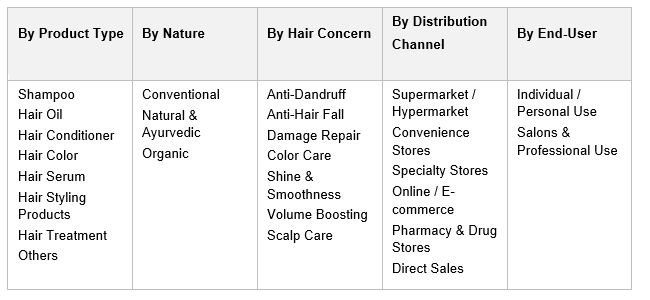

India Hair Care Market, By Product Type (Shampoo, Hair Oil, Hair Conditioner, Hair Color, Hair Serum, Hair Styling Products, Hair Treatment, Others); By Nature (Conventional, Natural & Ayurvedic, Organic); By Hair Concern (Anti-Dandruff, Anti-Hair Fall, Damage Repair, Color Care, Shine & Smoothness, Volume Boosting, Scalp Care); By Gender (Men, Women, Unisex); By Price Range (Premium, Mass, Economy); By End-User (Individual / Personal Use, Salons & Professional Use); By Distribution Channel (Supermarket / Hypermarket, Convenience Stores, Specialty Stores, Online / E-commerce, Pharmacy & Drug Stores, Direct Sales); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 130

- Report Format: pdf

- Report Price: $1800 USD

India Hair Care Market: Premiumisation, Ayurvedic Innovation, and D2C Distribution Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

| Market Size (2025) | USD 4.5 Billion |

| CAGR (2026-2032) | 8.2% |

| Leading Segment | Hair Oil (Conventional) |

| Fastest Growing Segment | Hair Serums & Premium Shampoos |

| Market Size (2032) | USD 7.8 Billion |

Source: Market Research Outlook

Market Overview: India Hair Care Market

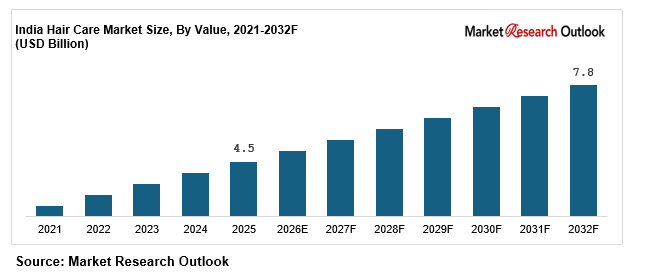

The India hair care market size is witnessing rapid expansion, driven by rising disposable income, rapid urbanisation, premiumisation, growing grooming awareness, the rapid consumer shift toward Ayurvedic and natural hair care, rapid expansion of e-commerce, D2C hair care brands, and quick commerce platforms, and growing investments by domestic and global personal care majors in India-specific hair care manufacturing capacity, R&D, and digital-first hair care brand platforms. Valued at USD 4.5 Billion in 2025 and projected to reach USD 7.8 Billion by 2032, growing at a CAGR of 8.2%, the India hair care market growth is being fuelled by strong demand for hair oil across mass and Ayurvedic categories, rising consumption of shampoo, hair conditioner, hair serum, hair color, and hair styling products, and growing institutional adoption across salons and professional hair care chains. Hair oil leads consumption, while hair serums and premium shampoos are emerging as the fastest growing categories in the India hair care market. Tightening ASCI, CDSCO, and AYUSH regulatory frameworks, growing ESG and clean beauty commitments by Indian consumers, and the structural premiumisation wave are reshaping the supply landscape. As domestic majors including Hindustan Unilever, Marico, Dabur, Emami, Bajaj Consumer Care, ITC, Godrej Consumer, and Patanjali Ayurved expand integrated hair care portfolios, and D2C and digital-first hair care brands including Honasa Consumer (Mamaearth, BBlunt, Aqualogica), WOW Skin Science, The Man Company, Bombay Shaving Company, Pilgrim, Minimalist, and Plum Goodness scale online pipelines, the India hair care market is evolving into a consumer-led, ingredient-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Hair Care Market

- The India hair care market size is projected to grow from USD 4.5 Billion in 2025 to USD 7.8 Billion by 2032, registering a strong CAGR of 8.2%, driven by accelerating premiumisation, rapid expansion of Ayurvedic and natural hair care, and the structural shift toward online and D2C hair care distribution.

