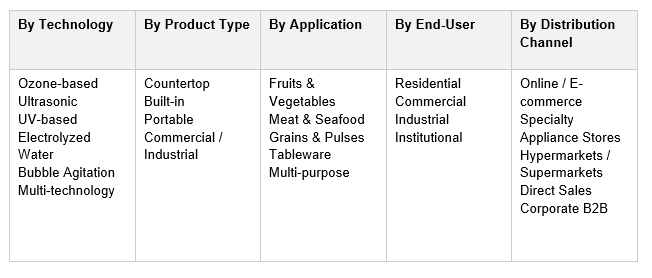

India Vegetable Washer System Market, By Technology (Ozone-based, Ultrasonic, UV-based, Electrolyzed Water, Bubble Agitation, Multi-technology); By Product Type (Countertop, Built-in, Portable, Commercial/Industrial); By Capacity (Below 5L, 5-10L, 10-20L, Above 20L); By Application (Fruits & Vegetables, Meat & Seafood, Grains & Pulses, Tableware, Multi-purpose); By End-User (Residential, Commercial, Industrial, Institutional); By Distribution Channel (Online/E-commerce, Specialty Appliance Stores, Hypermarkets, Direct Sales, B2B); By Price Range (Economy, Mid-Range, Premium, Luxury); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 130

- Report Format: pdf

- Report Price: $1800 USD

India Vegetable Washer System Market: Food Safety Awareness, Pesticide Concerns, and Smart Kitchen Adoption Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

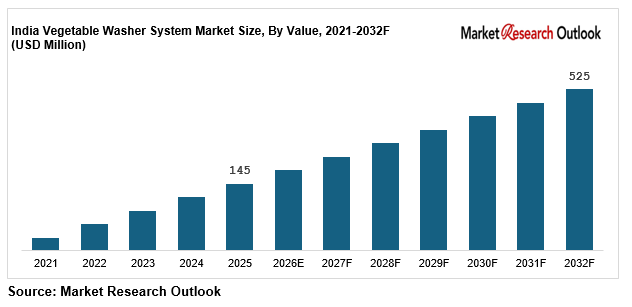

| Market Size (2025) | USD 145 Million |

| CAGR (2026-2032) | 20.2% |

| Leading Segment | Ozone-based Vegetable Washers (Residential) |

| Fastest Growing Segment | Ultrasonic + Smart IoT Vegetable Washers |

| Market Size (2032) | USD 525 Million |

Source: Market Research Outlook

Market Overview: India Vegetable Washer System Market

The India vegetable washer system market size is witnessing rapid expansion, driven by rising food safety awareness, accelerating concerns around pesticide residues, microbial contamination, and chemical pollutants in fresh produce, expanding modular kitchen integration across urban India, the rapid scaling of premium kitchen appliance adoption, growing FSSAI food safety regulations, and rising commercial demand from hotels, restaurants, cloud kitchens, and food processing units. Valued at USD 145 million in 2025 and projected to reach USD 525 million by 2032, growing at a CAGR of 20.2%, the India vegetable washer system market growth is being fuelled by strong residential adoption supported by health-conscious urban households, rising premium ozone and ultrasonic technology adoption, expanding commercial procurement under FSSAI compliance norms, and the rapid scaling of e-commerce and D2C distribution platforms. Ozone-based vegetable washers lead consumption, while ultrasonic and smart IoT-enabled multi-technology systems are emerging as the fastest growing category. Strengthening health and wellness awareness, post-pandemic hygiene preferences, and modular kitchen integration by Indian consumers, alongside aggressive product launches by leading brands, are reshaping the supply landscape. As domestic majors including Kent RO, Eureka Forbes, Havells, Hindware, and Faber scale residential and commercial portfolios, and global majors including LG, Samsung, and Bosch deepen India-specific innovation, the India vegetable washer system market is evolving into a technology-led, brand-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Vegetable Washer System Market

- The India vegetable washer system market size is projected to grow from USD 145 million in 2025 to USD 525 million by 2032, registering a strong CAGR of 20.2%, driven by accelerated food safety awareness, rising pesticide residue concerns, post-pandemic hygiene consciousness, and the structural shift toward technology-enabled vegetable cleaning across health-conscious Indian urban households.

