India 4-Octylphenol Market, By Purity Grade (99% Purity, 99.5% Purity, Others); By Application (Phenolic Resins, Nonionic Surfactants, Rubber & Tyre Additives, Adhesives & Sealants, Lubricant Additives, Others); By Form (Flakes, Molten, Granules, Lumps, Prills); By Distribution Channel (Direct Sales, Distributors & Traders, Online B2B Platforms, Specialty Chemical Dealers, Bulk Supply Contracts, Others); By End-Use Industry (Automotive, Construction, Electronics, Agrochemicals); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Chemicals & Advanced Materials

- Jun 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India 4-Octylphenol Market: Phenolic Resin Demand, Surfactant Growth and High-Purity Innovation Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

| Market Size (2025) | USD 62 Million |

| CAGR (2026-2032) | 6.3% |

| Leading Segment | 99% Purity Grade (Phenolic Resins) |

| Fastest Growing Segment | 99.5% High-Purity Grade (Nonionic Surfactants) |

| Market Size (2032) | USD 95 Million |

Source: Market Research Outlook

Market Overview: India 4-Octylphenol Market

The India 4-Octylphenol market size is witnessing rapid expansion, driven by accelerating phenolic resin demand for 4-Octylphenol, growing nonionic surfactant consumption of 4-Octylphenol, rising industrialization, expanding paints and coatings demand for 4-Octylphenol, increasing demand for high-purity 4-Octylphenol grades, and major capacity additions by domestic 4-Octylphenol majors. Valued at USD 62 million in 2025 and projected to reach USD 95 million by 2032, growing at a CAGR of 6.3%, the India 4-Octylphenol market growth is being fuelled by strong demand from the resin, rubber and agrochemical sectors, rising automotive and construction demand for 4-Octylphenol, and the rapid scaling of domestic alkylphenol production across western and southern India. The 99% purity 4-Octylphenol grade leads consumption, while the 99.5% high-purity 4-Octylphenol segment is emerging as the fastest growing category. Shifting buyer preferences toward consistent-quality 4-Octylphenol, growing surfactant awareness, and rising demand for durable resin systems are reshaping the supply landscape. As domestic majors including Prasol Chemicals, SI Group India, and integrated 4-Octylphenol producers expand capacity, and global chemical majors including Sasol, DIC Corporation, and ICC Industries scale supply pipelines, the India 4-Octylphenol market is evolving into a demand-led, innovation-driven, and capacity-enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India 4-Octylphenol Market

- The India 4-Octylphenol market size is projected to grow from USD 62 million in 2025 to USD 95 million by 2032, registering a strong CAGR of 6.3%, driven by accelerated phenolic resin demand, rising surfactant consumption, and the structural shift toward high-purity 4-Octylphenol grades across industrial India.

- The 99% purity 4-Octylphenol grade dominates the India 4-Octylphenol market, accounting for over 68% of total 4-Octylphenol volume in 2025, driven by its cost-effective use in surfactants and resins, the deep presence of producers such as Prasol Chemicals, SI Group, and DIC Corporation, and rising industrial demand across phenolic resin and rubber additive applications.

- The 99.5% high-purity 4-Octylphenol grade and nonionic surfactant applications are emerging as the fastest growing segments in the India 4-Octylphenol market, expected to grow at 8% to 11% annually as high-performance resin makers, surfactant formulators, and quality-focused buyers reshape sourcing strategies across western and southern industrial clusters.

- Rapid scaling of phenolic resin and surfactant capacity, with domestic 4-Octylphenol consumption crossing 38 thousand tonnes across India by 2025 and projected expansion toward 50 thousand tonnes by 2030, is structurally expanding the India 4-Octylphenol market across resins, rubber additives, and agrochemical categories.

- Rising investments by domestic chemical majors such as Prasol Chemicals, SI Group India, and integrated 4-Octylphenol producers in production capacity, high-purity processing, and backward-integrated phenol supply are strengthening local supply and supporting the India 4-Octylphenol market forecast 2032.