- Hair oil dominates the India hair care market, accounting for over 35% to 38% of total hair care revenue in 2025, driven by Marico Parachute, Dabur Vatika, Bajaj Almond Drops, Emami 7 Oils in One, Indulekha Bringha, and Patanjali Kesh Kanti, supported by deep Indian cultural affinity for hair oiling rituals.

- Hair serums and premium shampoos are emerging as the fastest growing hair care segments, expected to grow at 14% to 16% annually as urban Indian consumers shift toward dermatologist-tested, ingredient-led, and salon-quality hair care across Tier I and Tier II cities.

- Online and quick commerce channels are scaling rapidly in the India hair care market, contributing over 18% to 22% of total hair care sales in 2025, driven by Amazon, Flipkart, Nykaa, Tira, Purplle, Blinkit, Zepto, and Instamart, structurally expanding the digital hair care opportunity.

- Rising investments by domestic hair care majors such as Hindustan Unilever, Marico, Dabur, Emami, Bajaj Consumer Care, L’Oréal India, ITC, Godrej Consumer Products, and Honasa Consumer in hair care R&D, contract manufacturing, and India-specific Ayurvedic hair care platforms are strengthening local supply and supporting the India hair care market forecast 2032.

Key Market Drivers: India Hair Care Market

Rising Disposable Income, Urbanisation, and Premiumisation Driving Hair Care Consumption in India

Growth in the India hair care market is being driven by rising disposable income, rapid urbanisation, and a structural premiumisation wave reshaping hair care consumption across Indian households. India’s per-capita disposable income has grown at a CAGR of 9.5% between 2021 and 2025, while urban households now account for over 62% of total hair care spend in the this category. Premium and mass-premium hair care products are recording faster growth than economy hair care, with shampoos priced above INR 250 per 200 ml expanding at 12% to 14% annually. Demand for specialised hair care formats such as hair serums, scalp care treatments, and dermatologist-tested hair care is accelerating across Tier I and Tier II Indian cities. The India hair care market is also benefiting from rising grooming awareness among men, with men’s hair care registering double-digit growth, supported by hair styling products, anti-hair fall hair oil, and anti-dandruff shampoo categories. These trends are creating strong, multi-year structural pull-through demand across the Indian hair care category through 2032.

Growing Consumer Shift Toward Ayurvedic, Natural, and Organic Hair Care Products

The India hair care market is undergoing a clear consumer shift toward Ayurvedic, natural, and organic hair care products, with these categories collectively accounting for over 38% of total hair care sales in 2025 and growing at 11% to 13% annually. Heritage Ayurvedic hair care brands including Dabur Vatika, Patanjali Kesh Kanti, Emami Kesh King, Indulekha, and Himalaya have scaled hair oil, herbal shampoo, and hair fall treatment portfolios anchored in Indian botanical ingredients such as amla, bhringraj, brahmi, neem, hibiscus, and curry leaves. Mass-premium and digital-first hair care brands such as Mamaearth, WOW Skin Science, The Man Company, Plum Goodness, and BBlunt have built sizeable franchises around onion hair oil, argan oil shampoo, sulphate-free hair conditioner, and ingredient-led hair serum. Indian consumers are increasingly scrutinising hair care labels for parabens, sulphates, silicones, and synthetic fragrances, with over 47% of Indian shampoo buyers in 2025 actively seeking sulphate-free or natural-claim hair care, reinforcing the Indian hair care category’s structural pivot to naturals.

Rapid Expansion of E-Commerce, D2C, and Quick Commerce Reshaping Hair Care Distribution in India

Rapid scaling of e-commerce, direct-to-consumer (D2C) hair care brands, and quick commerce platforms is a major catalyst for the India hair care market, with online channels expected to account for over 22% of hair care sales by 2027, up from less than 8% in 2021. Marketplaces including Amazon, Flipkart, Nykaa, Tira, Purplle, and Myntra Beauty are driving discovery and trial of premium hair care, while quick commerce platforms such as Blinkit, Zepto, Instamart and BB Now are accelerating hair care category turnover with 10 to 30 minute deliveries across 25 Indian cities. D2C-first hair care brands including Mamaearth, WOW Skin Science, The Man Company, Bombay Shaving Company, Pilgrim, Minimalist (now part of Hindustan Unilever), and Arata are leveraging influencer-led marketing, performance media, and subscription-based hair care models to acquire customers. Established hair care majors including Hindustan Unilever, Marico, Dabur, Emami, L’Oréal India, and Procter & Gamble have ramped up direct online stores, exclusive online launches, and influencer-led campaigns, reinforcing the hair care market in India’s omnichannel transformation through 2032.

