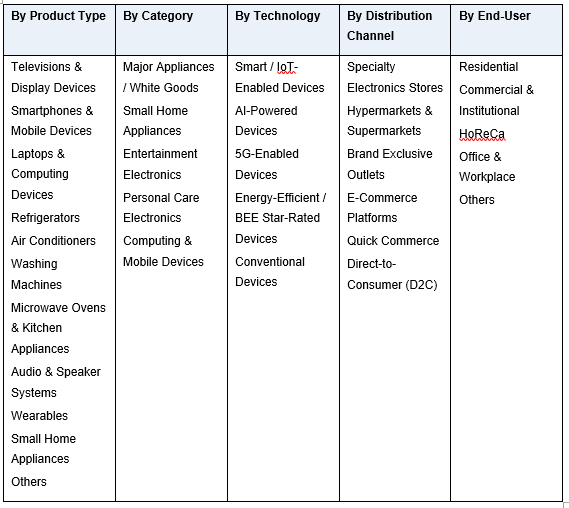

India Consumer Electronics and Appliances Market, By Product Type (Televisions & Display Devices, Smartphones & Mobile Devices, Laptops & Computing Devices, Refrigerators, Air Conditioners, Washing Machines, Microwave Ovens & Kitchen Appliances, Audio & Speaker Systems, Wearables (Smartwatches, Earbuds, Headphones), Small Home Appliances, Others); By Category (Major Appliances / White Goods, Small Home Appliances, Entertainment Electronics, Personal Care Electronics, Computing & Mobile Devices); By Technology (Smart / IoT-Enabled Devices, AI-Powered Devices, 5G-Enabled Devices, Energy-Efficient / BEE Star-Rated Devices, Conventional Devices); By Price Range (Premium, Mid-Range, Entry-Level / Mass); By Distribution Channel (Specialty Electronics Stores, Hypermarkets & Supermarkets, Brand Exclusive Outlets, E-Commerce Platforms, Quick Commerce, Direct-to-Consumer (D2C)); By End-User (Residential, Commercial & Institutional, HoReCa, Office & Workplace, Others); By Trend Analysis, Competitive Landscape & Forecast, 2021 to 2032

- Consumer Goods & Retail

- May 2026

- Pages 130

- Report Format: pdf

- Report Price: $1800 USD

India Consumer Electronics and Appliances Market: Smart, Connected & Premium Device Shift Powers Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

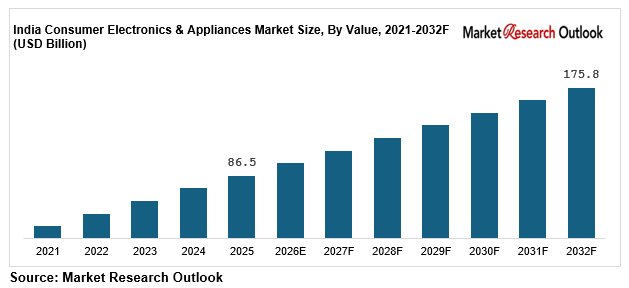

| Market Size (2025) | USD 86.5 Billion |

| CAGR (2026-2032) | 10.7% |

| Leading Segment | Major Appliances / White Goods |

| Fastest Growing Segment | Smart / IoT-Enabled & AI-Powered Devices |

| Market Size (2032) | USD 175.8 Billion |

Source: Market Research Outlook

Market Overview: India Consumer Electronics and Appliances Market

The India consumer electronics and appliances market size is witnessing rapid expansion, driven by accelerated disposable income growth, rising urbanisation and tier-2 and tier-3 city affluence, the structural shift toward smart, IoT-enabled, and energy-efficient devices, and major capacity expansions by global and domestic consumer electronics and appliances producers. Valued at USD 86.5 billion in 2025 and projected to reach USD 175.8 billion by 2032, growing at a CAGR of 10.7%, the India consumer electronics and appliances market growth is being fuelled by strong demand from residential households, commercial and institutional buyers, HoReCa operators, and office and workplace deployments. Major appliances and white goods lead consumption, while smart, IoT-enabled, and AI-powered devices are emerging as the fastest-growing segment. Tightening BIS Quality Control Order 2025, BEE star-rating norms, GST rate cuts on televisions above 32 inches, and corporate ESG commitments are reshaping the supply landscape. As global majors including Samsung, LG, Sony, Panasonic, and Whirlpool expand India-specific manufacturing capacity and domestic players including Voltas, Godrej Appliances, Havells India, Bajaj Electricals, and Blue Star scale premium and connected appliance capacity, the India consumer electronics and appliances market is evolving into a premium, connected, and consumer-experience-led ecosystem with strong long-term growth potential.

