India Food Services Market, By Service Type (Full-Service Restaurants, Quick Service Restaurants, Cafes & Bars, Cloud Kitchens, Pubs/Bars/Lounges, Frozen Yogurt/Ice Cream Parlours, Bakery & Sweet Shops, Others); By Cuisine Type (Indian, Asian, European, Continental, North American, Middle Eastern, Others); By Ownership (Standalone Outlets, Chained Outlets); By Order Mode (Dine-In, Takeaway, Online Food Delivery, Drive-Thru); By Pricing Tier (Premium, Mid-Range, Mass/Value); By End-User (Individual Consumers, Corporates, Institutional, Travel & Hospitality); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Food, Beverage & Nutrition

- May 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Food Services Market: QSR Expansion, Cloud Kitchens and Online Food Delivery Powering Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

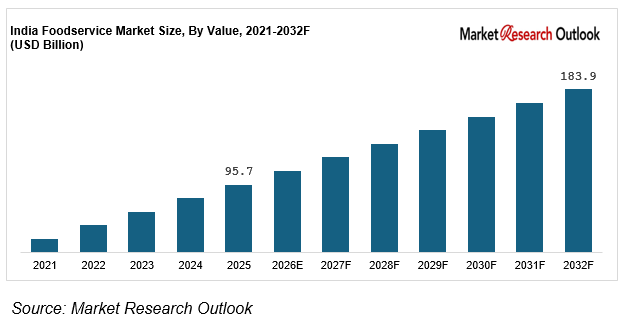

| Market Size (2025) | USD 95.7 Billion |

| CAGR (2026-2032) | 9.8% |

| Leading Segment | Quick Service Restaurants (QSR) – Chained Outlets |

| Fastest Growing Segment | Cloud Kitchens & Online Food Delivery |

| Market Size (2032) | USD 183.9 Billion |

Source: Market Research Outlook

Market Overview: India Food Services Market

The India food services market size is witnessing rapid expansion, driven by the world’s largest young consumer base in eating-out and ordering-in categories, rising disposable income, the accelerated scaling of online food delivery and cloud kitchens, expanding Tier-2 and Tier-3 city QSR penetration, and major capacity additions by domestic and global restaurant chains. Valued at USD 95.7 billion in 2025 and projected to reach USD 183.9 billion by 2032, growing at a CAGR of 9.8%, the India food services market growth is being fuelled by strong organised QSR demand, rising online food delivery led by Zomato (Eternal) and Swiggy, growing café and casual dining adoption across metros, and rapid expansion of cloud kitchens. Quick Service Restaurants lead consumption in the India food services market, while cloud kitchens and online food delivery are emerging as the fastest growing category. Tightening FSSAI hygiene mandates, GST input credit reforms, and the national push toward formalisation of the eating-out economy are reshaping the supply landscape. As domestic majors including Jubilant FoodWorks, Devyani International, Sapphire Foods, Westlife Foodworld, and Restaurant Brands Asia expand integrated outlet-to-delivery capacity, and digital-first operators such as Zomato (Eternal), Swiggy, Rebel Foods, EatClub, and Curefoods scale cloud kitchen pipelines, the India food services market is evolving into a consumer-led, technology-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Food Services Market

- The India food services market size is projected to grow from USD 95.7 billion in 2025 to USD 183.9 billion by 2032, registering a strong CAGR of 9.8%, driven by accelerated urbanisation-led eating-out adoption, rising online food delivery uptake, and the structural shift toward organised, chained, and digitally enabled foodservice consumption.

- Quick Service Restaurants (QSR) dominate the India food services market, accounting for over 22% of total organised foodservice revenue in 2025, driven by aggressive chain expansion by Domino’s, McDonald’s, KFC, Pizza Hut, Burger King, and Subway, falling unit economics in Tier-2/3 cities, and rising young consumer demand for affordable, fast, and consistent meals.

- Cloud kitchens and online food delivery are emerging as the fastest growing segment in the India food services market, expected to grow at 18% to 22% annually as digital ordering, 10-minute food delivery, multi-brand operators, and corporate dining mandates reshape consumer sourcing strategies.