- Ozone-based vegetable washers dominate the India vegetable washer system market, accounting for over 48% of total category value in 2025, driven by mid-range price points of INR 8,000 to INR 18,000, proven sanitization efficacy of 99.5%, and strong distribution across modern trade, specialty appliance stores, and online platforms across urban India.

- Ultrasonic and smart IoT-enabled vegetable washers are emerging as the fastest growing segment in the India vegetable washer system market, expected to grow at 26% to 32% annually as health-conscious consumers, premium kitchen adoption, and BLDC-motor technology drive the shift toward multi-technology and app-controlled vegetable cleaning systems.

- Rapid scaling of e-commerce platforms such as Amazon, Flipkart, Tata Cliq, Nykaa, and quick-commerce channels Blinkit, Zepto, and Swiggy Instamart, with online vegetable washer system sales crossing 42% to 48% of category value by mid-2025, is structurally expanding the India vegetable washer system market across residential and commercial Tier-II city consumption.

- Rising investments by domestic majors such as Kent RO, Eureka Forbes, Havells, Hindware, and Faber, alongside global majors LG, Samsung, and Bosch, in ozone generator manufacturing, ultrasonic transducer integration, and smart app-controlled launches are strengthening domestic supply and supporting the India vegetable washer system market forecast 2032.

Key Market Drivers: India Vegetable Washer System Market

Rising Food Safety Awareness, Pesticide Residue Concerns, and Health Consciousness Among Urban Indian Consumers

Growth in the India vegetable washer system market is being driven by rising food safety awareness, accelerating pesticide residue concerns, and structural health consciousness across Indian metros and Tier-II cities. According to FSSAI surveillance data published in 2024 and 2025, over 18% of fresh fruit and vegetable samples tested in India showed pesticide residues above the maximum allowable limit, raising consumer alarm about chemical contamination. Per-capita ambient food safety appliance spending in India remains well below global benchmarks of USD 8 to USD 16, while urban awareness of vegetable washer technology has crossed 32% in 2025, up from 14% in 2020, supported by rising health content on Instagram, YouTube, and short-form video platforms. India’s per-capita disposable income has grown at over 9% annually between 2020 and 2025, supporting discretionary spend on premium kitchen appliances. Food safety adoption among the 28 to 50-year-old age cohort, supported by post-pandemic hygiene consciousness, work-from-home cooking culture, and rising awareness of microbial contamination, is structurally pulling demand into the India vegetable washer system market. Mid-range ozone and ultrasonic vegetable washers between INR 8,000 and INR 18,000, available across modern trade, specialty appliance retail, and online platforms, continue to drive high-volume penetration across the country.

Growing Middle-Class Disposable Income, Premium Kitchen Appliance Adoption, and Modular Kitchen Integration

The India vegetable washer system market is benefiting from a strong structural push from rising middle-class disposable income, premium kitchen appliance adoption, and modular kitchen integration trends. India’s modular kitchen penetration has crossed 22% among urban households in 2025, up from 12% in 2020, driving integrated installation of built-in vegetable washers alongside dishwashers, RO water purifiers, and chimneys. Premium kitchen appliance category sales grew by over 28% in 2024 and 2025, supported by aspirational urban consumption and rising apartment supply across the top 8 metro cities. Domestic vegetable washer capacity has scaled rapidly, with leading brands including Kent RO, AO Smith, Eureka Forbes, Havells, Hindware, Faber, Elica, and Kaff scaling ozone-based and ultrasonic vegetable washer portfolios. The Make-in-India PLI scheme, BIS certification under emerging vegetable washer norms, and Basic Customs Duty on cheap imports have further strengthened domestic supply, supporting price competitiveness across the India vegetable washer system market. Average residential vegetable washer prices have compressed from INR 18,000 to INR 28,000 in 2020 to INR 9,500 to INR 18,500 in 2025, accelerating premium mid-market adoption.

