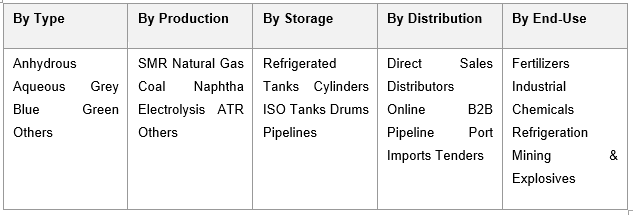

India Ammonia Market, By Type (Anhydrous Ammonia, Aqueous Ammonia, Grey Ammonia, Blue Ammonia, Green Ammonia, Others); By Production Technology (Steam Methane Reforming, Natural Gas Reforming, Coal Gasification, Naphtha Reforming, Electrolysis, Autothermal Reforming, Others); By Storage Form (Refrigerated Bulk Tanks, Pressurized Cylinders, ISO Tank Containers, Drums, Pipelines); By Distribution Channel (Direct Sales, Distributors & Traders, Online B2B Platforms, Pipeline Supply, Port-Based Imports, Industrial Tenders); By End-Use (Fertilizers, Industrial Chemicals, Refrigeration & Energy, Mining & Explosives); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Chemicals & Advanced Materials

- Jun 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Ammonia Market: Fertilizer Demand, Industrial Growth and Green Ammonia Innovation Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

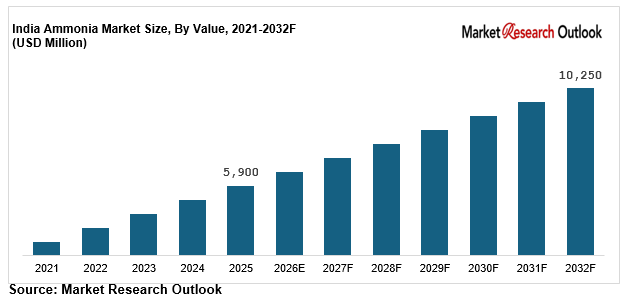

| Market Size (2025) | USD 5,900 Million |

| CAGR (2026-2032) | 8.2% |

| Leading Segment | Anhydrous Ammonia (Fertilizer Application) |

| Fastest Growing Segment | Green & Blue Ammonia |

| Market Size (2032) | USD 10,250 Million |

Source: Market Research Outlook

Market Overview: India Ammonia Market

The India ammonia market size is witnessing rapid expansion, driven by rising fertilizer and urea demand, growing industrial and refrigeration applications, expanding chemical-sector consumption, accelerating green and blue investment, and major capacity additions by domestic fertilizer majors. Valued at USD 5,900 million in 2025 and projected to reach USD 10,250 million by 2032, growing at a CAGR of 8.2%, this growth is being fuelled by strong demand from the agriculture sector, rising industrial chemical use, and the rapid scaling of low-carbon ammonia projects across major producing states. Anhydrous ammonia leads consumption, while green and blue ammonia is emerging as the fastest growing category. Shifting priorities toward energy security, lower emissions, and import substitution are reshaping the supply structure. As domestic majors including IFFCO, Rashtriya Chemicals and Fertilizers, National Fertilizers, GNFC, and Chambal Fertilisers expand integrated gas-to-fertilizer capacity, and energy players including Reliance Industries, Tata Chemicals, and Coromandel International scale low-carbon ammonia pipelines, the sector is evolving into a fertilizer-led, energy-linked, and increasingly low-carbon industry with strong long-term growth potential.

Key Report Takeaways: India Ammonia Market

- The India ammonia market size is projected to grow from USD 5,900 million in 2025 to USD 10,250 million by 2032, registering a strong CAGR of 8.2%, driven by rising fertilizer demand, expanding industrial and refrigeration applications, and the structural shift toward low-carbon blue and green ammonia across India.

- Anhydrous ammonia dominates the India ammonia market, accounting for over 84% of total volume in 2025, driven by its central role in urea and fertilizer production, the deep presence of producers such as IFFCO, RCF, and National Fertilizers, and rising industrial demand across chemical, refrigeration, and mining applications.

- Green and blue ammonia are emerging as the fastest growing segments in the India ammonia market, expected to grow at 30% to 40% annually as decarbonisation targets, energy-transition policy, and export opportunities reshape production strategies across major coastal and industrial hubs.

