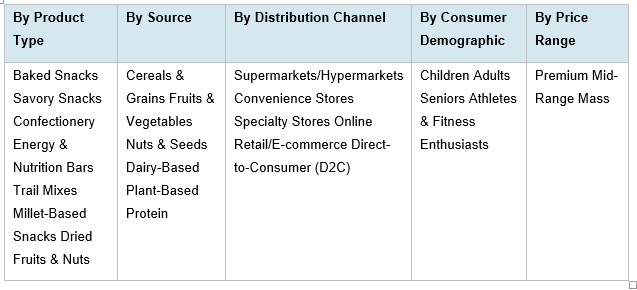

India Organic Snacks Market, By Product Type (Baked Snacks, Savory Snacks, Confectionery, Energy & Nutrition Bars, Trail Mixes, Millet-Based Snacks, Dried Fruits & Nuts, Others); By Source (Cereals & Grains, Fruits & Vegetables, Nuts & Seeds, Dairy-Based, Plant-Based Protein); By Packaging (Pouches, Boxes, Cans, Bags, Multi-Pack); By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail/E-commerce, Direct-to-Consumer); By Consumer Demographic (Children, Adults, Seniors, Athletes & Fitness Enthusiasts); By Price Range (Premium, Mid-Range, Mass); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Food, Beverage & Nutrition

- May 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Organic Snacks Market: Health-Conscious Consumption and Millet Revolution Powering Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

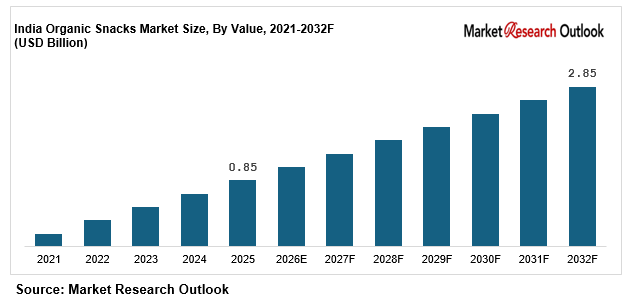

| Market Size (2025) | USD 0.85 Billion |

| CAGR (2026-2032) | 18.9% |

| Leading Segment | Organic Baked Snacks (Cookies, Biscuits & Crackers) |

| Fastest Growing Segment | Millet-Based Snacks & Organic Energy Bars |

| Market Size (2032) | USD 2.85 Billion |

Source: Market Research Outlook

Market Overview: India Organic Snacks Market

The India organic snacks market size is witnessing rapid expansion, driven by rising health consciousness across urban India, accelerating demand for clean-label snacking, the millet-led nutrition push under Shree Anna Yojana, expanding e-commerce and quick-commerce reach, and major investments by domestic organic snack brands. Valued at USD 0.85 billion in 2025 and projected to reach USD 2.85 billion by 2032, growing at a CAGR of 18.9%, the India organic snacks market growth is being fuelled by strong demand for organic baked snacks under premium urban adoption, rising millet-based snack innovation tied to government nutrition campaigns, and growing institutional procurement across schools, gyms, and corporate cafeterias. Organic baked snacks lead consumption in the India organic snacks market, while the millet-based snacks segment is emerging as the fastest growing category. Tightening FSSAI clean-label norms, India Organic and Jaivik Bharat certification mandates, and the national mission on organic farming are reshaping the supply landscape. As domestic majors including Organic India, 24 Mantra Organic, Conscious Food, Phalada Pure & Sure, and Pro Nature Organic expand integrated farm-to-shelf capacity, and D2C organic snack brands such as Yogabar, Open Secret, Slurrp Farm, Soulfull, and The Whole Truth scale product pipelines, the India organic snacks market is evolving into a health-led, technology-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Organic Snacks Market

- The India organic snacks market size is projected to grow from USD 0.85 billion in 2025 to USD 2.85 billion by 2032, registering a strong CAGR of 18.9%, driven by accelerated urban health awareness, rising millet-based snack adoption, and the structural shift toward clean-label, preservative-free organic snacking across India.

