

The CCUS market faces its main obstacle because it needs substantial initial funding before it can begin building carbon capture and transportation and storage systems. The development of capture facilities, pipeline networks, and secure storage sites involves high installation and operational costs, which can limit adoption, particularly for small and medium-sized industries. The financial obstacles that exist in Europe because of uncertain long-term investment returns and undefined carbon pricing systems create delays in implementing CCUS projects at a large scale.

Geopolitical Impact on Europe CCUS Market

Geopolitical factors play a significant role in shaping the Europe CCUS market, particularly in relation to energy security, cross-border carbon transport, and climate policy alignment. Europe has accelerated its energy transition efforts together with its low-carbon technology development efforts because the Russia–Ukraine conflict has decreased Europe’s need to import fossil fuels. European nations are expanding their markets through successful cooperation to build common CO₂ transportation systems and offshore storage facilities for the North Sea region. The different national regulations together with their funding systems and political aims create difficulties for nations to work together on projects and secure funding. Geopolitical dynamics push Europe to build its domestic carbon management capabilities which will lead to permanent growth of the CCUS industry.

Europe CCUS Market

Segmental Coverage

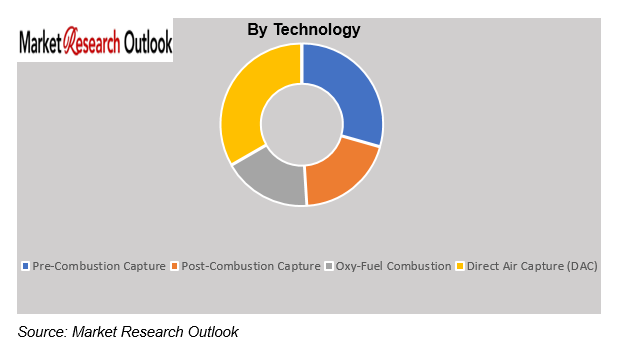

Europe CCUS Market – By Technology

Based on Technology, the Europe CCUS Market is segmented into Pre-Combustion Capture, Post-Combustion Capture, Oxy-Fuel Combustion, Direct Air Capture (DAC). The pre-combustion capture segment is expected to grow during the forecast period due to its increasing adoption in hydrogen production, power generation, and industrial processes that use fossil fuels as feedstock. The technology enables carbon dioxide removal before fuel combustion which makes it suitable for integrated gasification combined cycle power plants and blue hydrogen production facilities. The demand for low-carbon hydrogen combined with government policies that support clean energy and the growing investments in clean energy infrastructure across Europe will drive the pre-combustion capture segment expansion during the upcoming years.

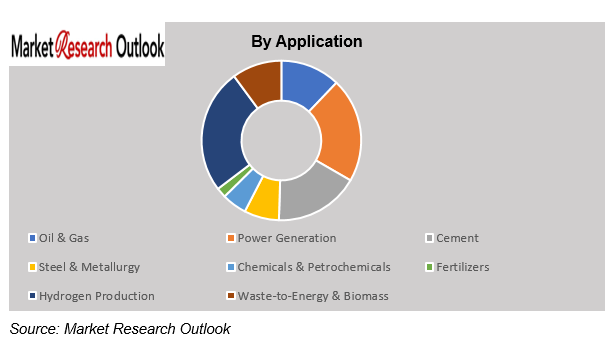

Europe CCUS Market – By Application

Based on application, the Europe CCUS Market is segmented into Oil & Gas, Power Generation, Cement, Steel & Metallurgy, Chemicals & Petrochemicals, Fertilizers, Hydrogen Production, Waste-to-Energy & Biomass. The oil and gas sector will experience growth during the upcoming forecast period because of rising implementation of CCUS technologies which help decrease carbon emissions from both upstream and downstream activities. European oil and gas companies are funding carbon capture technologies to achieve their decarbonization goals for refining and processing and hydrogen production processes while they comply with environmental regulations and net-zero targets. The oil and gas sector in the Europe CCUS market is expanding because of two factors which include using captured CO₂ for enhanced oil recovery (EOR) and establishing large-scale carbon storage hubs across regions like the North Sea.

Competitive Landscape

Key participants in the Europe CCUS market include Shell Plc, Equinor ASA, TotalEnergies SE, Siemens Energy, Aker Carbon Capture, Air Liquide, Linde plc, Technip Energies, Mitsubishi Heavy Industries (Europe operations), BASF SE and Other Prominent Players.

These companies are implementing strategic growth initiatives in order to gain a competitive advantage. The strategies being largely adopted include mergers and acquisitions, strategic alliances, joint ventures, licensing agreements, and new product launches. With the implementation of these strategies, the market participants aim to increase product portfolios, as well as enhance regional presence for long-term sustainable business growth in the CCUS industry of Europe.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | Europe |

| Product/ Service Segmentation | Technology, Service, Deployment Type, Application |

| Key Players | Shell Plc, Equinor ASA, TotalEnergies SE, Siemens Energy, Aker Carbon Capture, Air Liquide, Linde plc, Technip Energies, Mitsubishi Heavy Industries (Europe operations), BASF SE, and Other Prominent Players. |

Market Segmentation

- By Technology

- Pre-Combustion Capture

- Post-Combustion Capture

- Oxy-Fuel Combustion

- Direct Air Capture (DAC)

