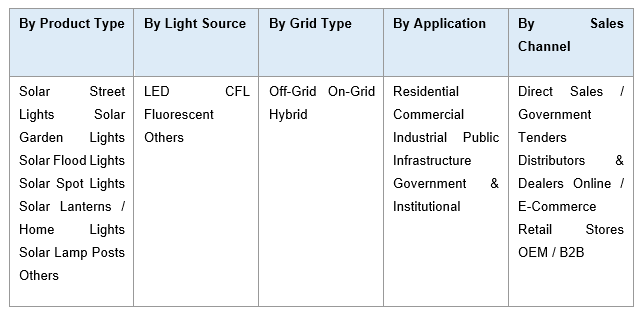

India Solar Lights Market, By Product Type (Solar Street Lights, Solar Garden Lights, Solar Flood Lights, Solar Spot Lights, Solar Lanterns / Home Lights, Solar Lamp Posts, Others); By Light Source (LED, CFL, Fluorescent, Others); By Grid Type (Off-Grid, On-Grid, Hybrid); By Component (Solar PV Module, LED Lamp, Battery, Charge Controller, Pole / Mounting Structure, Others); By Wattage (Below 20W, 20 to 50W, 50 to 100W, Above 100W); By Application (Residential, Commercial, Industrial, Public Infrastructure, Government & Institutional); By Sales Channel (Direct Sales / Government Tenders, Distributors & Dealers, Online / E-Commerce, Retail Stores, OEM / B2B); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- May 2026

- Pages 143

- Report Format: pdf

- Report Price: $1800 USD

India Solar Lights Market: Government Schemes and Smart City Rollouts Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

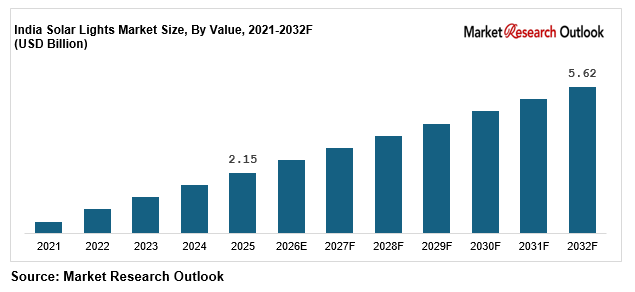

| Market Size (2025) | USD 2.15 Billion |

| CAGR (2026-2032) | 14.7% |

| Leading Segment | Solar Street Lights (Off-Grid LED) |

| Fastest Growing Segment | Smart & IoT-Enabled Solar Street Lights |

| Market Size (2032) | USD 5.62 Billion |

Source: Market Research Outlook

Market Overview: India Solar Lights Market

The India solar lights market size is witnessing rapid expansion, driven by accelerated rollout of government rural electrification schemes, rising deployment of solar street lights under Atal Jyoti Yojana and state-led programmes, the structural shift toward smart and IoT-enabled solar lighting solutions, and major manufacturing capacity expansions by domestic and global solar lighting players. Valued at USD 2.15 billion in 2025 and projected to reach USD 5.62 billion by 2032, growing at a CAGR of 14.7%, the India solar lights market growth is being fuelled by strong demand from government tenders, municipal corporations, smart city projects, rural electrification initiatives, and rising residential and commercial solar lighting adoption. Solar street lights lead consumption, while smart and IoT-enabled solar lighting solutions are emerging as the fastest growing segment. Government schemes such as Atal Jyoti Yojana, Mukhyamantri Gramin Solar Street Light Yojana, Deen Dayal Upadhyaya Gram Jyoti Yojana, and Street Lighting National Programme are reshaping the supply landscape. As Indian players including Halonix Technologies, Havells India, Bajaj Electricals, Surya Roshni, and Crompton Greaves Consumer Electricals expand solar lighting capacity, and PSU manufacturer ITI Limited scales solar street light supply under state schemes, the India solar lights market is evolving into a policy-led, technology-driven, and digitally enabled ecosystem with strong long-term growth potential.

Key Report Takeaways: India Solar Lights Market

- The India solar lights market size is projected to grow from USD 2.15 billion in 2025 to USD 5.62 billion by 2032, registering a strong CAGR of 14.7%, driven by accelerated government scheme rollouts, smart city deployment, falling solar PV and LED prices, and rising rural and urban solar lighting adoption.

- Solar street lights dominate the India solar lights market, accounting for over 55% of total demand, driven by Atal Jyoti Yojana, Mukhyamantri Gramin Solar Street Light Yojana, Deen Dayal Upadhyaya Gram Jyoti Yojana, and large municipal tenders by state governments and smart city authorities.