Key Market Drivers: India 4-Octylphenol Market

Rising Industrialization, Phenolic Resin Expansion, and Surfactant Demand Driving 4-Octylphenol Consumption Across India

Growth in the India 4-Octylphenol market is being driven by rapid industrialization, the rise of phenolic resin demand, and aggressive expansion of surfactant and rubber additive output across western, southern, and northern industrial belts. India’s manufacturing output rose steadily through 2025, with the chemical sector contributing over 7% of national GDP. Domestic phenolic resin capacity expanded notably between 2020 and 2025, led by demand from paints, coatings, adhesives, plywood, and tyre applications. High-purity 4-Octylphenol has become a critical intermediate for these segments, with average prices ranging between INR 110 and INR 165 per kilogram. Per-capita industrial consumption of 4-Octylphenol intermediates in India remains modest, indicating significant long-term headroom for growth. Rising automotive production, expanding construction activity, and growing agrochemical formulation demand are creating strong structural pull-through demand across the India 4-Octylphenol market.

Expanding Automotive Output, Rising Construction Activity, and Shifting Resin Preferences Fuelling High-Purity 4-Octylphenol Adoption

The India 4-Octylphenol market is benefiting from sustained growth in industrial output, with the automotive and construction sectors expanding steadily between 2014 and 2024, alongside continued cost reductions in modern alkylphenol processing, aseptic handling, and bulk logistics. Average prices of 4-Octylphenol in India now range between INR 110 and INR 165 per kilogram, with high-purity 99.5% 4-Octylphenol grades commanding INR 175 to INR 240 per kilogram. Domestic specialty chemical capacity has scaled rapidly, with combined 4-Octylphenol throughput rising steadily by 2025, led by Prasol Chemicals, SI Group, DIC Corporation, and integrated producers. BIS quality standards, REACH-aligned export norms, and growing trust in consistent-grade intermediates have further strengthened organized supply, supporting price competitiveness across the India 4-Octylphenol market. End-use industries including automotive and construction now account for over 60% of 4-Octylphenol consumption, with resin and surfactant buyers preferring high-purity grades, consistent 4-Octylphenol supply, and reliable 4-Octylphenol lead times.

Process Innovation in High-Purity, Low-Impurity, and Specialty 4-Octylphenol Grades Strengthening Industrial Segment Growth

Rapid growth in high-purity and specialty grades is a major catalyst for the India 4-Octylphenol market, with the 99.5% purity segment projected to grow at 8% to 11% annually through 2032. High-performance resin and surfactant systems require low-impurity inputs, creating strong demand for consistent, ultra-clean 4-Octylphenol. Quality-focused buyer behavior under high-durability material trends, performance-based formulation targets, and growing supply-security awareness are driving large consumers toward premium-grade 4-Octylphenol consumption. India’s tightening BIS and pollution-control norms in 2024 have increased transparency for industrial buyers, accelerating high-purity 4-Octylphenol adoption to hedge against quality and compliance concerns. Leading producers such as Prasol Chemicals, SI Group, DIC Corporation, Sasol, and ICC Industries have scaled high-purity and surfactant-grade 4-Octylphenol pipelines, with the nonionic surfactant segment alone representing an estimated USD 18 million addressable opportunity within Indian cleaning and agrochemical markets. Make in India incentives combined with import-substitution-led procurement are structurally expanding India 4-Octylphenol market growth across all major end-use categories through 2032.

Key Market Challenges: India 4-Octylphenol Market

Endocrine-Disruptor Scrutiny and Tightening Environmental Regulation Limiting Unrestricted 4-Octylphenol Use

The India 4-Octylphenol market continues to face challenges around endocrine-disruptor scrutiny and tightening environmental controls, as 4-Octylphenol is classified as a substance of concern under several global frameworks including REACH and TSCA. While Indian producers have improved effluent handling and worker-safety compliance, regulatory caution restricts certain consumer-facing and aquatic-exposure applications, reflecting bottlenecks in toxicity awareness, ecological concerns, and approval timelines. Environmental agencies continue to caution against unrestricted discharge of alkylphenol residues into water bodies, while safer substitute intermediates for sensitive applications remain under development. India’s exposure to evolving global chemical-safety norms limits adoption across certain regulated end-uses within the India 4-Octylphenol market.

Raw Material Dependence on Phenol and Diisobutylene Across Domestic Supply Chains

The India 4-Octylphenol market faces structural complexity from its dependence on phenol and diisobutylene, the two key feedstocks used in 4-Octylphenol synthesis. While integrated producers such as Prasol Chemicals and SI Group manage backward-linked feedstock access, smaller manufacturers remain exposed to phenol price swings and import reliance for diisobutylene. Domestic phenol availability is closely tied to petrochemical cycles, and any tightening in upstream supply directly raises 4-Octylphenol production costs. Differential access to feedstock, captive utilities, and reliable power across states creates operational complexity for 4-Octylphenol players operating pan-India. While Make in India and PCPIR petrochemical clusters have improved feedstock security, supply-chain fragmentation remains a near-term challenge for the India 4-Octylphenol market.