E-commerce Growth, D2C Brands, FSSAI Food Safety Norms, and Rising Commercial Demand from HoReCa

Rapid growth in online and D2C distribution is a major catalyst for the India vegetable washer system market, with the e-commerce channel projected to grow at 25% to 30% annually through 2032. Online vegetable washer system sales now account for an estimated 42% to 48% of total category value, led by platforms such as Amazon, Flipkart, Tata Cliq, Croma Online, and Reliance Digital. Quick-commerce platforms including Blinkit, Zepto, Swiggy Instamart, and BigBasket Now have emerged as new growth engines for portable countertop vegetable washers in urban markets. The Food Safety and Standards Authority of India (FSSAI) has tightened food safety norms for HoReCa, cloud kitchens, and food processing units, mandating enhanced vegetable washing and sanitization protocols. The commercial HoReCa segment, supported by over 28 lakh restaurants, cafes, and food service establishments across India, alongside more than 6,200 cloud kitchen brands operating from over 22,000 cloud kitchen units, is driving structural demand for commercial-grade vegetable washer systems. Leading D2C and digital-first brands such as Kent, Cleanyo, and Borosil have scaled aggressive influencer, content, and performance marketing pipelines, supporting structural expansion of the India vegetable washer system market across all major end-user categories through 2032.

Key Market Challenges: India Vegetable Washer System Market

Low Consumer Awareness of Vegetable Washer Technology and Limited Category Education

The India vegetable washer system market continues to face challenges around low consumer awareness of vegetable washer technology, limited category education, and a structural understanding gap on ozone, ultrasonic, and UV-based cleaning efficacy. Urban household awareness of vegetable washer system technology stood at only 32% in 2025, while Tier-II and Tier-III city awareness remains below 14%, reflecting bottlenecks in consumer education, demonstration retailing, and influencer marketing penetration. Traditional Indian washing methods using salt water, vinegar, baking soda, and tap water rinsing continue to dominate over 78% of household vegetable cleaning practices, supported by generational cooking culture and perceived efficacy. Brand-led category education campaigns, demo events at modern trade outlets, and influencer-driven content on the science of pesticide residue removal are gradually expanding awareness, but consumer education gaps remain a structural constraint. Strengthening brand investment in television advertising, online video education, and in-store demonstrations is gradually easing these pressures across the India vegetable washer system market.

High Upfront Cost Limiting Mass-Market Adoption Among Middle-Income Households

The India vegetable washer system market faces structural complexity from high upfront costs and price sensitivity among middle-income households. Entry-level vegetable washer prices of INR 8,000 to INR 12,000, mid-range models priced at INR 15,000 to INR 25,000, and premium models above INR 30,000 place the category beyond the reach of many middle-income Indian households. While EMI schemes from Bajaj Finserv, HDFC, and Pine Labs have improved affordability, vegetable washers still represent a discretionary spend versus traditional washing methods that cost effectively zero. Banks and NBFCs continue to be cautious in extending unsecured kitchen appliance loans for newer product categories, while EMI-linked financing for vegetable washers remains under-penetrated in Tier-II and Tier-III cities. India’s continued price sensitivity in the under-INR 10,000 kitchen appliance segment limits adoption among middle-income and rural households across the India vegetable washer system market. Falling component costs, domestic manufacturing scale-up, and price competition from new D2C brands are gradually compressing premium pricing toward more accessible mid-market price points.

