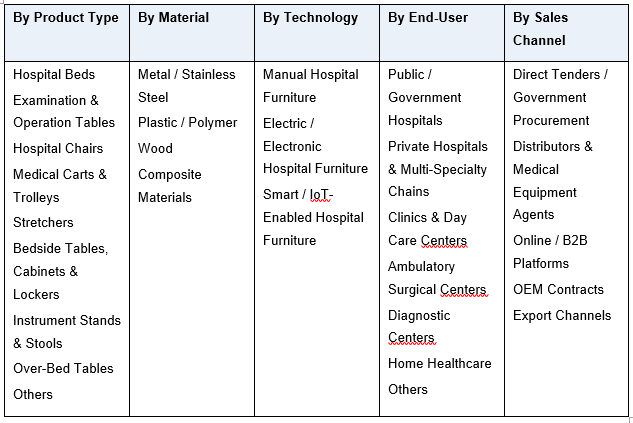

India Hospital Furniture Market, By Product Type (Hospital Beds (Acute Care, ICU, Psychiatric, Bariatric, Pediatric), Examination & Operation Tables (Surgical, Examination, Delivery), Hospital Chairs (Manual, Electric, Blood Donor, Dental), Medical Carts & Trolleys, Stretchers, Bedside Tables, Cabinets & Lockers, Instrument Stands & Stools, Over-Bed Tables, Others); By Material (Metal / Stainless Steel, Plastic / Polymer, Wood, Composite Materials); By Technology (Manual Hospital Furniture, Electric / Electronic Hospital Furniture, Smart / IoT-Enabled Hospital Furniture); By End-User (Public / Government Hospitals, Private Hospitals & Multi-Specialty Chains, Clinics & Day Care Centers, Ambulatory Surgical Centers, Diagnostic Centers, Home Healthcare, Others); By Sales Channel (Direct Tenders / Government Procurement, Distributors & Medical Equipment Agents, Online / B2B Platforms, OEM Contracts, Export Channels); By Trend Analysis, Competitive Landscape & Forecast, 2021 to 2032

- Consumer Goods & Retail

- May 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Hospital Furniture Market: Healthcare Infrastructure Expansion & Smart Ergonomic Furniture Shift Powers Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

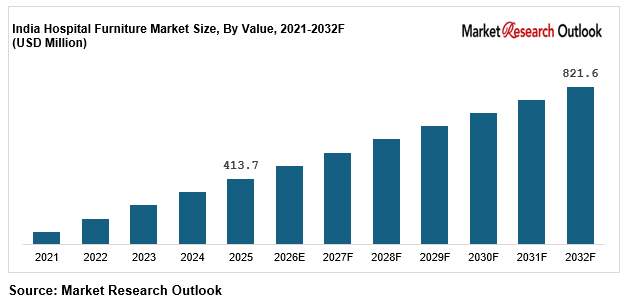

| Market Size (2025) | USD 413.7 Million |

| CAGR (2026-2032) | 10.3% |

| Leading Segment | Hospital Beds |

| Fastest Growing Segment | Electric & Smart IoT-Enabled Hospital Furniture |

| Market Size (2032) | USD 821.6 Million |

Source: Market Research Outlook

Market Overview: India Hospital Furniture Market

The India hospital furniture market size is witnessing rapid expansion, driven by accelerated healthcare infrastructure development, rising private hospital chain investments, the structural shift toward electric and smart ergonomic hospital furniture, and major capacity expansions by global and domestic hospital furniture producers. Valued at USD 413.7 million in 2025 and projected to reach USD 821.6 million by 2032, growing at a CAGR of 10.3%, the India hospital furniture market growth is being fuelled by strong demand from public and private hospitals, multi-specialty chains, ambulatory surgical centers, diagnostic centers, and home healthcare applications. Hospital beds lead consumption, while electric and smart IoT-enabled hospital furniture is emerging as the fastest-growing segment. Tightening CDSCO and BIS norms, NABH and JCI accreditation standards, Ayushman Bharat and PM-ABHIM healthcare missions, and corporate ESG commitments are reshaping the supply landscape. As global majors including Hill-Rom (Baxter), Stryker, Paramount Bed, and Midmark expand India-specific manufacturing capacity and domestic players including Godrej Interio, GPC Medical, Narang Medical, PMT Healthcare, and Hitech Medicare Devices scale electric and ergonomic furniture capacity, the India hospital furniture market is evolving into a patient-experience-led, infection-control-focused, and export-competitive ecosystem with strong long-term growth potential.