- Rapid scaling of online food delivery aggregators, with Zomato (Eternal) and Swiggy collectively processing over 2.5 million daily orders by mid-2025 and India’s online food delivery market crossing USD 9.5 billion in gross order value, is structurally expanding the India food services market across QSR, casual dining, cafe, and cloud kitchen categories.

- Rising investments by domestic and global food services majors such as Jubilant FoodWorks, Devyani International, Sapphire Foods, Westlife Foodworld, Restaurant Brands Asia, and Tata Starbucks in outlet expansion, central kitchens, and integrated supply chain are strengthening local execution and supporting the India food services market forecast 2032.

Key Market Drivers: India Food Services Market

Rising Disposable Income, Urbanisation and Young Demographics Driving Organised Foodservice Adoption

Growth in the India food services market is being driven by rising disposable income, accelerating urbanisation, and a young demographic profile, with over 65% of India’s 1.4 billion population below the age of 35 and the urban consumer base crossing 520 million by 2025. India’s per-capita disposable income has grown at a CAGR of 9% to 10% between 2019 and 2025, with nuclear families and dual-income households driving eating-out frequency from 5 times a month in 2019 to over 9 times a month in 2025 in Tier-1 metros. Per-capita organised foodservice spending in India remains below 35% of addressable urban consumption, indicating significant long-term headroom for growth. Government formalisation initiatives, falling unit-level capex of INR 35 lakh to 1 crore per QSR outlet, and rising premium eating-out across cafes, casual dining, and pubs are creating strong structural pull-through demand across the India food services market.

Online Food Delivery, Quick-Commerce and Cloud Kitchen Expansion Strengthening Off-Premise Consumption

The India food services market is benefiting from a sustained surge in online food delivery, quick-commerce, and cloud kitchen formats, with the online food delivery sub-segment crossing USD 9.5 billion in gross order value in 2025, expanding at 22% year-on-year. Zomato (Eternal) and Swiggy collectively process over 2.5 million daily food orders, while quick-commerce platforms such as Blinkit, Zepto, Swiggy Instamart, and BigBasket Now have added 10-minute ready-to-eat food categories. Average online food delivery order value in metros has risen to INR 380 to 450 per order, with restaurant-partnered orders contributing over 65% of total volumes. Cloud kitchen capacity has scaled rapidly, with India’s organised cloud kitchen base exceeding 4,500 outlets by 2025, led by Rebel Foods, EatClub, Curefoods, Biryani By Kilo, and Bowl Company. Approved FSSAI cloud kitchen norms and digital-only license simplifications have further strengthened off-premise supply, supporting cost competitiveness across the India food services market.

Tier-2/3 City Expansion, Corporate Dining and Tourism Recovery Driving Multi-Format Demand

Rapid growth in Tier-2 and Tier-3 cities is a major catalyst for the India food services market, with non-metro QSR, cafe, and casual dining outlets projected to grow at 14% to 16% annually through 2032. Cities such as Lucknow, Indore, Jaipur, Surat, Coimbatore, Kochi, Visakhapatnam, and Bhubaneswar are emerging as new chain expansion hotspots. Corporate dining is recovering strongly, with hybrid-work-driven office cafeteria contracts scaling 18% in 2025 across IT and BFSI clusters in Bengaluru, Hyderabad, Pune, and Gurugram. India’s tourism sector recorded over 9.5 million foreign tourist arrivals and 2.5 billion domestic tourist visits in 2024, accelerating QSR, cafe, and full-service restaurant offtake in transit, hospitality, and leisure venues. Leading food services operators such as Jubilant FoodWorks, Devyani International, Sapphire Foods, Westlife Foodworld, Tata Starbucks, and Haldiram’s have scaled Tier-2/3 outlet pipelines, with the non-metro segment alone representing an estimated USD 35 billion addressable opportunity within India by 2030. Government infrastructure programmes combined with corporate dining recovery are structurally expanding India food services market growth across all major service formats through 2032.