Strong Traditional Washing Habits and Effective Alternative Practices

The India vegetable washer system market faces practical constraints around deeply entrenched traditional washing practices and the perceived effectiveness of low-cost alternative methods. Indian households have used salt water, vinegar solution, turmeric water, and baking soda rinsing for generations as low-cost vegetable cleaning practices, with traditional methods perceived as adequate for 70% to 78% of urban consumers. Studies by FSSAI and consumer research organizations have shown that while traditional methods remove surface dirt and water-soluble residues effectively, they have limited efficacy against fat-soluble pesticide residues, microbial contamination, and chemical pollutants that modern ozone, ultrasonic, and UV technologies can remove with 95% to 99.5% efficacy. Limited awareness of these efficacy differences, combined with the absence of standardized BIS or FSSAI certification frameworks for vegetable washer performance claims, has slowed category trust-building. After-sales service gaps, including ozone generator replacement, ultrasonic transducer maintenance, and UV lamp servicing, remain a key consumer pain point across Tier-II and rural markets. While leading brands such as Kent, Eureka Forbes, Havells, and Faber have built service networks of 300 to 700 cities, smaller and regional players continue to face execution gaps across the India vegetable washer system market.

Key Market Trends: India Vegetable Washer System Market

Rapid Adoption of Ozone, Ultrasonic, and UV-Based Multi-Technology Washer Systems

The India vegetable washer system market is undergoing a clear technology shift toward ozone, ultrasonic, and UV-based multi-technology systems, with these advanced category configurations expected to capture over 65% of new vegetable washer installations by 2027. Ozone-based vegetable washers, currently leading category share, deliver pesticide removal efficacy of 95% to 99% by oxidizing chemical residues through reactive oxygen molecules. Ultrasonic washers, growing fastest at 26% to 32% annually, use high-frequency sound waves of 28 to 40 kHz to dislodge contaminants from produce surfaces, with adoption rising among premium urban households. UV-C light disinfection, integrated as a secondary sanitization layer, kills 99.9% of microbial contamination including E. coli, Salmonella, and Listeria. Multi-technology systems combining ozone, ultrasonic, and UV layers in a single appliance are emerging as the premium category benchmark, with leading domestic manufacturers including Kent, Eureka Forbes, Havells, Hindware, and global majors LG, Samsung, and Bosch scaling multi-technology production capacity through 2024 and 2025. Smart vegetable washers with BLDC motors, programmable cycles, and mobile app integration are gaining strong consumer traction. This technology transition is reinforcing the India vegetable washer system market forecast 2032 across both residential and commercial categories.

Growth of Smart IoT-Enabled, App-Controlled, and BLDC-Motor Vegetable Washers

A clear shift toward smart IoT-enabled, app-controlled, and BLDC-motor vegetable washer systems is reshaping the India vegetable washer system market, particularly across the premium and metro consumer segments. Smart vegetable washer launches grew by over 38% in 2024 and 2025, with leading brands scaling Wi-Fi-connected washers, IoT-enabled cleaning cycle monitoring, smartphone app integration, and voice control via Amazon Alexa and Google Assistant. BLDC motor adoption in premium vegetable washers, offering 40% to 55% power savings over traditional induction motors, has crossed 35% of new launches by mid-2025. Programmable cleaning cycles tailored for leafy greens, root vegetables, fruits, meat, seafood, and tableware are emerging as a category differentiator, with leading models offering 8 to 12 preset programs. Anti-microbial inner basket coating, child safety locks, and energy-efficient operation are increasingly central to premium positioning. This smart and BLDC technology momentum is supporting category value growth and is reinforcing structural growth across the India vegetable washer system market.