Key Report Takeaways: India Hospital Furniture Market

- The India hospital furniture market size is projected to grow from USD 413.7 million in 2025 to USD 821.6 million by 2032, registering a strong CAGR of 10.3%, driven by accelerated healthcare infrastructure development, private hospital chain expansion, and the structural shift toward electric and smart hospital furniture.

- Hospital beds dominate the India hospital furniture market, accounting for over 38% of total demand, driven by strong adoption across acute care, ICU, psychiatric, bariatric, and pediatric applications in public and private hospital settings.

- Electric and smart IoT-enabled hospital furniture is emerging as the fastest-growing segment in the India hospital furniture market, expected to grow at 13% to 16% annually as critical care expansion, infection control protocols, and ergonomic procurement reshape product strategies.

- Accelerated growth of the Indian healthcare industry, led by Apollo Hospitals, Fortis Healthcare, Manipal Hospitals, Max Healthcare, Narayana Health, and Medanta, along with new tertiary care additions including AIIMS, ESIC, and PM-ABHIM-funded hospitals, is structurally expanding demand for hospital furniture across critical care and surgical categories.

- Rising investments by global hospital furniture majors such as Hill-Rom (Baxter), Stryker, Paramount Bed, and Midmark in India-specific manufacturing capacity and clinical engineering laboratories are strengthening local innovation and supporting the India hospital furniture market forecast 2032.

Key Market Drivers: India Hospital Furniture Market

Rapid Expansion of Healthcare Infrastructure in Tier-2 and Tier-3 Cities Driving Hospital Furniture Demand

Growth in the India hospital furniture market is being driven by the rapid expansion of Indian healthcare infrastructure, which is growing at 11% to 13% annually under Ayushman Bharat, PM-ABHIM, and state-level health missions, significantly outpacing most other healthcare end-uses. Hospital bed capacity addition accounts for approximately 60% of new healthcare infrastructure investment, with hospital furniture forming the core procurement category for new and expanding facilities. Per-capita hospital bed availability in India currently stands at around 1.5 to 1.7 beds per 1,000 population, compared to 4 to 6 in developed markets, indicating significant long-term headroom for growth. Major hospital chains including Apollo Hospitals, Fortis Healthcare, Manipal Hospitals, Max Healthcare, and Narayana Health, along with new tertiary care additions including AIIMS expansions and PM-ABHIM-funded hospitals, have announced combined capacity expansions exceeding USD 6 billion, creating strong structural pull-through demand for hospital beds, examination tables, and medical carts across the India hospital furniture market.

Structural Shift Toward Electric, Smart, and IoT-Enabled Hospital Furniture Aligned with Modern Critical Care Norms

The India hospital furniture market is witnessing a strong and accelerating shift toward electric and smart IoT-enabled hospital furniture, growing at 13% to 16% annually, nearly twice the pace of conventional manual alternatives. Tightening CDSCO medical device norms, NABH and JCI accreditation requirements, infection control protocols, and corporate ESG mandates are reshaping procurement strategies across acute care, ICU, surgical, and ambulatory care segments. Electric ICU beds typically deliver 30% to 40% better patient outcomes through pressure redistribution, integrated weighing, and remote monitoring compared to manual alternatives, making them the preferred choice for premium and critical care installations. Global hospital furniture majors including Hill-Rom (Baxter), Stryker, Paramount Bed, and Midmark have launched expanded electric and smart-enabled portfolios in 2024 and 2025, while domestic players are parallelly scaling electric assembly capacity, reinforcing this structural trend across the India hospital furniture market.