- Rapid expansion of fertilizer and chemical capacity, with domestic ammonia output crossing 15 million tonnes in 2025 and projected to scale further by 2030, is structurally expanding the India ammonia market across fertilizer, industrial, refrigeration, and energy categories.

- Rising investments by domestic majors such as IFFCO, RCF, National Fertilizers, GNFC, and Chambal Fertilisers in capacity revamps, feedstock efficiency, and green ammonia projects are strengthening local supply and supporting the India ammonia market forecast 2032.

Key Market Drivers: India Ammonia Market

Rising Fertilizer Demand, Food Security Needs, and Government Subsidy Support Driving Ammonia Consumption Across India

Growth in the India ammonia market is being driven by rising fertilizer demand, food-security priorities, and sustained government subsidy support across nitrogen-based fertilizers. India’s foodgrain production crossed 330 million tonnes in 2025, while urea consumption exceeded 35 million tonnes, keeping supply central to domestic agriculture. Around 80% of India’s ammonia output is consumed in fertilizer production, led by IFFCO, RCF, National Fertilizers, GNFC, GSFC, and Chambal Fertilisers. The nutrient-based subsidy and urea subsidy programmes, combined with the target of fertilizer self-sufficiency, continue to support steady demand. Per-hectare nitrogen application in India remains uneven across states, indicating significant long-term headroom for balanced fertilizer growth. Rising rural incomes, expanding irrigation, and continued government procurement support are creating strong structural pull-through demand across the market.

Expanding Industrial, Refrigeration, and Chemical Applications and Import Substitution Fuelling Ammonia Demand

The India ammonia market is benefiting from expanding industrial, refrigeration, and chemical applications, alongside a growing import-substitution agenda. Demand from industrial uses including explosives, mining, pharmaceuticals, textiles, refrigeration, and water treatment is rising at 6% to 9% annually. India currently imports around 2 to 3 million tonnes each year, creating strong incentives for domestic capacity addition and brownfield revamps. Average delivered prices in India have ranged between USD 350 and USD 700 per tonne across 2022 to 2025, tracking global gas and feedstock cycles. Domestic capacity has scaled steadily, with output crossing 15 million tonnes by 2025, led by IFFCO, RCF, National Fertilizers, GNFC, and Chambal Fertilisers. Tightening environmental norms, BIS quality standards, and rising trust in domestic supply have further strengthened the organized domestic market, supporting competitiveness across the India ammonia market.

Investment in Green and Blue Ammonia, National Green Hydrogen Mission, and Energy-Transition Demand Strengthening Low-Carbon Growth

Rapid investment in green and blue ammonia is a major catalyst for the India ammonia market, with the low-carbon segment projected to grow at 30% to 40% annually through 2032. India’s National Green Hydrogen Mission, backed by an outlay of around INR 19,744 crore, targets 5 million tonnes of green hydrogen capacity by 2030, much of which is expected to be converted into green fuel for fertilizer and export use. More than 20 green ammonia projects have been announced across coastal and industrial states, with Reliance Industries, Indian fertilizer majors, and global offtake partners scaling renewable-powered electrolysis and carbon-capture pipelines. Green ammonia for export and marine fuel represents an estimated multi-billion-dollar addressable opportunity for Indian producers. Government incentives, renewable-energy expansion, and corporate decarbonisation targets are structurally expanding market growth across all major end-use categories through 2032.

Key Market Challenges: India Ammonia Market

High Natural Gas Dependence and Feedstock Import Reliance Exposing Ammonia Producers to Price Volatility

The India ammonia market continues to face challenges around high natural gas dependence and feedstock import reliance, with natural gas accounting for over 70% of domestic ammonia production and India importing more than 50% of its natural gas. While long-term gas contracts and domestic gas allocation have improved stability, producer margins remain sensitive to global gas prices, which swung sharply between 2021 and 2024. Producers continue to face cost pressure from imported feedstock, currency movement, and freight, while fertilizer-grade ammonia pricing is partly shaped by subsidy mechanisms. India’s continued dependence on imported gas and ammonia limits margin predictability for producers across the India ammonia market.

