India Clinical Nutrition for Diabetes Care Market, By Product Type (Oral Nutritional Supplements, Ready-to-Drink Formulas, Diabetic Meal Replacements, Enteral & Tube-Feeding Formulas, Functional Diabetic Foods & Bars, Others); By Flavor (Chocolate, Vanilla, Strawberry, Coffee, Cardamom & Kesar, Unflavored, Others); By Packaging (Tins & Cans, Sachets & Pouches, Tetra Packs & Bottles, Single-Serve Packs, Bulk & Institutional Packs); By Distribution Channel (Hospital Pharmacies, Retail Pharmacies & Chemists, Online Pharmacies & E-Commerce, Supermarkets & Hypermarkets, Specialty Nutrition Stores, Direct & Institutional Sales); By End-User (Hospitals & Clinics, Homecare & Households, Specialty Diabetes Centers, Long-Term & Geriatric Care); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Food, Beverage & Nutrition

- Jun 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Clinical Nutrition for Diabetes Care Market: Rising Diabetes Prevalence, Online Pharmacy Expansion and Low-Glycemic Innovation Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

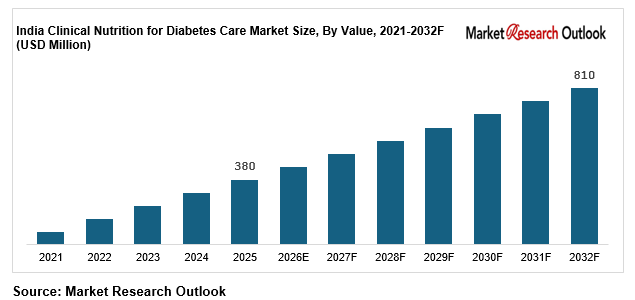

| Market Size (2025) | USD 380 Million |

| CAGR (2026-2032) | 11.5% |

| Leading Segment | Oral Nutritional Supplements (Vanilla Flavor) |

| Fastest Growing Segment | Ready-to-Drink Diabetic Formulas |

| Market Size (2032) | USD 810 Million |

Source: Market Research Outlook

Market Overview: India Clinical Nutrition for Diabetes Care Market

The India clinical nutrition for diabetes care market size is witnessing rapid expansion, driven by rising diabetes prevalence, growing hospital and homecare nutrition adoption, increasing clinical awareness, expanding online pharmacy networks, increasing demand for low-glycemic and high-protein formulas, and major capacity additions by domestic and global nutrition majors. Valued at USD 380 million in 2025 and projected to reach USD 810 million by 2032, growing at a CAGR of 11.5%, the India clinical nutrition for diabetes care market growth is being fuelled by strong demand from diagnosed diabetic patients, rising disposable incomes, and the rapid scaling of online pharmacy and e-commerce platforms across tier-1 and tier-2 cities. Oral nutritional supplement powders lead consumption, while the ready-to-drink diabetic formula segment is emerging as the fastest growing category. Shifting patient preferences toward clinically validated nutrition, growing physician and dietitian recommendations, and rising demand for convenient yet functional formulas are reshaping the supply landscape. As global and domestic majors including Abbott, Dr. Reddy’s, Nestlé Health Science, Danone, and British Biologicals expand integrated formulation-to-shelf capacity, and hospital and online pharmacy chains including Apollo Pharmacy, MedPlus, Tata 1mg, and PharmEasy scale distribution pipelines, the India clinical nutrition for diabetes care market is evolving into a patient-led, innovation-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Clinical Nutrition for Diabetes Care Market

- The India clinical nutrition for diabetes care market size is projected to grow from USD 380 million in 2025 to USD 810 million by 2032, registering a strong CAGR of 11.5%, driven by accelerated hospital and online pharmacy penetration, rising low-glycemic formula adoption, and the structural shift toward clinically formulated diabetic nutrition across urban India.

- Oral nutritional supplement powders dominate the India clinical nutrition for diabetes care market, accounting for over 55% of total value in 2025, driven by strong physician preference for established diabetic formulas, the deep presence of brands such as Glucerna, Celevida, and Resource Diabetic, and rising demand across hospital and retail pharmacy channels.