- Smart and IoT-enabled solar street lights are emerging as the fastest growing segment in the India solar lights market, expected to grow at 18 to 22% annually as motion sensors, remote monitoring, GSM connectivity, and centralised control platforms reshape municipal and smart city procurement strategies.

- Accelerated rollout of central and state government schemes, including the installation of over 4 lakh solar street lights under Atal Jyoti Yojana phases and 1.8 lakh units under Bihar’s Mukhyamantri Gramin Solar Street Light Yojana, is structurally expanding the India solar lights market across rural, semi-urban, and urban categories.

- Rising investments by domestic players such as Halonix Technologies, Havells India, Bajaj Electricals, Surya Roshni, Crompton Greaves Consumer Electricals, and PSU manufacturer ITI Limited in solar lighting capacity, LED integration, and lithium-ion battery storage are strengthening local supply and supporting the India solar lights market forecast 2032.

Key Market Drivers: India Solar Lights Market

Government Schemes and Rural Electrification Driving Solar Street Lights Adoption

Growth in the India solar lights market is being driven by the rapid scaling of central and state government schemes targeting rural electrification, road safety, and public lighting in semi-urban and urban areas. The Ministry of New and Renewable Energy launched Atal Jyoti Yojana (AJAY) in September 2016, under which approximately 2.72 lakh solar street lights were installed across Uttar Pradesh, Assam, Bihar, Jharkhand, Odisha, and other states in two phases, with an additional 1.37 lakh units installed under the extended phase up to June 2022. State-level schemes including Bihar’s Mukhyamantri Gramin Solar Street Light Yojana (1.8 lakh units ordered through ITI Limited and BREDA in 2024), Uttar Pradesh’s UPNEDA solar lighting projects, and Smart Cities Mission deployments are creating strong structural pull-through demand. The funding model under AJAY, where the Ministry of New and Renewable Energy contributes 75% and Member of Parliament Local Area Development Funds (MPLADS) contribute 25%, has made solar street lights highly accessible across the India solar lights market.

Falling Solar PV Module, LED, and Lithium-Ion Battery Prices Improving Cost Economics

The India solar lights market is benefiting from a sustained decline in core component prices, with solar PV module prices down by over 80% between 2010 and 2024, LED chip prices down by 40 to 50% over the past five years, and lithium-ion battery prices falling from over USD 700 per kWh in 2014 to below USD 130 per kWh in 2024 according to BloombergNEF. Average all-in cost of a 12W to 20W solar street light system in India now ranges between INR 8,000 and INR 18,000 depending on battery type, controller, and pole specifications, with payback periods of 3 to 5 years compared to grid-connected LED street lights. The Production Linked Incentive (PLI) Scheme for solar PV modules and white goods, Approved List of Models and Manufacturers (ALMM) policy, and Basic Customs Duty on imports have further strengthened domestic supply, supporting price competitiveness and quality assurance across the India solar lights market.

Smart Cities Mission, Street Lighting National Programme, and Smart Solar Lighting Demand

Rapid scaling of smart city infrastructure and intelligent public lighting is a major catalyst for the India solar lights market, with the Indian smart solar lighting segment projected to grow at 18 to 22% annually through 2032. The Street Lighting National Programme (SLNP) under Energy Efficiency Services Limited (EESL) has replaced over 1.3 crore conventional street lights with smart LED street lights across 500+ cities, with progressive integration of solar power. Smart Cities Mission projects across 100 cities are deploying IoT-enabled solar street lights with motion sensors, GSM connectivity, remote dimming, fault detection, and centralised control management systems. Leading players such as Halonix Technologies, Havells India, Bajaj Electricals, Crompton Greaves, Signify Innovations India, and Surya Roshni have launched smart solar street light portfolios in 2024 and 2025. Government tenders combined with municipal modernisation programmes are structurally expanding India solar lights market growth across all major end-user categories through 2032.

Key Market Challenges: India Solar Lights Market

High Upfront Capital Cost and Tender-Based Procurement Pressuring Margins

The India solar lights market continues to face challenges around high upfront capital costs compared to traditional grid-connected LED street lights, with average solar street light installations costing INR 22,000 to 35,000 per pole compared to INR 6,000 to 12,000 for conventional LED street lights. While solar street lights deliver significantly lower lifetime cost through eliminated electricity bills, the higher upfront capital expenditure remains a barrier for cash-strapped municipal corporations and gram panchayats. Tender-based procurement under government schemes including Atal Jyoti Yojana, EESL, ITI Limited, and BREDA has resulted in intense price-led competition, with margins for solar lighting suppliers compressed to 8 to 12%, creating sustainability concerns for unorganised sector players across the India solar lights market.