Key Report Takeaways: India Consumer Electronics and Appliances Market

- The India consumer electronics and appliances market size is projected to grow from USD 86.5 billion in 2025 to USD 175.8 billion by 2032, registering a strong CAGR of 10.7%, driven by accelerated disposable income growth, premiumisation, and the structural shift toward smart and energy-efficient devices.

- Major appliances and white goods dominate the India consumer electronics and appliances market, accounting for over 42% of total demand, driven by strong adoption across refrigerators, air conditioners, washing machines, and microwave ovens in residential and commercial segments.

- Smart, IoT-enabled, and AI-powered devices are emerging as the fastest-growing segment in the India consumer electronics and appliances market, expected to grow at 14% to 17% annually as connectivity, energy efficiency, and consumer experience expectations reshape product strategies.

- Accelerated growth of the Indian consumer durables industry, led by Samsung, LG, Sony, Panasonic, Whirlpool, and Voltas, along with new premium entrants including Bosch (BSH Home Appliances), Apple, and Xiaomi, is structurally expanding demand across major and small appliance categories.

- Rising investments by global consumer electronics majors such as Samsung, LG, Sony, Apple, Xiaomi, and Bosch in India-specific manufacturing capacity, R&D centers, and component localisation under PLI scheme are strengthening local innovation and supporting the India consumer electronics and appliances market forecast 2032.

Key Market Drivers: India Consumer Electronics and Appliances Market

Rising Disposable Income, Urbanisation, and Tier-2 and Tier-3 City Affluence Driving Consumer Durables Penetration

Growth in the India consumer electronics and appliances market is being driven by the rapid expansion of Indian household disposable income, growing at 9% to 11% annually, significantly outpacing most other emerging markets. Tier-2 and tier-3 city consumers account for approximately 45% of the Indian consumer durables industry, with average monthly spending on consumer durables soaring by 72% in FY25 according to the CMS Consumption Report 2025. Per-capita appliance penetration in India currently stands at around 35% to 40% for refrigerators and 8% to 10% for air conditioners, compared to 80% to 90% in developed markets, indicating significant long-term headroom for growth. Major consumer electronics companies including Samsung, LG, Sony, Panasonic, and Voltas, along with new premium entrants Apple, Xiaomi, and BSH Home Appliances (Bosch), have announced combined capacity expansions exceeding USD 5 billion, creating strong structural pull-through demand for premium and connected consumer electronics and appliances across the India consumer electronics and appliances market.

Make in India and PLI Scheme Accelerating Local Manufacturing and Reducing Import Dependence

The India consumer electronics and appliances market is witnessing a strong and accelerating shift toward localised manufacturing under the Make in India initiative and Production Linked Incentive (PLI) scheme, with locally manufactured consumer electronics output growing at 18% to 22% annually, nearly twice the pace of overall market growth. Tightening BIS Quality Control Order 2025 standards, the National Policy on Electronics 2019 targets of USD 300 billion electronics manufacturing by FY26, and corporate ESG mandates are reshaping sourcing strategies across televisions, smartphones, refrigerators, air conditioners, and washing machines. India-manufactured consumer electronics typically deliver 12% to 18% lower landed cost compared to imported alternatives, making them the preferred choice for entry-level and mid-range product launches. Global majors including Samsung, LG, and Sony have launched expanded India-specific manufacturing operations in 2024 and 2025, while domestic players are parallelly scaling component and assembly capacity, reinforcing this structural trend across the India consumer electronics and appliances market.

Accelerated Adoption of Smart, IoT-Enabled, and Energy-Efficient Devices Across Smartphones, Televisions, and Appliances

Rapid digitalisation, smart home adoption, and rising consumer awareness on energy efficiency are major catalysts for the India consumer electronics and appliances market, with the Indian smart appliances market growing at 15% to 18% annually and the BEE 5-star rated appliances category expanding at 14% to 16%. Smart and IoT-enabled devices are core enablers for connected homes, smart kitchens, voice-controlled environments, and energy-efficient consumption, with demand driven by metro and tier-1 city households, rising 5G smartphone penetration, Smart Cities Mission, and expanding e-commerce-led discovery. Leading brands such as Samsung (Bespoke AI series), LG (ThinQ smart appliances), Voltas (inverter ACs), Godrej Appliances, and Whirlpool have scaled premium product portfolios. Government initiatives combined with formalisation of after-sales service are structurally expanding India consumer electronics and appliances market growth across premium and mass segments through 2032.