- Organic baked snacks dominate the India organic snacks market, accounting for over 32% of total revenue in 2025, supported by rising demand for organic cookies, biscuits, crackers, and ragi-based bakes among urban families, growing offtake in metros, and rapid expansion of D2C bakery brands across Tier-1 and Tier-2 cities.

- Millet-based organic snacks and energy bars are emerging as the fastest growing segment of the India organic snacks market, expected to grow at 22% to 26% annually as Shree Anna Yojana, the International Year of Millets follow-through, fitness-led consumption, and high-protein clean-label demand reshape consumer sourcing strategies.

- Rapid scaling of organic farming acreage under NPOP and PKVY, with India crossing 2.6 million hectares of certified organic farmland by 2024 and over 1.9 million certified organic farmers, is structurally expanding the India organic snacks market across baked, savory, millet-based, and dried fruit categories.

- Rising investments by domestic organic majors such as Organic India, 24 Mantra Organic, Conscious Food, Phalada Pure & Sure, and Pro Nature Organic in farm sourcing, processing, and integrated retail are strengthening local supply and supporting the India organic snacks market forecast 2032.

Key Market Drivers: India Organic Snacks Market

Rising Health Consciousness and Lifestyle Disease Burden Driving Clean-Label Organic Snack Adoption

Growth in the India organic snacks market is being driven by rising health consciousness across urban India, with the country reporting over 101 million diabetes cases and 315 million pre-diabetes cases per ICMR-INDIAB 2023 data, alongside one of the highest cardiovascular disease burdens globally. Consumer demand has shifted decisively toward organic snacks free from synthetic pesticides, preservatives, refined sugar, and trans fats. Urban Indian households now allocate close to 9% to 11% of their food spend to packaged snacks, with the organic share rising sharply post-2020. Per-capita organic food penetration in India remains below 1% of addressable urban consumers, indicating significant long-term headroom. Government nutrition campaigns, falling certification costs, and growing recognition of India Organic and Jaivik Bharat marks are creating strong structural pull-through demand across the India organic snacks market.

Government Initiatives, NPOP and PKVY Schemes Strengthening Organic Snack Supply Chains

The India organic snacks market is benefiting from sustained government policy support, with India’s organic farmland crossing 2.6 million hectares by 2024 under the National Programme for Organic Production (NPOP) and Paramparagat Krishi Vikas Yojana (PKVY), alongside the Mission Organic Value Chain Development for North Eastern Region (MOVCDNER) and the Shree Anna Yojana focused on millet revival. Certified organic farmer numbers have crossed 1.9 million, making India home to the world’s largest organic farming community by participant count. Combined budget outlays of over INR 1,584 crore under PKVY and INR 600 crore under the Shree Anna Yojana have strengthened raw-material supply, helping organic snack brands such as 24 Mantra Organic, Conscious Food, Soulfull, and Slurrp Farm secure traceable inputs. The One District One Product (ODOP) initiative and APEDA’s Tracenet platform have further reinforced certification credibility, supporting price competitiveness and trust across the India organic snacks market.

E-commerce, Quick-Commerce and D2C Channel Expansion Driving Organic Snack Demand

Rapid growth of e-commerce, quick-commerce, and direct-to-consumer (D2C) channels is a major catalyst for the India organic snacks market, with online channels projected to contribute over 28% of organic snack sales by 2030. Platforms such as Amazon, Flipkart, BigBasket, Blinkit, Zepto, and Swiggy Instamart have made premium organic snack brands accessible across Tier-1, Tier-2, and Tier-3 cities. Consumer adoption is accelerating, with average organic snack basket sizes on quick-commerce platforms rising 35% to 45% year-on-year in 2025. Leading D2C organic snack brands such as Yogabar, Open Secret, Slurrp Farm, The Whole Truth Foods, True Elements, and Happilo have scaled subscription and bundling models. The Indian D2C food market alone represents an estimated USD 4 to 5 billion addressable opportunities by 2030. Government Digital India initiatives combined with rising smartphone-led discovery are structurally expanding India organic snacks market growth across all major consumer categories through 2032.