Accelerated Private Hospital Chain Expansion, Medical Tourism, and Ambulatory Surgical Center Demand

Rapid private hospital chain expansion, medical tourism, and ambulatory care development are major catalysts for the India hospital furniture market, with the Indian private hospital industry growing at 12% to 14% annually and the medical tourism sector expanding at 15% to 18%. Hospital furniture is a core procurement category for new hospital builds, ICU additions, OT modernisation, day care centers, and home healthcare programs, with demand driven by Apollo Hospitals, Fortis Healthcare, Manipal Hospitals, Narayana Health, Medanta, and Amrita Hospital expansions. Leading hospital chains have scaled capacity and broadened service portfolios, while medical tourism inflows from the Middle East, Africa, SAARC, and CIS regions reached over 7.3 million visitors in 2024-25. Government healthcare programs combined with formalisation of the ambulatory surgical center segment are structurally expanding India hospital furniture market growth across premium and mass segments through 2032.

Key Market Challenges: India Hospital Furniture Market

High Cost of Advanced Electric and Smart Hospital Furniture Pressuring Public Hospital Penetration

The India hospital furniture market is highly sensitive to price elasticity in its core electric and smart hospital furniture categories, including electric ICU beds, motorised operation tables, electric examination chairs, and IoT-connected medical carts, which together account for 35% to 50% of premium hospital furniture cost and are directly linked to imported motors, actuators, and electronic controllers. Component price movements within a 15% to 30% range over the past 24 months have translated into 18% to 28% swings in landed equipment costs, compressing producer margins and complicating long-term pricing contracts with public hospital procurement and tender authorities. India’s continued dependence on imported motors, actuators, and electronic control systems from China, Germany, Japan, and the US further amplifies this exposure. Leading producers are responding through PLI scheme participation, component localisation, long-term supply contracts, and accelerated electric assembly across the India hospital furniture market.

Heavy Import Dependence for Premium Electric Beds, ICU Furniture, and Specialty Surgical Tables

India remains structurally import-dependent for several premium hospital furniture categories, with over 50% to 60% of high-end electric ICU beds, motorised operation tables, and specialty surgical chairs met through imports from Germany, Japan, the US, China, and South Korea. High-performance categories including electric ICU beds, neonatal warmers, OT tables, and smart connected hospital furniture see similar import intensity. Geopolitical tensions, shipping disruptions, and shifts in global medical device manufacturing capex have exposed Indian hospital procurement teams to supply disruption risk and extended lead times of 8 to 16 weeks. While domestic capacity expansions by Godrej Interio, GPC Medical, PMT Healthcare, Hitech Medicare Devices, and other Make in India players are expected to reduce this dependence materially by 2028 to 2030, supply security remains a near-term strategic challenge in the India hospital furniture market.

Regulatory Compliance Complexity Around CDSCO, BIS Norms, and Biomedical Waste Management

The India hospital furniture market faces rising compliance complexity around CDSCO medical device registration, BIS certification, and biomedical waste management regulations. Hospital furniture manufacturing is increasingly capital and quality-intensive, with stringent CDSCO Medical Device Rules 2017, ISO 13485 certification, and CPCB biomedical waste handling adding 7% to 11% to compliance cost. Export markets such as the EU, US, and the Middle East impose additional requirements including CE marking, FDA 510(k) clearance, and evolving sustainability disclosures. Downstream hospital procurement teams also face tightening NABH, JCI, and infection control mandates that cascade upstream to hospital furniture manufacturers. While these regulations create entry barriers, they also favour organised, integrated, and R&D-led players in the India hospital furniture market.

