South Africa Water and Wastewater Treatment Market, By Product Type (Membrane Separation Systems, Biological Treatment Systems, Disinfection Systems, Sludge Treatment Systems, Treatment Chemicals, Others); By Technology (Reverse Osmosis, Ultrafiltration, Activated Sludge, Membrane Bioreactor, Chlorination & UV Disinfection, Ion Exchange, Others); By Treatment Process (Primary Treatment, Secondary Treatment, Tertiary Treatment, Advanced Treatment, Others); By Distribution Channel (Direct Sales, Distributors & Dealers, OEM Suppliers, Aftermarket & Service Contracts, Government & Municipal Tenders, Others); By Application (Municipal, Industrial, Commercial & Institutional, Agriculture); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Chemicals & Advanced Materials

- Jul 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

South Africa Water and Wastewater Treatment Market: Water Scarcity, Infrastructure Investment and Industrial Reuse Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

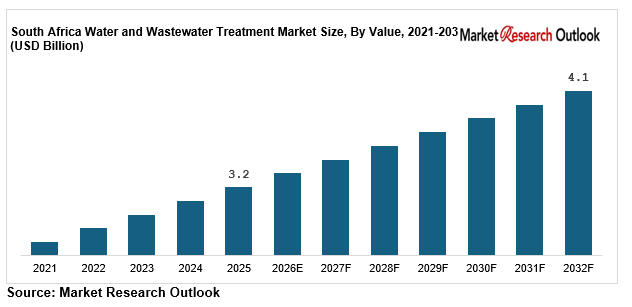

| Market Size (2025) | USD 3.2 Billion |

| CAGR (2026-2032) | 3.5% |

| Leading Segment | Municipal Application (Membrane Separation) |

| Fastest Growing Segment | Industrial & Tertiary Treatment |

| Market Size (2032) | USD 4.1 Billion |

Source: Market Research Outlook

Market Overview: South Africa Water and Wastewater Treatment Market

The South Africa water and wastewater treatment market size is witnessing steady expansion, driven by a deepening water crisis, growing municipal and industrial effluent volumes, rising urbanization, expanding regulatory enforcement, increasing demand for water reuse and recycling, and major investment in treatment plant refurbishment. Valued at USD 3.2 billion in 2025 and projected to reach USD 4.1 billion by 2032, growing at a CAGR of 3.5%, the South Africa water and wastewater treatment market growth is being fuelled by escalating water scarcity, rising government infrastructure spending, and the rapid adoption of membrane and advanced treatment technologies across municipal and industrial applications. Municipal treatment leads demand, while the industrial and tertiary treatment segments are emerging as the fastest growing categories. Deteriorating water quality, aging infrastructure, and rising pressure to meet effluent discharge standards are reshaping the supply landscape. As global technology majors including Veolia, SUEZ, Xylem, and Ecolab expand local capacity, and domestic specialists including WEC Projects, Proxa Water, and NuWater scale project pipelines, the South Africa water and wastewater treatment market is evolving into an investment-led, technology-driven, and reuse-focused ecosystem with steady long-term growth potential.

Key Report Takeaways: South Africa Water and Wastewater Treatment Market

- The South Africa water and wastewater treatment market size is projected to grow from USD 3.2 billion in 2025 to USD 4.1 billion by 2032, registering a steady CAGR of 3.5%, driven by escalating water scarcity, rising government infrastructure investment, and the structural shift toward advanced treatment and water reuse across the country.

- Municipal treatment dominates the South Africa water and wastewater treatment market, accounting for over 60% of total demand in 2025, driven by government-funded wastewater plants, rising urban effluent volumes, and the deep involvement of water boards such as Rand Water and Umgeni Water across metros and municipalities.

- Industrial and tertiary treatment are emerging as the fastest growing segments in the South Africa water and wastewater treatment market, expected to grow at 4.5% annually as mining companies, manufacturers, and food & beverage producers reshape water reuse strategies across Gauteng, the Western Cape, and industrial belts.