Limited Skilled Installation Workforce and Quality Variability in Unorganised Sector

The India solar lights market faces structural challenges from a shortage of skilled solar lighting installation, commissioning, and operations & maintenance workforce, particularly in rural and remote regions. Average installation timelines under government schemes have stretched by 30 to 45% due to limited certified installer availability. The unorganised sector, which accounts for an estimated 30 to 35% of solar lights supply in India, exhibits high quality variability in solar PV modules, batteries, charge controllers, and LED drivers, with field failure rates of 15 to 25% within the first three years of installation. Inconsistent battery quality, particularly in low-cost lead-acid systems, drives premature replacement costs and reduces consumer trust in the broader solar lights category. Skill India, MNRE Suryamitra programme, and BIS standardisation efforts are gradually addressing these gaps across the India solar lights market.

Battery Replacement, O&M Costs, and Theft & Vandalism Issues in Rural Areas

The India solar lights market faces ongoing operational complexity around battery replacement, ongoing maintenance costs, and theft and vandalism risks, particularly in rural and remote installation sites. Lead-acid batteries used in legacy solar street light installations typically require replacement every 2 to 3 years at INR 3,500 to 6,000 per unit, contributing to a 15 to 22% lifetime maintenance cost overhead. Lithium-ion batteries offer 8 to 10 year service life but add 25 to 35% to upfront cost. Theft of solar PV modules, batteries, and copper wiring has been reported across rural districts in Uttar Pradesh, Bihar, Jharkhand, and Odisha, with annual loss rates estimated at 3 to 6% of installed base in vulnerable areas. Smart solar street lights with GSM-based theft alerts, integrated battery designs, and tamper-proof enclosures are emerging as solutions, but premium pricing remains a barrier to widespread adoption across the India solar lights market.

Key Market Trends: India Solar Lights Market

Rapid Adoption of Smart, IoT-Enabled Solar Street Lights with Sensors and Remote Monitoring

The India solar lights market is undergoing a clear shift toward smart, IoT-enabled solar street light systems with motion sensors, GSM connectivity, remote dimming, fault diagnostics, and centralised control management, with smart solar lighting growing at 18 to 22% annually, significantly outpacing conventional solar street lights. Smart solar street lights deliver 40 to 60% additional energy savings through adaptive dimming based on traffic patterns, while integrated GSM and IoT modules enable real-time fault detection, theft alerts, and remote firmware updates. In 2024, WindStream Energy Technologies launched a hybrid wind-solar LED street light system delivering higher generation per square foot than conventional solar street lights. Smart Cities Mission deployments across 100 cities, combined with municipal modernisation initiatives by Brihanmumbai Municipal Corporation, Pune Municipal Corporation, Bengaluru BBMP, and Delhi NDMC, are reinforcing this structural trend across the India solar lights market.

Shift from Lead-Acid to Lithium-Ion Battery Storage in Solar Lighting Systems

A clear shift from lead-acid to lithium-ion (LiFePO4) battery storage is reshaping the India solar lights market, with lithium-ion adoption expected to capture over 65% of new solar street light installations by 2027. Lithium-ion batteries deliver 8 to 10 year service life compared to 2 to 3 years for lead-acid, while offering 30 to 50% higher depth of discharge, faster charging cycles, and significantly lower maintenance requirements. Falling lithium-ion battery prices, down from USD 700+ per kWh in 2014 to below USD 130 per kWh in 2024, combined with PLI scheme support for advanced chemistry cell manufacturing, are accelerating this transition. Leading players such as Halonix Technologies, Havells India, Bajaj Electricals, Crompton Greaves, Surya Roshni, and Signify Innovations India have shifted product portfolios toward lithium-ion-based solar street lights and integrated battery designs across the India solar lights market.