Key Market Trends: India Hospital Furniture Market

Rapid Adoption of Electric, Smart, and IoT-Enabled Hospital Furniture in India

The India hospital furniture market is undergoing a clear shift toward electric, smart, and IoT-enabled hospital furniture, with connected hospital furniture deployments growing at 13% to 16% annually, significantly outpacing manual mechanical alternatives. Tightening CDSCO norms, NABH and JCI accreditation, infection control mandates, and corporate ESG commitments are reshaping product strategies across hospital beds, OT tables, examination chairs, and medical carts. Smart connected beds with patient monitoring, exit alerts, pressure redistribution, and remote diagnostics are gaining traction as hospitals commit to clinical outcome improvements and lifecycle cost reduction. In 2025, global majors including Hill-Rom (Baxter), Stryker, Paramount Bed, and Midmark launched expanded electric and IoT-connected portfolios for the Indian market, reinforcing the structural shift across the India hospital furniture market.

Capacity Expansion by Global Majors and Domestic Producers in the India Hospital Furniture Market

A wave of domestic capacity expansion and global major investment is reshaping the India hospital furniture market supply landscape. Combined India-focused capital expenditure announcements in hospital furniture manufacturing and ergonomic R&D exceeded USD 400 million across 2023 to 2025. Hill-Rom (Baxter) expanded its India service network, Stryker scaled clinical engineering operations, Paramount Bed strengthened its India presence, and Midmark commissioned new examination furniture capacity. Domestic players including Godrej Interio (Healthcare), GPC Medical, Narang Medical, PMT Healthcare, Hitech Medicare Devices, and Steelcraft (Vissco) expanded electric and ergonomic furniture capacity. Ayushman Bharat-linked supply to new health and wellness centers, PM-ABHIM hospital additions, and downstream private chain capacity additions by Apollo, Fortis, Manipal, Max, Narayana, and Medanta are structurally reinforcing demand growth in the India hospital furniture market.

Rising Role of Ambulatory Surgical Centers, Home Healthcare, and ICU Modernisation in Hospital Furniture Demand

Ambulatory surgical centers, home healthcare, and ICU modernisation are emerging as high-growth pull-through segments for the India hospital furniture market, collectively expected to account for over 32% of total hospital furniture demand by 2032. The Indian ambulatory surgical center market is growing at 14% to 17% annually, while home healthcare is expanding at 18% to 22%, with hospital furniture used extensively in day care procedures, outpatient surgery, post-acute care at home, and ICU upgrades. Leading players including Godrej Interio (Healthcare), Midmark, GPC Medical, Narang Medical, Hill-Rom (Baxter), Stryker, and Paramount Bed have scaled capacity and launched premium electric and smart product ranges. This structural pull-through is reinforcing the India hospital furniture market forecast 2032 across both domestic and export-oriented segments.

Segmental Insights: India Hospital Furniture Market

By Product Type: Hospital Beds Dominate the India Hospital Furniture Market

The hospital beds product segment dominates the India hospital furniture market, accounting for an estimated 38% to 42% of total hospital furniture consumption, driven by strong demand from acute care, ICU, psychiatric, bariatric, and pediatric applications across public and private hospital settings. Electric and motorised hospital beds are the dominant categories within this segment, with smart IoT-connected variants rapidly gaining share. Examination and operation tables contribute another 18% to 22% of demand, while medical carts, trolleys, and stretchers contribute 15% to 18%. In 2025, leading hospital chains including Apollo Hospitals, Fortis Healthcare, Manipal Hospitals, Max Healthcare, and Narayana Health scaled up hospital furniture procurement tied to new capacity additions, reinforcing the segment’s dominance in the India hospital furniture market.

By Material: Metal and Stainless Steel Lead While Composite and Antimicrobial Surfaces Grow Fastest

Metal and stainless steel hospital furniture leads the India hospital furniture market material landscape, accounting for approximately 60% to 65% of total consumption, driven by superior durability, corrosion resistance, ease of disinfection, and antimicrobial compatibility. Plastic and polymer-based hospital furniture contribute another 18% to 22%, followed by composite materials at 8% to 12%, and wood at 5% to 8%. Composite materials, antimicrobial coatings, and stainless steel with antimicrobial properties are the fastest-growing categories within the India hospital furniture market, expanding at 13% to 16% annually, driven by infection control protocols, NABH and JCI mandates, and global hospital sustainability commitments across critical care, operation theatre, and ambulatory care applications.