Key Market Challenges: India Food Services Market

High Real Estate Costs, Manpower Attrition and Raw Material Inflation Pressuring Restaurant Margins

The India food services market continues to face challenges around high real estate costs, manpower attrition, and rising raw material inflation, with rentals contributing 14% to 22% of total restaurant operating costs in metros and manpower costs accounting for another 18% to 24%. While organised chains have negotiated revenue-share leases in malls and high-street locations, average restaurant attrition rates remain at 50% to 70% annually across kitchen, service, and rider staff. Food and beverage raw material inflation, including edible oil, dairy, and protein, has averaged 7% to 9% between 2022 and 2025, compressing operating margins. EBITDA margins for organised QSR chains have moderated from 15% to 18% pre-pandemic to 10% to 13% in 2025. Smaller standalone outlets face sharper margin compression, while franchise-led expansion in non-metro markets remains underdeveloped. India’s continued dependence on imported ingredients and premium real estate limits scalability among mid-market operators across the India food services market.

Fragmented Regulatory Framework, FSSAI Compliance and GST Complexity Across States

The India food services market faces structural complexity from variations in FSSAI compliance norms, GST input credit rules, and state-level licensing across different states. While the FSSAI has standardised hygiene ratings and licensing through the Food Safety Compliance System (FoSCoS), GST treatment of restaurant services at 5% without input credit versus standalone bars and clubs at 18% with input credit creates pricing distortions. Average license and approval timelines range between 45 and 90 days, and excise approvals for pubs and bars have emerged as a key bottleneck in metro expansion. Differential treatment of liquor licensing, music licensing, and labour rules across states such as Maharashtra, Karnataka, Tamil Nadu, and Delhi NCR creates operational complexity for chained operators such as Jubilant FoodWorks, Devyani International, Sapphire Foods, Westlife Foodworld, and Restaurant Brands Asia operating pan-India. While the Ministry of Food Processing Industries has standardised processes for cloud kitchens, regulatory fragmentation remains a near-term challenge for the India food services market.

Intense Competition from Unorganised Street Food, Dark Kitchens and Price-Sensitive Consumers

The India food services market faces practical constraints around intense competition from the unorganised segment, which still accounts for nearly 60% to 65% of total foodservice revenue, dominated by street food, dhabas, and standalone eateries. Average ticket sizes in unorganised foodservice remain at INR 80 to 150 per meal, significantly below the INR 250 to 600 organised average. Tier-2 and Tier-3 consumers continue to anchor to value-led pricing, with discount-led ordering on Zomato and Swiggy contributing 35% to 45% of online food delivery volumes. Multi-tenant high-street locations face additional governance complexity in approvals, while ghost kitchens often face brand-recall challenges and limited repeat ordering. Hygiene-rated outlets, FSSAI A-grade certification, and central commissary-supplied chains are emerging as differentiators, but premium pricing and limited installer capability remain barriers to widespread organised adoption across the India food services market.

Key Market Trends: India Food Services Market

Rapid Adoption of Cloud Kitchens, Multi-Brand Operators and Ghost Kitchens in India

The India food services market is undergoing a clear technology shift toward cloud kitchens, multi-brand operators, and ghost kitchen formats, with these advanced models expected to capture over 28% of online food delivery volumes by 2027. Cloud kitchens deliver unit-level capex of INR 15 lakh to 30 lakh, compared to INR 40 lakh to 1 crore for traditional QSR dine-in outlets, while multi-brand operators add 25% to 40% additional revenue per kitchen through portfolio scaling. Leading domestic operators including Rebel Foods (Faasos, Behrouz, Oven Story), EatClub (Box8, MOJO Pizza), Curefoods (EatFit, Sharief Bhai, Nomad Pizza), Biryani By Kilo, and Bowl Company have scaled cloud kitchen production capacity through 2024 and 2025. Quick-commerce-led 10-minute food delivery is also gaining traction, particularly in metro cities such as Mumbai, Delhi NCR, and Bengaluru where Blinkit Bistro, Zepto Cafe, and Swiggy Instamart Food are scaling fast. This technology transition is reinforcing the India food services market forecast 2032 across both QSR and casual dining categories.