Capacity Expansion by Domestic Manufacturers and PSU-Led Tenders Reshaping Supply

A wave of domestic capacity expansion and PSU-led tender activity is reshaping the India solar lights market supply landscape. ITI Limited received an order from BREDA in September 2024 to supply and install 1 lakh solar street light systems in Bihar, on top of the 80,000 systems already under execution under Mukhyamantri Gramin Solar Street Light Yojana. EESL has expanded solar street light tenders under Street Lighting National Programme integration. Domestic players including Halonix Technologies, Havells India, Bajaj Electricals, Surya Roshni, and Crompton Greaves have scaled solar lighting capacity through 2024 and 2025, with combined India-focused capital expenditure announcements in solar lighting and integrated LED-solar manufacturing exceeding INR 1,500 crore. Smart Cities Mission tenders, Mumbai Municipal Corporation lighting upgrades, and large-scale Uttar Pradesh UPNEDA installations such as the Ayodhya 470 solar street light corridor are reinforcing the India solar lights market forecast 2032 across the entire value chain.

Segmental Insights: India Solar Lights Market

By Product Type: Solar Street Lights Dominate the India Solar Lights Market

The solar street lights product segment dominates the India solar lights market, accounting for an estimated 55 to 58% of total solar lights consumption, driven by strong demand from government tenders under Atal Jyoti Yojana, Mukhyamantri Gramin Solar Street Light Yojana, Deen Dayal Upadhyaya Gram Jyoti Yojana, and Smart Cities Mission. LED-based solar street lights with off-grid configuration represent over 80% of solar street light installations, with smart and IoT-enabled variants gaining share rapidly. Solar lanterns and home lighting systems contribute another 15 to 18% of demand, supported by rural electrification programmes by NGOs and social enterprises such as Sun King (Greenlight Planet) and d.light. Solar garden lights, flood lights, and spot lights together contribute 18 to 22% of demand, driven by residential and commercial adoption. In 2025, leading players including Halonix Technologies, Havells India, Bajaj Electricals, Surya Roshni, and Crompton Greaves scaled up solar street light supply tied to government tenders, reinforcing segment dominance in the India solar lights market.

By Light Source: LED Leads While Smart Adaptive LED Grows Fastest

LED-based solar lights lead the India solar lights market by light source, accounting for approximately 88 to 92% of total solar lights demand, driven by their superior efficacy of 130 to 180 lumens per watt, longer service life of 50,000+ hours, lower heat generation, and improving cost economics. Smart adaptive LED solar lights with motion sensors and dimming controls are the fastest growing category within the India solar lights market, expanding at 18 to 22% annually, driven by smart city deployments and municipal modernisation. CFL and fluorescent solar lights, which dominated the market a decade ago, now account for less than 8% of demand, primarily in legacy installations. Leading domestic LED manufacturers including Halonix Technologies, Havells India, Bajaj Electricals, Crompton Greaves, Surya Roshni, Wipro Lighting, and Signify Innovations India have aligned product portfolios to high-efficacy LED chip integration, driving smart LED adoption across the India solar lights market.

Regional Insights: India Solar Lights Market

Regional analysis of the India solar lights market shows that North India and West India collectively account for approximately 55 to 58% of total solar lights demand, driven by large-scale government scheme rollouts in Uttar Pradesh, Bihar, Rajasthan, Haryana, Madhya Pradesh, Gujarat, and Maharashtra, supported by Atal Jyoti Yojana, Mukhyamantri Gramin Solar Street Light Yojana, and Smart Cities Mission deployments. North India alone accounts for around 30 to 32% of demand, led by Uttar Pradesh’s UPNEDA installations including the Ayodhya 470 solar street light corridor and Bihar’s BREDA tenders for 1.8 lakh solar street lights. South India contributes around 22 to 24% of demand, led by Karnataka, Tamil Nadu, Andhra Pradesh, and Telangana, supported by smart city deployments in Bengaluru, Chennai, and Hyderabad. East and Central India together account for 20 to 24% of demand, supported by West Bengal, Odisha, Jharkhand, Madhya Pradesh, and Chhattisgarh, where rural electrification under Deen Dayal Upadhyaya Gram Jyoti Yojana is accelerating. In 2025, capacity additions and tender execution by ITI Limited in Bihar, Halonix Technologies and Havells India across pan-India sites, Bajaj Electricals in Maharashtra, and Surya Roshni in Uttar Pradesh reinforced regional supply hubs across the India solar lights market.

Recent Developments: India Solar Lights Market

- The India solar lights market witnessed strong momentum in tender execution and product innovation during 2024 and 2025. ITI Limited received a major order from BREDA in September 2024 to supply and install 1 lakh solar street light systems in Bihar, adding to 80,000 systems already under execution under Mukhyamantri Gramin Solar Street Light Yojana. The Uttar Pradesh government installed a record-breaking 470 solar-powered street lights stretching 10.2 km from Guptar Ghat to Laxman Ghat in Ayodhya through UPNEDA, becoming one of the world’s longest solar street light corridors.