- Ready-to-drink and meal-replacement diabetic formulas are emerging as the fastest growing segments in the India clinical nutrition for diabetes care market, expected to grow at 14% to 18% annually as working patients, caregivers, and convenience-focused urban consumers reshape sourcing strategies across metro and tier-1 markets.

- Rising diabetes prevalence, with over 101 million diagnosed diabetic patients across India by 2025 and a prediabetic pool exceeding 136 million, is structurally expanding the India clinical nutrition for diabetes care market across hospital, homecare, and online delivery categories.

- Rising investments by global and domestic nutrition majors such as Abbott, Dr. Reddy’s, Nestlé Health Science, Danone, and British Biologicals in manufacturing infrastructure, clinical research, and innovative diabetic nutrition variants are strengthening local supply and supporting the India clinical nutrition for diabetes care market forecast 2032.

Key Market Drivers: India Clinical Nutrition for Diabetes Care Market

Rising Diabetes Prevalence, Growing Clinical Awareness, and Hospital Nutrition Adoption Driving Demand Across India

Growth in the India clinical nutrition for diabetes care market is being driven by rising diabetes prevalence, growing clinical awareness, and aggressive expansion of hospital and homecare nutrition adoption across tier-1, tier-2, and tier-3 cities. India’s diagnosed diabetic population crossed 101 million in 2025, with prevalence rates climbing among adults and projected to rise further by 2030. Hospital and diabetes-care networks have expanded steadily, led by chains such as Apollo, Fortis, Max, Manipal, and AIIMS. Diabetes-specific nutrition has become a core recommendation in these settings, with average diabetic nutrition pack prices ranging between INR 400 and INR 900 per tin. Per-capita spending on clinical nutrition in India remains well below developed markets, indicating significant long-term headroom for growth. Rising health awareness, falling delivery times under 15 minutes via online pharmacies, and growing physician-led recommendations are creating strong structural pull-through demand across the India clinical nutrition for diabetes care market.

Growing Healthcare Infrastructure, Rising Disposable Incomes, and Physician Recommendations Fuelling Premium Diabetic Nutrition Adoption

The India clinical nutrition for diabetes care market is benefiting from sustained growth in disposable incomes, with per-capita income rising by over 70% between 2014 and 2024 according to MOSPI, alongside continued cost reductions in modern nutrition processing, spray-drying, and aseptic packaging. Average retail diabetic nutrition prices in India now range between INR 400 and INR 900 per 400 gram tin, with premium variants commanding INR 900 to INR 1,500 per pack. Domestic clinical nutrition manufacturing capacity has scaled rapidly, with organized diabetic nutrition output exceeding 24 thousand tonnes by 2025, led by Abbott, Dr. Reddy’s, Nestlé Health Science, Danone, and British Biologicals. FSSAI labelling reforms, BIS quality standards, and growing trust in clinically validated nutrition have further strengthened organized supply, supporting price competitiveness across the India clinical nutrition for diabetes care market. Diagnosed patients between 35 and 64 years now account for over 60% of diabetic nutrition consumption, with working professionals and caregivers preferring clinically backed formulas, premium packaging, and on-the-go convenience.

Product Innovation in Low-Glycemic, High-Protein, and Plant-Based Diabetic Formulas Strengthening Packaged Segment Growth

Rapid growth in low-glycemic and plant-based diabetic nutrition is a major catalyst for the India clinical nutrition for diabetes care market, with the plant-based segment projected to grow at 14% to 18% annually through 2032. Rising lifestyle disease awareness across roughly 60% of urban Indian adults is creating strong demand for slow-release carbohydrate, high-fiber, and millet-based diabetic formulas. Health-conscious patient behavior under fitness and wellness trends, science-based nutrition targets, and growing protein intake awareness are driving patients toward fortified diabetic nutrition consumption. The FSSAI’s clean-label labelling guidelines in 2024 have increased transparency for clinical nutrition buyers, accelerating premium diabetic nutrition adoption to hedge against rising health concerns. Leading innovators such as Abbott, Dr. Reddy’s, Nestlé Health Science, Danone, and Hexagon Nutrition have scaled low-glycemic, high-protein, and plant-based diabetic nutrition pipelines, with the plant-based diabetic nutrition segment alone representing an estimated USD 70 million addressable opportunity within Indian wellness markets. Government health programs combined with corporate health-led procurement are structurally expanding India clinical nutrition for diabetes care market growth across all major end-user categories through 2032.