Regional Insights: India Hospital Furniture Market

Regional analysis of the India hospital furniture market shows that North India and South India collectively account for approximately 56% to 60% of total hospital furniture production and consumption, driven by the concentration of large multi-specialty hospital chains in Delhi NCR, Punjab, Haryana, and Uttar Pradesh, along with strong tertiary care clusters in Bengaluru, Chennai, Hyderabad, and Kochi. West India contributes around 22% to 25% of demand, led by Maharashtra and Gujarat, supported by Mumbai’s private hospital chains, Pune’s health corridor, and growing Ahmedabad medical tourism activity. East and Central India together account for 16% to 19% of demand, supported by West Bengal’s tertiary care hubs and growing healthcare activity in Odisha, Jharkhand, and Madhya Pradesh. In 2025, capacity additions by Godrej Interio in Maharashtra, GPC Medical in Haryana, Hitech Medicare Devices in Punjab, and PMT Healthcare across multiple plants reinforced regional supply hubs, supporting closer collaboration with hospital procurement, group purchasing organisations, and tender authorities across the India hospital furniture market.

Recent Developments: India Hospital Furniture Market

- The India hospital furniture market has witnessed strong momentum in capacity expansion and electric ergonomic product innovation during 2024 and 2025. Hill-Rom (Baxter) expanded its India service network, Stryker scaled clinical engineering operations, Paramount Bed strengthened its India product portfolio, and Midmark commissioned new examination furniture capacity. Domestic players including Godrej Interio (Healthcare), GPC Medical, Narang Medical, PMT Healthcare, Hitech Medicare Devices, and Steelcraft (Vissco) announced capacity additions for electric and smart hospital furniture, reinforcing India as a globally competitive hospital furniture manufacturing hub.

- Downstream hospital chains have deepened India sourcing of hospital furniture, with Apollo Hospitals, Fortis Healthcare, Manipal Hospitals, Max Healthcare, Narayana Health, and Medanta scaling long-term supply contracts with domestic and global hospital furniture producers in 2025. New hospital builds including the 2,400-bed Amrita Hospital in Faridabad, AIIMS expansions, and PM-ABHIM-funded health and wellness centers commissioned major capacity, driving further structural hospital furniture demand. Ambulatory surgical center and home healthcare operators including Portea, HealthCare atHome, and Apollo Homecare also expanded capacity and broadened electric and smart product ranges, reinforcing downstream linkage across the India hospital furniture market.

- Sustainability-led innovation has gained strong traction in the India hospital furniture market. In 2025, global majors including Hill-Rom (Baxter), Stryker, Paramount Bed, and Midmark launched expanded electric, smart connected, and antimicrobial-coated hospital furniture portfolios targeted at Indian hospital chain and tertiary care customers. The May 2023 launch of the National Medical Device Policy aiming to grow the medical device sector to USD 50 billion by 2030, combined with PLI scheme allocations and Make in India incentives, is positioning India as an emerging hub for sustainable hospital furniture manufacturing, strengthening long-term competitive positioning in the India hospital furniture market forecast 2032.

Key Market Players: India Hospital Furniture Market

- Godrej Interio (Healthcare Furniture Division)

- Midmark India Pvt. Ltd. (Janak Healthcare)

- GPC Medical Limited

- Narang Medical Limited

- PMT Healthcare Pvt. Ltd.

- Hitech Medicare Devices Pvt. Ltd.

- Surgitech India

- Steelcraft Hospital Furniture Industries (Vissco)

- Carevel Medical Systems Pvt. Ltd.

- Stryker India Pvt. Ltd.

- Hill-Rom India (Baxter)

- Paramount Bed India Pvt. Ltd.