- Escalating water scarcity, with around 34% of South Africa’s water systems in high or critical risk in 2022 and non-revenue water losses near 41%, is structurally expanding the South Africa water and wastewater treatment market across municipal, industrial, and reuse categories.

- Rising investments by global and domestic players such as Veolia, SUEZ, Xylem, WEC Projects, and Proxa Water in membrane systems, plant refurbishment, and public-private partnerships are strengthening local capacity and supporting the South Africa water and wastewater treatment market forecast 2032.

Key Market Drivers: South Africa Water and Wastewater Treatment Market

Escalating Water Scarcity, Rising Pollution, and Urbanization Driving Water and Wastewater Treatment Demand Across South Africa

Growth in the South Africa water and wastewater treatment market is being driven by escalating water scarcity, rising water pollution, and rapid urbanization across metros and secondary cities. South Africa is a water-stressed country, with around 34% of its water systems in high or critical risk in 2022 according to the Department of Water and Sanitation. Non-revenue water losses reach around 41% nationally, while South Africans use around 234 litres per person daily, well above the global average of 173 litres. Deteriorating raw water quality, driven by river pollution, mining runoff, and failing sewage systems such as those affecting the Vaal Dam, is increasing demand for treatment across municipal and industrial applications. Only around 64% of households have access to reliable and safe water, indicating significant long-term investment need. Rising urban population, industrial effluent volumes, and mounting pressure to meet effluent discharge standards are creating strong structural demand across the South Africa water and wastewater treatment market.

Rising Government Infrastructure Investment, Regulatory Enforcement, and Municipal Plant Upgrades Fuelling Treatment Demand

The South Africa water and wastewater treatment market is benefiting from rising government infrastructure investment, stricter regulatory enforcement, and large-scale municipal plant upgrades. Under the National Development Plan 2030, the government is targeting universal access to safe water and improved sanitation, supported by the Department of Water and Sanitation and water boards. The Green Drop and Blue Drop regulatory programs have intensified compliance pressure, with around 39% of municipal wastewater treatment works, or 334 of 850 plants, found in critical condition in the 2022 Green Drop report. This has triggered refurbishment, capacity expansion, and monitoring investment across provinces. Primary treatment dominates the process landscape with around 45% share, while tertiary treatment is expanding fastest. Rising public spending, donor funding, and municipal grants have further strengthened organized demand, supporting the South Africa water and wastewater treatment market.

Industrial Water Reuse, Mining Effluent Treatment, and Technology Modernization Strengthening Treatment Demand

Rapid growth in industrial water reuse, mining effluent treatment, and technology modernization is a major catalyst for the South Africa water and wastewater treatment market, with the industrial application segment projected to grow at around 4.5% annually through 2032. Water-intensive sectors including mining, power generation, chemicals, and food and beverage face rising water costs and discharge regulations, driving adoption of on-site treatment and reuse. Membrane separation leads the equipment landscape with around 35% share, driven by reverse osmosis and ultrafiltration adoption for high-recovery reuse. Acid mine drainage treatment, zero-liquid-discharge systems, and desalination are gaining traction, particularly in the Western Cape following recurring drought. Global technology players such as Veolia, SUEZ, Xylem, and Ecolab, alongside domestic specialists including WEC Projects, Proxa Water, and NuWater, have scaled modular and advanced treatment pipelines. Industrial reuse programs combined with corporate water-stewardship targets are structurally expanding South Africa water and wastewater treatment market growth across all major applications through 2032.