Volatility in Phenol Prices and Energy Costs Impacting Overall 4-Octylphenol Margins

The India 4-Octylphenol market faces practical constraints around feedstock price volatility, energy cost inflation, and margin compression across the value chain. Indian phenol prices have risen by 12% to 18% between 2022 and 2025, while energy and utility input costs have moved up by 8% to 14% over the same period. Smaller 4-Octylphenol producers face additional complexity in passing through cost increases without losing volume. Average gross margins for domestic 4-Octylphenol intermediates range between 14% and 22%, reducing the effective profitability of new capacity by 4% to 10%. High-purity grades, process-efficiency upgrades, and backward integration into phenol are emerging as solutions to differentiate, but capital intensity and regulatory compliance remain barriers to rapid expansion across the India 4-Octylphenol market.

Key Market Trends: India 4-Octylphenol Market

Rapid Adoption of High-Purity, Surfactant-Grade, and Specialty 4-Octylphenol in India

The India 4-Octylphenol market is undergoing a clear technology shift toward high-purity, surfactant-grade, and specialty 4-Octylphenol, with these advanced grades expected to capture over 18% of new alkylphenol demand by 2027. High-purity 99.5% grades deliver lower impurity profiles suited to advanced 4-Octylphenol resin and surfactant systems, compared to standard 99% 4-Octylphenol grades used in general industrial 4-Octylphenol applications. Leading domestic and global producers including Prasol Chemicals, SI Group, DIC Corporation, Sasol, and ICC Industries have scaled high-purity and surfactant-grade 4-Octylphenol production capacity through 2024 and 2025. Specialty 4-Octylphenol grades tailored for ethoxylates, UV stabilizers, and lubricant additives are also gaining traction, particularly in western and southern industrial clusters where formulators are rising, with producers offering performance-positioned 4-Octylphenol variants for high-spec buyers. This grade transition is reinforcing the India 4-Octylphenol market forecast 2032 across both resin and surfactant categories.

Growth of Nonionic Surfactant, Ethoxylate, and Agrochemical Demand in the India 4-Octylphenol Market

A clear shift toward nonionic surfactants, ethoxylates, and agrochemical formulations is reshaping the India 4-Octylphenol market, particularly in the cleaning and crop-protection segment. As a precursor to 4-Octylphenol ethoxylates, 4-Octylphenol supports emulsifiers, wetting agents, and dispersants used across detergents, textiles, and agrochemical sprays. Leading surfactant and agrochemical formulators have built combined demand spanning hundreds of industrial sites, with 4-Octylphenol ranking among the key 4-Octylphenol intermediates consumed. Domestic ethoxylate makers such as Matangi Industries, Venus Ethoxyethers, and allied surfactant producers are also reducing import dependence and accelerating 4-Octylphenol adoption across both resin and surfactant segments of the India 4-Octylphenol market. By 2025, surfactant and agrochemical applications account for a rising share of 4-Octylphenol consumption in India, up from a smaller base in 2020, with formulators increasingly preferring consistent domestic supply over imported 4-Octylphenol.

Capacity Expansion by Domestic Alkylphenol Producers and High-Purity Processing Investments

A wave of domestic capacity expansion and high-purity processing investments is reshaping the India 4-Octylphenol market supply landscape. Combined India-focused capital expenditure announcements across specialty chemical and alkylphenol capacity rose steadily across 2023 to 2025. Prasol Chemicals expanded acetone-based and alkylphenol-linked capacity across its Khopoli and Mahad units, SI Group scaled 4-Octylphenol intermediates for resin customers, integrated producers commissioned new high-purity lines for western India, and downstream surfactant makers expanded ethoxylation facilities. BIS standard upgrades, Production Linked Incentive (PLI) allocations for chemicals and petrochemicals, and import-substitution incentives have structurally favoured domestic supply. Combined with phenolic resin demand driving industrial offtake and surfactant procurement scaling rapidly, these developments are reinforcing the India 4-Octylphenol market forecast 2032 across the entire value chain.