- Nilkamal Limited (Healthcare)

- Wipro Furniture Limited

- Medline India Pvt. Ltd.

Report Scope

In this report, the India Hospital Furniture Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Hospital Beds (Acute Care, ICU, Psychiatric, Bariatric, Pediatric)

- Examination & Operation Tables (Surgical, Examination, Delivery)

- Hospital Chairs (Manual, Electric, Blood Donor, Dental)

- Medical Carts & Trolleys

- Stretchers

- Bedside Tables, Cabinets & Lockers

- Instrument Stands & Stools

- Over-Bed Tables

- Others

- By Material

- Metal / Stainless Steel

- Plastic / Polymer

- Wood

- Composite Materials

- By Technology

- Manual Hospital Furniture

- Electric / Electronic Hospital Furniture

- Smart / IoT-Enabled Hospital Furniture

- By End-User

- Public / Government Hospitals

- Private Hospitals & Multi-Specialty Chains

- Clinics & Day Care Centers

- Ambulatory Surgical Centers

- Diagnostic Centers

- Home Healthcare

- Others

- By Sales Channel

- Direct Tenders / Government Procurement

- Distributors & Medical Equipment Agents

- Online / B2B Platforms

- OEM Contracts

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Hospital Furniture Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic hospital furniture producers, electric and smart furniture specialists, global entrants, or niche segment leaders.

The India Hospital Furniture Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Material

- By Technology

- By End-User

- By Sales Channel

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Hospital Furniture Market

- India Hospital Furniture Market Insights

- Market Dynamics

- Growth Drivers

- Rapid expansion of healthcare infrastructure in tier-2 and tier-3 cities driving core hospital furniture consumption.

- Structural shift toward electric, smart, and IoT-enabled hospital furniture driven by modern critical care and ergonomic norms.

- Accelerated private hospital chain expansion, medical tourism growth, and ambulatory surgical center demand for hospital furniture.

- Restraints

- High cost of advanced electric and smart hospital furniture pressuring penetration in price-sensitive public hospital segment.

- Heavy import dependence for premium electric beds, ICU furniture, and specialty surgical tables creating supply risk.

- Regulatory compliance complexity around BIS, CDSCO medical device norms, and biomedical waste management raising compliance costs.

- Opportunities

- Rapid scale-up of ICU beds, electric ergonomic furniture, and smart connected medical furniture aligned with critical care expansion.

- High-growth demand from private hospital chains, ambulatory surgical centers, and home healthcare supporting healthcare build-out.

- Emerging export opportunity for India-manufactured hospital furniture to Middle East, Southeast Asia, and African markets with growing healthcare industries.

- Challenges

- Intense price-led competition between domestic hospital furniture producers and Chinese imports compressing margins.

- Fragmented distribution network and tender-driven public procurement cycles limiting predictable revenue and pricing power.

- Shortage of skilled metal fabricators, electric assembly technicians, and ergonomic designers limiting scale-up speed of new capacity.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Raw Material Suppliers (steel, stainless steel, aluminum, polymer, wood, composite materials)

- Component Producers (motors, actuators, casters, hydraulics, electronic controllers, IV poles)

- Antimicrobial Coatings & Surface Treatment Providers (powder coating, electroplating, ecolabels)

- Hospital Furniture OEMs & Assembly Operations (welding, fabrication, ergonomic engineering, electric assembly)

- Quality Control, R&D & Application Laboratories (BIS, CDSCO, ISO 13485, biomedical waste norms)

- Distributors, Medical Equipment Agents & B2B Marketplaces

- Downstream Healthcare Procurement (hospital purchase departments, group purchasing organisations, tenders)

- Healthcare Brand Owners & Hospital Chains (Apollo, Fortis, Manipal, AIIMS, Max, Narayana, Medanta)

- Installation & Service Channels (commissioning, AMC providers, technicians, repair networks)

- End-Use Segments (public hospitals, private hospitals, ASCs, clinics, diagnostic centers, home healthcare)