Key Market Challenges: India Organic Snacks Market

High Price Premium and Limited Affordability for Mass-Market Consumers

The India organic snacks market continues to face challenges around high price premiums and limited affordability for mass-market consumers, with a typical organic snack pack costing 40% to 80% more than conventional alternatives. While urban premium and middle-class buyers are willing to pay this gap, penetration into mass-market segments remains capped, as average monthly per-capita food spending in semi-urban India hovers around INR 1,500 to 2,000. Organic certification fees of INR 25,000 to 60,000 per cycle, limited domestic processing capacity, and small-batch production economics keep landed costs elevated for organic snack manufacturers. EMI-linked subscription models for premium organic snacks remain underdeveloped, while supermarkets and traditional kirana stores continue to be cautious in stocking high-priced organic SKUs in non-metro markets. India’s continued dependence on premium positioning limits adoption among middle-income and rural households across the India organic snacks market.

Fragmented Certification, Mislabelling Risks and Supply Chain Integrity Issues

The India organic snacks market faces structural complexity from fragmented certification, mislabelling risks, and supply chain integrity issues across multiple states. While the India Organic, Jaivik Bharat, and PGS-India marks have created a national framework, smaller regional players often use ambiguous claims such as natural, farm-fresh, or chemical-free, which dilute consumer trust. Average certification cycle timelines range between 36 and 48 months for full organic conversion, creating long lead times. APEDA-administered NPOP, PGS-India, and FSSAI organic norms operate parallelly, generating compliance overhead. Differential treatment of imported organic ingredients, residue norms, and labelling rules across states creates operational complexity for pan-India organic snack brands such as Organic India, 24 Mantra Organic, Phalada Pure & Sure, and Conscious Food. While FSSAI has tightened the Food Safety and Standards (Organic Foods) Regulations 2017, certification fragmentation remains a near-term challenge for the India organic snacks market.

Short Shelf-Life, Cold-Chain Gaps and Tier-2 and Tier-3 Distribution Constraints

The India organic snacks market faces practical constraints around short shelf-life, cold-chain gaps, and distribution reach in Tier-2 and Tier-3 cities. Preservative-free organic snacks typically carry shelf-lives of 3 to 6 months, compared to 9 to 12 months for conventional snacks, increasing inventory risk for distributors. India’s organised cold-chain infrastructure penetration remains below 11% of total perishable food output, with rural last-mile coverage particularly weak in central and eastern India. Average wastage rates for premium organic snacks in non-metro markets touch 8% to 15%, eroding gross margins. Modern trade, organised retail, and quick-commerce platforms cover roughly 28% of total snack distribution, leaving a large share of India’s consumer base under-served. While brands like Soulfull, Slurrp Farm, and True Elements are scaling pan-India logistics through ITC and Mondelez-linked networks, distribution fragmentation remains a barrier to widespread adoption across the India organic snacks market.

Key Market Trends: India Organic Snacks Market

Rapid Adoption of Millet, Ragi, Jowar and Bajra-Based Organic Snack Innovation in India

The India organic snacks market is undergoing a clear shift toward millet-based, ragi-based, jowar-based, and bajra-based innovation, with millet-led organic snacks expected to capture over 24% of new launches by 2027. Millet-based snacks deliver protein densities of 11 to 14 grams per 100 grams, compared to 6 to 8 grams in traditional refined-flour snacks, while offering high fibre, low glycemic index, and gluten-free attributes. Leading domestic brands including Soulfull (Tata Consumer Products), Slurrp Farm, Two Brothers Organic Farms, Mille, and 24 Mantra Organic have scaled millet-based snack production through 2024 and 2025. Premium organic bars from Yogabar, True Elements, and The Whole Truth Foods are integrating millet bases with nuts and seeds, particularly in Tier-1 metros where consumer awareness is highest. This nutrition transition is reinforcing the India organic snacks market forecast 2032 across both kids and adult categories.