Key Market Challenges: South Africa Water and Wastewater Treatment Market

Aging Infrastructure, Failing Municipal Plants, and High Non-Revenue Water Losses

The South Africa water and wastewater treatment market continues to face challenges around aging infrastructure, failing municipal plants, and high water losses, with around 39% of municipal wastewater treatment works in critical condition in 2022. While regulatory programs such as Green Drop and growing investment have improved oversight, non-revenue water losses remain near 41% nationally, reflecting bottlenecks in maintenance, metering, and leak repair. The largest plant, the Cape Flats wastewater treatment works, scored 0% for microbiological compliance in 2020 and 2021, underscoring the scale of the backlog. Deferred maintenance, deteriorating pump stations, and overloaded facilities across municipalities create operational complexity for utilities and contractors operating nationally. While national grants and refurbishment programs continue, infrastructure decay remains a near-term challenge for the South Africa water and wastewater treatment market.

Funding Constraints, Skills Shortages, and Maintenance Backlogs Across Municipalities

The South Africa water and wastewater treatment market faces structural complexity from municipal funding constraints, skills shortages, and maintenance backlogs across different provinces. While metros such as Johannesburg, Cape Town, Durban, and Tshwane maintain relatively capable utilities, many smaller municipalities operate with limited budgets, weak revenue collection, and few qualified engineers and process controllers. A shortage of skilled technical staff is a key bottleneck in operating advanced treatment plants and meeting discharge standards. Differential availability of funding, technical capacity, and operational reliability across municipalities creates complexity for technology suppliers and EPC contractors operating nationally. While the Department of Water and Sanitation and development finance institutions provide support, funding and capacity fragmentation remains a near-term challenge for the South Africa water and wastewater treatment market.

Volatility in Energy Costs, Load-Shedding, and Chemical Prices Impacting Treatment Operations

The South Africa water and wastewater treatment market faces practical constraints around energy cost volatility, load-shedding, and treatment chemical price inflation across operations. Treatment plants are energy-intensive, and recurring load-shedding disrupts pumping, aeration, and disinfection, forcing investment in backup power and raising operating costs. Prices for treatment chemicals such as chlorine, coagulants, and polymers have risen over recent years, pressuring municipal and industrial operating budgets. Average operating margins for private treatment contractors remain modest, reducing the effective returns on new projects. Energy-efficient systems, renewable-powered plants, and chemical optimization are emerging as solutions, but capital constraints and reliability concerns remain barriers to widespread adoption across the South Africa water and wastewater treatment market.

Key Market Trends: South Africa Water and Wastewater Treatment Market

Rapid Adoption of Membrane Filtration, Water Reuse, and Desalination in South Africa

The South Africa water and wastewater treatment market is undergoing a clear technology shift toward membrane filtration, water reuse, and desalination, with these advanced solutions expected to capture a rising share of new treatment capacity by 2027. Reverse osmosis and ultrafiltration deliver high recovery rates for reuse and desalination, while membrane bioreactors improve effluent quality for discharge and recycling. Leading global and domestic players including Veolia, SUEZ, Xylem, and NuWater have scaled membrane, reuse, and desalination capacity through 2024 and 2025. Water reuse and zero-liquid-discharge systems are also gaining traction, particularly in the Western Cape following recurring drought and in mining regions such as Gauteng and Mpumalanga, where operators are adopting acid mine drainage treatment and reclaimed-water schemes. This technology transition is reinforcing the South Africa water and wastewater treatment market forecast 2032 across both municipal and industrial applications.

Growth of Public-Private Partnerships and Private Water Treatment Investment in the South Africa Water and Wastewater Treatment Market

A clear shift toward public-private partnerships and private water treatment investment is reshaping the South Africa water and wastewater treatment market, particularly across constrained municipalities. Faced with funding and capacity gaps, municipalities are increasingly partnering with private operators to finance, build, and operate treatment facilities. In 2023, the City of Cape Town partnered with an international water management company to develop wastewater treatment capacity addressing regional water supply. Build-operate-transfer and concession models are expanding, with private specialists including WEC Projects, Proxa Water, NuWater, and Quality Filtration Systems delivering modular and package plants. Development finance institutions and blended-finance structures are reducing project costs and accelerating treatment capacity across both municipal and industrial segments of the South Africa water and wastewater treatment market. Private investment now accounts for a rising share of new treatment capacity, up from earlier years, as government seeks to close the infrastructure gap.