Growth of Online Food Delivery, Quick-Commerce Food and Subscription Models in the India Food Services Market

A clear shift toward online food delivery, quick-commerce food, and subscription models is reshaping the India food services market, particularly in the metro and Tier-1 segment. Under subscription and loyalty models such as Zomato Gold, Swiggy One, and Domino’s Cheesy Rewards, operators offer free delivery and discounts of 10% to 25% on every order. Leading online food delivery and aggregator platforms including Zomato (Eternal), Swiggy, EatSure, Domino’s online ordering, and McDonald’s McDelivery have built combined active monthly user bases exceeding 110 million. Quick-commerce platforms such as Blinkit, Zepto, Swiggy Instamart, and BigBasket Now are adding ready-to-eat and 10-minute food categories. Online food delivery aggregators and digital-only platforms such as Zomato, Swiggy, and ONDC are also reducing customer acquisition costs and accelerating organised foodservice adoption across both metro and Tier-2 segments of the India food services market.

Capacity Expansion by Domestic QSR Chains and Vertical Integration of Supply Chain

A wave of domestic capacity expansion and vertical integration is reshaping the India food services market supply landscape. Combined India-focused capital expenditure announcements in outlet expansion, central kitchens, and supply chain integration exceeded USD 2.5 billion across 2023 to 2025. Jubilant FoodWorks expanded Domino’s network to over 2,050 outlets, Devyani International scaled KFC and Pizza Hut to over 1,800 stores combined, Sapphire Foods crossed 950 outlets, Westlife Foodworld expanded McDonald’s West & South to over 400 outlets, and Restaurant Brands Asia grew Burger King India to over 480 outlets. Tata Starbucks crossed 460 stores, and homegrown café chains such as Blue Tokai, Third Wave Coffee, and Subko expanded specialty coffee footprints. Approved FSSAI norms, the Production Linked Incentive (PLI) scheme for food processing exceeding INR 10,900 crore, and reduced GST friction have structurally favoured organised supply. Combined with online food delivery driving demand and quick-commerce scaling rapidly, these developments are reinforcing the India food services market forecast 2032 across the entire value chain.

Segmental Insights: India Food Services Market

By Service Type: Quick Service Restaurants Segment Dominates the India Food Services Market

The Quick Service Restaurants (QSR) segment dominates the India food services market, accounting for an estimated 22% to 25% of organised foodservice revenue, driven by the rapid expansion of Domino’s, KFC, McDonald’s, Pizza Hut, Burger King, Subway, and homegrown chains like Wow! Momo and Haldiram’s. Chained QSR outlets are the dominant model within this segment, with multi-city standalone franchises capturing over 75% of QSR installations. The Full-Service Restaurants (casual and fine dining) segment contributes another 18% to 21% of demand, driven by Barbeque Nation, Speciality Restaurants, Lite Bite Foods, and Massive Restaurants. The Cafes & Bars segment accounts for 14% to 16%, led by Tata Starbucks, Cafe Coffee Day, Third Wave Coffee, Blue Tokai, and Pret A Manger. Cloud Kitchens contribute 8% to 10% and growing fastest. In 2025, leading operators including Jubilant FoodWorks, Devyani International, Sapphire Foods, Westlife Foodworld, and Restaurant Brands Asia scaled up QSR and casual dining deployment under online food delivery and corporate ESG mandates, reinforcing segment dominance in the India food services market.

By Cuisine Type: Indian Cuisine Leads While Asian and Continental Grow Fastest

Indian cuisine leads the India food services market product landscape, accounting for approximately 50% to 53% of organised foodservice consumption, driven by regional staples, biryani, North Indian, South Indian, and street-food formats. Asian cuisine including Chinese, Thai, Korean, and Japanese contributes another 17% to 19%, primarily through chained QSR and casual dining outlets in metros. Continental and European cuisines including Italian (pizza, pasta) and Mediterranean are the fastest growing categories within the India food services market, expanding at 12% to 15% annually, driven by superior unit economics of pizza chains, growing pasta and burger adoption, and rising premium dining in metros. North American (burgers, fries) and Middle Eastern (shawarma, kebab) cuisines together account for 11% to 13% of the market, with Middle Eastern expected to grow rapidly through 2032 in metro and Tier-1 markets. Leading domestic operators including Jubilant FoodWorks, Devyani International, Sapphire Foods, Restaurant Brands Asia, and Haldiram’s have aligned cuisine portfolios to this mix, driving multi-cuisine adoption across the India food services market.