Growth of D2C, Quick-Commerce and Subscription Models in the India Organic Snacks Market

A clear shift toward D2C, quick-commerce, and subscription-led business models is reshaping the India organic snacks market, particularly in the premium urban segment. Under D2C and subscription models, brands deliver organic snacks directly to consumers under monthly plans of INR 499 to INR 1,499, often at price points 15% to 25% below MRP through bundling. Leading D2C and digital-first organic snack brands such as Yogabar, Open Secret, The Whole Truth Foods, Happilo, True Elements, and Nourish You have built combined online consumer bases exceeding 5 million users. Quick-commerce platforms including Blinkit, Zepto, and Swiggy Instamart now contribute 14% to 18% of online organic snack sales, with 10-minute delivery driving impulse purchases. Online aggregators and digital first-mile platforms such as Amazon, Flipkart, and BigBasket are also reducing customer acquisition costs and accelerating organic snack adoption across both kids and adult segments of the India organic snacks market.

Capacity Expansion by Domestic Organic Food Manufacturers and Vertical Integration

A wave of domestic capacity expansion and vertical integration is reshaping the India organic snacks market supply landscape. Combined India-focused capital expenditure announcements in organic food processing, contract farming, and packaging exceeded USD 350 million across 2023 to 2025. 24 Mantra Organic (Sresta Natural Bioproducts) expanded sourcing acreage beyond 200,000 acres, Organic India scaled global exports while deepening Indian retail presence, Phalada Pure & Sure grew its Karnataka processing facility, Tata Consumer Products integrated Soulfull into its broader portfolio, and ITC scaled Aashirvaad organic and Sunfeast Farmlite ranges. Approved certification under NPOP, India Organic registrations, and Production Linked Incentive (PLI) scheme allocations for food processing exceeding INR 10,900 crore have structurally favoured domestic supply. Combined with Shree Anna Yojana driving millet demand and D2C procurement scaling rapidly, these developments are reinforcing the India organic snacks market forecast 2032 across the entire value chain.

Segmental Insights: India Organic Snacks Market

By Product Type: Organic Baked Snacks Segment Dominates the India Organic Snacks Market

The organic baked snacks segment dominates the India organic snacks market, accounting for an estimated 30% to 32% of total revenue, driven by rising demand for organic cookies, biscuits, ragi-based bakes, and whole-wheat crackers, expanding D2C bakery brands, and improving urban distribution. Cookies and biscuits are the dominant sub-category within this segment, with on-shelf premium variants capturing over 60% of organic baked snack sales. Savory snacks contribute another 19% to 21% of demand, driven by organic chips, makhana, roasted chana, and millet puffs adopted by health-led consumers. Millet-based snacks account for 14% to 16%, growing fastest. Confectionery and dried fruits each contribute 9% to 11%. In 2025, leading organic snack brands including 24 Mantra Organic, Conscious Food, Soulfull, Slurrp Farm, and Yogabar scaled up baked and millet-based snack deployment under premium retail and D2C mandates, reinforcing segment dominance in the India organic snacks market.

By Source: Cereals and Grains Lead While Nuts, Seeds and Millets Grow Fastest

Organic cereals and grains lead the India organic snacks market source landscape, accounting for approximately 44% to 47% of total raw-material usage, driven by their broad applicability across baked snacks, energy bars, breakfast crunchies, and savory mixes. Fruits and vegetables contribute another 16% to 18%, primarily in dried fruit snacks, fruit chips, and trail mixes. Nuts and seeds along with millet-based sources are the fastest growing categories within the India organic snacks market, expanding at 22% to 26% annually, driven by superior protein content of 11% to 14%, gluten-free attributes, and growing adoption in premium and athlete-focused snack lines. Plant-based protein sources and dairy-based organic ingredients together account for 8% to 10% of the market, with plant-based protein expected to grow rapidly through 2032. Leading domestic manufacturers including 24 Mantra Organic, Organic India, Phalada Pure & Sure, Conscious Food, and Soulfull have aligned product portfolios to this source mix, driving high-protein organic snack adoption across the India organic snacks market.