Capacity Expansion, Plant Refurbishment, and Digital Smart-Water Monitoring

A wave of capacity expansion, plant refurbishment, and digital monitoring is reshaping the South Africa water and wastewater treatment market supply landscape. Combined public and private capital commitments in water and sanitation infrastructure run into billions of rand annually, targeting refurbishment of failing plants and new capacity. Water boards such as Rand Water and Umgeni Water are expanding bulk treatment capacity, while metros refurbish overloaded works. Digital and smart-water technologies, including remote monitoring, telemetry, and process automation, are being adopted to improve compliance and reduce losses. Green Drop and Blue Drop regulatory pressure, National Development Plan 2030 targets, and rising industrial reuse have structurally favoured organized supply. Combined with public-private partnerships and technology modernization scaling rapidly, these developments are reinforcing the South Africa water and wastewater treatment market forecast 2032 across the entire value chain.

Segmental Insights: South Africa Water and Wastewater Treatment Market

By Application: Municipal Segment Dominates the South Africa Water and Wastewater Treatment Market

The municipal application segment dominates the South Africa water and wastewater treatment market, accounting for an estimated 60% of total demand, driven by government-funded treatment plants, rising urban effluent volumes, and improving regulatory enforcement. Membrane separation and biological treatment are the dominant technologies within this segment, with water boards and metros accounting for the bulk of municipal treatment demand. The industrial application segment contributes another 30% of demand, driven by mining, power, chemicals, and food and beverage operators adopting on-site treatment and reuse. The commercial and institutional segment accounts for around 7%, led by hospitals, malls, and estates, while agriculture and others make up the balance. In 2025, leading players including Veolia, SUEZ, Xylem, and WEC Projects scaled up municipal and industrial treatment deployment under refurbishment and reuse programs, reinforcing segment dominance in the South Africa water and wastewater treatment market.

By Product Type: Membrane Separation Leads While Tertiary Treatment and Reuse Systems Grow Fastest

Membrane separation systems lead the South Africa water and wastewater treatment market product landscape, accounting for approximately 35% of total demand, driven by high-recovery reuse, desalination, and superior effluent quality. Biological treatment and disinfection systems together contribute another 40%, primarily across municipal sewage and industrial effluent applications. Tertiary and advanced treatment systems are the fastest growing categories within the South Africa water and wastewater treatment market, expanding at around 5% annually, driven by reuse mandates, stricter discharge standards, and growing adoption in water-scarce regions. Sludge treatment systems and treatment chemicals account for the remaining share, serving both municipal and industrial operators. Leading suppliers including Veolia, SUEZ, Xylem, Ecolab, and Improchem have aligned portfolios to this product mix, driving advanced treatment adoption across the South Africa water and wastewater treatment market.

Regional Insights: South Africa Water and Wastewater Treatment Market

Regional analysis of the South Africa water and wastewater treatment market shows that Gauteng and the Western Cape collectively account for approximately 54% of total treatment demand, driven by Johannesburg and Tshwane (industrial and municipal hub), Ekurhuleni, and Cape Town (drought-driven reuse and desalination), supported by dense urban populations and strong industrial activity. Gauteng leads with around 34% of demand, supported by mining, manufacturing, and the largest municipal effluent volumes around the Vaal system. The Western Cape contributes around 20%, led by Cape Town reuse and desalination projects. KwaZulu-Natal accounts for around 18%, driven by Durban’s industrial and port economy, while the Eastern Cape contributes around 13%. The rest of South Africa, including Mpumalanga mining regions and the Free State, makes up the balance. In 2025, capacity additions and projects by Veolia, SUEZ, Xylem, WEC Projects, and Proxa Water across Gauteng, the Western Cape, and KwaZulu-Natal reinforced regional supply hubs, supporting closer execution of municipal and industrial treatment projects across the South Africa water and wastewater treatment market.