Key Market Challenges: India Clinical Nutrition for Diabetes Care Market

Low Awareness Among Rural and Middle-Income Patients Limiting Frequency of Diabetic Nutrition Use

The India clinical nutrition for diabetes care market continues to face challenges around low awareness and limited usage frequency among rural and middle-income patients, with a typical month of diabetic nutrition costing between INR 1,200 and INR 3,000 before any physician guidance. While clean-label reforms by FSSAI and growing demand for affordable and plant-based variants have improved transparency, organized diabetic nutrition usage frequency outside metro cities remains modest, reflecting bottlenecks in clinical awareness, affordability concerns, and dietary patterns. Doctors and dietitians continue to recommend structured diabetic nutrition for diagnosed and pre-diabetic households, while affordable, regional-language-labelled, and low-cost diabetic nutrition variants remain underdeveloped. India’s continued dependence on generic supplements and home remedies limits adoption among middle-income and rural households across the India clinical nutrition for diabetes care market.

Fragmented Distribution and Limited Insurance Reimbursement Across Tier-2 and Tier-3 Cities

The India clinical nutrition for diabetes care market faces structural complexity from variations in pharmacy coverage, hospital nutrition adoption, and last-mile reach across different cities. While metros such as Delhi, Mumbai, Bengaluru, Chennai, and Hyderabad have well-established hospital and pharmacy frameworks with organized retail penetration above 30%, others remain dominated by fragmented chemist and wholesale networks. Average shelf life for packaged diabetic nutrition ranges between 12 and 24 months, but limited insurance reimbursement and high out-of-pocket cost remain a key bottleneck in tier-2 and tier-3 rollout. Differential availability of pharmacy shelves, distributor networks, and last-mile reach across states creates operational complexity for nutrition players such as Abbott, Dr. Reddy’s, Nestlé Health Science, and Danone operating pan-India. While the Ministry of Health and Family Welfare has launched chronic-disease awareness schemes, distribution fragmentation remains a near-term challenge for the India clinical nutrition for diabetes care market.

Regulatory Complexity Around Medical Nutrition Claims and Raw Material Cost Pressures Impacting Overall Margins

The India clinical nutrition for diabetes care market faces practical constraints around regulatory complexity, raw material price volatility, and margin compression across the value chain. Indian protein and micronutrient input prices have risen by 12% to 18% between 2022 and 2025, while packaging input costs including tins, sachets, and aluminium have moved up by 8% to 14% over the same period. Smaller nutrition brands face additional governance complexity in meeting FSSAI medical nutrition claim requirements without losing volume. Average gross margins for branded diabetic nutrition in India range between 30% and 42%, reducing the effective profitability of new launches by 4% to 10%. Plant-based ingredients, clinical validation studies, and high-protein formulations are emerging as solutions to differentiate, but premium pricing and limited patient awareness remain barriers to widespread adoption across the India clinical nutrition for diabetes care market.

Key Market Trends: India Clinical Nutrition for Diabetes Care Market

Rapid Adoption of Low-Glycemic, Plant-Based, and Millet-Based Diabetic Nutrition in India

The India clinical nutrition for diabetes care market is undergoing a clear shift toward low-glycemic, plant-based, and millet-based diabetic nutrition, with these advanced variants expected to capture over 18% of new diabetic nutrition launches by 2027. Plant-based diabetic formulas deliver protein levels of 9 to 12 grams per serving, compared to 6 to 8 grams for some traditional variants, while high-fiber blends add slow-release carbohydrates for glycemic control. Leading domestic and global brands including Abbott, Dr. Reddy’s, Nestlé Health Science, Danone, and Hexagon Nutrition have scaled low-glycemic and plant-based diabetic nutrition production capacity through 2024 and 2025. Functional formulas with added fiber, vitamins, minerals, and probiotics are also gaining traction, particularly in metro cities such as Mumbai and Bengaluru where wellness patients are rising, with brands like Glucerna, Celevida, and Pentasure DM offering clinically positioned diabetic nutrition variants for health-focused buyers. This product transition is reinforcing the India clinical nutrition for diabetes care market forecast 2032 across both hospital and homecare categories.