Regional Insights: India Organic Snacks Market

Regional analysis of the India organic snacks market shows that South India and West India collectively account for approximately 56% to 60% of total organic snack consumption, driven by Karnataka (Bengaluru leads urban organic snack penetration nationwide), Tamil Nadu (Chennai, Coimbatore), Maharashtra (Mumbai, Pune), Gujarat, and Telangana, supported by strong urban health awareness and high disposable incomes. North India contributes around 22% to 25% of demand, led by Delhi NCR, Punjab, Haryana, and Uttar Pradesh, supported by retail and D2C adoption in metro and Tier-1 city clusters around Delhi, Gurugram, Noida, and Jaipur. Central and East India together account for 14% to 17% of demand, supported by Madhya Pradesh, West Bengal, Odisha, and Chhattisgarh, where Shree Anna Yojana adoption is accelerating millet-based snack uptake. In 2025, capacity additions and retail operations by 24 Mantra Organic across South India, Organic India in Uttar Pradesh, Soulfull and Slurrp Farm across pan-India retail, and Conscious Food across Maharashtra and Gujarat reinforced regional supply hubs, supporting closer execution of premium and mass organic snack projects across the India organic snacks market.

Recent Developments: India Organic Snacks Market

- The India organic snacks market witnessed strong momentum in launches and policy progress during 2024 and 2025. India’s organic food sector recorded retail value growth of over 24% year-on-year in 2025, with the organic snacks sub-segment growing at 27%, according to APEDA and industry data. Shree Anna Yojana-linked millet snack launches crossed 180 new SKUs by mid-2025, with the millet-based segment accounting for 22% of new product introductions. Cumulative organic food retail sales in India are projected to reach USD 4.8 to 5.2 billion by FY27, growing at an average 25% annually.

- Domestic organic snack manufacturers have deepened India-focused capacity expansion. In 2025, 24 Mantra Organic scaled contract-farmed sourcing beyond 200,000 acres with new ragi and jowar lines, Organic India expanded retail SKUs across Tier-2 cities, Conscious Food commissioned new clean-label processing capacity, Soulfull (Tata Consumer Products) expanded its millet bowl and ragi bites range, and Slurrp Farm grew its kids’ organic snack catalogue. The Whole Truth Foods completed a Series B funding round and expanded clean-label bar production. These developments are strengthening domestic supply and supporting the India organic snacks market forecast 2032.

- D2C and quick-commerce momentum has gained strong traction in the India organic snacks market. In 2025, leading D2C and digital-first organic snack brands including Yogabar (ITC-backed), Open Secret, Happilo, True Elements (Marico-backed), The Whole Truth Foods, and Nourish You expanded contracted retail portfolios. Strategic partnerships between domestic organic food manufacturers and quick-commerce platforms such as Blinkit, Zepto, and Swiggy Instamart are positioning India as one of the most actively scaling organic snack markets globally, strengthening long-term competitive positioning in the India organic snacks market forecast 2032.

Key Market Players: India Organic Snacks Market

- Organic India Pvt. Ltd.

- 24 Mantra Organic (Sresta Natural Bioproducts Pvt. Ltd.)

- Conscious Food Pvt. Ltd.

- Phalada Pure & Sure (Phalada Agro Research Foundations Pvt. Ltd.)

- Pro Nature Organic Foods Pvt. Ltd.

- Soulfull (Tata Consumer Products Ltd.)

- Yogabar (Sproutlife Foods Pvt. Ltd.)

- Slurrp Farm (Wholsum Foods Pvt. Ltd.)

- Open Secret (Open Secret Healthy Snacks Pvt. Ltd.)

- True Elements (Hey Kitto Pvt. Ltd.)

- The Whole Truth Foods (And Nothing Else Pvt. Ltd.)

- Happilo International Pvt. Ltd.

- Nourish You Pvt. Ltd.