Key Market Challenges: India Hair Care Market

High Price Sensitivity and Intense Competition Compressing Margins in Mass-Market Hair Care

The India hair care market remains highly price-sensitive, particularly across mass and economy hair care segments where sachet-led hair care continues to account for over 30% of unit volume. Intense competition between Hindustan Unilever, Procter & Gamble, Marico, Dabur, Emami, ITC, Godrej Consumer, Patanjali, and a fast-growing pool of D2C hair care brands has compressed gross margins across mass shampoo, mass hair oil, and mass hair conditioner. Aggressive trade promotions, price-pack architecture innovation, and frequent discounting in modern trade and quick commerce have made it difficult for new hair care entrants to scale profitably. Local and regional hair care brands across Indian states continue to compete aggressively on price, with private-label hair care also gaining share in modern trade and online channels. Sustained inflation in palm oil, surfactant, packaging, and freight inputs has further squeezed hair care manufacturer margins, making cost engineering, premiumisation, and channel mix optimisation critical strategic levers in the Indian hair care industry.

Regulatory Complexity Around Natural and Ayurvedic Claims, Labelling, and Ingredient Safety

The India hair care market faces structural complexity from evolving regulations around cosmetic claims, natural and Ayurvedic positioning, ingredient safety, and labelling. The Central Drugs Standard Control Organisation (CDSCO), the Bureau of Indian Standards (BIS), and the Ministry of AYUSH oversee distinct but overlapping regulatory frameworks for hair care products, with Ayurvedic hair care covered under the Drugs and Cosmetics Act read alongside Ayush licensing rules. Hair care brands making natural, organic, sulphate-free, paraben-free, or dermatologist-tested claims must align with BIS labelling standards and the Legal Metrology rules. Misleading hair care advertising remains an area of focus for the Advertising Standards Council of India (ASCI), with multiple hair fall, dandruff, and hair growth claims contested in 2024 and 2025. New hair care ingredient approvals, restricted-ingredient lists, and import compliance under the Cosmetics Rules 2020 add to the regulatory load on hair care companies operating in the Indian hair care industry.

Rising Raw Material, Packaging, and Freight Costs Squeezing Hair Care Manufacturer Margins

The India hair care market is exposed to volatility in key raw materials including coconut oil, mustard oil, almond oil, palm-derived surfactants, silicones, and herbal extracts, alongside packaging inputs such as HDPE, PET, aluminium tubes, and corrugated boxes. Coconut oil prices in India rose by over 38% between 2023 and 2025, materially affecting Marico’s Parachute, Dabur’s Anmol, and Bajaj Consumer Care’s almond hair oil portfolios. Crude-linked surfactants, fragrance, and silicone inputs used in hair care shampoo, hair conditioner, and hair serum manufacturing have remained inflationary, with cost-push inflation passing through to consumer hair care MRP across both mass and premium hair care categories. Sea freight, road freight, and last-mile logistics costs across the the market have risen by 12% to 18% post 2022, while quick commerce service fees and platform commissions in online hair care add a structural margin overhang. Cost engineering, backward integration, local sourcing of botanicals, and selective premiumisation are emerging as critical responses in the India hair care market.

Key Market Trends: India Hair Care Market

Surge in Personalisation, Customised Hair Care, and Ingredient-Led Formulations in India

The hair care market in India is undergoing a clear shift toward personalisation, customised hair care, and ingredient-led formulations, with personalised hair care expected to account for over 12% of premium hair care by 2030. AI-driven hair diagnostic platforms, online hair quizzes, and salon-led hair analysis are powering customised hair care regimens across hair oil, shampoo, hair conditioner, and hair serum categories. Indian D2C hair care brands such as Bare Anatomy, Traya, Vedix, Skin Story, Wishful, and Re’equil have built propositions around customised hair care kits, anti-hair fall protocols, and dermatologist-prescribed hair care. Ingredient-led hair care storytelling around rosemary oil, ceramides, peptides, biotin, caffeine, redensyl, and onion bulb extract has gone mainstream, with online hair care content driving consumer education. Heritage Indian hair care brands have responded by relaunching Ayurvedic hair care portfolios with modern ingredient call-outs, reinforcing the India hair care market’s premiumisation and ingredient-first orientation through 2032.