Growth of Online Pharmacies, E-Commerce, and Digital Distribution in the India Clinical Nutrition for Diabetes Care Market

A clear shift toward online pharmacies, e-commerce, and digital distribution models is reshaping the India clinical nutrition for diabetes care market, particularly in the urban and metro segment. Under online pharmacy platforms such as Tata 1mg, PharmEasy, Netmeds, and Apollo 24by7, diabetic nutrition is delivered within hours at prices typically in line with or slightly below MRP. Leading e-commerce platforms including Amazon and Flipkart have built combined operational reach exceeding 800 Indian cities, with diabetic nutrition ranking among the top health-supplement categories ordered. Online aggregators and digital platforms such as Tata 1mg, PharmEasy, and Amazon are also reducing customer acquisition costs and accelerating diabetic nutrition adoption across both hospital and homecare segments of the India clinical nutrition for diabetes care market. By 2025, online channels account for over 18% of diabetic nutrition sales in India, up from less than 5% in 2020, with metro buyers increasingly preferring subscription-based delivery convenience over in-store purchase.

Capacity Expansion by Global and Domestic Nutrition Majors and Clinical Research Investments

A wave of domestic capacity expansion and clinical research investments is reshaping the India clinical nutrition for diabetes care market supply landscape. Combined India-focused capital expenditure announcements in nutrition manufacturing, formulation, and packaging exceeded USD 320 million across 2023 to 2025. Abbott expanded diabetic nutrition capacity across its facilities, Dr. Reddy’s scaled Celevida production, Nestlé Health Science expanded Resource Diabetic supply, Danone grew its Nutricia diabetic portfolio, and British Biologicals expanded its clinical nutrition lines. FSSAI clean-label reforms, Production Linked Incentive (PLI) scheme allocations for food processing exceeding INR 10,900 crore, and a stable regulatory structure on medical nutrition have structurally favoured organized supply. Combined with hospital nutrition adoption driving demand and online pharmacy procurement scaling rapidly, these developments are reinforcing the India clinical nutrition for diabetes care market forecast 2032 across the entire value chain.

Segmental Insights: India Clinical Nutrition for Diabetes Care Market

By End-User: Homecare Segment Dominates the India Clinical Nutrition for Diabetes Care Market

The homecare and households end-user segment dominates the India clinical nutrition for diabetes care market, accounting for an estimated 55% to 60% of total value, driven by rising diabetes prevalence, growing at-home chronic-care management, and improving clinical nutrition economics. Powder and ready-to-drink formats are the dominant variants within this segment, with tin and single-serve sachet formats capturing over 70% of homecare diabetic nutrition purchases. The hospitals and clinics segment contributes another 25% to 28% of demand, driven by inpatient nutrition, diabetes wards, and post-operative care adopting diabetic nutrition as a standard protocol. The specialty diabetes centers segment accounts for 10% to 12%, led by endocrinology clinics and chronic-care facilities. In 2025, leading nutrition players including Abbott, Dr. Reddy’s, Nestlé Health Science, Danone, and Hexagon Nutrition scaled up homecare and hospital-focused diabetic nutrition deployment under online pharmacy and hospital expansion, reinforcing segment dominance in the India clinical nutrition for diabetes care market.

By Product Type: Powders Lead While Ready-to-Drink and Plant-Based Grow Fastest

Oral nutritional supplement powders lead the India clinical nutrition for diabetes care market product landscape, accounting for approximately 55% of total value, driven by their clinical validation, deep distribution presence, and improving cost economics. Ready-to-drink and meal-replacement formulas contribute another 20% to 24%, primarily across metro and tier-1 cities. Ready-to-drink and plant-based diabetic formulas are the fastest growing categories within the India clinical nutrition for diabetes care market, expanding at 14% to 18% annually, driven by superior convenience and nutrition positioning of 9 to 12 grams of protein per serving, additional functional benefits, and growing adoption in homecare and premium urban segments. Enteral and functional diabetic foods together account for 12% to 16% of the market, with the plant-based segment expected to grow rapidly through 2032 in metro markets. Leading manufacturers including Abbott, Dr. Reddy’s, Nestlé Health Science, Danone, and British Biologicals have aligned product portfolios to this product mix, driving premium diabetic nutrition adoption across the India clinical nutrition for diabetes care market.