Capacity Expansion and Rising Commercial HoReCa, Cloud Kitchen, and Food Processing Adoption

A wave of domestic capacity expansion and rising commercial adoption is reshaping the India vegetable washer system market supply landscape. Combined India-focused capital expenditure announcements in kitchen appliance and food safety equipment manufacturing exceeded INR 1,200 crore across 2023 to 2025 under the Make-in-India and PLI schemes. Kent RO expanded ozone generator manufacturing, AO Smith scaled UV-based washer production, Eureka Forbes added new ultrasonic models, Havells expanded modular kitchen appliance lines, and Hindware grew its premium appliance portfolio. Commercial demand from HoReCa establishments, supported by over 28 lakh restaurants and cafes across India, more than 6,200 cloud kitchen brands operating from over 22,000 cloud kitchen units, and growing institutional catering for hospitals, schools, and corporate cafeterias, is scaling structurally. Food processing companies including ITC, Nestle, Britannia, Mother Dairy, Amul, and quick-commerce dark stores from Zepto, Blinkit, and BigBasket are increasingly adopting industrial-grade vegetable washer systems for FSSAI compliance. Combined with rising health consciousness across urban India, these developments are reinforcing the India vegetable washer system market forecast 2032 across the entire value chain.

Segmental Insights: India Vegetable Washer System Market

By Technology: Ozone-Based Segment Dominates the India Vegetable Washer System Market

The ozone-based segment dominates the India vegetable washer system market, accounting for an estimated 46% to 50% of total category value, driven by proven pesticide and contaminant removal efficacy of 95% to 99%, established consumer trust, and improving cost economics. Ultrasonic vegetable washers contribute another 22% to 25% of demand, driven by premium urban household adoption and superior cleaning of leafy greens and delicate produce. UV-based washers, often integrated as secondary disinfection layers, account for 12% to 15% of category value. Electrolyzed water and bubble agitation technologies together capture 8% to 10%, with adoption rising in mid-market price points. Multi-technology washers combining ozone, ultrasonic, and UV layers in single appliances contribute 5% to 8% but are the fastest growing category, expanding at 28% to 35% annually. In 2025, leading brands including Kent RO, AO Smith, Eureka Forbes, LG, Samsung, Bosch, Havells, Hindware, Faber, and Elica scaled up multi-technology product launches and commercial-grade vegetable washer deployment under FSSAI compliance and modular kitchen integration trends, reinforcing segment dynamics in the India vegetable washer system market.

By Product Type and End-User: Countertop Leads While Built-in and Commercial Grow Fastest

Countertop vegetable washers lead the India vegetable washer system market product landscape, accounting for approximately 58% to 62% of total installations, driven by their compact form factor, easy plug-and-play installation in existing Indian kitchens, and improving cost economics with mid-range price points of INR 8,000 to INR 18,000. Portable and travel-friendly vegetable washers contribute another 14% to 17%, popular among urban professionals and small households. Built-in modular kitchen-integrated vegetable washers are the fastest growing product category within the India vegetable washer system market, expanding at 24% to 28% annually, driven by villa, luxury apartment, and modular kitchen adoption. Commercial and industrial vegetable washers account for 14% to 18% of category value, growing at 22% to 26% annually, supported by HoReCa, cloud kitchen, and food processing demand. By end-user, residential consumers dominate with 65% to 68% share, while commercial HoReCa is the fastest growing end-user cohort at 25% to 30% annually. Leading domestic and global manufacturers including Kent, Eureka Forbes, LG, Samsung, Bosch, Havells, Hindware, and Faber have aligned product portfolios to this product-type and end-user mix, driving multi-segment vegetable washer adoption across the India vegetable washer system market.