- India Hospital Furniture Market: Regulatory Framework

- India Hospital Furniture Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (‘000 Units)

- Market Share & Forecast

- By Product Type

- Hospital Beds (Acute Care, ICU, Psychiatric, Bariatric, Pediatric)

- Examination & Operation Tables (Surgical, Examination, Delivery)

- Hospital Chairs (Manual, Electric, Blood Donor, Dental)

- Medical Carts & Trolleys

- Stretchers

- Bedside Tables, Cabinets & Lockers

- Instrument Stands & Stools

- Over-Bed Tables

- Others

- By Material

- Metal / Stainless Steel

- Plastic / Polymer

- Wood

- Composite Materials

- By Technology

- Manual Hospital Furniture

- Electric / Electronic Hospital Furniture

- Smart / IoT-Enabled Hospital Furniture

- By End-User

- Public / Government Hospitals

- Private Hospitals & Multi-Specialty Chains

- Clinics & Day Care Centers

- Ambulatory Surgical Centers

- Diagnostic Centers

- Home Healthcare

- Others

- By Sales Channel

- Direct Tenders / Government Procurement

- Distributors & Medical Equipment Agents

- Online / B2B Platforms

- OEM Contracts

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Hospital Furniture Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Godrej Interio (Healthcare Furniture Division)

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Godrej Interio (Healthcare Furniture Division)

- Market Size & Forecast, 2021-2032

*(Same Data Pointers Will Be Provided for The Below Companies)

- Midmark India Pvt. Ltd. (Janak Healthcare)

- GPC Medical Limited

- Narang Medical Limited

- PMT Healthcare Pvt. Ltd.

- Hitech Medicare Devices Pvt. Ltd.

- Surgitech India

- Steelcraft Hospital Furniture Industries (Vissco)

- Carevel Medical Systems Pvt. Ltd.

- Stryker India Pvt. Ltd.

- Hill-Rom India (Baxter)

- Paramount Bed India Pvt. Ltd.

- Nilkamal Limited (Healthcare)

- Wipro Furniture Limited

- Medline India Pvt. Ltd.

- Other Prominent Players

** Financial information in case of non-listed companies will be provided as per availability*

*** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable*

Frequently Asked Questions

1. How large is the India hospital furniture market and what is its growth forecast?

Ans: The India hospital furniture market size is valued at USD 413.7 million in 2025 and is projected to reach USD 821.6 million by 2032, growing at a CAGR of around 10.3%. This strong India hospital furniture market growth is driven by accelerated healthcare infrastructure development, rising private hospital chain investments, structural shift toward electric and smart hospital furniture, and major domestic and global capacity expansions. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India hospital furniture market?

Ans: The India hospital furniture market segmentation shows that hospital beds dominate with approximately 38% to 42% share, followed by examination and operation tables at 18% to 22% and medical carts, trolleys, and stretchers at 15% to 18%. Metal and stainless steel lead by material with 60% to 65% share, while electric and smart IoT-enabled hospital furniture is the fastest-growing segment, expanding at 13% to 16% annually. The report breaks down demand across product types, materials, technologies, end-users, and sales channels, helping businesses understand where growth is accelerating across the India hospital furniture market.

3. What are the key drivers of growth in the India hospital furniture market?

Ans: Key India hospital furniture market drivers include rapid expansion of Indian healthcare infrastructure growing at 11% to 13% annually under Ayushman Bharat and PM-ABHIM, structural shift toward electric and smart IoT-enabled hospital furniture driven by NABH and JCI accreditation norms, and accelerated private hospital chain expansion, medical tourism, and ambulatory surgical center demand. Global hospital furniture majors such as Hill-Rom (Baxter), Stryker, Paramount Bed, and Midmark are investing in India-specific manufacturing capacity and clinical engineering laboratories. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends shaping the India hospital furniture market.