Rapid Growth of D2C, Quick Commerce, and Influencer-Led Marketing in the India Hair Care Market

A clear shift toward D2C-first hair care, quick commerce, and influencer-led marketing is reshaping the this category, particularly in the premium and mass-premium tiers. Honasa Consumer (Mamaearth), The Good Glamm Group, WOW Skin Science, Pilgrim, The Man Company, Bombay Shaving Company, Plum Goodness, and Minimalist have scaled annual hair care revenues into the hundreds of crores by combining D2C websites, marketplaces, and quick commerce. Quick commerce platforms now contribute 6% to 9% of online hair care sales in India, with hair oil, dry shampoo, anti-dandruff shampoo, and hair styling products as fast-rotating categories. Hair care influencer marketing in India has scaled rapidly, with hair care content creators driving discovery on Instagram, YouTube, and short-video platforms across hair fall, hair growth, scalp care, hair color, and curly hair conversations. Established hair care majors have responded with influencer ecosystems, digital-first launches, and creator-led storytelling to defend share in the India hair care market.

Sustainability, Clean Beauty, and Refillable Hair Care Packaging Gaining Momentum

A wave of sustainability, clean beauty, and refillable packaging innovation is reshaping the hair care market in India. Plastic waste, ingredient transparency, and cruelty-free positioning are increasingly important to Indian hair care consumers, with over 41% of urban Indian hair care buyers in 2025 willing to pay a premium for clean and sustainable hair care. Hair care brands are reformulating products with biodegradable surfactants, plant-based silicones, and locally sourced botanicals across hair oil, shampoo, hair conditioner, and hair serum lines. Refillable hair care pouches, shampoo bars, and recyclable mono-material PET bottles are scaling across both mass and premium hair care portfolios. Major personal care companies including Hindustan Unilever, L’Oréal India, Dabur, Marico, and Honasa Consumer have committed to recycled-content plastic and net-zero targets that directly impact their India hair care market portfolios. These developments are reinforcing the domestic hair care category forecast 2032 across the entire value chain.

Segmental Insights: India Hair Care Market

By Product Type: Hair Oil Dominates While Hair Serums and Premium Shampoos Grow Fastest

Hair oil dominates the India hair care market by product type, accounting for an estimated 35% to 38% of total hair care revenue in 2025, supported by coconut, almond, and Ayurvedic hair oil consumption across both urban and rural Indian households. Shampoo is the second-largest hair care product category, with around 30% revenue share, driven by mass shampoo and anti-dandruff shampoo in sachet and small SKU formats. Hair conditioner contributes 10% to 12% of the Indian hair care category, with rising adoption in Tier I and Tier II Indian cities. Hair serum and hair styling products together account for 9% to 11% of the India hair care market and are the fastest growing hair care product categories, expanding at 14% to 16% annually, driven by premiumisation, frizz control, and heat-protection demand. Hair color contributes 8% to 10% of the Indian hair care category, dominated by Godrej Expert, L’Oréal Garnier, Hindustan Unilever’s Indulekha Bringha and Henna brands, and salon hair color professional formats.

By Nature: Natural and Ayurvedic Hair Care Leads, Organic Hair Care Grows Fastest

Natural and Ayurvedic hair care leads the India hair care market by nature, accounting for over 38% to 42% of total hair care sales in 2025, anchored in deep cultural affinity for Indian botanical hair care ingredients such as amla, bhringraj, neem, brahmi, hibiscus, curry leaves, fenugreek, and onion. Conventional hair care still represents the largest share by value at 50% to 55%, dominated by global hair care majors including Hindustan Unilever, Procter & Gamble, L’Oréal India, and Henkel. Certified organic hair care is the fastest growing category, expanding at over 16% annually, although it remains a small share of the Indian hair care segment overall. Indian heritage hair care brands such as Dabur Vatika, Patanjali Kesh Kanti, Emami Kesh King, Indulekha, Himalaya, and Forest Essentials have aligned product portfolios to natural and Ayurvedic positioning, reinforcing the India hair care market’s structural pivot.

By Distribution Channel: Modern Trade and Online Hair Care Outpace Traditional Retail

Traditional general trade still accounts for the largest channel in the Indian hair care industry, contributing 55% to 60% of total hair care sales, supported by over 12 million general trade outlets across Indian cities, towns, and villages. Modern trade and specialty beauty stores contribute another 14% to 17%, anchored by Reliance Retail, DMart, More Retail, Nykaa, Tira, Sephora India, Health & Glow, and Shoppers Stop Beauty. Online and quick commerce together account for 18% to 22% of the India hair care market in 2025 and are the fastest growing hair care channels, expanding at over 22% annually. Pharmacy and chemist channels contribute 4% to 6%, while salon and professional hair care channels account for 3% to 5% of the hair care market in India, driven by professional hair color, hair treatment, hair smoothening, and keratin services.

Regional Insights: India Hair Care Market

Regional analysis of the India hair care market shows that North India and West India collectively account for approximately 52% to 56% of total hair care consumption, driven by Delhi NCR, Uttar Pradesh, Punjab, Haryana, Rajasthan, Maharashtra, and Gujarat, supported by larger Tier I and Tier II urban clusters, higher disposable income, and stronger modern trade and online hair care penetration. South India contributes around 26% to 29% of demand, led by Karnataka, Tamil Nadu, Telangana, Andhra Pradesh, and Kerala, supported by deep hair oil consumption (Kerala alone is one of India’s largest per-capita hair oil markets) and growing premium hair care adoption in Bengaluru, Chennai, and Hyderabad. East India and Central India together account for 18% to 22% of demand, supported by West Bengal, Odisha, Bihar, Madhya Pradesh, Chhattisgarh, and Jharkhand, where mass hair care, sachet hair care, and Ayurvedic hair care continue to anchor the India hair care market. In 2025, Hindustan Unilever, Marico, Dabur, Emami, Bajaj Consumer Care, Honasa Consumer, L’Oréal India, and Patanjali Ayurved expanded regional distribution, manufacturing, and influencer-led marketing across Indian states, reinforcing regional supply hubs and supporting closer execution of mass and premium hair care across the India hair care market.

Recent Developments: India Hair Care Market

- The India hair care market witnessed strong momentum across product launches, premiumisation, and digital-first hair care expansion during 2024 and 2025. Hindustan Unilever scaled Indulekha Bringha hair oil and Indulekha shampoo to over INR 1,000 crore in annual hair care revenue, expanded the Dove and TRESemmé premium hair care portfolios, and acquired Minimalist to deepen its dermatologist-led India hair care market presence. Procter & Gamble strengthened Pantene Pro-V Miracles and Head & Shoulders, while L’Oréal India scaled L’Oréal Paris Total Repair 5, Garnier Ultra Blends, Schwarzkopf, and Kérastase hair care.

- Indian hair care majors have deepened India-focused product innovation and capacity expansion. Marico expanded Parachute Advansed hair oil, Nihar Naturals, Hair & Care, Livon hair serum, and acquired Beardo and Just Herbs to deepen premium hair care and men’s grooming. Dabur scaled Vatika, Amla, and Dabur Almond hair oil while building digital-first hair care extensions; Emami expanded Kesh King, 7 Oils in One, and Navratna into newer hair care formats; Bajaj Consumer Care relaunched Bajaj Almond Drops; and ITC scaled Fiama and Vivel hair care alongside premium hair care launches.

- Digital-first and D2C hair care momentum has gained strong traction in the India hair care market. Honasa Consumer’s Mamaearth, BBlunt, and Aqualogica scaled hair care SKUs across hair oil, shampoo, and hair serum; The Good Glamm Group expanded St. Botanica and MyGlamm hair care; WOW Skin Science, The Man Company, Bombay Shaving Company, Pilgrim, Minimalist, Plum Goodness, and Forest Essentials scaled digital-first hair care portfolios. These developments are reinforcing the India hair care market forecast 2032 by structurally widening category penetration and channel mix.

Key Market Players: India Hair Care Market

- Hindustan Unilever Limited

- Marico Limited

- Dabur India Limited

- Procter & Gamble Hygiene and Health Care Limited

- Emami Limited

- Bajaj Consumer Care Limited

- L’Oréal India Pvt. Ltd.