Regional Insights: India Vegetable Washer System Market

Regional analysis of the India vegetable washer system market shows that West India and South India collectively account for approximately 56% to 60% of total category value, driven by Maharashtra (Mumbai, Pune metro premium kitchen belt), Gujarat (Ahmedabad, Surat), Karnataka (Bengaluru tech corridor), Tamil Nadu (Chennai, Coimbatore), and Telangana (Hyderabad), supported by strong urban food safety awareness, premium modular kitchen adoption, and proximity to appliance manufacturing clusters. North India contributes around 25% to 28% of demand, led by Delhi NCR (Gurugram, Noida), Punjab, Haryana, and Uttar Pradesh (Lucknow, Noida), supported by upper middle-income household adoption and growing concern over pesticide residues in Northern Indian agricultural produce. East and Central India together account for 12% to 16% of demand, supported by West Bengal (Kolkata), Odisha (Bhubaneswar), Madhya Pradesh (Indore, Bhopal), where vegetable washer system adoption is gradually accelerating among Tier-II cities. In 2025, capacity additions and brand expansion by Kent RO across pan-India, AO Smith in South India, Eureka Forbes across West and North India, Havells in North India, Hindware across West India, and Faber and Elica across modular kitchen integration partnerships reinforced regional supply hubs, supporting closer execution of residential and commercial vegetable washer deployment across the India vegetable washer system market.

Recent Developments: India Vegetable Washer System Market

- The India vegetable washer system market witnessed strong momentum in new product launches, FSSAI compliance adoption, and channel expansion during 2024 and 2025. The category grew by an estimated 22% to 26% in value terms in 2025, supported by aggressive product launches, post-pandemic hygiene awareness, festive renovation cycles, and quick-commerce expansion. Online and D2C sales crossed 42% to 48% of total category value, with ultrasonic and smart vegetable washer sales growing by over 35% year-on-year, according to leading industry trackers. Cumulative branded category penetration is projected to expand from 32% in 2025 to 55% to 60% by FY32, growing at an average 20% to 24% annually.

- Domestic vegetable washer manufacturers have deepened India-focused capacity expansion and brand portfolio building. In 2025, Kent RO scaled ozone generator manufacturing and launched new multi-technology washer variants, AO Smith expanded UV-based washer production, Eureka Forbes added new ultrasonic Aquaguard models, Havells expanded built-in modular kitchen vegetable washer lines, and Hindware grew its premium appliance portfolio. Faber, Elica, and Kaff Appliances added new countertop and built-in vegetable washer models with BLDC motors and IoT integration. These developments are strengthening domestic supply and supporting the India vegetable washer system market forecast 2032.

- Premium and D2C vegetable washer momentum has gained strong traction in the India vegetable washer system market. In 2025, leading premium and digital-first players including Kent, Borosil, Cleanyo, Inalsa, and Glen scaled premium ozone, ultrasonic, multi-technology, and smart app-controlled vegetable washer portfolios. Strategic partnerships between domestic appliance manufacturers, e-commerce platforms such as Amazon, Flipkart, Tata Cliq, and Reliance Digital, and quick-commerce platforms Blinkit, Zepto, and Swiggy Instamart are positioning India as one of the most actively scaling vegetable washer markets globally, strengthening long-term competitive positioning in the India vegetable washer system market forecast 2032.

Key Market Players: India Vegetable Washer System Market

- Kent RO Systems Limited

- AO Smith India Water Products Pvt. Ltd.

- Eureka Forbes Limited (Aquaguard)

- LG Electronics India Pvt. Ltd.

- Samsung India Electronics Pvt. Ltd.

- Bosch Limited (BSH Home Appliances)

- Havells India Limited

- Hindware Home Innovation Limited

- Faber India Appliances

- Elica India Pvt. Ltd.

- Kaff Appliances India Pvt. Ltd.

- Glen Appliances Pvt. Ltd.

- Borosil Limited

- Inalsa Appliances Pvt. Ltd.

- Cleanyo India Pvt. Ltd.