Energy-Intensive Production, Carbon Emissions, and Tightening Environmental Norms Raising Compliance Costs

The market faces structural complexity from energy-intensive production, carbon emissions, and tightening environmental norms. Conventional grey ammonia production through steam methane reforming is highly energy-intensive and a significant source of industrial carbon emissions, with the sector accounting for a meaningful share of chemical-industry energy use. While leading producers such as IFFCO, RCF, GNFC, and Chambal Fertilisers have invested in energy-efficient revamps and lower specific energy consumption, older plants maintain higher emission and energy footprints. Compliance with emission norms, carbon-reduction targets, and emerging carbon-pricing mechanisms adds cost and capital complexity across plants operating pan-India. While government decarbonisation schemes support cleaner production, the transition cost remains a near-term challenge for the India ammonia market.

Handling, Storage, and Transport Safety Risks and Infrastructure Gaps Constraining Ammonia Distribution

The India ammonia market faces practical constraints around handling, storage, and transport safety, infrastructure gaps, and distribution complexity across the value chain. It is a hazardous, toxic, and corrosive chemical requiring specialised refrigerated or pressurised storage, trained handling, and strict safety compliance, raising logistics and insurance costs. Dedicated storage terminals, cryogenic tanks, and pipeline coverage remain limited, with most movement dependent on tankers and port-based imports concentrated at a few coastal hubs. Average inland transport adds 8% to 14% to delivered costs, while safety incidents and stringent norms increase compliance burden. Investments in ammonia-ready ports, storage terminals, and pipelines are emerging as solutions, but infrastructure gaps and safety requirements remain barriers across the market.

Key Market Trends: India Ammonia Market

Rapid Scaling of Green and Blue Ammonia Projects in India

The India ammonia market is undergoing a clear technology shift toward green and blue ammonia, with these variants expected to capture a growing share of new capacity announcements by 2030. Green ammonia produced through renewable-powered electrolysis and blue ammonia produced with carbon capture deliver substantially lower emissions than conventional grey ammonia. Leading domestic and global players including Reliance Industries, IFFCO, GNFC, Chambal Fertilisers, and global offtake partners have scaled green and blue projects through 2024 and 2025. Ammonia is also gaining traction as a hydrogen carrier and marine fuel, particularly around coastal hubs such as Kandla, Paradeep, and Tuticorin where export-oriented projects are rising, with producers positioning low-carbon ammonia for fertilizer, energy, and export buyers. This production transition is reinforcing the India ammonia market forecast 2032 across both domestic and export categories.

Capacity Expansion, Brownfield Revamps, and Feedstock Diversification by Domestic Fertilizer Majors

A clear shift toward capacity expansion, brownfield revamps, and feedstock diversification is reshaping the market, particularly across the fertilizer-producing belt. New and revived urea-ammonia complexes such as Ramagundam, Gorakhpur, Sindri, Barauni, and Talcher have added significant domestic capacity between 2021 and 2025. Producers are diversifying feedstock toward natural gas, coal gasification, and renewable electrolysis to reduce import reliance and emissions. Leading producers including IFFCO, RCF, National Fertilizers, GNFC, and Chambal Fertilisers operate across more than 30 ammonia-urea plants nationwide, ranking among the most strategically important industrial chemicals. Government support through fertilizer-sector revival schemes is also accelerating domestic output across both fertilizer and industrial segments of the market. By 2025, domestic production met over 85% of fertilizer-grade ammonia demand, with producers increasingly prioritising self-sufficiency over imports.

Emergence of Ammonia as an Energy Carrier, Marine Fuel, and Export Commodity

A wave of energy-transition investment is reshaping the market supply structure, positioning the product as an energy carrier, marine fuel, and export commodity. Combined India-focused investment announcements in green and blue ammonia, electrolyser capacity, and supporting infrastructure exceeded USD 5 billion across 2023 to 2025. Reliance Industries advanced large-scale green hydrogen and green ammonia plans, IFFCO and GNFC progressed green ammonia pilots, Chambal Fertilisers and National Fertilizers pursued energy-efficiency revamps, and several developers signed export memoranda with buyers in Japan, Korea, and Europe. The National Green Hydrogen Mission, with an outlay of around INR 19,744 crore, reduced renewable-energy costs, and a target of capturing a meaningful share of global low-carbon ammonia trade have structurally favoured domestic supply. Combined with rising fertilizer demand and growing industrial procurement, these developments are reinforcing the India ammonia market forecast 2032 across the entire value chain.