Recent Developments: South Africa Water and Wastewater Treatment Market

- The South Africa water and wastewater treatment market witnessed steady momentum in projects and capacity progress during 2024 and 2025. Municipalities and water boards accelerated refurbishment of failing wastewater treatment works, supported by national grants and Green Drop regulatory pressure. Private treatment investment expanded, with build-operate-transfer and package-plant projects growing across provinces. Cumulative treated water and wastewater volumes in South Africa continue to rise steadily, driven by urban growth and industrial reuse, with reuse and desalination capacity expanding fastest across the Western Cape and Gauteng.

- Domestic and global players have deepened South Africa-focused capacity expansion. In 2025, Veolia, SUEZ, and Xylem advanced membrane and reuse projects, while domestic specialists WEC Projects, Proxa Water, and NuWater commissioned modular and package treatment plants for municipal and industrial clients. Cape Town continued to progress reuse and desalination programs following recurring drought, and mining operators in Gauteng and Mpumalanga expanded acid mine drainage and reclaimed-water schemes. These developments are strengthening local capacity and supporting the South Africa water and wastewater treatment market forecast 2032.

- Public-private partnership and reuse momentum has gained strong traction in the South Africa water and wastewater treatment market. In 2025, municipalities expanded partnerships with private operators to finance and operate treatment facilities, while industrial users deepened water-stewardship and reuse commitments. Strategic collaboration between water boards, private specialists, and technology suppliers is positioning South Africa as one of the most active water-treatment markets in the region, strengthening long-term competitive positioning in the South Africa water and wastewater treatment market forecast 2032.

Key Market Players: South Africa Water and Wastewater Treatment Market

- Veolia Water Technologies South Africa (Pty) Ltd

- SUEZ Water Technologies & Solutions

- Xylem Water Solutions South Africa (Pty) Ltd

- Ecolab (Nalco Water) South Africa

- Kurita Water Industries Ltd

- Aquatech International LLC

- WEC Projects (Pty) Ltd

- Talbot & Talbot (Pty) Ltd

- Improchem (Pty) Ltd

- Proxa Water (Pty) Ltd

- NuWater (Pty) Ltd

- Quality Filtration Systems (Pty) Ltd

- Grundfos South Africa (Pty) Ltd

Report Scope

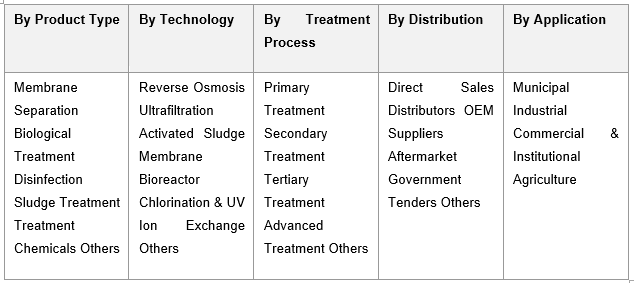

In this report, the South Africa Water and Wastewater Treatment Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Membrane Separation Systems

- Biological Treatment Systems

- Disinfection Systems

- Sludge Treatment Systems

- Treatment Chemicals

- Others

- By Technology

- Reverse Osmosis (RO)

- Ultrafiltration & Nanofiltration

- Activated Sludge

- Membrane Bioreactor (MBR)

- Chlorination & UV Disinfection

- Ion Exchange

- Others

- By Treatment Process

- Primary Treatment

- Secondary Treatment

- Tertiary Treatment

- Advanced Treatment

- Others

- By Distribution Channel

- Direct Sales (EPC & System Integrators)

- Distributors & Dealers

- OEM Equipment Suppliers

- Aftermarket & Service Contracts

- Government & Municipal Tenders

- Others

- By Application

- Municipal

- Industrial

- Commercial & Institutional

- Agriculture

- By Geography

- Gauteng

- Western Cape

- KwaZulu-Natal

- Eastern Cape

- Rest of South Africa

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the South Africa Water and Wastewater Treatment Market, including business overview, product portfolio, financial performance, and strategic developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic water treatment specialists, package and modular treatment plant providers, regional EPC contractors, or niche municipal and industrial service brands.