4. Which regions are driving growth in the India hospital furniture market?

Ans: Regional analysis of the India hospital furniture market shows that North and South India together account for nearly 56% to 60% of total demand, driven by large multi-specialty hospital chains in Delhi NCR, Punjab, Haryana, and Uttar Pradesh, along with strong tertiary care clusters in Bengaluru, Chennai, Hyderabad, and Kochi. West India contributes around 22% to 25%, supported by Maharashtra and Gujarat private hospital chains and medical tourism activity. East and Central India together account for 16% to 19%, supported by West Bengal’s tertiary care hubs and growing healthcare activity. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India hospital furniture market?

Ans: Recent trends in the India hospital furniture market include rapid adoption of electric, smart, and IoT-enabled hospital furniture growing at 13% to 16% annually, capacity expansion by global majors and domestic producers, rising role of ambulatory surgical centers, home healthcare, and ICU modernisation, and accelerated launches by Hill-Rom (Baxter), Stryker, Paramount Bed, and Midmark. Sustainability-led innovation, antimicrobial-coated surfaces, and ergonomic patient-centric design are reshaping product strategies. The report covers latest product launches, partnerships, capacity expansions, and competitive moves shaping the long-term India hospital furniture market forecast 2032.

Frequently Asked Questions

1. How large is the India hospital furniture market and what is its growth forecast?

Ans: The India hospital furniture market size is valued at USD 413.7 million in 2025 and is projected to reach USD 821.6 million by 2032, growing at a CAGR of around 10.3%. This strong India hospital furniture market growth is driven by accelerated healthcare infrastructure development, rising private hospital chain investments, structural shift toward electric and smart hospital furniture, and major domestic and global capacity expansions. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India hospital furniture market?

Ans: The India hospital furniture market segmentation shows that hospital beds dominate with approximately 38% to 42% share, followed by examination and operation tables at 18% to 22% and medical carts, trolleys, and stretchers at 15% to 18%. Metal and stainless steel lead by material with 60% to 65% share, while electric and smart IoT-enabled hospital furniture is the fastest-growing segment, expanding at 13% to 16% annually. The report breaks down demand across product types, materials, technologies, end-users, and sales channels, helping businesses understand where growth is accelerating across the India hospital furniture market.

3. What are the key drivers of growth in the India hospital furniture market?

Ans: Key India hospital furniture market drivers include rapid expansion of Indian healthcare infrastructure growing at 11% to 13% annually under Ayushman Bharat and PM-ABHIM, structural shift toward electric and smart IoT-enabled hospital furniture driven by NABH and JCI accreditation norms, and accelerated private hospital chain expansion, medical tourism, and ambulatory surgical center demand. Global hospital furniture majors such as Hill-Rom (Baxter), Stryker, Paramount Bed, and Midmark are investing in India-specific manufacturing capacity and clinical engineering laboratories. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends shaping the India hospital furniture market.

4. Which regions are driving growth in the India hospital furniture market?

Ans: Regional analysis of the India hospital furniture market shows that North and South India together account for nearly 56% to 60% of total demand, driven by large multi-specialty hospital chains in Delhi NCR, Punjab, Haryana, and Uttar Pradesh, along with strong tertiary care clusters in Bengaluru, Chennai, Hyderabad, and Kochi. West India contributes around 22% to 25%, supported by Maharashtra and Gujarat private hospital chains and medical tourism activity. East and Central India together account for 16% to 19%, supported by West Bengal’s tertiary care hubs and growing healthcare activity. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India hospital furniture market?

Ans: Recent trends in the India hospital furniture market include rapid adoption of electric, smart, and IoT-enabled hospital furniture growing at 13% to 16% annually, capacity expansion by global majors and domestic producers, rising role of ambulatory surgical centers, home healthcare, and ICU modernisation, and accelerated launches by Hill-Rom (Baxter), Stryker, Paramount Bed, and Midmark. Sustainability-led innovation, antimicrobial-coated surfaces, and ergonomic patient-centric design are reshaping product strategies. The report covers latest product launches, partnerships, capacity expansions, and competitive moves shaping the long-term India hospital furniture market forecast 2032.