Segmental Insights: India Ammonia Market

By End-Use: Fertilizers Segment Dominates the India Ammonia Market

The fertilizers end-use segment dominates the India ammonia market, accounting for an estimated 80% to 82% of total volume, driven by sustained urea and complex-fertilizer demand, food-security priorities, and government subsidy support. Anhydrous ammonia routed into urea and nitrogen fertilizers is the dominant use within this segment, with captive fertilizer plants consuming over 80% of domestic output. The industrial chemicals segment contributes another 9% to 12% of demand, driven by explosives, nitric acid, caprolactam, and specialty chemical production. The refrigeration and energy segment accounts for 5% to 7%, led by cold-storage, food processing, and emerging clean-energy use, while mining and explosives add the balance. In 2025, leading producers including IFFCO, RCF, National Fertilizers, GNFC, and Chambal Fertilisers scaled fertilizer and industrial ammonia deployment under capacity revamps and self-sufficiency programmes, reinforcing segment dominance in the India ammonia market.

By Type: Anhydrous Ammonia Leads While Green and Blue Ammonia Grow Fastest

Anhydrous ammonia leads the India ammonia market by type, accounting for approximately 84% of total volume, driven by its central role in fertilizer and industrial chemical production, deep distribution presence, and improving cost efficiency. Aqueous ammonia contributes another 8% to 10%, primarily across refrigeration, water treatment, and specialty applications. Green and blue ammonia are the fastest growing categories within the market, expanding at 30% to 40% annually, driven by lower-carbon positioning, energy-transition demand, and growing export and marine-fuel use. Grey conventional ammonia still accounts for the largest share of current output, with green and blue grades expected to scale rapidly through 2032. Leading domestic producers including IFFCO, RCF, National Fertilizers, GNFC, and Chambal Fertilisers have aligned production portfolios to this mix, driving low-carbon adoption across the market.

Regional Insights: India Ammonia Market

Regional analysis of the market shows that West India and North India collectively account for approximately 55% to 60% of total ammonia volume, driven by Gujarat (IFFCO Kalol, GSFC, GNFC), Maharashtra (RCF Thal and Trombay), Rajasthan (Chambal Fertilisers Gadepan), Uttar Pradesh (IFFCO Aonla and Phulpur), and Punjab (National Fertilizers), supported by major fertilizer complexes and strong agricultural demand. South India contributes around 24% to 27% of demand, led by Tamil Nadu (Madras Fertilizers, SPIC), Kerala (FACT), Karnataka (Mangalore Chemicals), and Telangana and Andhra Pradesh (Ramagundam, Coromandel International), supported by fertilizer and industrial ammonia use. Central and East India together account for 14% to 17% of demand, supported by Madhya Pradesh, Odisha (IFFCO Paradeep), West Bengal, and Assam, where capacity revival is accelerating. In 2025, capacity additions and operations by IFFCO across Gujarat and Odisha, RCF across Maharashtra, Chambal Fertilisers across Rajasthan, and National Fertilizers across North India reinforced regional supply hubs, supporting closer execution of fertilizer and industrial projects across the India ammonia market.

Recent Developments: India Ammonia Market

- The market witnessed strong momentum in capacity and project progress during 2024 and 2025. Domestic ammonia output crossed 15 million tonnes in calendar year 2025, reflecting steady growth from revived urea complexes, according to industry tracking. India announced more than 20 green ammonia projects by mid-2025, with the fertilizer segment accounting for the largest share of planned offtake. Cumulative domestic ammonia demand in India is projected to reach 20 to 22 million tonnes by FY27 from around 17.5 million tonnes in FY25, growing at an average mid-single-digit rate annually.

- Domestic fertilizer majors have deepened capacity expansion. In 2025, IFFCO scaled output across its Kalol, Aonla, Phulpur, and Paradeep complexes, RCF advanced revamps at Thal and Trombay, National Fertilizers progressed energy-efficiency upgrades, GNFC expanded ammonia and downstream capacity, and Chambal Fertilisers ramped its Gadepan III urea-ammonia line. Reliance Industries advanced large-scale green hydrogen and green ammonia plans. These developments are strengthening domestic supply and supporting the India ammonia market forecast 2032.

- Green and blue ammonia momentum has gained strong traction in the India ammonia market. In 2025, leading players including Reliance Industries, IFFCO, GNFC, Chambal Fertilisers, and global offtake partners advanced green and blue ammonia and export projects. Strategic partnerships between domestic producers, energy companies, and international buyers are positioning India as one of the most actively scaling low-carbon markets globally, strengthening long-term competitive positioning in the market forecast 2032.