- By Service

- Capture

- Transportation

- Utilization

- Storage

- By Deployment Type

- Onshore CCUS Projects

- Offshore CCUS Projects

- By Application

- Oil & Gas

- Power Generation

- Cement

- Steel & Metallurgy

- Chemicals & Petrochemicals

- Fertilizers

- Hydrogen Production

- Waste-to-Energy & Biomass

- By Country

- Germany

- United Kingdom

- Italy

- France

- Spain

- Belgium

- Russia

- Netherlands

- Rest of Europe

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- Europe CCUS Market Insights

- Growth Drivers

- Restraints

- Opportunities

- Challenges

- Technology Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Industry Value Chain & Entry Points

- Europe CCUS Market: Regulatory Framework

- Europe CCUS Market: Marketing Strategies

- Europe CCUS Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- Pre-Combustion Capture

- Post-Combustion Capture

- Oxy-Fuel Combustion

- Direct Air Capture (DAC)

- By Service

- Capture

- Transportation

- Utilization

- Storage

- By Deployment Type

- Onshore CCUS Projects

- Offshore CCUS Projects

- By Application

- Oil & Gas

- Power Generation

- Cement

- Steel & Metallurgy

- Chemicals & Petrochemicals

- Fertilizers

- Hydrogen Production

- Waste-to-Energy & Biomass

- By Country

- Germany

- United Kingdom

- Italy

- France

- Spain

- Belgium

- Russia

- Netherlands

- Rest of Europe

- By Technology

- Market Size & Forecast, 2021-2032

- Germany CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- Market Size & Forecast, 2021-2032

- United Kingdom CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- Italy CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- France CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- Spain CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- Belgium CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- Russia CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- Netherlands CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- Rest of Europe CCUS Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Technology

- By Service

- By Deployment Type

- By Application

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution by End-Use Industry

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List of Key Players and Their Offerings

- Europe CCUS Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, etc.)

- Geopolitical Impact on Europe CCUS Market

- Company Profile

- Shell plc

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Shell plc

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

**(same data pointers will be provided for the below companies)

- Equinor ASA

- TotalEnergies SE

- Siemens Energy

- Aker Carbon Capture

- Air Liquide

- Linde plc

- Technip Energies

- Mitsubishi Heavy Industries (Europe operations)

- BASF SE

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown of Primary Research Respondents, By Region

- Assumption & Limitation

- Qualitative Research

* Financial information in case of non-listed companies will be provided as per availability

**The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. What is the expected growth rate of the Europe CCUS Market during the forecast period?

Ans: The Europe CCUS Market size was estimated at USD 2.65 billion in 2025.

2. What is the expected growth rate of the Europe CCUS Market during the forecast period?

Ans: Europe CCUS Market is expected to grow at a CAGR of around 48.2% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Europe CCUS Market by 2032?

Ans: The Europe CCUS Market is projected to reach a value of approximately USD 41.80 billion by 2032.

4. What are the major factors driving the growth of the Europe CCUS Market?

Ans: The Europe CCUS (Carbon Capture, Utilization, and Storage) market will show considerable expansion from 2026 until 2032 because European Union policies and national government backing will enforce more strict emission reduction requirements.

5. Name the key players operating in the Europe CCUS Market.

Ans: The key players of Europe CCUS Market are Shell Plc, Equinor ASA, TotalEnergies SE, Siemens Energy, Aker Carbon Capture, Air Liquide, Linde plc, Technip Energies, Mitsubishi Heavy Industries (Europe operations), BASF SE and Other Prominent Players.

6. Which is the fastest-growing application segment in the Europe CCUS Market?

Ans: The oil and gas sector will experience growth during the upcoming forecast period because of rising implementation of CCUS technologies which help decrease carbon emissions from both upstream and downstream activities.

7. Which country contributes significantly to the growth of the Europe CCUS Market?

Ans: Germany will show economic expansion during the forecast period because the country demonstrates strong dedication toward industrial decarbonization and climate neutrality targets. The country is investing heavily in carbon capture and storage infrastructure to reduce emissions from hard-to-abate industries such as steel, cement, and chemicals.

Frequently Asked Questions

1. What is the expected growth rate of the Europe CCUS Market during the forecast period?

Ans: The Europe CCUS Market size was estimated at USD 2.65 billion in 2025.

2. What is the expected growth rate of the Europe CCUS Market during the forecast period?

Ans: Europe CCUS Market is expected to grow at a CAGR of around 48.2% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Europe CCUS Market by 2032?

Ans: The Europe CCUS Market is projected to reach a value of approximately USD 41.80 billion by 2032.

4. What are the major factors driving the growth of the Europe CCUS Market?

Ans: The Europe CCUS (Carbon Capture, Utilization, and Storage) market will show considerable expansion from 2026 until 2032 because European Union policies and national government backing will enforce more strict emission reduction requirements.

5. Name the key players operating in the Europe CCUS Market.

Ans: The key players of Europe CCUS Market are Shell Plc, Equinor ASA, TotalEnergies SE, Siemens Energy, Aker Carbon Capture, Air Liquide, Linde plc, Technip Energies, Mitsubishi Heavy Industries (Europe operations), BASF SE and Other Prominent Players.

6. Which is the fastest-growing application segment in the Europe CCUS Market?

Ans: The oil and gas sector will experience growth during the upcoming forecast period because of rising implementation of CCUS technologies which help decrease carbon emissions from both upstream and downstream activities.

7. Which country contributes significantly to the growth of the Europe CCUS Market?

Ans: Germany will show economic expansion during the forecast period because the country demonstrates strong dedication toward industrial decarbonization and climate neutrality targets. The country is investing heavily in carbon capture and storage infrastructure to reduce emissions from hard-to-abate industries such as steel, cement, and chemicals.