Report Scope

In this report, the India Organic Snacks Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Baked Snacks (Cookies, Biscuits, Crackers, Ragi Bakes)

- Savory Snacks (Chips, Makhana, Roasted Chana, Millet Puffs)

- Confectionery (Organic Chocolates, Candies, Jellies)

- Energy & Nutrition Bars

- Trail Mixes

- Millet-Based Snacks

- Dried Fruits & Nuts

- Others

- By Source

- Cereals & Grains

- Fruits & Vegetables

- Nuts & Seeds

- Dairy-Based

- Plant-Based Protein

- By Packaging

- Pouches

- Boxes

- Cans

- Bags

- Multi-Pack

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail/E-commerce

- Direct-to-Consumer (D2C)

- By Consumer Demographic

- Children

- Adults

- Seniors

- Athletes & Fitness Enthusiasts

- By Price Range

- Premium

- Mid-Range

- Mass

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Organic Snacks Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic organic snack brands, specialty millet-based and gluten-free producers, D2C and subscription-led players, or niche regional organic food brands.

The India Organic Snacks Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Source

- By Distribution Channel

- By Consumer Demographic

- By Price Range

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Organic Snacks Market

- India Organic Snacks Market Insights

- Market Dynamics

- Growth Drivers

- Rising health consciousness and lifestyle disease burden driving clean-label organic snack adoption.

- Government initiatives, NPOP and PKVY schemes strengthening organic snack supply chains.

- E-commerce, quick-commerce and D2C channel expansion driving organic snack demand.

- Restraints

- High price premium and limited affordability for mass-market consumers.

- Fragmented certification, mislabelling risks and supply chain integrity issues creating regulatory complexity.

- Short shelf-life, cold-chain gaps and Tier-2 and Tier-3 distribution constraints limiting reach.

- Opportunities

- Shree Anna Yojana and millet revival creating a massive long-term millet-based organic snack opportunity.

- Premium kids’ organic snack segment and clean-label nutrition for children opening new value pools.

- Plant-based protein, vegan and gluten-free product innovation supporting next-generation growth.

- Challenges

- Slow consumer trial-to-repeat conversion of premium organic snacks limiting near-term scale.

- Limited skilled workforce for organic food processing, certification audits and quality assurance.

- Cold-chain integration constraints, last-mile delivery limitations, and certification fragmentation in select states.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Growth Drivers

- Industry Value Chain & Entry Points

- Upstream Raw Materials (organic grains, millets, nuts, seeds, fruits, dairy)

- Organic Farmers & Producer Companies (FPOs, contract farming, certified clusters)

- Processing, Roasting & Bakery Units (clean-label, gluten-free, vegan lines)

- Packaging & Cold-Chain Suppliers (compostable, recyclable, sustainable packaging)

- Quality Control, Certification & Testing Laboratories (NPOP, India Organic, Jaivik Bharat, FSSAI)

- Distributors, Modern Trade & Online Aggregators (B2B and B2C platforms)

- E-commerce & Quick-Commerce Platforms (Amazon, Flipkart, BigBasket, Blinkit, Zepto, Swiggy Instamart)

- Brand Owners & D2C Players (Organic India, 24 Mantra Organic, Soulfull, Yogabar, Slurrp Farm)

- Retail Stores, Specialty Outlets & Direct Channels (organic specialty stores, kirana, supermarkets)

- End-Users (children, adults, seniors, athletes, fitness enthusiasts, institutional buyers)

- India Organic Snacks Market: Regulatory Framework

- India Organic Snacks Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Tonnes)

- Market Share & Forecast

- By Product Type

- Baked Snacks

- Savory Snacks

- Confectionery

- Energy & Nutrition Bars

- Trail Mixes

- Millet-Based Snacks

- Dried Fruits & Nuts

- Others

- By Source

- Cereals & Grains

- Fruits & Vegetables

- Nuts & Seeds

- Dairy-Based

- Plant-Based Protein

- By Packaging

- Pouches

- Boxes

- Cans

- Bags

- Multi-Pack

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail/E-commerce

- Direct-to-Consumer (D2C)

- By Consumer Demographic

- Children

- Adults

- Seniors

- Athletes & Fitness Enthusiasts

- By Price Range

- Premium

- Mid-Range

- Mass

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Organic Snacks Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Organic India Pvt. Ltd.