Regional Insights: India Food Services Market

Regional analysis of the India food services market shows that West India and South India collectively account for approximately 56% to 60% of total foodservice revenue, driven by Maharashtra (which alone contributes over 19% of total India organised foodservice revenue through Mumbai and Pune), Karnataka (Bengaluru), Tamil Nadu (Chennai), Gujarat, and Telangana (Hyderabad), supported by progressive state licensing frameworks and high urban consumer density. North India contributes around 25% to 28% of demand, led by Delhi NCR, Punjab, Haryana, and Uttar Pradesh, supported by QSR, cafe, and casual dining adoption in metro and Tier-1 city clusters around Delhi, Gurugram, Noida, Jaipur, and Lucknow. East and Central India together account for 14% to 17% of demand, supported by West Bengal (Kolkata), Madhya Pradesh, Chhattisgarh, and Odisha, where chained QSR and cloud kitchen adoption is accelerating. In 2025, capacity additions and outlet operations by Jubilant FoodWorks across Tamil Nadu and Karnataka, Westlife Foodworld in Maharashtra and Gujarat, Tata Starbucks across pan-India metros, and Sapphire Foods across Andhra Pradesh and Telangana reinforced regional supply hubs, supporting closer execution of QSR and casual dining projects across the India food services market.

Recent Developments: India Food Services Market

- The India food services market witnessed strong momentum in expansion and policy progress during 2024 and 2025. India’s organised foodservice sector recorded value growth of over 14% year-on-year in 2025, with the online food delivery sub-segment growing at 22%, according to NRAI and industry data. Chained QSR outlet additions crossed 2,400 stores by mid-2025, with the QSR segment accounting for 38% of new outlet openings. Cumulative organised foodservice revenue in India is projected to reach USD 130 to 140 billion by FY28 from USD 95.7 billion in FY25, growing at an average 11% annually.

- Domestic foodservice operators have deepened India-focused capacity expansion. In 2025, Jubilant FoodWorks scaled Domino’s network beyond 2,050 outlets with new commissary additions, Devyani International expanded KFC and Pizza Hut footprint to over 1,800 stores combined, Sapphire Foods commissioned new South India commissaries, Westlife Foodworld expanded McDonald’s West & South to over 400 outlets, and Restaurant Brands Asia grew Burger King India to over 480 stores. Tata Starbucks crossed 460 stores and Haldiram’s expanded packaged QSR retail. These developments are strengthening domestic supply and supporting the India food services market forecast 2032.

- Cloud kitchen and online food delivery momentum has gained strong traction in the India food services market. In 2025, leading cloud kitchen operators including Rebel Foods (Faasos, Behrouz, Oven Story), EatClub (Box8, MOJO Pizza), Curefoods (EatFit, Sharief Bhai), Biryani By Kilo, and Bowl Company expanded contracted outlet portfolios. Zomato (Eternal) and Swiggy crossed combined 2.5 million daily orders. Strategic partnerships between domestic QSR chains and online food delivery platforms are positioning India as one of the most actively scaling foodservice markets globally, strengthening long-term competitive positioning in the India food services market forecast 2032.

Key Market Players: India Food Services Market

- Jubilant FoodWorks Limited (Domino’s, Popeyes, Dunkin’)

- Devyani International Limited (KFC, Pizza Hut, Costa Coffee)

- Sapphire Foods India Limited (KFC, Pizza Hut)

- Westlife Foodworld Limited (McDonald’s West & South)

- Restaurant Brands Asia Limited (Burger King India)

- Zomato Limited (Eternal Limited)

- Swiggy Limited (Bundl Technologies)

- Rebel Foods Pvt. Ltd. (Faasos, Behrouz, Oven Story)

- Barbeque Nation Hospitality Limited

- Speciality Restaurants Limited

- Tata Starbucks Pvt. Ltd.

- Haldiram’s Foods International Pvt. Ltd.

- Wow! Momo Foods Pvt. Ltd.