- Domestic solar lighting manufacturers have deepened India-focused capacity expansion. In 2024 and 2025, Halonix Technologies launched smart solar street light variants with IoT integration, Havells India expanded its solar-powered outdoor lighting portfolio, Bajaj Electricals strengthened its Built to Shine positioning with refreshed solar street light ranges, Surya Roshni scaled solar LED capacity at its Malanpur and Kashipur facilities, and Crompton Greaves expanded smart solar lighting offerings. Combined India-focused capital expenditure in solar lighting and integrated LED-solar manufacturing crossed INR 1,500 crore across 2023 to 2025.

- Smart and IoT-enabled solar lighting momentum has gained strong traction in the India solar lights market. In 2024 and 2025, Smart Cities Mission deployments across Pune, Bengaluru, Surat, Indore, Bhopal, and Bhubaneswar expanded smart solar street light coverage with motion sensors, GSM connectivity, and centralised management systems. Strategic partnerships between Indian solar lighting players and global LED chip suppliers including Signify Innovations India, Bridgelux, and Osram are positioning India as one of the most actively scaling solar lighting markets globally, strengthening long-term competitive positioning in the India solar lights market forecast 2032.

Key Market Players: India Solar Lights Market

- Halonix Technologies Pvt. Ltd.

- Havells India Limited

- Bajaj Electricals Limited

- Crompton Greaves Consumer Electricals Limited

- Surya Roshni Limited

- Signify Innovations India Limited (Philips Lighting)

- Wipro Enterprises Limited (Wipro Lighting)

- Syska LED Lights Pvt. Ltd.

- Polycab India Limited

- Goldmedal Electricals Pvt. Ltd.

- Orient Electric Limited

- ITI Limited (Government of India PSU)

- Tata Power Solar Systems Limited

- Sun King (Greenlight Planet India Pvt. Ltd.)

- Novergy Energy Solutions Pvt. Ltd.

Report Scope

In this report, the India Solar Lights Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Solar Street Lights

- Solar Garden Lights

- Solar Flood Lights

- Solar Spot Lights

- Solar Lanterns / Home Lights

- Solar Lamp Posts

- Others

- By Light Source

- LED

- CFL

- Fluorescent

- Others

- By Grid Type

- Off-Grid

- On-Grid

- Hybrid

- By Component

- Solar PV Module

- LED Lamp

- Battery (Lithium-Ion, Lead-Acid)

- Charge Controller

- Pole / Mounting Structure

- Others

- By Wattage

- Below 20W

- 20 to 50W

- 50 to 100W

- Above 100W

- By Application

- Residential

- Commercial

- Industrial

- Public Infrastructure

- Government & Institutional

- By Sales Channel

- Direct Sales / Government Tenders

- Distributors & Dealers

- Online / E-Commerce

- Retail Stores

- OEM / B2B

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Solar Lights Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic solar lighting manufacturers, smart and IoT-enabled solar street light specialists, hybrid lighting innovators, or niche segment leaders.

The India Solar Lights Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Application

- By Light Source

- By Grid Type

- By Sales Channel

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Solar Lights Market

- India Solar Lights Market Insights

- Market Dynamics

- Growth Drivers

- Government schemes and rural electrification driving solar street lights adoption across India.

- Falling solar PV module, LED, and lithium-ion battery prices improving solar lights cost economics.

- Smart Cities Mission, Street Lighting National Programme, and growing smart solar lighting demand.

- Restraints

- High upfront capital cost and tender-based procurement pressuring solar lights margins.

- Limited skilled installation workforce and quality variability in unorganised solar lights sector.

- Battery replacement, O&M costs, and theft & vandalism issues in rural solar street light installations.

- Opportunities

- Smart and IoT-enabled solar street lights with motion sensors, GSM connectivity, and remote monitoring.

- Hybrid solar-wind lighting systems and integrated lithium-ion battery solutions for higher reliability.

- Export opportunities for Indian solar lights manufacturers to Africa, Middle East, and Southeast Asia.

- Challenges

- Intense price-led competition between organised and unorganised players compressing margins.

- Shortage of skilled solar lighting installation, commissioning, and operations & maintenance workforce.