Regional Insights: India Clinical Nutrition for Diabetes Care Market

Regional analysis of the India clinical nutrition for diabetes care market shows that South India and West India collectively account for approximately 55% to 59% of total value, driven by Karnataka (Bengaluru healthcare market), Tamil Nadu (Chennai hospital belt), Telangana, Maharashtra (Mumbai and Pune medical belt), and Gujarat, supported by strong hospital infrastructure and high diabetes prevalence levels. North India contributes around 24% to 27% of demand, led by Delhi NCR, Punjab, Haryana, and Uttar Pradesh, supported by hospital and homecare diabetic nutrition adoption in metro and tier-1 clusters around Delhi, Gurugram, Noida, and Lucknow. Central and East India together account for 14% to 17% of demand, supported by Madhya Pradesh, West Bengal, Bihar, and Odisha, where organized pharmacy adoption is accelerating. In 2025, capacity additions and distribution operations by Abbott across West and South India, Dr. Reddy’s across pan-India networks, Nestlé Health Science across South India, and Danone across North India reinforced regional supply hubs, supporting closer execution of hospital and homecare projects across the India clinical nutrition for diabetes care market.

Recent Developments: India Clinical Nutrition for Diabetes Care Market

- The India clinical nutrition for diabetes care market witnessed strong momentum in launches and capacity progress during 2024 and 2025. India added a record 180 new diabetic nutrition SKUs in calendar year 2025, representing a 38% year-on-year increase from 130 SKUs in 2024, according to industry tracking. Online pharmacy platforms recorded over 40 million diabetic nutrition orders by mid-2025, with the powder segment accounting for 64% of new orders. Cumulative organized diabetic nutrition volume in India is projected to reach 30 to 34 thousand tonnes by FY27 from 24 thousand tonnes in FY25, growing at an average 14% annually.

- Global and domestic nutrition majors have deepened India-focused capacity expansion. In 2025, Abbott scaled diabetic nutrition capacity across its facilities, Dr. Reddy’s expanded Celevida production lines, Nestlé Health Science expanded Resource Diabetic supply, Danone grew its Nutricia diabetic portfolio, and British Biologicals expanded its clinical nutrition lines. Hexagon Nutrition entered new plant-based diabetic formula ranges. These developments are strengthening domestic supply and supporting the India clinical nutrition for diabetes care market forecast 2032.

- Online pharmacy and hospital nutrition momentum has gained strong traction in the India clinical nutrition for diabetes care market. In 2025, leading pharmacy and e-commerce players including Apollo Pharmacy, MedPlus, Tata 1mg, PharmEasy, and Netmeds expanded diabetic nutrition assortments. Strategic partnerships between nutrition brands and hospital chains are positioning India as one of the most actively scaling diabetic nutrition markets globally, strengthening long-term competitive positioning in the India clinical nutrition for diabetes care market forecast 2032.

Key Market Players: India Clinical Nutrition for Diabetes Care Market

- Abbott India Limited (Glucerna)

- Reddy’s Laboratories Limited (Celevida)

- Nestlé Health Science India (Resource Diabetic)

- Danone India Pvt. Ltd. (Nutricia Diasip)

- Fresenius Kabi India Pvt. Ltd. (Diben)

- Braun Medical (India) Pvt. Ltd.

- British Biologicals (D-Protin)

- Hexagon Nutrition Limited (Pentasure DM)

- Zydus Wellness Limited

- Pristine Organics Pvt. Ltd.