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- 24 Mantra Organic (Sresta Natural Bioproducts Pvt. Ltd.)

- Conscious Food Pvt. Ltd.

- Phalada Pure & Sure (Phalada Agro Research Foundations Pvt. Ltd.)

- Pro Nature Organic Foods Pvt. Ltd.

- Soulfull (Tata Consumer Products Ltd.)

- Yogabar (Sproutlife Foods Pvt. Ltd.)

- Slurrp Farm (Wholsum Foods Pvt. Ltd.)

- Open Secret (Open Secret Healthy Snacks Pvt. Ltd.)

- True Elements (Hey Kitto Pvt. Ltd.)

- The Whole Truth Foods (And Nothing Else Pvt. Ltd.)

- Happilo International Pvt. Ltd.

- Nourish You Pvt. Ltd.

- Other Prominent Players

- Organic India Pvt. Ltd.

- By Product Type

- Market Size & Forecast, 2021-2032

- Market Dynamics

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India organic snacks market and what is its growth forecast?

Ans: The India organic snacks market is valued at USD 0.85 billion in 2025 and is projected to reach USD 2.85 billion by 2032, growing at a strong CAGR of 18.9%, driven by rising health awareness and clean-label demand.

2. Which segments are driving demand in the India organic snacks market?

Ans: Organic baked snacks lead the India organic snacks market with over 32% revenue share, while millet-based snacks and energy bars are the fastest growing segments, supported by Shree Anna Yojana and rising fitness-led consumption.

3. What are the key drivers of growth in the India organic snacks market?

Ans: Key India organic snacks market drivers include rising lifestyle disease burden, NPOP and PKVY government support, e-commerce and quick-commerce expansion, millet-led innovation, and strong D2C brand adoption across urban Indian households.

4. Which regions are driving growth in the India organic snacks market?

Ans: South India and West India lead the India organic snacks market with around 58% combined share, driven by Bengaluru, Chennai, Mumbai, Pune, and Hyderabad, followed by North India led by Delhi NCR.

5. What are the latest trends in the India organic snacks market?

Ans: Latest India organic snacks market trends include rapid millet-based snack innovation, quick-commerce led D2C growth, clean-label and vegan launches, subscription bundling, plant-based protein bars, and premium kids' organic snack expansion.

6.

Ans:

Frequently Asked Questions

1. How large is the India organic snacks market and what is its growth forecast?

Ans: The India organic snacks market is valued at USD 0.85 billion in 2025 and is projected to reach USD 2.85 billion by 2032, growing at a strong CAGR of 18.9%, driven by rising health awareness and clean-label demand.

2. Which segments are driving demand in the India organic snacks market?

Ans: Organic baked snacks lead the India organic snacks market with over 32% revenue share, while millet-based snacks and energy bars are the fastest growing segments, supported by Shree Anna Yojana and rising fitness-led consumption.

3. What are the key drivers of growth in the India organic snacks market?

Ans: Key India organic snacks market drivers include rising lifestyle disease burden, NPOP and PKVY government support, e-commerce and quick-commerce expansion, millet-led innovation, and strong D2C brand adoption across urban Indian households.

4. Which regions are driving growth in the India organic snacks market?

Ans: South India and West India lead the India organic snacks market with around 58% combined share, driven by Bengaluru, Chennai, Mumbai, Pune, and Hyderabad, followed by North India led by Delhi NCR.

5. What are the latest trends in the India organic snacks market?

Ans: Latest India organic snacks market trends include rapid millet-based snack innovation, quick-commerce led D2C growth, clean-label and vegan launches, subscription bundling, plant-based protein bars, and premium kids' organic snack expansion.

6.

Ans: