India Emergency Lighting Market, By Product Type (Emergency Exit Signs, Self-Contained Emergency Luminaires, Industrial Emergency Lighting, Recessed Emergency Luminaires, Spotlights & Floodlights, Others); By Power Source (Self-Contained, Central Battery System, Hybrid Systems); By Lamp Type (LED, Fluorescent, Incandescent, Halogen, Others); By Operation (Maintained, Non-Maintained, Combined / Sustained); By Battery Type (Lead-Acid, Nickel-Cadmium, Lithium-Ion, Nickel-Metal Hydride); By Application (Egress / Escape Route, Open Area / Anti-Panic, High-Risk Task Area, Standby Lighting); By End-User (Commercial, Industrial, Residential, Healthcare, Hospitality, Educational, Transportation & Infrastructure, Government & Public); By Distribution Channel (Direct Sales, Distributors / Dealers, Online / E-Commerce, Specialty Lighting Stores); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 130

- Report Format: pdf

- Report Price: $1800 USD

India Emergency Lighting Market: NBC 2016 Compliance and Smart Infrastructure Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

| Market Size (2025) | USD 312 Million |

| CAGR (2026-2032) | 11.7% |

| Leading Segment | Self-Contained LED Emergency Luminaires (Commercial) |

| Fastest Growing Segment | Smart / IoT-Connected Emergency Lighting Systems |

| Market Size (2032) | USD 678 Million |

Source: Market Research Outlook

Market Overview: India Emergency Lighting Market

The India emergency lighting market size is witnessing rapid expansion, driven by stringent National Building Code (NBC 2016) compliance enforcement, rapid commercial real estate, healthcare, and hospitality infrastructure expansion, the Smart Cities Mission rollout across 100 cities, expanding metro rail and airport modernisation projects, and the rapid transition from conventional fluorescent and incandescent backup luminaires to LED-based, smart, addressable emergency lighting systems. Valued at USD 312 Million in 2025 and projected to reach USD 678 Million by 2032, growing at a CAGR of 11.7%, the India emergency lighting market growth is being fuelled by strong commercial and institutional demand, rising healthcare and hospitality construction, and growing adoption across factories, warehouses, MSMEs, government buildings, schools, and high-rise residential societies. The commercial segment leads consumption, while smart and IoT-connected emergency lighting systems are emerging as the fastest growing category. Tightening fire safety enforcement, BIS / IS 15498 compliance, NBC 2016 mandates, and rising occupant-safety expectations are reshaping the supply landscape. As domestic majors including Halonix Technologies, Bajaj Electricals, Wipro Lighting, Havells India, Crompton Greaves, Surya Roshni, and Polycab expand integrated LED emergency luminaire capacity, and global majors including Signify (Philips), Schneider Electric, Legrand, Honeywell, and Eaton scale India-specific premium portfolios, the India emergency lighting market is evolving into a compliance-led, technology-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Emergency Lighting Market

- The India emergency lighting market size is projected to grow from USD 312 Million in 2025 to USD 678 Million by 2032, registering a strong CAGR of 11.7%, driven by accelerated NBC 2016 compliance enforcement, rapid commercial real estate expansion, rising healthcare and hospitality construction, and the structural shift toward LED-based, smart, addressable emergency lighting systems.

- Commercial buildings dominate the India emergency lighting market, accounting for over 38% of total demand in 2025, driven by rapid Grade A office space addition of approximately 70 million sq. ft. across 2024 to 2025, mandatory fire NOC compliance, and rising adoption of self-contained LED emergency luminaires across IT parks, retail malls, and corporate offices.

- Smart and IoT-connected emergency lighting systems are emerging as the fastest growing segment in the India emergency lighting market, expected to grow at 18 to 22% annually through 2032, driven by Building Management System (BMS) integration, automated self-testing and compliance reporting, and addressable luminaire adoption in premium commercial, healthcare, and transportation infrastructure.

- Rapid scaling of the Smart Cities Mission with allocations exceeding INR 1.66 lakh crore across 100 cities, an operational metro rail network crossing 950 km in 21 cities by 2025, and airport modernisation across 25+ greenfield and brownfield projects is structurally expanding the India emergency lighting market across transportation, public infrastructure, and government building categories.

- Rising investments by domestic lighting majors such as Halonix Technologies, Bajaj Electricals, Wipro Lighting, Havells India, and Crompton Greaves in LED-based emergency luminaire manufacturing, lithium-ion battery integration, and IoT-enabled smart systems are strengthening local supply and supporting the India emergency lighting market forecast 2032.

Key Market Drivers: India Emergency Lighting Market

National Building Code (NBC 2016) Compliance and Stringent Fire Safety Regulations Driving Mandatory Emergency Lighting Installations

Growth in the India emergency lighting market is being driven by stringent enforcement of the National Building Code of India (NBC 2016), which mandates emergency lighting and exit signage across high-rise residential buildings, commercial complexes, healthcare facilities, hotels, educational institutions, transportation terminals, and industrial sites. NBC 2016 specifies a minimum 90-minute autonomy for emergency lighting in egress paths, anti-panic lighting in open areas above 60 sq. m., and high-risk task area lighting in industrial premises, in line with IS 15498 and IEC 60598-2-22 standards. The Bureau of Indian Standards (BIS) has tightened certification requirements for emergency luminaires, while state fire departments across Maharashtra, Karnataka, Tamil Nadu, Gujarat, Delhi NCR, and Telangana have made fire NOC issuance contingent on compliant emergency lighting installation. Penetration of compliant emergency lighting in India remains below 35% of addressable buildings, indicating significant long-term headroom for growth across the India emergency lighting market.

Rapid Commercial Real Estate, Healthcare, and Hospitality Infrastructure Expansion Boosting Emergency Lighting Demand

The India emergency lighting market is benefiting from rapid expansion across commercial real estate, healthcare, and hospitality infrastructure. India added approximately 70 million sq. ft. of Grade A office space across 2024 to 2025 according to leading property consultants, while organised retail mall stock crossed 110 million sq. ft. across the top eight cities. The healthcare segment added over 9,000 new hospital beds in 2024 alone, with major chains including Apollo, Manipal, Max Healthcare, and Fortis aggressively expanding multi-specialty hospital networks. Hospitality saw the addition of more than 15,000 branded hotel keys during 2024 to 2025, with international chains including Marriott, IHG, Hilton, Hyatt, and domestic groups such as Indian Hotels Company, ITC Hotels, and Lemon Tree expanding pipelines. Each new hospital, hotel, mall, and office tower mandatorily requires NBC 2016-compliant emergency lighting and exit signage systems, creating sustained downstream demand across the India emergency lighting market.

Transition to LED-Based Energy-Efficient Emergency Lighting and Smart Connected Systems Across End-User Segments

Rapid adoption of LED-based emergency lighting is a major catalyst for the India emergency lighting market, with the LED segment projected to account for over 78% of new installations by 2027. LED emergency luminaires deliver 60 to 70% energy savings compared to fluorescent and incandescent backup lighting, lifespans exceeding 50,000 hours, and superior compatibility with lithium-ion batteries delivering 3-hour autonomy in compact form factors. Smart, addressable, and IoT-enabled emergency lighting systems with self-test functions, automated compliance reporting, and Building Management System (BMS) integration are gaining strong traction in premium commercial, healthcare, and transportation infrastructure. Domestic majors including Halonix Technologies, Bajaj Electricals, Wipro Lighting, Havells India, and Crompton Greaves, alongside global players such as Signify (Philips), Schneider Electric, Legrand, Honeywell, and Eaton, are scaling integrated LED emergency luminaire portfolios with smart-connected and addressable features. Combined with rising occupant-safety expectations and corporate ESG commitments, these developments are structurally expanding India emergency lighting market growth across all major end-user categories through 2032.

Key Market Challenges: India Emergency Lighting Market

Price Sensitivity and Competition from Unorganised, Low-Cost Local Manufacturers

The India emergency lighting market continues to face challenges around price sensitivity and intense competition from unorganised, low-cost local manufacturers, particularly in residential and small commercial segments. The unorganised segment accounts for an estimated 30 to 35% of total emergency lighting unit sales in India, with low-cost imports and grey-market products often retailing 35 to 50% below organised brand prices. While these products lack BIS / IS 15498 certification and frequently fail to meet NBC 2016 autonomy requirements, end-user awareness of compliance and quality differentiation remains limited outside Tier 1 cities. Banks and project consultants continue to award tenders on lowest-quote basis, while EMI-linked financing for premium smart emergency lighting systems remains underdeveloped. India’s continued price-led procurement culture in the residential and SME segments limits adoption of higher-specification compliant systems across the India emergency lighting market.