Report Scope

In this report, the India Food Services Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

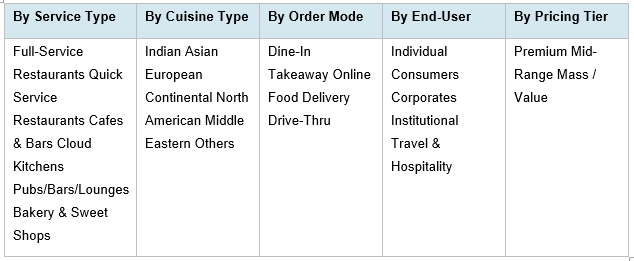

- By Service Type

- Full-Service Restaurants (Casual Dining, Fine Dining)

- Quick Service Restaurants (QSR)

- Cafes & Bars

- Cloud Kitchens

- Pubs/Bars/Lounges

- Frozen Yogurt/Ice Cream Parlours

- Bakery & Sweet Shops

- Others

- By Cuisine Type

- Indian

- Asian

- European

- Continental

- North American

- Middle Eastern

- Others

- By Ownership

- Standalone Outlets

- Chained Outlets

- By Order Mode

- Dine-In

- Takeaway

- Online Food Delivery

- Drive-Thru

- By Pricing Tier

- Premium

- Mid-Range

- Mass / Value

- By End-User

- Individual Consumers

- Corporates

- Institutional

- Travel & Hospitality

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Food Services Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic cloud kitchen operators, specialty cafe and bakery chains, online food delivery aggregators, or niche regional QSR brands.

The India Food Services Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

India Food Services Market, 2032

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Service Type

- By Cuisine Type

- By Order Mode

- By End-User

- By Pricing Tier

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Food Services Market

- India Food Services Market Insights

- Market Dynamics

- Growth Drivers

- Rising disposable income, urbanisation and young demographics driving organised foodservice adoption.

- Online food delivery, quick-commerce and cloud kitchen expansion strengthening off-premise consumption.

- Tier-2/3 city expansion, corporate dining and tourism recovery driving multi-format demand.

- Restraints

- High real estate costs, manpower attrition and raw material inflation pressuring restaurant margins.

- Fragmented regulatory framework, FSSAI compliance and GST complexity across states creating regulatory complexity.

- Intense competition from unorganised street food, dark kitchens and price-sensitive consumers limiting organised share.

- Opportunities

- Tier-2 and Tier-3 city expansion creating a massive long-term QSR and cafe opportunity.

- Cloud kitchens, food halls and multi-brand operators opening new value pools.

- Healthy eating, regional cuisine premiumisation and sustainable packaging supporting next-generation growth.

- Challenges

- Slow franchise-to-profitability conversion of new outlets limiting near-term scale.

- Limited skilled workforce for kitchen, service, and rider operations.

- Supply chain integration constraints, cold-chain limitations, and licensing caps in select states.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Growth Drivers

- Industry Value Chain & Entry Points

- Upstream Raw Materials (grains, dairy, protein, edible oil, packaging materials)

- Food Processors & Central Commissaries (frozen, ready-to-cook, semi-prepared bases)

- Equipment, Cold-Chain & Packaging Suppliers (ovens, fryers, refrigeration, takeaway packaging)

- Logistics & Last-Mile Delivery Partners (3PL, rider networks, dark stores)

- Quality Control, FSSAI & Food Safety Laboratories (FoSCoS, HACCP, ISO 22000)

- Distributors, B2B Aggregators & Online Marketplaces (HoReCa supply, ONDC, Reliance JioMart)

- Food Services Operators (QSR, casual dining, cafes, cloud kitchens, pubs)

- Brand Owners & Master Franchisees (Jubilant, Devyani, Sapphire, Westlife, RBA, Tata Starbucks)

- Online Food Delivery & Aggregator Platforms (Zomato, Swiggy, ONDC, EatSure)

- End-Users (individual consumers, corporates, institutional, travel & hospitality)

- India Food Services Market: Regulatory Framework

- India Food Services Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Outlets / Orders)

- Market Share & Forecast

- By Service Type

- Full-Service Restaurants

- Quick Service Restaurants

- Cafes & Bars

- Cloud Kitchens

- Pubs/Bars/Lounges

- Frozen Yogurt/Ice Cream Parlours

- Bakery & Sweet Shops

- Others

- By Cuisine Type

- Indian

- Asian

- European

- Continental

- North American

- Middle Eastern

- Others

- By Ownership

- Standalone Outlets

- Chained Outlets

- By Order Mode

- Dine-In

- Takeaway

- Online Food Delivery

- Drive-Thru

- By Pricing Tier

- Premium

- Mid-Range

- Mass / Value

- By End-User

- Individual Consumers

- Corporates

- Institutional

- Travel & Hospitality

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Food Services Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Jubilant FoodWorks Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Jubilant FoodWorks Limited