Segmental Insights: India 4-Octylphenol Market

By End-Use Industry: Automotive and Construction Dominate the India 4-Octylphenol Market

The automotive and construction end-use industries dominate the India 4-Octylphenol market, accounting for an estimated 38% to 42% of total volume, driven by rising 4-Octylphenol demand from vehicle production, expanding infrastructure activity, and improving resin and rubber additive economics. Phenolic resins and rubber compounding are the dominant applications within this segment, with 99% purity grades capturing over 72% of industrial 4-Octylphenol purchases. The chemicals and surfactant segment contributes another 24% to 27% of demand, driven by detergent, textile, and agrochemical formulators adopting 4-Octylphenol ethoxylates. The electronics segment accounts for 22% to 24%, led by coatings, encapsulants, and stabilizer applications. In 2025, leading producers including Prasol Chemicals, SI Group, DIC Corporation, and Sasol scaled up resin and surfactant-focused 4-Octylphenol supply under capacity expansion, reinforcing segment dominance in the India 4-Octylphenol market.

By Purity Grade: 99% Grade Leads While 99.5% High-Purity Grows Fastest

The 99% purity 4-Octylphenol grade leads the India 4-Octylphenol market landscape, accounting for approximately 68% of total 4-Octylphenol volume, driven by its balanced reactivity, deep industrial 4-Octylphenol usage, and improving cost economics. Standard industrial grades contribute another 15% to 18%, primarily across general resin and rubber applications. The 99.5% high-purity 4-Octylphenol grade and surfactant-grade 4-Octylphenol are the fastest growing categories within the India 4-Octylphenol market, expanding at 8% to 11% annually, driven by superior 4-Octylphenol performance positioning in advanced resins and surfactants, lower impurity profiles, and growing adoption in premium industrial segments. Specialty and tailored grades together account for 4% to 6% of the market, with the high-purity segment expected to grow rapidly through 2032 across western markets. Leading producers including Prasol Chemicals, SI Group, DIC Corporation, Sasol, and ICC Industries have aligned portfolios to this grade mix, driving high-purity 4-Octylphenol adoption across the India 4-Octylphenol market.

Regional Insights: India 4-Octylphenol Market

Regional analysis of the India 4-Octylphenol market shows that West India and South India collectively account for approximately 56% to 60% of total 4-Octylphenol volume, driven by Maharashtra (Mumbai and Navi Mumbai chemical belt), Gujarat (Dahej and Ankleshwar clusters), Tamil Nadu, Telangana, and Karnataka, supported by established petrochemical infrastructure and strong industrial consumption levels. North India contributes around 24% to 27% of demand, led by Gujarat-linked supply routes, Uttar Pradesh, Punjab, and Haryana, supported by resin, rubber, and agrochemical 4-Octylphenol adoption in industrial clusters. Central and East India together account for 14% to 17% of demand, supported by Madhya Pradesh, West Bengal, Odisha, and Jharkhand, where industrial chemical adoption is accelerating. In 2025, capacity additions and supply operations by Prasol Chemicals across Maharashtra, SI Group across western India, and integrated producers across Gujarat reinforced regional supply hubs, supporting closer execution of resin and surfactant projects across the India 4-Octylphenol market.

Recent Developments: India 4-Octylphenol Market

- The India 4-Octylphenol market witnessed strong momentum in capacity and demand progress during 2024 and 2025. India recorded steady growth in 4-Octylphenol intermediate demand through calendar year 2025, supported by rising phenolic resin and surfactant offtake. Domestic producers reported higher 99% and 99.5% 4-Octylphenol grade utilization by mid-2025, with the 4-Octylphenol resin segment accounting for the largest share of new 4-Octylphenol demand. Cumulative domestic 4-Octylphenol consumption in India is projected to reach 44 to 47 thousand tonnes by FY27 from 38 thousand tonnes in FY25, growing at an average 6% annually.

- Domestic chemical majors have deepened India-focused capacity expansion. In 2025, Prasol Chemicals scaled acetone-based and alkylphenol-linked capacity across its Khopoli and Mahad units, SI Group expanded 4-Octylphenol intermediates for resin customers, integrated producers commissioned new high-purity 4-Octylphenol lines in western India, and downstream surfactant makers expanded ethoxylation facilities. Several producers advanced backward integration into phenol and diisobutylene feedstock. These developments are strengthening domestic supply and supporting the India 4-Octylphenol market forecast 2032.

- Resin and surfactant demand momentum has gained strong traction in the India 4-Octylphenol market. In 2025, leading downstream players across paints, coatings, adhesives, tyres, and agrochemicals expanded phenolic resin and surfactant capacity drawing on 4-Octylphenol. Strategic supply partnerships between domestic 4-Octylphenol producers and resin makers are positioning India as one of the most actively scaling alkylphenol markets in Asia, strengthening long-term competitive positioning in the India 4-Octylphenol market forecast 2032.