Inconsistent Enforcement of Fire Safety Codes Across Tier 2 and Tier 3 Cities

The India emergency lighting market faces structural complexity from inconsistent enforcement of NBC 2016 and state fire safety codes across Tier 2 and Tier 3 cities. While metropolitan markets such as Mumbai, Delhi NCR, Bengaluru, Chennai, Hyderabad, and Pune maintain rigorous fire NOC and periodic compliance audits, enforcement remains limited across smaller cities, leading to widespread non-compliant installations and the use of sub-standard emergency luminaires. Average fire NOC renewal cycles vary between 1 to 5 years across states, and audit-led upgrade demand is concentrated in compliance-driven categories such as healthcare, hospitality, and IT-enabled services. Differential interpretation of NBC 2016 specifications, IS 15498 requirements, and state-specific fire safety rules creates operational complexity for emergency lighting OEMs and EPC players such as Halonix, Bajaj, Wipro, Havells, and Crompton operating pan-India. While the National Disaster Management Authority and Bureau of Indian Standards have standardised core specifications, regulatory fragmentation remains a near-term challenge for the India emergency lighting market.

Limited Awareness Among Residential Consumers and SME Segments

The India emergency lighting market faces practical constraints around limited awareness among residential consumers and Small and Medium Enterprise (SME) segments. While high-rise apartment complexes above 15 metres are technically required to install compliant emergency lighting under NBC 2016, awareness of egress lighting, anti-panic luminaires, and self-contained LED systems remains low among Resident Welfare Associations and individual home-owners. SME factories and warehouses often install only basic exit signage rather than comprehensive emergency lighting covering high-risk task areas and open-area anti-panic zones. Insurance-led specifications are gradually tightening, with leading general insurers requiring compliant emergency lighting for fire and property cover, and PSU banks linking project finance to NBC 2016 audit reports. However, demand pull-through from the residential and SME segments remains uneven, and awareness-led market expansion remains a structural challenge across the India emergency lighting market.

Key Market Trends: India Emergency Lighting Market

Rapid Adoption of LED-Based Self-Contained Emergency Luminaires with Lithium-Ion Batteries

The India emergency lighting market is undergoing a clear technology shift toward LED-based self-contained emergency luminaires integrated with lithium-ion battery packs, with these advanced systems expected to capture over 65% of new emergency lighting installations by 2027. LED self-contained luminaires deliver 60 to 70% energy savings, compact form factors, and 3-hour autonomy in line with NBC 2016 mandates, while lithium-ion batteries offer 3 to 5 times longer cycle life compared to traditional Ni-Cd and lead-acid alternatives. Leading domestic manufacturers including Halonix Technologies, Bajaj Electricals, Wipro Lighting, Havells India, Crompton Greaves, Surya Roshni, and Polycab have scaled LED emergency luminaire portfolios through 2024 and 2025. Smart self-test functions, occupancy-linked dimming, and addressable connectivity are also gaining traction, particularly in metro cities such as Mumbai, Delhi NCR, and Bengaluru where premium commercial buildings demand BMS-integrated systems. This technology transition is reinforcing the India emergency lighting market forecast 2032 across both commercial and institutional categories.

Growth of Smart, Addressable, and IoT-Connected Emergency Lighting Systems

A clear shift toward smart, addressable, and IoT-connected emergency lighting business models is reshaping the India emergency lighting market, particularly in the commercial, healthcare, and transportation segments. Under smart addressable systems, individual luminaires perform automated self-tests, report status to a central panel, and integrate with Building Management Systems (BMS) and fire detection networks, eliminating manual periodic inspections that previously required 200 to 400 person-hours per facility annually. Leading global players including Signify (Philips), Schneider Electric, Legrand, Honeywell, and Eaton, alongside domestic majors such as Halonix and Bajaj, have launched IoT-enabled addressable emergency lighting platforms in India. Online aggregators and digital procurement platforms such as Amazon Business, IndiaMART, Moglix, and Industrybuying are also reducing customer acquisition costs and accelerating emergency lighting adoption across both commercial and SME segments of the India emergency lighting market.

Integration of Emergency Lighting with Building Management Systems (BMS) and Fire Safety Networks

A wave of BMS integration and digital convergence is reshaping the India emergency lighting market supply landscape. Combined India-focused capital expenditure announcements in LED emergency luminaire manufacturing, lithium-ion battery integration, and smart-connected lighting systems exceeded USD 850 Million across 2023 to 2025. Halonix Technologies expanded LED capacity with new emergency luminaire lines, Bajaj Electricals scaled smart connected portfolios, Wipro Lighting commissioned addressable system production, Havells India expanded its Neemrana facility, and Signify scaled India-specific premium emergency lighting portfolios. Bureau of Indian Standards (BIS) registration mandates, IS 15498 certification, and the Production Linked Incentive (PLI) scheme for LED lighting components have structurally favoured domestic supply. Combined with NBC 2016 enforcement driving compliance demand and Smart Cities Mission projects scaling rapidly, these developments are reinforcing the India emergency lighting market forecast 2032 across the entire value chain.

Segmental Insights: India Emergency Lighting Market

By End-User: Commercial Segment Dominates the India Emergency Lighting Market

The commercial end-user segment dominates the India emergency lighting market, accounting for an estimated 38 to 40% of total demand, driven by the rapid expansion of Grade A office space, retail malls, IT parks, and corporate buildings, mandatory fire NOC compliance, and rising adoption of LED self-contained emergency luminaires. LED-based luminaires are the dominant technology within this segment, with self-contained systems capturing over 75% of commercial installations. The industrial segment contributes another 18 to 20% of demand, driven by factories, warehouses, MSMEs in textiles, automotive, chemicals, food processing, and engineering adopting NBC 2016-compliant emergency lighting to meet fire safety norms. The healthcare and hospitality segments together contribute 18 to 22%, while the transportation and infrastructure segment accounts for 12 to 15%, supported by metro rail, airport, and railway station modernisation. In 2025, leading emergency lighting players including Halonix Technologies, Bajaj Electricals, Wipro Lighting, Havells India, and Signify scaled commercial and institutional emergency lighting deployment under NBC 2016 enforcement and Smart Cities Mission projects, reinforcing segment dominance in the India emergency lighting market.

By Product Type: Self-Contained Emergency Luminaires Lead While Smart Addressable Systems Grow Fastest

Self-contained emergency luminaires lead the India emergency lighting market product landscape, accounting for approximately 55 to 58% of total emergency lighting installations, driven by their cost-effectiveness, compact form factor, and ease of installation across commercial, residential, and SME segments. Emergency exit signs contribute another 18 to 20%, primarily across egress paths in commercial, healthcare, hospitality, and transportation buildings. Smart addressable and IoT-connected emergency lighting systems are the fastest growing categories within the India emergency lighting market, expanding at 18 to 22% annually, driven by automated self-test functions, BMS integration, and growing adoption in premium commercial and institutional installations. Industrial emergency lighting and recessed luminaires together account for 15 to 18% of the market, with industrial high-bay emergency luminaires growing rapidly through 2032 across factories and logistics warehouses. Leading domestic manufacturers including Halonix Technologies, Bajaj Electricals, Wipro Lighting, Havells India, and Crompton Greaves have aligned product portfolios to this technology mix, driving high-efficiency emergency lighting adoption across the India emergency lighting market.

Regional Insights: India Emergency Lighting Market

Regional analysis of the India emergency lighting market shows that West India and South India collectively account for approximately 55 to 58% of total emergency lighting demand, driven by Maharashtra (Mumbai, Pune commercial belt), Gujarat (Ahmedabad, Surat industrial corridor), Karnataka (Bengaluru IT parks), Tamil Nadu (Chennai industrial and commercial clusters), and Telangana (Hyderabad IT and pharma clusters), supported by stringent fire safety enforcement and large-scale commercial real estate addition. North India contributes around 25 to 28% of demand, led by Delhi NCR, Uttar Pradesh, Haryana, Rajasthan, and Punjab, supported by commercial, hospitality, and warehousing expansion across Noida, Gurugram, and Greater Noida industrial corridors. East and Central India together account for 14 to 17% of demand, supported by West Bengal, Odisha, Madhya Pradesh, and Chhattisgarh, where Smart Cities Mission projects and metro rail expansion are accelerating compliance demand. In 2025, capacity additions and product launches by Halonix Technologies across Tamil Nadu and Karnataka, Bajaj Electricals in Maharashtra, Wipro Lighting in Karnataka and Tamil Nadu, Havells across Rajasthan and Haryana, and Signify across pan-India premium projects reinforced regional supply hubs, supporting closer execution of commercial, healthcare, hospitality, and transportation projects across the India emergency lighting market.

Recent Developments: India Emergency Lighting Market

- The India emergency lighting market witnessed strong momentum in product launches and policy progress during 2024 and 2025. India added approximately 70 million sq. ft. of new Grade A commercial office space across 2024 to 2025, with each new tower mandating NBC 2016-compliant emergency lighting installations. The Smart Cities Mission crossed completion of more than 8,000 individual projects across 100 cities, with allocations exceeding INR 1.66 lakh crore. Cumulative installed metro rail network in India crossed 950 km across 21 cities by 2025, growing at an average 12% annually, with each new corridor mandating compliant emergency lighting and exit signage.

- Domestic emergency lighting manufacturers have deepened India-focused capacity expansion. In 2025, Halonix Technologies scaled LED emergency luminaire production with new lithium-ion battery integrated lines, Bajaj Electricals expanded smart-connected emergency lighting portfolios, Wipro Lighting commissioned addressable system manufacturing, Havells India expanded its Neemrana and Alwar facilities, and Crompton Greaves grew its institutional emergency lighting portfolio. Signify Innovations India expanded its India-specific premium emergency luminaire portfolio. These developments are strengthening domestic supply and supporting the India emergency lighting market forecast 2032.

- Smart and IoT-connected emergency lighting momentum has gained strong traction in the India emergency lighting market. In 2025, leading global and domestic players including Schneider Electric, Legrand, Honeywell Automation India, Eaton, Signify (Philips), Halonix Technologies, and Bajaj Electricals expanded BMS-integrated and addressable emergency lighting portfolios. Strategic partnerships between domestic luminaire manufacturers, building safety EPC players, and facility management firms are positioning India as one of the most actively scaling emergency lighting markets globally, strengthening long-term competitive positioning in the India emergency lighting market forecast 2032.

Key Market Players: India Emergency Lighting Market

- Halonix Technologies Pvt. Ltd.

- Bajaj Electricals Limited

- Wipro Lighting (Wipro Enterprises Pvt. Ltd.)

- Havells India Limited

- Crompton Greaves Consumer Electricals Limited

- Signify Innovations India Limited (Philips)

- Eveready Industries India Limited

- Surya Roshni Limited

- Polycab India Limited

- Syska LED Lights

- Orient Electric Limited

- Schneider Electric India Pvt. Ltd.

- Legrand India Pvt. Ltd.

- Honeywell Automation India Limited

- Eaton Power Quality Pvt. Ltd.

Report Scope

In this report, the India Emergency Lighting Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

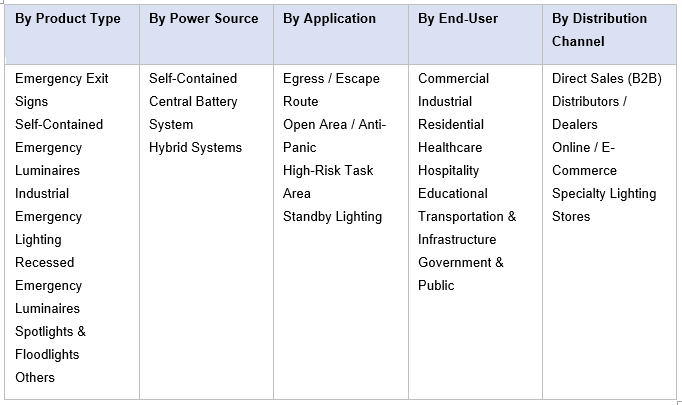

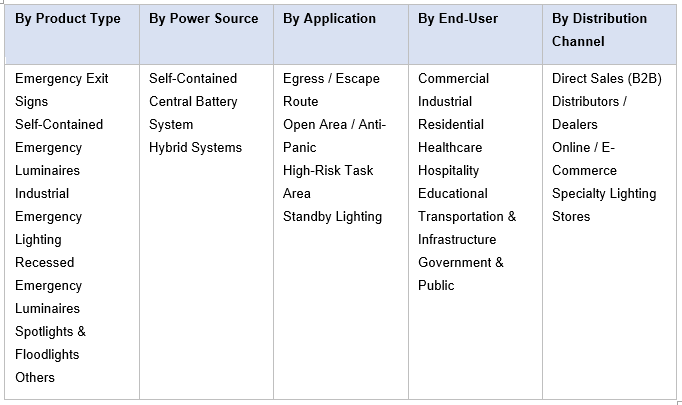

- By Product Type

- Emergency Exit Signs

- Self-Contained Emergency Luminaires

- Industrial Emergency Lighting

- Recessed Emergency Luminaires

- Spotlights & Floodlights

- Others

- By Power Source

- Self-Contained (Single-Point)

- Central Battery System

- Hybrid Systems

- By Lamp Type

- LED

- Fluorescent

- Incandescent

- Halogen

- Others

- By Operation

- Maintained

- Non-Maintained

- Combined / Sustained

- By Battery Type

- Lead-Acid

- Nickel-Cadmium (Ni-Cd)

- Lithium-Ion (Li-Ion)

- Nickel-Metal Hydride (NiMH)

- By Application

- Egress / Escape Route Lighting

- Open Area / Anti-Panic Lighting

- High-Risk Task Area Lighting

- Standby Lighting

- By End-User

- Commercial

- Industrial

- Residential

- Healthcare

- Hospitality

- Educational

- Transportation & Infrastructure

- Government & Public Buildings

- By Distribution Channel

- Direct Sales (B2B)

- Distributors / Dealers

- Online / E-Commerce

- Specialty Lighting Stores

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Emergency Lighting Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic emergency lighting OEMs, specialty addressable and IoT-connected luminaire producers, RESCO and OPEX-model players, or niche state-level installers and EPC firms.

The India Emergency Lighting Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Application

- By End-User

- By Power Source

- By Lamp Type

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Emergency Lighting Market

- India Emergency Lighting Market Insights

- Market Dynamics

- Growth Drivers

- National Building Code (NBC 2016) compliance and stringent fire safety regulations driving mandatory emergency lighting installations.

- Rapid commercial real estate, healthcare, and hospitality infrastructure expansion boosting emergency lighting demand.

- Transition to LED-based energy-efficient emergency lighting and smart connected systems across end-user segments.

- Restraints

- Price sensitivity and intense competition from unorganised and low-cost local manufacturers compressing margins.

- Inconsistent enforcement of fire safety codes across Tier 2 and Tier 3 cities limiting compliance-led demand.

- Limited awareness among residential consumers and SME segments delaying retrofit and upgrade adoption.

- Opportunities

- Smart Cities Mission, metro rail, airport modernisation, and logistics infrastructure expansion creating large project pipelines.

- IoT-enabled, addressable, and BMS-integrated emergency lighting systems opening premium commercial and industrial segments.

- Replacement demand from aging fluorescent and incandescent emergency lighting installations transitioning to LED.

- Challenges

- Skilled installation, periodic testing, and operations & maintenance workforce shortage limiting service quality.

- Battery lifecycle concerns and high upfront cost of lithium-ion battery-based emergency lighting limiting mid-market penetration.

- Counterfeit and sub-standard imported products eroding market confidence and complicating BIS / IS compliance enforcement.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Materials (LED chips, drivers, batteries, polycarbonate housings, electronic components)

- LED & Lamp Manufacturers (LED, fluorescent, incandescent, halogen)

- Battery, Inverter & Power Supply Suppliers (Li-Ion, Ni-Cd, NiMH, lead-acid)

- Electronic Drivers, Sensors & Smart Control System Providers

- Quality Control, R&D & Testing Laboratories (BIS, IS 15498, NBC 2016, IEC 60598-2-22)

- Distributors, Dealers & Online Aggregators (B2B and B2C platforms)

- Emergency Lighting OEMs & EPC Companies

- Brand Owners & Service Providers (Halonix, Bajaj, Wipro, Havells, Crompton, Signify, Eaton, Schneider, Legrand, Honeywell)

- Installation, Periodic Testing, O&M & Compliance Audits

- End-Users (commercial, industrial, residential, healthcare, hospitality, educational, transportation, government)

- India Emergency Lighting Market: Regulatory Framework

- India Emergency Lighting Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Million Units)

- Market Share & Forecast

- By Product Type

- Emergency Exit Signs

- Self-Contained Emergency Luminaires

- Industrial Emergency Lighting

- Recessed Emergency Luminaires

- Spotlights & Floodlights

- Others

- By Power Source

- Self-Contained (Single-Point)

- Central Battery System

- Hybrid Systems

- By Lamp Type

- LED

- Fluorescent

- Incandescent

- Halogen

- Others

- By Operation

- Maintained

- Non-Maintained

- Combined / Sustained

- By Battery Type

- Lead-Acid

- Nickel-Cadmium (Ni-Cd)

- Lithium-Ion (Li-Ion)

- Nickel-Metal Hydride (NiMH)

- By Application

- Egress / Escape Route Lighting

- Open Area / Anti-Panic Lighting

- High-Risk Task Area Lighting

- Standby Lighting

- By End-User

- Commercial

- Industrial

- Residential

- Healthcare

- Hospitality

- Educational

- Transportation & Infrastructure

- Government & Public Buildings

- By Distribution Channel

- Direct Sales (B2B)

- Distributors / Dealers

- Online / E-Commerce

- Specialty Lighting Stores

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Emergency Lighting Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Halonix Technologies Pvt. Ltd.

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- (Same Data Pointers Will Be Provided for The Below Companies)

- Bajaj Electricals Limited

- Wipro Lighting (Wipro Enterprises Pvt. Ltd.)

- Havells India Limited

- Crompton Greaves Consumer Electricals Limited

- Signify Innovations India Limited (Philips)

- Eveready Industries India Limited

- Surya Roshni Limited

- Polycab India Limited

- Syska LED Lights

- Orient Electric Limited

- Schneider Electric India Pvt. Ltd.

- Legrand India Pvt. Ltd.

- Honeywell Automation India Limited

- Eaton Power Quality Pvt. Ltd.

- Other Prominent Players

- Halonix Technologies Pvt. Ltd.

- Market Size & Forecast, 2021-2032

* Financial information in case of non-listed companies will be provided as per availability

** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. How large is the India emergency lighting market and what is its growth forecast?

Ans: The India emergency lighting market is entering a high-growth phase, supported by stringent NBC 2016 fire safety enforcement, rapid commercial real estate and healthcare infrastructure expansion, the Smart Cities Mission, and strong demand from commercial, industrial, hospitality, transportation, and institutional segments. The market is valued at USD 312 Million in 2025 and is projected to grow to USD 678 Million by 2032 at a CAGR of 11.7%, more than doubling over the forecast period. Growth is being supported by accelerated LED-based emergency lighting adoption, smart connected systems, and replacement demand from aging conventional luminaires. The report provides detailed market sizing, forecast modelling, and segment-wise analysis across capacity, value, end-use sector, system size, ownership model, and state-level demand.

2. Which segments are driving demand in the India emergency lighting market?

Ans: The India emergency lighting market segmentation shows that commercial buildings remain the largest demand base, contributing nearly 38 to 40% of total demand, driven by Grade A office space addition, retail malls, IT parks, and corporate buildings. However, smart and IoT-connected emergency lighting systems are now the fastest-growing category, supported by NBC 2016 compliance, BMS integration, and rising occupant-safety expectations across healthcare, hospitality, and transportation. The report analyses emergency lighting demand across commercial, industrial, residential, healthcare, hospitality, educational, transportation, and government applications. It also breaks down the market by product type, power source, lamp type, operation, battery type, and distribution channel.

3. What are the key drivers of growth in the India emergency lighting market?

Ans: Key India emergency lighting market drivers include stringent NBC 2016 compliance enforcement, rapid commercial real estate and healthcare infrastructure expansion, accelerated transition to LED-based energy-efficient luminaires, rising adoption of smart connected and addressable systems, and growing fire NOC-led specifications across commercial buildings. Demand is also being supported by the Smart Cities Mission with allocations exceeding INR 1.66 lakh crore across 100 cities, an operational metro rail network of more than 950 km across 21 cities, and airport modernisation projects. Growing demand from factories, malls, schools, hospitals, hotels, warehouses, and high-rise societies is further reinforcing structural growth across the India emergency lighting market.

4. Which regions are driving growth in the India emergency lighting market?

Ans: Regional analysis of the India emergency lighting market shows strong growth across Maharashtra, Gujarat, Karnataka, Tamil Nadu, Telangana, Delhi NCR, Uttar Pradesh, Haryana, Rajasthan, and West Bengal. Maharashtra and Gujarat have emerged as the strongest commercial and industrial emergency lighting markets, supported by Grade A office space expansion, manufacturing clusters, and stringent fire safety enforcement. Karnataka, Tamil Nadu, and Telangana lead in IT and ITeS-driven commercial demand. For healthcare and hospitality emergency lighting, demand is concentrated around Mumbai, Pune, Bengaluru, Chennai, Hyderabad, Delhi NCR, and Ahmedabad. The report provides state-wise and city-wise insights to help companies identify high-potential markets for OEM expansion, channel partnerships, and EPC opportunities.