The South Africa Water and Wastewater Treatment Market report is part of our ongoing research coverage. For early access, customised insights, or to discuss a tailored scope, please connect with our research team.

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Technology

- By Treatment Process

- By Distribution Channel

- By Application

- By Region

- Analyst Recommendations

- Geopolitical Impact on South Africa Water and Wastewater Treatment Market

- South Africa Water and Wastewater Treatment Market Insights

- Market Dynamics

- Growth Drivers

- Escalating water scarcity, rising pollution, and urbanization driving water and wastewater treatment demand across South Africa.

- Rising government infrastructure investment, regulatory enforcement, and municipal plant upgrades fuelling treatment demand.

- Industrial water reuse, mining effluent treatment, and technology modernization strengthening treatment demand.

- Restraints

- Aging infrastructure, failing municipal plants, and high non-revenue water losses limiting treatment reliability across South Africa.

- Funding constraints, skills shortages, and maintenance backlogs restricting treatment capacity across municipalities.

- Volatility in energy costs, load-shedding, and chemical prices impacting overall water and wastewater treatment operations.

- Opportunities

- Membrane filtration, water reuse, and desalination innovation opening untapped reuse pools across water-scarce regions.

- Advanced tertiary treatment and zero-liquid-discharge systems supporting next-generation growth in industrial and municipal segments.

- Public-private partnerships, private investment, and modular treatment plants creating massive capacity opportunities.

- Challenges

- Intense competition among global technology majors, domestic EPC specialists, and small treatment contractors.

- Limited municipal funding and inconsistent operational capacity across smaller South African towns.

- Maintaining compliance, effluent quality, and plant reliability at scale across diverse South African municipalities.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Inputs (raw and surface water, membranes, pumps, treatment chemicals, equipment, instrumentation)

- Treatment Equipment & Technology Manufacturers (Veolia, SUEZ, Xylem, Kurita, Grundfos)

- Treatment Chemical Suppliers (Improchem, Ecolab, Kurita, coagulants, disinfectants, polymers)

- EPC Contractors & System Integrators (WEC Projects, Proxa Water, NuWater, Quality Filtration Systems)

- Quality Control, R&D & Testing Laboratories (SABS, SANS standards, DWS Green & Blue Drop, ISO)

- Water Boards & Municipal Utilities (Rand Water, Umgeni Water, Johannesburg Water, City of Cape Town)

- Industrial End-Users (mining, power, chemicals, food & beverage operators)

- Operations, Maintenance & Service Providers (plant O&M, monitoring, refurbishment contractors)

- Reuse, Discharge & Distribution (reclaimed water, industrial reuse, municipal distribution networks)

- End-Users (households, municipalities, industries, commercial and institutional users)

- South Africa Water and Wastewater Treatment Market: Regulatory Framework

- South Africa Water and Wastewater Treatment Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- By Volume (Million Cubic Metres)

- Market Share & Forecast

- By Product Type

- Membrane Separation Systems

- Biological Treatment Systems

- Disinfection Systems

- Sludge Treatment Systems

- Treatment Chemicals

- Others

- By Technology

- Reverse Osmosis (RO)

- Ultrafiltration & Nanofiltration

- Activated Sludge

- Membrane Bioreactor (MBR)

- Chlorination & UV Disinfection

- Ion Exchange

- Others

- By Treatment Process

- Primary Treatment

- Secondary Treatment

- Tertiary Treatment

- Advanced Treatment

- Others

- By Distribution Channel

- Direct Sales (EPC & System Integrators)