Key Market Players: India Ammonia Market

- Indian Farmers Fertiliser Cooperative Limited (IFFCO)

- Rashtriya Chemicals and Fertilizers Limited (RCF)

- Gujarat State Fertilizers & Chemicals Limited (GSFC)

- Gujarat Narmada Valley Fertilizers & Chemicals Limited (GNFC)

- National Fertilizers Limited (NFL)

- The Fertilisers and Chemicals Travancore Limited (FACT)

- Chambal Fertilisers and Chemicals Limited

- Tata Chemicals Limited

- Coromandel International Limited

- Deepak Fertilisers and Petrochemicals Corporation Limited

- Madras Fertilizers Limited

- Mangalore Chemicals & Fertilizers Limited

- Reliance Industries Limited

Report Scope

In this report, the India Ammonia Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Type

- Anhydrous Ammonia

- Aqueous Ammonia

- Grey Ammonia

- Blue Ammonia

- Green Ammonia

- Others

- By Production Technology

- Steam Methane Reforming (SMR)

- Natural Gas Reforming

- Coal Gasification

- Naphtha Reforming

- Electrolysis (Green Hydrogen)

- Autothermal Reforming (ATR)

- Others

- By Storage Form

- Refrigerated Bulk Tanks

- Pressurized Cylinders

- ISO Tank Containers

- Drums

- Pipelines

- By Distribution Channel

- Direct Sales

- Distributors & Traders

- Online B2B Platforms

- Pipeline Supply

- Port-Based Imports

- Industrial Tenders & Contracts

- By End-Use

- Fertilizers

- Industrial Chemicals

- Refrigeration & Energy

- Mining & Explosives

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Ammonia Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic producers, specialty green and blue ammonia developers, regional fertilizer players, or niche industrial ammonia suppliers.

The India Ammonia Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Type

- By Production Technology

- By Storage Form

- By Distribution Channel

- By End-Use

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Ammonia Market

- India Ammonia Market Insights

- Market Dynamics

- Growth Drivers

- Rising fertilizer demand, food security needs, and government subsidy support driving ammonia consumption across India.

- Expanding industrial, refrigeration, and chemical applications and import substitution fuelling ammonia demand across India.

- Investment in green and blue ammonia, the National Green Hydrogen Mission, and energy-transition demand strengthening low-carbon ammonia growth.

- Restraints

- High natural gas dependence and feedstock import reliance exposing ammonia producers to price volatility.

- Energy-intensive production, carbon emissions, and tightening environmental norms raising compliance and decarbonisation costs.

- Handling, storage, and transport safety risks and infrastructure gaps constraining ammonia distribution across regions.

- Opportunities

- Green and blue ammonia innovation opening export, energy, and marine-fuel demand across coastal hubs.

- Ammonia as a hydrogen carrier and clean-energy vector supporting next-generation energy and decarbonisation demand.

- Capacity revamps, the National Green Hydrogen Mission, and port infrastructure creating large distribution opportunities.

- Challenges

- Intense competition from low-cost ammonia imports and global producers in coastal and import-dependent regions.

- Limited dedicated storage, pipeline, and handling infrastructure across smaller industrial regions.

- Maintaining consistent feedstock supply, plant utilisation, and safety compliance across diverse Indian plants.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (natural gas, coal, naphtha, hydrogen, renewable power, catalysts)

- Ammonia Producers & Fertilizer Manufacturers (IFFCO, RCF, National Fertilizers, GNFC, Chambal Fertilisers)

- Feedstock & Catalyst Suppliers (natural gas, coal, hydrogen, reforming and synthesis catalysts)

- Green & Blue Ammonia Developers (renewable electrolysis, carbon capture, low-carbon ammonia)

- Quality Control, R&D & Testing Laboratories (BIS, ISO, safety and emission standards)

- Distributors, Traders & Bulk Logistics (B2B distribution and tanker networks)

- Industrial & Chemical Buyers (fertilizer plants, explosives, refrigeration, pharmaceuticals)

- Producers & Energy Players (IFFCO, RCF, GNFC, Reliance Industries, Tata Chemicals)

- Ports, Pipelines & Export Channels (Kandla, Paradeep, Tuticorin, tanker and pipeline supply)

- End-Users (farmers, fertilizer plants, chemical and refrigeration industries, energy and export buyers)

- India Ammonia Market: Regulatory Framework

- India Ammonia Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Million Tonnes)