5. What are the latest trends in the India emergency lighting market?

Ans: The latest India emergency lighting market trends include rapid LED-based emergency luminaire adoption, increasing penetration of lithium-ion battery-integrated systems, growing interest in smart addressable and IoT-connected emergency lighting, rising demand for BMS-integrated luminaires, and wider use of automated self-test and compliance reporting platforms. LED-based emergency lighting accounted for more than 70% of new installations in 2025, highlighting the growing importance of energy-efficient distributed life-safety systems within India's building safety mix. The market is also seeing stronger demand for high-efficiency luminaires, addressable controls, remote monitoring, energy management software, and compliance-led specification models. The report provides detailed insights into emerging technology trends, policy changes, state-level opportunities, pricing benchmarks, competitive landscape, and future demand shifts across the India emergency lighting market.

Frequently Asked Questions

1. How large is the India emergency lighting market and what is its growth forecast?

Ans: The India emergency lighting market is entering a high-growth phase, supported by stringent NBC 2016 fire safety enforcement, rapid commercial real estate and healthcare infrastructure expansion, the Smart Cities Mission, and strong demand from commercial, industrial, hospitality, transportation, and institutional segments. The market is valued at USD 312 Million in 2025 and is projected to grow to USD 678 Million by 2032 at a CAGR of 11.7%, more than doubling over the forecast period. Growth is being supported by accelerated LED-based emergency lighting adoption, smart connected systems, and replacement demand from aging conventional luminaires. The report provides detailed market sizing, forecast modelling, and segment-wise analysis across capacity, value, end-use sector, system size, ownership model, and state-level demand.

2. Which segments are driving demand in the India emergency lighting market?

Ans: The India emergency lighting market segmentation shows that commercial buildings remain the largest demand base, contributing nearly 38 to 40% of total demand, driven by Grade A office space addition, retail malls, IT parks, and corporate buildings. However, smart and IoT-connected emergency lighting systems are now the fastest-growing category, supported by NBC 2016 compliance, BMS integration, and rising occupant-safety expectations across healthcare, hospitality, and transportation. The report analyses emergency lighting demand across commercial, industrial, residential, healthcare, hospitality, educational, transportation, and government applications. It also breaks down the market by product type, power source, lamp type, operation, battery type, and distribution channel.

3. What are the key drivers of growth in the India emergency lighting market?

Ans: Key India emergency lighting market drivers include stringent NBC 2016 compliance enforcement, rapid commercial real estate and healthcare infrastructure expansion, accelerated transition to LED-based energy-efficient luminaires, rising adoption of smart connected and addressable systems, and growing fire NOC-led specifications across commercial buildings. Demand is also being supported by the Smart Cities Mission with allocations exceeding INR 1.66 lakh crore across 100 cities, an operational metro rail network of more than 950 km across 21 cities, and airport modernisation projects. Growing demand from factories, malls, schools, hospitals, hotels, warehouses, and high-rise societies is further reinforcing structural growth across the India emergency lighting market.

4. Which regions are driving growth in the India emergency lighting market?

Ans: Regional analysis of the India emergency lighting market shows strong growth across Maharashtra, Gujarat, Karnataka, Tamil Nadu, Telangana, Delhi NCR, Uttar Pradesh, Haryana, Rajasthan, and West Bengal. Maharashtra and Gujarat have emerged as the strongest commercial and industrial emergency lighting markets, supported by Grade A office space expansion, manufacturing clusters, and stringent fire safety enforcement. Karnataka, Tamil Nadu, and Telangana lead in IT and ITeS-driven commercial demand. For healthcare and hospitality emergency lighting, demand is concentrated around Mumbai, Pune, Bengaluru, Chennai, Hyderabad, Delhi NCR, and Ahmedabad. The report provides state-wise and city-wise insights to help companies identify high-potential markets for OEM expansion, channel partnerships, and EPC opportunities.

5. What are the latest trends in the India emergency lighting market?

Ans: The latest India emergency lighting market trends include rapid LED-based emergency luminaire adoption, increasing penetration of lithium-ion battery-integrated systems, growing interest in smart addressable and IoT-connected emergency lighting, rising demand for BMS-integrated luminaires, and wider use of automated self-test and compliance reporting platforms. LED-based emergency lighting accounted for more than 70% of new installations in 2025, highlighting the growing importance of energy-efficient distributed life-safety systems within India's building safety mix. The market is also seeing stronger demand for high-efficiency luminaires, addressable controls, remote monitoring, energy management software, and compliance-led specification models. The report provides detailed insights into emerging technology trends, policy changes, state-level opportunities, pricing benchmarks, competitive landscape, and future demand shifts across the India emergency lighting market.