Key Market Players: India 4-Octylphenol Market

- Prasol Chemicals Limited

- SI Group India Private Limited

- DIC India Limited

- Sasol Chemicals (India)

- ICC Industries Inc.

- Leap Chem Co. Limited

- PCC Group

- Skyrun Industrial Co. Limited

- Hexion India Private Limited

- Matangi Industries LLP

- Venus Ethoxyethers Pvt. Ltd.

- Aarti Industries Limited

- Atul Limited

Report Scope

In this report, the India 4-Octylphenol Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

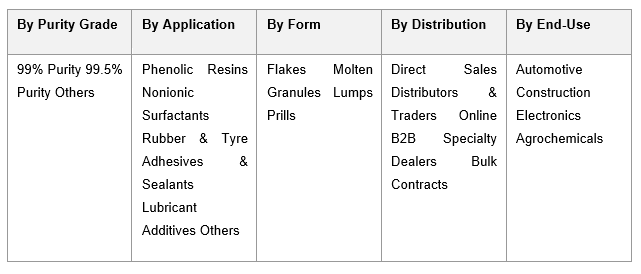

- By Purity Grade

- 99% Purity Grade

- 5% Purity Grade

- Technical Grade

- Surfactant Grade

- Specialty Grade

- Others

- By Application

- Phenolic Resins

- Nonionic Surfactants

- Rubber & Tyre Additives

- Adhesives & Sealants

- Lubricant Additives

- Agrochemical Intermediates

- Others

- By Form

- Flakes

- Molten / Liquid

- Granules

- Lumps

- Prills

- By Distribution Channel

- Direct Sales

- Distributors & Traders

- Online B2B Platforms

- Specialty Chemical Dealers

- Bulk Supply Contracts

- Others

- By End-Use

- Automotive

- Construction

- Electronics

- Agrochemicals

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India 4-Octylphenol Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic 4-Octylphenol producers, specialty alkylphenol and surfactant-grade manufacturers, regional intermediate suppliers, or niche specialty chemical players.

The India 4-Octylphenol Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Purity Grade

- By Application

- By Form

- By Distribution Channel

- By End-Use

- By Region

- Analyst Recommendations

- Geopolitical Impact on India 4-Octylphenol Market

- India 4-Octylphenol Market Insights

- Market Dynamics

- Growth Drivers

- Rising industrialization, phenolic resin expansion, and surfactant demand driving 4-Octylphenol consumption across India.

- Expanding automotive output, rising construction activity, and shifting resin preferences fuelling high-purity 4-Octylphenol adoption.

- Process innovation in high-purity, low-impurity, and specialty 4-Octylphenol grades strengthening industrial segment growth.

- Restraints

- Endocrine-disruptor scrutiny and tightening environmental regulation limiting unrestricted 4-Octylphenol use across applications.

- Raw material dependence on phenol and diisobutylene restricting 4-Octylphenol supply security across domestic producers.

- Volatility in phenol prices and energy costs impacting overall 4-Octylphenol margins.

- Opportunities

- High-purity, surfactant-grade, and specialty 4-Octylphenol innovation opening untapped industrial pools across western clusters.

- High-performance resin, ethoxylate, and stabilizer applications supporting next-generation growth in advanced material segments.

- Import substitution, Make in India incentives, and domestic capacity expansion creating massive supply opportunities.

- Challenges

- Intense competition from imported 4-Octylphenol and low-cost alkylphenol intermediates from regional suppliers.

- Limited feedstock availability and inconsistent phenol supply across smaller domestic producers.

- Maintaining purity consistency, impurity control, and quality at scale across diverse Indian industrial markets.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (phenol, diisobutylene, catalysts, solvents, packaging materials)

- Alkylphenol Producers & 4-Octylphenol Manufacturers (Prasol Chemicals, SI Group, DIC, Sasol)

- Feedstock & Catalyst Suppliers (phenol, diisobutylene, acid catalysts)

- Downstream Resin & Surfactant Makers (phenolic resins, ethoxylates, stabilizers)

- Quality Control, R&D & Testing Laboratories (BIS, ISO, REACH compliance standards)

- Distributors, Wholesalers & Specialty Traders (B2B industrial distribution networks)

- Resin, Rubber & Agrochemical Processors (paints, coatings, tyres, crop protection)

- End-Product Owners & Industrial Formulators (resin, surfactant, lubricant brands)