- Patanjali Ayurved Limited

- ITC Limited

- Godrej Consumer Products Limited

- Honasa Consumer Limited (Mamaearth)

- Himalaya Wellness Company

- Forest Essentials

Report Scope

In this report, the India Hair Care Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Shampoo

- Hair Oil

- Hair Conditioner

- Hair Color

- Hair Serum

- Hair Styling Products

- Hair Treatment

- Others

- By Nature

- Conventional

- Natural & Ayurvedic

- Organic

- By Hair Concern

- Anti-Dandruff

- Anti-Hair Fall

- Damage Repair

- Color Care

- Shine & Smoothness

- Volume Boosting

- Scalp Care

- By Gender

- Men

- Women

- Unisex

- By Price Range

- Premium

- Mass

- Economy

- By End-User

- Individual / Personal Use

- Salons & Professional Use

- By Distribution Channel

- Supermarket / Hypermarket

- Convenience Stores

- Specialty Stores

- Online / E-commerce

- Pharmacy & Drug Stores

- Direct Sales

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Hair Care Market, including business overview, hair care product portfolio (hair oil, shampoo, hair conditioner, hair serum, hair color, hair styling), strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional hair care players (up to five companies), including emerging Indian D2C hair care brands, specialty Ayurvedic hair care producers, salon-channel hair care suppliers, or niche state-level hair care manufacturers.

The India Hair Care Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Nature

- By Hair Concern

- By Gender

- By Price Range

- By End-User

- By Distribution Channel

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Hair Care Market

- India Hair Care Market Insights

- Market Dynamics

- Growth Drivers

- Rising disposable income, urbanisation, premiumisation, and grooming awareness driving hair care consumption.

- Growing consumer shift toward Ayurvedic, natural, and organic hair care products.

- Rapid expansion of e-commerce, D2C brands, and quick commerce platforms reshaping hair care distribution.

- Restraints

- High price sensitivity and intense competition compressing margins in mass-market hair care.

- Regulatory complexity around natural and Ayurvedic claims, labelling, and ingredient safety.

- Rising raw material, packaging, and freight costs squeezing hair care manufacturer margins.

- Opportunities

- Premiumisation and growing demand for specialised hair care including hair serums, scalp care, and dermatologist-tested formulations.

- Tier II and Tier III city expansion through digital channels and modern retail in India hair care market.

- Sustainability, clean beauty, and refillable packaging opening new value pools in the India hair care market.

- Challenges

- Counterfeiting, grey-market imports, and brand dilution affecting premium hair care players in semi-urban and rural India.

- Slow penetration of premium hair care formats beyond Tier I metros limiting near-term scale.

- Climate variability, water-hardness, and humidity differences across India affecting hair care product performance.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (coconut oil, mustard oil, almond oil, surfactants, silicones, herbal extracts, fragrance, packaging)

- Active Ingredient & Formulation Suppliers (Ayurvedic botanicals, sulphate-free surfactants, peptides, biotin, ceramides)

- Hair Care Contract Manufacturers (mass shampoo, hair oil, hair conditioner, hair serum, hair color)

- Quality Control, R&D & Testing Laboratories (CDSCO, BIS, AYUSH, ASCI compliance)

- Distributors, Wholesalers & Modern Trade Partners (Reliance Retail, DMart, More, Nykaa, Tira)

- E-commerce, D2C & Quick Commerce Platforms (Amazon, Flipkart, Nykaa, Blinkit, Zepto, Instamart)

- Hair Care Brand Owners & FMCG Majors (Hindustan Unilever, Marico, Dabur, P&G, L’Oréal India)

- Salon Channel & Professional Hair Care Operators (Lakmé Salon, Naturals, Jawed Habib, Bblunt)

- Retail Outlets, Pharmacies & General Trade Stores (kirana, chemist, beauty store networks)

- End-Users (Individual / Personal Use, Salons & Professional Use)

- India Hair Care Market: Regulatory Framework

- India Hair Care Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Thousand Tonnes)