Report Scope

In this report, the India Vegetable Washer System Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Technology

- Ozone-based

- Ultrasonic

- UV-based

- Electrolyzed Water

- Bubble Agitation

- Multi-technology

- By Product Type

- Countertop

- Built-in

- Portable

- Commercial / Industrial

- By Capacity

- Below 5L

- 5L to 10L

- 10L to 20L

- Above 20L

- By Application

- Fruits & Vegetables

- Meat & Seafood

- Grains & Pulses

- Tableware

- Multi-purpose

- By End-User

- Residential

- Commercial (HoReCa, Cloud Kitchens)

- Industrial (Food Processing)

- Institutional (Hospitals, Schools, Catering)

- By Distribution Channel

- Online / E-commerce

- Specialty Appliance Stores

- Hypermarkets / Supermarkets

- Direct Sales

- Corporate B2B

- By Price Range

- Economy

- Mid-Range

- Premium

- Luxury

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Vegetable Washer System Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic D2C vegetable washer brands, specialty ozone and ultrasonic appliance manufacturers, premium built-in modular kitchen integrators, or niche regional commercial food safety equipment players.

The India Vegetable Washer System Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Technology

- By Product Type

- By Capacity

- By Application

- By End-User

- By Distribution Channel

- By Price Range

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Vegetable Washer System Market

- India Vegetable Washer System Market Insights

- Market Dynamics

- Growth Drivers

- Rising food safety awareness, pesticide residue concerns, and health consciousness among urban Indian consumers.

- Growing middle-class disposable income, premium kitchen appliance adoption, and modular kitchen integration.

- E-commerce growth, D2C brands, FSSAI food safety norms, and rising commercial demand from HoReCa segment.

- Restraints

- Low consumer awareness of vegetable washer technology and limited category education across India.

- High upfront cost of INR 8,000 to 35,000 limiting mass-market adoption among middle-income households.

- Strong traditional salt, vinegar, and baking soda washing habits and entrenched alternative practices.

- Opportunities

- Tier-II and Tier-III city expansion creating a massive untapped vegetable washer system demand base.

- Smart IoT-enabled, app-controlled, and BLDC-motor vegetable washers opening new premium value pools.

- Commercial HoReCa, cloud kitchen, and food processing industry adoption supporting next-generation growth.

- Challenges

- Limited skilled installer, service technician, and after-sales support network across pan-India coverage.

- Raw material price volatility for ozone generators, ultrasonic transducers, UV lamps, and electronic controllers.

- Lack of standardized BIS, FSSAI, or BEE certification frameworks for vegetable washer system performance.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (stainless steel, ozone generators, ultrasonic transducers, UV lamps, electronics)

- Component & Motor Manufacturers (BLDC motors, water pumps, ozone modules, IoT controllers)

- Smart Electronics & Sensor Suppliers (IoT modules, app integration, water-quality sensors)

- Contract Manufacturers & Original Design Manufacturers

- Quality Control, R&D & Testing Laboratories (BIS, FSSAI, NABL accredited labs)

- Distributors, Wholesalers, Dealers & Online Aggregators

- Vegetable Washer Brand Owners (Kent, AO Smith, Eureka Forbes, LG, Samsung, Bosch, Havells)

- Retailers, Specialty Appliance Stores, Hypermarkets, D2C Platforms & Quick-commerce

- Installation, After-Sales Service & Authorized Service Centres

- End-Users (residential households, restaurants, hotels, cloud kitchens, food processing units)

- India Vegetable Washer System Market: Regulatory Framework

- India Vegetable Washer System Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Thousand Units)

- Market Share & Forecast

- By Technology

- Ozone-based

- Ultrasonic

- UV-based

- Electrolyzed Water

- Bubble Agitation

- Multi-technology

- By Product Type

- Countertop

- Built-in

- Portable

- Commercial / Industrial

- By Capacity

- Below 5L

- 5L to 10L

- 10L to 20L

- Above 20L

- By Application

- Fruits & Vegetables

- Meat & Seafood

- Grains & Pulses

- Tableware

- Multi-purpose

- By End-User

- Residential

- Commercial (HoReCa, Cloud Kitchens)

- Industrial (Food Processing)

- Institutional (Hospitals, Schools, Catering)

- By Distribution Channel

- Online / E-commerce

- Specialty Appliance Stores

- Hypermarkets / Supermarkets

- Direct Sales

- Corporate B2B

- By Price Range

- Economy

- Mid-Range

- Premium

- Luxury

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Vegetable Washer System Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Kent RO Systems Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- AO Smith India Water Products Pvt. Ltd.