- By Service Type

- Market Size & Forecast, 2021-2032

- Market Dynamics

(Same Data Pointers Will Be Provided for The Below Companies)

- Devyani International Limited

- Sapphire Foods India Limited

- Westlife Foodworld Limited

- Restaurant Brands Asia Limited

- Zomato Limited (Eternal Limited)

- Swiggy Limited (Bundl Technologies)

- Rebel Foods Pvt. Ltd.

- Barbeque Nation Hospitality Limited

- Speciality Restaurants Limited

- Tata Starbucks Pvt. Ltd.

- Haldiram’s Foods International Pvt. Ltd.

- Wow! Momo Foods Pvt. Ltd.

- Other Prominent Players

Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

- Competitive Landscape

- India Food Services Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Jubilant FoodWorks Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- Devyani International Limited

- Sapphire Foods India Limited

- Westlife Foodworld Limited

- Restaurant Brands Asia Limited

- Zomato Limited (Eternal Limited)

- Swiggy Limited (Bundl Technologies)

- Rebel Foods Pvt. Ltd.

- Barbeque Nation Hospitality Limited

- Speciality Restaurants Limited

- Tata Starbucks Pvt. Ltd.

- Haldiram’s Foods International Pvt. Ltd.

- Wow! Momo Foods Pvt. Ltd.

- Other Prominent Players

*Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India food services market and what is its growth forecast?

Ans: The India food services market is valued at USD 95.7 billion in 2025 and is projected to reach USD 183.9 billion by 2032, growing at a CAGR of 9.8%, driven by rising eating-out and online food delivery demand.

2. Which segments are driving demand in the India food services market?

Ans: Quick Service Restaurants lead the India food services market with over 22% revenue share, while cloud kitchens and online food delivery are the fastest growing segments, supported by digital ordering and Tier-2/3 city expansion.

3. What are the key drivers of growth in the India food services market?

Ans: Key India food services market drivers include rising disposable income, urbanisation, online food delivery and cloud kitchen growth, Tier-2/3 city expansion, corporate dining recovery, and tourism momentum across urban India.

4. Which regions are driving growth in the India food services market?

Ans: West India and South India lead the India food services market with around 58% combined share, driven by Mumbai, Bengaluru, Chennai, Pune, and Hyderabad, followed by North India led by Delhi NCR.

5. What are the latest trends in the India food services market?

Ans: Latest India food services market trends include rapid cloud kitchen adoption, quick-commerce 10-minute food delivery, subscription loyalty programmes, healthy and regional cuisine premiumisation, and chained QSR Tier-2/3 expansion.

Frequently Asked Questions

1. How large is the India food services market and what is its growth forecast?

Ans: The India food services market is valued at USD 95.7 billion in 2025 and is projected to reach USD 183.9 billion by 2032, growing at a CAGR of 9.8%, driven by rising eating-out and online food delivery demand.

2. Which segments are driving demand in the India food services market?

Ans: Quick Service Restaurants lead the India food services market with over 22% revenue share, while cloud kitchens and online food delivery are the fastest growing segments, supported by digital ordering and Tier-2/3 city expansion.

3. What are the key drivers of growth in the India food services market?

Ans: Key India food services market drivers include rising disposable income, urbanisation, online food delivery and cloud kitchen growth, Tier-2/3 city expansion, corporate dining recovery, and tourism momentum across urban India.

4. Which regions are driving growth in the India food services market?

Ans: West India and South India lead the India food services market with around 58% combined share, driven by Mumbai, Bengaluru, Chennai, Pune, and Hyderabad, followed by North India led by Delhi NCR.

5. What are the latest trends in the India food services market?

Ans: Latest India food services market trends include rapid cloud kitchen adoption, quick-commerce 10-minute food delivery, subscription loyalty programmes, healthy and regional cuisine premiumisation, and chained QSR Tier-2/3 expansion.