- Wockhardt Limited

- Sami-Sabinsa Group

- Mankind Pharma Limited

Report Scope

In this report, the India Clinical Nutrition for Diabetes Care Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

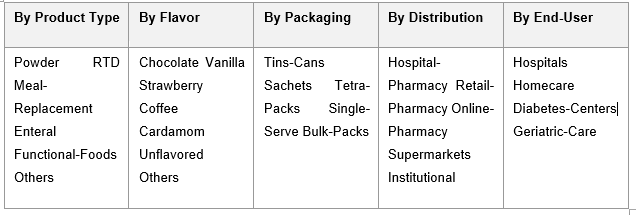

- By Product Type

- Oral Nutritional Supplements (Powder)

- Ready-to-Drink Formulas

- Diabetic Meal Replacements

- Enteral & Tube-Feeding Formulas

- Functional Diabetic Foods & Bars

- Others

- By Flavor

- Chocolate

- Vanilla

- Strawberry

- Coffee

- Cardamom & Kesar

- Unflavored

- Others

- By Packaging

- Tins & Cans

- Sachets & Pouches

- Tetra Packs & Bottles

- Single-Serve Packs

- Bulk & Institutional Packs

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Chemists

- Online Pharmacies & E-Commerce

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

- Direct & Institutional Sales

- By End-User

- Hospitals & Clinics

- Homecare & Households

- Specialty Diabetes Centers

- Long-Term & Geriatric Care

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Clinical Nutrition for Diabetes Care Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic diabetic nutrition brands, specialty plant-based and clinical nutrition producers, regional nutraceutical players, or niche hospital-nutrition brands.

The India Clinical Nutrition for Diabetes Care Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Flavor

- By Packaging

- By Distribution Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Clinical Nutrition for Diabetes Care Market

- India Clinical Nutrition for Diabetes Care Market Insights

- Market Dynamics

- Growth Drivers

- Rising diabetes prevalence, growing clinical awareness, and expanding hospital nutrition adoption driving diabetic nutrition demand across India.

- Growing healthcare infrastructure, rising disposable incomes, and increasing physician recommendations fuelling premium diabetic nutrition adoption.

- Product innovation in low-glycemic, high-protein, and plant-based diabetic formulas strengthening packaged clinical nutrition segment growth.

- Restraints

- Low awareness of diabetes-specific nutrition among rural and middle-income patients limiting penetration across India.

- High product cost and limited insurance reimbursement restricting affordability and frequency of diabetic nutrition use.

- Fragmented distribution and regulatory complexity around medical nutrition claims and labelling impacting overall market expansion.

- Opportunities

- Low-glycemic, plant-based, and millet-based diabetic nutrition innovation opening untapped patient pools across metro cities.

- Homecare, geriatric, and preventive nutrition expansion supporting next-generation growth in wellness and chronic-care segments.

- Online pharmacies, e-commerce, and teleconsultation-led nutrition prescriptions creating massive distribution opportunities.

- Challenges

- Intense competition from unorganized local supplements, generic protein powders, and unbranded nutrition products.

- Counterfeiting, mislabeling, and inconsistent quality across smaller Indian cities.

- Maintaining taste, glycemic consistency, and clinical efficacy at scale across diverse Indian patient groups.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (whey and plant proteins, slow-release carbohydrates, dietary fiber, vitamins, minerals, sweeteners, packaging materials)

- Clinical Nutrition Manufacturers & Processors (Abbott, Dr. Reddy’s, Nestlé Health Science, Danone, British Biologicals)

- Flavor & Ingredient Suppliers (vanilla, chocolate, isomaltulose, inulin, micronutrient premixes)

- Specialty & Plant-Based Nutrition Makers (soy, pea protein, millet-based diabetic formulas)

- Quality Control, R&D & Testing Laboratories (FSSAI, BIS, ISO food safety standards)

- Distributors, Wholesalers & Modern Trade (B2B and B2C distribution networks)

- Hospitals, Clinics & Diabetes Centers (Apollo, Fortis, Max, Manipal, AIIMS)

- Brand Owners & Nutrition Companies (Abbott, Nestlé, Danone, Dr. Reddy’s, Fresenius Kabi)

- Retail Channels & Online Pharmacies (Apollo Pharmacy, MedPlus, Tata 1mg, PharmEasy, Netmeds)

- End-Users (hospitals, homecare patients, caregivers, diabetes centers, geriatric facilities)

- India Clinical Nutrition for Diabetes Care Market: Regulatory Framework

- India Clinical Nutrition for Diabetes Care Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Thousand Tonnes)

- Market Share & Forecast

- By Product Type

- Oral Nutritional Supplements (Powder)