- Market Share & Forecast

- By Type

- Anhydrous Ammonia

- Aqueous Ammonia

- Grey Ammonia

- Blue Ammonia

- Green Ammonia

- Others

- By Production Technology

- Steam Methane Reforming (SMR)

- Natural Gas Reforming

- Coal Gasification

- Naphtha Reforming

- Electrolysis (Green Hydrogen)

- Autothermal Reforming (ATR)

- Others

- By Storage Form

- Refrigerated Bulk Tanks

- Pressurized Cylinders

- ISO Tank Containers

- Drums

- Pipelines

- By Distribution Channel

- Direct Sales

- Distributors & Traders

- Online B2B Platforms

- Pipeline Supply

- Port-Based Imports

- Industrial Tenders & Contracts

- By End-Use

- Fertilizers

- Industrial Chemicals

- Refrigeration & Energy

- Mining & Explosives

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Ammonia Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Indian Farmers Fertiliser Cooperative Limited (IFFCO)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

(Same Data Pointers Will Be Provided for The Below Companies)

- Rashtriya Chemicals and Fertilizers Limited (RCF)

- Gujarat State Fertilizers & Chemicals Limited (GSFC)

- Gujarat Narmada Valley Fertilizers & Chemicals Limited (GNFC)

- National Fertilizers Limited (NFL)

- The Fertilisers and Chemicals Travancore Limited (FACT)

- Chambal Fertilisers and Chemicals Limited

- Tata Chemicals Limited

- Coromandel International Limited

- Deepak Fertilisers and Petrochemicals Corporation Limited

- Madras Fertilizers Limited

- Mangalore Chemicals & Fertilizers Limited

- Reliance Industries Limited

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India ammonia market and what is its growth forecast?

Ans: The India ammonia market is valued at USD 5,900 million in 2025 and is projected to reach USD 10,250 million by 2032, growing at a CAGR of 8.2%, supported by rising fertilizer demand, industrial growth, and green ammonia investment.

2. Which segments are driving demand in the India ammonia market?

Ans: Anhydrous ammonia leads with over 84% volume share, while green and blue ammonia are the fastest-growing segments, driven by decarbonisation targets, energy-transition policy, and rising export and marine-fuel demand across India.

3. What are the key drivers of growth in the India ammonia market?

Ans: Key drivers include rising fertilizer and urea demand, government subsidy support, expanding industrial and refrigeration applications, import substitution, and growing investment in green and blue ammonia under the National Green Hydrogen Mission.

4. Which regions are driving growth in the India ammonia market?

Ans: West India and North India lead with around 55% to 60% of total volume, driven by Gujarat, Maharashtra, Rajasthan, Uttar Pradesh, and Punjab. South India also shows strong fertilizer and industrial ammonia demand.

5. What are the latest trends in the India ammonia market?

Ans: The latest trends include rapid scaling of green and blue ammonia, capacity revamps by fertilizer majors, feedstock diversification, and the emergence of ammonia as a hydrogen carrier, marine fuel, and export commodity.

Frequently Asked Questions

1. How large is the India ammonia market and what is its growth forecast?

Ans: The India ammonia market is valued at USD 5,900 million in 2025 and is projected to reach USD 10,250 million by 2032, growing at a CAGR of 8.2%, supported by rising fertilizer demand, industrial growth, and green ammonia investment.

2. Which segments are driving demand in the India ammonia market?

Ans: Anhydrous ammonia leads with over 84% volume share, while green and blue ammonia are the fastest-growing segments, driven by decarbonisation targets, energy-transition policy, and rising export and marine-fuel demand across India.

3. What are the key drivers of growth in the India ammonia market?

Ans: Key drivers include rising fertilizer and urea demand, government subsidy support, expanding industrial and refrigeration applications, import substitution, and growing investment in green and blue ammonia under the National Green Hydrogen Mission.

4. Which regions are driving growth in the India ammonia market?

Ans: West India and North India lead with around 55% to 60% of total volume, driven by Gujarat, Maharashtra, Rajasthan, Uttar Pradesh, and Punjab. South India also shows strong fertilizer and industrial ammonia demand.

5. What are the latest trends in the India ammonia market?

Ans: The latest trends include rapid scaling of green and blue ammonia, capacity revamps by fertilizer majors, feedstock diversification, and the emergence of ammonia as a hydrogen carrier, marine fuel, and export commodity.