- Distributors & Dealers

- OEM Equipment Suppliers

- Aftermarket & Service Contracts

- Government & Municipal Tenders

- Others

- By Application

- Municipal

- Industrial

- Commercial & Institutional

- Agriculture

- By Geography

- Gauteng

- Western Cape

- KwaZulu-Natal

- Eastern Cape

- Rest of South Africa

- Competitive Landscape

- South Africa Water and Wastewater Treatment Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Veolia Water Technologies South Africa (Pty) Ltd

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

(Same Data Pointers Will Be Provided for The Below Companies)

- SUEZ Water Technologies & Solutions

- Xylem Water Solutions South Africa (Pty) Ltd

- Ecolab (Nalco Water) South Africa

- Kurita Water Industries Ltd

- Aquatech International LLC

- WEC Projects (Pty) Ltd

- Talbot & Talbot (Pty) Ltd

- Improchem (Pty) Ltd

- Proxa Water (Pty) Ltd

- NuWater (Pty) Ltd

- Quality Filtration Systems (Pty) Ltd

- Grundfos South Africa (Pty) Ltd

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the South Africa water and wastewater treatment market and what is its growth forecast?

Ans: The South Africa water and wastewater treatment market is valued at USD 3.2 billion in 2025 and projected to reach USD 4.1 billion by 2032, growing at a CAGR of 3.5%, supported by water scarcity, infrastructure investment, and industrial reuse.

2. Which segments are driving demand in the South Africa water and wastewater treatment market?

Ans: Municipal treatment leads with around 60% share and membrane separation holds about 35%, while industrial and tertiary treatment are the fastest-growing segments, driven by water reuse, mining effluent, and stricter discharge standards.

3. What are the key drivers of growth in the South Africa water and wastewater treatment market?

Ans: Key drivers include escalating water scarcity, rising water pollution, growing urbanization, increased government infrastructure investment, stricter regulatory enforcement, and rising industrial water reuse across the mining, power, and manufacturing sectors of South Africa.

4. Which regions are driving growth in the South Africa water and wastewater treatment market?

Ans: Gauteng and the Western Cape lead with around 54% of demand, driven by Johannesburg, Tshwane, and Cape Town, while KwaZulu-Natal and the Eastern Cape also show strong and rising water treatment demand.

5. What are the latest trends in the South Africa water and wastewater treatment market?

Ans: The latest trends include rising membrane filtration and desalination, growth in water reuse and zero-liquid-discharge, public-private partnerships, plant refurbishment, and digital smart-water monitoring across both municipal and industrial water treatment operations.

Frequently Asked Questions

1. How large is the South Africa water and wastewater treatment market and what is its growth forecast?

Ans: The South Africa water and wastewater treatment market is valued at USD 3.2 billion in 2025 and projected to reach USD 4.1 billion by 2032, growing at a CAGR of 3.5%, supported by water scarcity, infrastructure investment, and industrial reuse.

2. Which segments are driving demand in the South Africa water and wastewater treatment market?

Ans: Municipal treatment leads with around 60% share and membrane separation holds about 35%, while industrial and tertiary treatment are the fastest-growing segments, driven by water reuse, mining effluent, and stricter discharge standards.

3. What are the key drivers of growth in the South Africa water and wastewater treatment market?

Ans: Key drivers include escalating water scarcity, rising water pollution, growing urbanization, increased government infrastructure investment, stricter regulatory enforcement, and rising industrial water reuse across the mining, power, and manufacturing sectors of South Africa.

4. Which regions are driving growth in the South Africa water and wastewater treatment market?

Ans: Gauteng and the Western Cape lead with around 54% of demand, driven by Johannesburg, Tshwane, and Cape Town, while KwaZulu-Natal and the Eastern Cape also show strong and rising water treatment demand.

5. What are the latest trends in the South Africa water and wastewater treatment market?

Ans: The latest trends include rising membrane filtration and desalination, growth in water reuse and zero-liquid-discharge, public-private partnerships, plant refurbishment, and digital smart-water monitoring across both municipal and industrial water treatment operations.