- Eureka Forbes Limited (Aquaguard)

- LG Electronics India Pvt. Ltd.

- Samsung India Electronics Pvt. Ltd.

- Bosch Limited (BSH Home Appliances)

- Havells India Limited

- Hindware Home Innovation Limited

- Faber India Appliances

- Elica India Pvt. Ltd.

- Kaff Appliances India Pvt. Ltd.

- Glen Appliances Pvt. Ltd.

- Borosil Limited

- Inalsa Appliances Pvt. Ltd.

- Cleanyo India Pvt. Ltd.

- Other Prominent Players

- Kent RO Systems Limited

- By Technology

- Market Size & Forecast, 2021-2032

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India vegetable washer system market and what is its growth forecast?

Ans: The India vegetable washer system market is valued at USD 145 million in 2025 and is projected to reach USD 525 million by 2032, growing at a CAGR of 20.2%, supported by rising food safety awareness, modular kitchen adoption, and FSSAI norms.

2. Which segments are driving demand in the India vegetable washer system market?

Ans: Ozone-based washers dominate the India vegetable washer system market with over 48% value share, while ultrasonic and smart IoT-enabled multi-technology washers are the fastest growing segments, supported by premium urban household adoption.

3. What are the key drivers of growth in the India vegetable washer system market?

Ans: Key drivers include rising food safety awareness, pesticide residue concerns, growing middle-class income, modular kitchen integration, FSSAI compliance norms, e-commerce expansion, and rising HoReCa demand across India's vegetable washer system market.

4. Which regions are driving growth in the India vegetable washer system market?

Ans: Maharashtra, Gujarat, Karnataka, Tamil Nadu, Telangana, and Delhi NCR lead the India vegetable washer system market, supported by premium kitchen adoption, urban food safety awareness, and strong HoReCa, cloud kitchen, and modular kitchen penetration.

5. What are the latest trends in the India vegetable washer system market?

Ans: Latest trends include multi-technology ozone-ultrasonic-UV washers, smart IoT-enabled app-controlled models, BLDC motor adoption, built-in modular kitchen integration, quick-commerce expansion, and rising HoReCa adoption across India's vegetable washer system market.

Frequently Asked Questions

1. How large is the India vegetable washer system market and what is its growth forecast?

Ans: The India vegetable washer system market is valued at USD 145 million in 2025 and is projected to reach USD 525 million by 2032, growing at a CAGR of 20.2%, supported by rising food safety awareness, modular kitchen adoption, and FSSAI norms.

2. Which segments are driving demand in the India vegetable washer system market?

Ans: Ozone-based washers dominate the India vegetable washer system market with over 48% value share, while ultrasonic and smart IoT-enabled multi-technology washers are the fastest growing segments, supported by premium urban household adoption.

3. What are the key drivers of growth in the India vegetable washer system market?

Ans: Key drivers include rising food safety awareness, pesticide residue concerns, growing middle-class income, modular kitchen integration, FSSAI compliance norms, e-commerce expansion, and rising HoReCa demand across India's vegetable washer system market.

4. Which regions are driving growth in the India vegetable washer system market?

Ans: Maharashtra, Gujarat, Karnataka, Tamil Nadu, Telangana, and Delhi NCR lead the India vegetable washer system market, supported by premium kitchen adoption, urban food safety awareness, and strong HoReCa, cloud kitchen, and modular kitchen penetration.

5. What are the latest trends in the India vegetable washer system market?

Ans: Latest trends include multi-technology ozone-ultrasonic-UV washers, smart IoT-enabled app-controlled models, BLDC motor adoption, built-in modular kitchen integration, quick-commerce expansion, and rising HoReCa adoption across India's vegetable washer system market.