- Inconsistent product quality, premature battery failures, and field reliability concerns in rural deployments.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Growth Drivers

- Industry Value Chain & Entry Points

- Upstream Raw Materials (silicon wafers, polysilicon, LED chips, semiconductor materials, lithium, lead)

- Solar PV Module Manufacturers (Mono PERC, polycrystalline, small-format modules for solar lights)

- LED Chip & Driver Suppliers (Bridgelux, Osram, Signify, domestic LED manufacturers)

- Battery Manufacturers (lithium-ion / LiFePO4, lead-acid, integrated battery designs)

- Charge Controllers, Sensors & IoT Module Suppliers (smart lighting electronics)

- Solar Lights OEM & Assembly (Halonix, Havells, Bajaj, Crompton, Surya Roshni, ITI Limited)

- Distributors, Dealers & Online Marketplaces (B2B and B2C platforms)

- Government Tendering Agencies (EESL, MNRE, BREDA, UPNEDA, ITI, smart city SPVs)

- Installation, Commissioning & O&M Service Providers (certified installers, EPC contractors)

- End-Users (residential, commercial, industrial, government, municipal, institutional)

- India Solar Lights Market: Regulatory Framework

- India Solar Lights Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (Units Installed)

- Market Share & Forecast

- By Product Type

- Solar Street Lights

- Solar Garden Lights

- Solar Flood Lights

- Solar Spot Lights

- Solar Lanterns / Home Lights

- Solar Lamp Posts

- Others

- By Light Source

- LED

- CFL

- Fluorescent

- Others

- By Grid Type

- Off-Grid

- On-Grid

- Hybrid

- By Component

- Solar PV Module

- LED Lamp

- Battery (Lithium-Ion, Lead-Acid)

- Charge Controller

- Pole / Mounting Structure

- Others

- By Wattage

- Below 20W

- 20 to 50W

- 50 to 100W

- Above 100W

- By Application

- Residential

- Commercial

- Industrial

- Public Infrastructure

- Government & Institutional

- By Sales Channel

- Direct Sales / Government Tenders

- Distributors & Dealers

- Online / E-Commerce

- Retail Stores

- OEM / B2B

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Solar Lights Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Halonix Technologies Pvt. Ltd.

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- *(Same Data Pointers Will Be Provided for The Below Companies)*

- Havells India Limited

- Bajaj Electricals Limited

- Crompton Greaves Consumer Electricals Limited

- Surya Roshni Limited

- Signify Innovations India Limited (Philips Lighting)

- Wipro Enterprises Limited (Wipro Lighting)

- Syska LED Lights Pvt. Ltd.

- Polycab India Limited

- Goldmedal Electricals Pvt. Ltd.

- Orient Electric Limited

- ITI Limited (Government of India PSU)

- Tata Power Solar Systems Limited

- Sun King (Greenlight Planet India Pvt. Ltd.)

- Novergy Energy Solutions Pvt. Ltd.

- Other Prominent Players

- By Product Type

- Market Size & Forecast, 2021-2032

- Market Dynamics

** Financial information in case of non-listed companies will be provided as per availability*

*** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable*

Frequently Asked Questions

1. How large is the India solar lights market and what is its growth forecast?

Ans: The India solar lights market is entering a high-growth phase, supported by accelerated rural electrification schemes, smart city deployments, falling solar PV and lithium-ion battery prices, and rising residential, commercial, and government demand. The India solar lights market is valued at USD 2.15 billion in 2025 and is projected to reach USD 5.62 billion by 2032, growing at a CAGR of 14.7%. India added significant solar street light capacity in 2024 and 2025, supported by central schemes including Atal Jyoti Yojana, Mukhyamantri Gramin Solar Street Light Yojana, Smart Cities Mission, and Deen Dayal Upadhyaya Gram Jyoti Yojana. The market is expected to continue expanding steadily through 2032 as gram panchayats, municipal corporations, smart city authorities, MSMEs, residential societies, and institutional buyers shift toward off-grid LED solar lighting and smart IoT-enabled solar street lights to reduce energy costs and strengthen public safety. The report provides detailed India solar lights market sizing, forecast modelling, and segment-wise analysis across product type, light source, grid type, wattage, application, sales channel, and state-level demand.

2. Which segments are driving demand in the India solar lights market?

Ans: The India solar lights market segmentation shows that solar street lights remain the largest demand base, accounting for an estimated 55 to 58% of total solar lights consumption, driven by Atal Jyoti Yojana, Mukhyamantri Gramin Solar Street Light Yojana, Smart Cities Mission, and large municipal tenders by state governments and gram panchayats. Smart and IoT-enabled solar street lights with motion sensors, GSM connectivity, and remote monitoring are now the fastest-growing category, supported by smart city deployments, municipal modernisation, and rising adoption of lithium-ion batteries. The report analyses India solar lights market demand across residential, commercial, industrial, public infrastructure, and government & institutional applications. It also breaks down the market by product type (solar street lights, solar garden lights, solar flood lights, solar spot lights, solar lanterns and home lights, solar lamp posts), light source (LED, CFL, fluorescent), grid type (off-grid, on-grid, hybrid), wattage class, component, and sales channel.