- Industrial Channels & B2B Supply (direct contracts, distributor networks, online B2B)

- End-Use Industries (automotive, construction, electronics, agrochemicals, paints)

- India 4-Octylphenol Market: Regulatory Framework

- India 4-Octylphenol Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Thousand Tonnes)

- Market Share & Forecast

- By Purity Grade

- 99% Purity Grade

- 5% Purity Grade

- Technical Grade

- Surfactant Grade

- Specialty Grade

- Others

- By Application

- Phenolic Resins

- Nonionic Surfactants

- Rubber & Tyre Additives

- Adhesives & Sealants

- Lubricant Additives

- Agrochemical Intermediates

- Others

- By Form

- Flakes

- Molten / Liquid

- Granules

- Lumps

- Prills

- By Distribution Channel

- Direct Sales

- Distributors & Traders

- Online B2B Platforms

- Specialty Chemical Dealers

- Bulk Supply Contracts

- Others

- By End-Use

- Automotive

- Construction

- Electronics

- Agrochemicals

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India 4-Octylphenol Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Prasol Chemicals Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

(Same Data Pointers Will Be Provided for The Below Companies)

- SI Group India Private Limited

- DIC India Limited

- Sasol Chemicals (India)

- ICC Industries Inc.

- Leap Chem Co. Limited

- PCC Group

- Skyrun Industrial Co. Limited

- Hexion India Private Limited

- Matangi Industries LLP

- Venus Ethoxyethers Pvt. Ltd.

- Aarti Industries Limited

- Atul Limited

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India 4-Octylphenol market and what is its growth forecast?

Ans: The India 4-Octylphenol market is valued at USD 62 million in 2025 and is projected to reach USD 95 million by 2032, growing at a CAGR of 6.3%, supported by rising phenolic resin demand, surfactant consumption, and high-purity grade adoption.

2. Which segments are driving demand in the India 4-Octylphenol market?

Ans: The 99% purity grade leads the market with over 68% volume share, while 99.5% high-purity grades and nonionic surfactants are the fastest-growing segments, driven by phenolic resin, rubber additive, and agrochemical demand across industrial clusters.

3. What are the key drivers of growth in the India 4-Octylphenol market?

Ans: Key drivers include rising industrialization, expanding phenolic resin demand, growing surfactant consumption, rising automotive and construction output, process innovation in high-purity grades, and rapid scaling of domestic alkylphenol capacity across India.

4. Which regions are driving growth in the India 4-Octylphenol market?

Ans: West India and South India lead with around 56% to 60% of total volume, driven by Maharashtra, Gujarat, Tamil Nadu, Telangana, and Karnataka. North India also shows strong industrial 4-Octylphenol demand.

5. What are the latest trends in the India 4-Octylphenol market?

Ans: The latest trends include rapid adoption of high-purity 4-Octylphenol, growth in nonionic surfactants, rising demand for surfactant-grade variants, specialty grade innovation, and expanding domestic capacity driving import substitution across the market.

Frequently Asked Questions

1. How large is the India 4-Octylphenol market and what is its growth forecast?

Ans: The India 4-Octylphenol market is valued at USD 62 million in 2025 and is projected to reach USD 95 million by 2032, growing at a CAGR of 6.3%, supported by rising phenolic resin demand, surfactant consumption, and high-purity grade adoption.

2. Which segments are driving demand in the India 4-Octylphenol market?

Ans: The 99% purity grade leads the market with over 68% volume share, while 99.5% high-purity grades and nonionic surfactants are the fastest-growing segments, driven by phenolic resin, rubber additive, and agrochemical demand across industrial clusters.

3. What are the key drivers of growth in the India 4-Octylphenol market?

Ans: Key drivers include rising industrialization, expanding phenolic resin demand, growing surfactant consumption, rising automotive and construction output, process innovation in high-purity grades, and rapid scaling of domestic alkylphenol capacity across India.

4. Which regions are driving growth in the India 4-Octylphenol market?

Ans: West India and South India lead with around 56% to 60% of total volume, driven by Maharashtra, Gujarat, Tamil Nadu, Telangana, and Karnataka. North India also shows strong industrial 4-Octylphenol demand.

5. What are the latest trends in the India 4-Octylphenol market?

Ans: The latest trends include rapid adoption of high-purity 4-Octylphenol, growth in nonionic surfactants, rising demand for surfactant-grade variants, specialty grade innovation, and expanding domestic capacity driving import substitution across the market.