- Market Share & Forecast

- By Product Type

- Shampoo

- Hair Oil

- Hair Conditioner

- Hair Color

- Hair Serum

- Hair Styling Products

- Hair Treatment

- Others

- By Nature

- Conventional

- Natural & Ayurvedic

- Organic

- By Hair Concern

- Anti-Dandruff

- Anti-Hair Fall

- Damage Repair

- Color Care

- Shine & Smoothness

- Volume Boosting

- Scalp Care

- By Gender

- Men

- Women

- Unisex

- By Price Range

- Premium

- Mass

- Economy

- By End-User

- Individual / Personal Use

- Salons & Professional Use

- By Distribution Channel

- Supermarket / Hypermarket

- Convenience Stores

- Specialty Stores

- Online / E-commerce

- Pharmacy & Drug Stores

- Direct Sales

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Hair Care Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Hindustan Unilever Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- Marico Limited

- Dabur India Limited

- Procter & Gamble Hygiene and Health Care Limited

- Emami Limited

- Bajaj Consumer Care Limited

- L’Oréal India Pvt. Ltd.

- Patanjali Ayurved Limited

- ITC Limited

- Godrej Consumer Products Limited

- Honasa Consumer Limited (Mamaearth)

- Himalaya Wellness Company

- Forest Essentials

- Other Prominent Players

- Hindustan Unilever Limited

- Market Size & Forecast, 2021-2032

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India hair care market and what is its growth forecast?

Ans: India hair care market is projected to grow from USD 4.5 Billion in 2025 to USD 7.8 Billion by 2032, at a CAGR of 8.2%, driven by premiumisation, Ayurvedic innovation, D2C scaling, and Tier II city expansion.

2. Which segments are driving demand in the India hair care market?

Ans: Hair oil leads with 35% to 38% revenue share, anchored by mass and Ayurvedic categories. Hair serums and premium shampoos grow fastest at 14% to 16% annually, driven by dermatologist-tested and ingredient-led formulations across Indian metros.

3. What are the key drivers of growth in the India hair care market?

Ans: Key drivers include rising disposable income, urbanisation, premiumisation, growing grooming awareness, accelerating consumer shift toward Ayurvedic and natural hair care, and rapid expansion of e-commerce, D2C brands, and quick commerce platforms reshaping hair care distribution in India.

4. Which regions are driving growth in the India hair care market?

Ans: North and West India together account for 52% to 56% of demand, led by Delhi NCR, Maharashtra, Gujarat, Uttar Pradesh, and Rajasthan. South India contributes 26% to 29%, anchored by Kerala, Karnataka, Tamil Nadu, Telangana, and Andhra Pradesh.

5. What are the latest trends in the India hair care market?

Ans: Latest trends include personalisation and ingredient-led formulations, rapid D2C and quick commerce growth, influencer-led marketing, sustainability and refillable packaging, and rising adoption of sulphate-free, dermatologist-tested, and Ayurvedic-hybrid hair care across India.

Frequently Asked Questions

1. How large is the India hair care market and what is its growth forecast?

Ans: India hair care market is projected to grow from USD 4.5 Billion in 2025 to USD 7.8 Billion by 2032, at a CAGR of 8.2%, driven by premiumisation, Ayurvedic innovation, D2C scaling, and Tier II city expansion.

2. Which segments are driving demand in the India hair care market?

Ans: Hair oil leads with 35% to 38% revenue share, anchored by mass and Ayurvedic categories. Hair serums and premium shampoos grow fastest at 14% to 16% annually, driven by dermatologist-tested and ingredient-led formulations across Indian metros.

3. What are the key drivers of growth in the India hair care market?

Ans: Key drivers include rising disposable income, urbanisation, premiumisation, growing grooming awareness, accelerating consumer shift toward Ayurvedic and natural hair care, and rapid expansion of e-commerce, D2C brands, and quick commerce platforms reshaping hair care distribution in India.

4. Which regions are driving growth in the India hair care market?

Ans: North and West India together account for 52% to 56% of demand, led by Delhi NCR, Maharashtra, Gujarat, Uttar Pradesh, and Rajasthan. South India contributes 26% to 29%, anchored by Kerala, Karnataka, Tamil Nadu, Telangana, and Andhra Pradesh.

5. What are the latest trends in the India hair care market?

Ans: Latest trends include personalisation and ingredient-led formulations, rapid D2C and quick commerce growth, influencer-led marketing, sustainability and refillable packaging, and rising adoption of sulphate-free, dermatologist-tested, and Ayurvedic-hybrid hair care across India.