- Ready-to-Drink Formulas

- Diabetic Meal Replacements

- Enteral & Tube-Feeding Formulas

- Functional Diabetic Foods & Bars

- Others

- By Flavor

- Chocolate

- Vanilla

- Coffee

- Cardamom & Kesar

- Unflavored

- Banana

- Others

- By Packaging

- Tins & Cans

- Sachets & Pouches

- Tetra Packs & Bottles

- Single-Serve Packs

- Bulk & Institutional Packs

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Chemists

- Online Pharmacies & E-Commerce

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

- Direct & Institutional Sales

- By End-User

- Hospitals & Clinics

- Homecare & Households

- Specialty Diabetes Centers

- Long-Term & Geriatric Care

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Clinical Nutrition for Diabetes Care Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Abbott India Limited (Glucerna)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

(Same Data Pointers Will Be Provided for The Below Companies)

- Reddy’s Laboratories Limited (Celevida)

- Nestlé Health Science India (Resource Diabetic)

- Danone India Pvt. Ltd. (Nutricia Diasip)

- Fresenius Kabi India Pvt. Ltd. (Diben)

- Braun Medical (India) Pvt. Ltd.

- British Biologicals (D-Protin)

- Hexagon Nutrition Limited (Pentasure DM)

- Zydus Wellness Limited

- Pristine Organics Pvt. Ltd.

- Wockhardt Limited

- Sami-Sabinsa Group

- Mankind Pharma Limited

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India clinical nutrition for diabetes care market and what is its growth forecast?

Ans: The India clinical nutrition for diabetes care market is valued at USD 380 million in 2025 and projected to reach USD 810 million by 2032, growing at a CAGR of 11.5% on rising diabetes prevalence.

2. Which segments are driving demand in the India clinical nutrition for diabetes care market?

Ans: Oral nutritional supplement powders lead with over 55% value share, while ready-to-drink and plant-based diabetic formulas are the fastest-growing segments, driven by working patients, caregivers, and health-conscious urban consumers.

3. What are the key drivers of growth in the India clinical nutrition for diabetes care market?

Ans: Key drivers include rising diabetes prevalence, growing clinical awareness, expanding hospital and homecare nutrition, rising disposable incomes, product innovation in low-glycemic and plant-based formulas, and rapid scaling of online pharmacies.

4. Which regions are driving growth in the India clinical nutrition for diabetes care market?

Ans: South India and West India lead with around 55% to 59% of total value, driven by Karnataka, Tamil Nadu, Telangana, Maharashtra, and Gujarat. North India and Delhi NCR also show strong demand.

5. What are the latest trends in the India clinical nutrition for diabetes care market?

Ans: The latest trends include rapid adoption of low-glycemic, plant-based, and millet-based diabetic nutrition, growth in online pharmacy delivery, rising demand for high-protein variants, and clinically validated formula innovation.

Frequently Asked Questions

1. How large is the India clinical nutrition for diabetes care market and what is its growth forecast?

Ans: The India clinical nutrition for diabetes care market is valued at USD 380 million in 2025 and projected to reach USD 810 million by 2032, growing at a CAGR of 11.5% on rising diabetes prevalence.

2. Which segments are driving demand in the India clinical nutrition for diabetes care market?

Ans: Oral nutritional supplement powders lead with over 55% value share, while ready-to-drink and plant-based diabetic formulas are the fastest-growing segments, driven by working patients, caregivers, and health-conscious urban consumers.

3. What are the key drivers of growth in the India clinical nutrition for diabetes care market?

Ans: Key drivers include rising diabetes prevalence, growing clinical awareness, expanding hospital and homecare nutrition, rising disposable incomes, product innovation in low-glycemic and plant-based formulas, and rapid scaling of online pharmacies.

4. Which regions are driving growth in the India clinical nutrition for diabetes care market?

Ans: South India and West India lead with around 55% to 59% of total value, driven by Karnataka, Tamil Nadu, Telangana, Maharashtra, and Gujarat. North India and Delhi NCR also show strong demand.

5. What are the latest trends in the India clinical nutrition for diabetes care market?

Ans: The latest trends include rapid adoption of low-glycemic, plant-based, and millet-based diabetic nutrition, growth in online pharmacy delivery, rising demand for high-protein variants, and clinically validated formula innovation.