3. What are the key drivers of growth in the India solar lights market?

Ans: Key India solar lights market drivers include rising government scheme rollouts, falling solar PV module and lithium-ion battery prices, accelerated smart city deployments, improving financing availability for municipal bodies, and growing adoption of smart IoT-enabled solar street lights with adaptive dimming. Under Atal Jyoti Yojana, around 2.72 lakh solar street lights were installed across two phases, with an additional 1.37 lakh units deployed under the extended phase up to June 2022. State-level momentum is equally strong, with ITI Limited receiving an order from BREDA in September 2024 to supply and install 1 lakh solar street light systems in Bihar, on top of 80,000 units already in execution under Mukhyamantri Gramin Solar Street Light Yojana. Demand is also supported by falling lithium-ion battery prices (from over USD 700 per kWh in 2014 to below USD 130 per kWh in 2024), rising LED chip efficacy of 130 to 180 lumens per watt, domestic manufacturing expansion under PLI scheme, and growing demand from gram panchayats, municipal corporations, smart city SPVs, schools, hospitals, factories, warehouses, and residential societies.

4. Which regions are driving growth in the India solar lights market?

Ans: Regional analysis of the India solar lights market shows strong growth across Uttar Pradesh, Bihar, Rajasthan, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Tamil Nadu, Andhra Pradesh, Telangana, Odisha, Jharkhand, and West Bengal. North India and West India collectively account for approximately 55 to 58% of total solar lights demand, with Uttar Pradesh emerging as one of the strongest markets, supported by UPNEDA installations including the record-breaking Ayodhya 470 solar street light corridor stretching 10.2 km from Guptar Ghat to Laxman Ghat. Bihar has emerged as a leading state for solar street light deployment under BREDA tenders and Mukhyamantri Gramin Solar Street Light Yojana. Maharashtra, Gujarat, Rajasthan, and Madhya Pradesh are also among the leading states for solar street light adoption. For commercial and residential solar lights demand, growth is concentrated around urban clusters such as Mumbai, Delhi NCR, Bengaluru, Hyderabad, Pune, Chennai, Indore, and Ahmedabad. The report provides state-wise and city-wise insights to help companies identify high-potential markets for tender participation, dealer expansion, channel partnerships, financing, and component sales across the India solar lights market.

5. What are the latest trends in the India solar lights market?

Ans: The latest India solar lights market trends include rapid adoption of smart IoT-enabled solar street lights with motion sensors and remote monitoring, growing shift from lead-acid to lithium iron phosphate (LiFePO4) batteries, increasing deployment of hybrid solar-wind street light systems, rising integration of GSM-based theft alerts, and expanding use of centralised lighting management systems for municipal and smart city applications. Smart solar street lights are projected to grow at 18 to 22% annually through 2032, delivering 40 to 60% additional energy savings through adaptive dimming. Lithium-ion battery adoption is expected to capture over 65% of new solar street light installations by 2027. The market is also seeing stronger demand for high-efficacy LED chips (130 to 180 lumens per watt), tamper-proof integrated battery designs, premium solar garden and flood lights for residential and commercial users, and online e-commerce sales channels for residential solar lighting products. The report provides detailed insights into emerging technology trends, government scheme updates, state-level tender opportunities, pricing benchmarks, competitive landscape, and future demand shifts across the India solar lights market through 2032.

Frequently Asked Questions

1. How large is the India solar lights market and what is its growth forecast?

Ans: The India solar lights market is entering a high-growth phase, supported by accelerated rural electrification schemes, smart city deployments, falling solar PV and lithium-ion battery prices, and rising residential, commercial, and government demand. The India solar lights market is valued at USD 2.15 billion in 2025 and is projected to reach USD 5.62 billion by 2032, growing at a CAGR of 14.7%. India added significant solar street light capacity in 2024 and 2025, supported by central schemes including Atal Jyoti Yojana, Mukhyamantri Gramin Solar Street Light Yojana, Smart Cities Mission, and Deen Dayal Upadhyaya Gram Jyoti Yojana. The market is expected to continue expanding steadily through 2032 as gram panchayats, municipal corporations, smart city authorities, MSMEs, residential societies, and institutional buyers shift toward off-grid LED solar lighting and smart IoT-enabled solar street lights to reduce energy costs and strengthen public safety. The report provides detailed India solar lights market sizing, forecast modelling, and segment-wise analysis across product type, light source, grid type, wattage, application, sales channel, and state-level demand.

2. Which segments are driving demand in the India solar lights market?

Ans: The India solar lights market segmentation shows that solar street lights remain the largest demand base, accounting for an estimated 55 to 58% of total solar lights consumption, driven by Atal Jyoti Yojana, Mukhyamantri Gramin Solar Street Light Yojana, Smart Cities Mission, and large municipal tenders by state governments and gram panchayats. Smart and IoT-enabled solar street lights with motion sensors, GSM connectivity, and remote monitoring are now the fastest-growing category, supported by smart city deployments, municipal modernisation, and rising adoption of lithium-ion batteries. The report analyses India solar lights market demand across residential, commercial, industrial, public infrastructure, and government & institutional applications. It also breaks down the market by product type (solar street lights, solar garden lights, solar flood lights, solar spot lights, solar lanterns and home lights, solar lamp posts), light source (LED, CFL, fluorescent), grid type (off-grid, on-grid, hybrid), wattage class, component, and sales channel.

3. What are the key drivers of growth in the India solar lights market?

Ans: Key India solar lights market drivers include rising government scheme rollouts, falling solar PV module and lithium-ion battery prices, accelerated smart city deployments, improving financing availability for municipal bodies, and growing adoption of smart IoT-enabled solar street lights with adaptive dimming. Under Atal Jyoti Yojana, around 2.72 lakh solar street lights were installed across two phases, with an additional 1.37 lakh units deployed under the extended phase up to June 2022. State-level momentum is equally strong, with ITI Limited receiving an order from BREDA in September 2024 to supply and install 1 lakh solar street light systems in Bihar, on top of 80,000 units already in execution under Mukhyamantri Gramin Solar Street Light Yojana. Demand is also supported by falling lithium-ion battery prices (from over USD 700 per kWh in 2014 to below USD 130 per kWh in 2024), rising LED chip efficacy of 130 to 180 lumens per watt, domestic manufacturing expansion under PLI scheme, and growing demand from gram panchayats, municipal corporations, smart city SPVs, schools, hospitals, factories, warehouses, and residential societies.

4. Which regions are driving growth in the India solar lights market?

Ans: Regional analysis of the India solar lights market shows strong growth across Uttar Pradesh, Bihar, Rajasthan, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Tamil Nadu, Andhra Pradesh, Telangana, Odisha, Jharkhand, and West Bengal. North India and West India collectively account for approximately 55 to 58% of total solar lights demand, with Uttar Pradesh emerging as one of the strongest markets, supported by UPNEDA installations including the record-breaking Ayodhya 470 solar street light corridor stretching 10.2 km from Guptar Ghat to Laxman Ghat. Bihar has emerged as a leading state for solar street light deployment under BREDA tenders and Mukhyamantri Gramin Solar Street Light Yojana. Maharashtra, Gujarat, Rajasthan, and Madhya Pradesh are also among the leading states for solar street light adoption. For commercial and residential solar lights demand, growth is concentrated around urban clusters such as Mumbai, Delhi NCR, Bengaluru, Hyderabad, Pune, Chennai, Indore, and Ahmedabad. The report provides state-wise and city-wise insights to help companies identify high-potential markets for tender participation, dealer expansion, channel partnerships, financing, and component sales across the India solar lights market.

5. What are the latest trends in the India solar lights market?

Ans: The latest India solar lights market trends include rapid adoption of smart IoT-enabled solar street lights with motion sensors and remote monitoring, growing shift from lead-acid to lithium iron phosphate (LiFePO4) batteries, increasing deployment of hybrid solar-wind street light systems, rising integration of GSM-based theft alerts, and expanding use of centralised lighting management systems for municipal and smart city applications. Smart solar street lights are projected to grow at 18 to 22% annually through 2032, delivering 40 to 60% additional energy savings through adaptive dimming. Lithium-ion battery adoption is expected to capture over 65% of new solar street light installations by 2027. The market is also seeing stronger demand for high-efficacy LED chips (130 to 180 lumens per watt), tamper-proof integrated battery designs, premium solar garden and flood lights for residential and commercial users, and online e-commerce sales channels for residential solar lighting products. The report provides detailed insights into emerging technology trends, government scheme updates, state-level tender opportunities, pricing benchmarks, competitive landscape, and future demand shifts across the India solar lights market through 2032.