Key Market Challenges: India Consumer Electronics and Appliances Market

High Import Dependence for Semiconductors, Display Panels, and Key Components Linked to Global Supply Chain Disruptions

The India consumer electronics and appliances market is highly sensitive to import dependence in its core component categories, including semiconductors, display panels, lithium-ion batteries, compressors, and motors, which together account for 55% to 70% of consumer electronics input cost and are directly linked to global supply chain dynamics. Component price movements within a 15% to 30% range over the past 24 months have translated into 10% to 18% swings in landed product costs, compressing OEM margins and complicating long-term pricing contracts with retailers and channel partners. India’s continued dependence on imported semiconductors, OLED and LCD panels, and specialty electronic components from China, South Korea, Taiwan, Japan, and Vietnam further amplifies this exposure. Leading producers are responding through PLI scheme participation, component localisation, long-term supply contracts, and accelerated India-specific R&D across the India consumer electronics and appliances market.

Counterfeit Products, Grey Market Imports, and Unorganised Retail Fragmentation Pressuring Brand Margins

India remains structurally exposed to counterfeit products, grey market imports, and unorganised retail fragmentation across several consumer electronics and appliances categories, with over 25% to 35% of small appliances, accessories, and entry-level mobile devices market reportedly affected by unauthorised imports and counterfeits. High-volume categories including chargers, audio accessories, smartphone parts, and small kitchen appliances see similar vulnerability. Geopolitical tensions, port enforcement gaps, and shifts in global manufacturing capex have exposed Indian consumer electronics brand owners to brand dilution risk and channel arbitrage pressure of 8% to 15% on margins. While GST formalisation, BIS QCO 2025, and e-commerce platform compliance enforcement by Daalchini, Amazon, Flipkart, and Reliance Digital are expected to reduce this dependence materially by 2028 to 2030, channel integrity remains a near-term strategic challenge in the India consumer electronics and appliances market.

Compliance Complexity Around BIS, BEE Energy Efficiency, and Tightening E-Waste Norms

The India consumer electronics and appliances market faces rising compliance complexity around BIS QCO 2025 certification, BEE star-rating efficiency norms, and electronic waste management regulations. Consumer electronics and appliances manufacturing is increasingly capital and energy-intensive, with stringent CPCB standards around e-waste handling, Extended Producer Responsibility (EPR) mandates, and packaging waste norms adding 5% to 9% to compliance cost. Export markets such as the EU, US, and the Middle East impose additional requirements including CE marking, FCC certification, and evolving sustainability disclosures under CSRD and CBAM. Downstream retailers and e-commerce platforms also face tightening right-to-repair mandates and consumer protection norms that cascade upstream to OEMs. While these regulations create entry barriers, they also favour organised, integrated, and R&D-led players in the India consumer electronics and appliances market.

Key Market Trends: India Consumer Electronics and Appliances Market

Rapid Adoption of Smart, IoT-Enabled, and AI-Powered Consumer Electronics and Appliances in India

The India consumer electronics and appliances market is undergoing a clear shift toward smart, IoT-enabled, and AI-powered devices, with connected appliance and smart electronics deployments growing at 14% to 17% annually, significantly outpacing conventional alternatives. Expanding 5G penetration, Smart Cities Mission rollout, BEE star-rating norms, and corporate ESG commitments are reshaping product strategies across televisions, smartphones, refrigerators, air conditioners, and wearables. AI-driven personalisation, predictive maintenance, and connected ecosystems are gaining traction as consumers commit to smart home experiences and lifestyle premiumisation. In 2025, global majors including Samsung (Bespoke AI), LG (ThinQ), Sony, Panasonic, and Whirlpool launched expanded smart and AI-enabled portfolios for the Indian market, reinforcing the structural shift across the India consumer electronics and appliances market.

Capacity Expansion by Global Majors and Domestic Producers in the India Consumer Electronics and Appliances Market

A wave of domestic capacity expansion and global major investment is reshaping the India consumer electronics and appliances market supply landscape. Combined India-focused capital expenditure announcements in consumer electronics manufacturing exceeded USD 7 billion across 2023 to 2025. LG Electronics announced a USD 600 million third manufacturing plant in Sri City, Andhra Pradesh, Samsung expanded its Noida and Sriperumbudur facilities, Apple scaled iPhone manufacturing through Foxconn and Tata Electronics partnerships, and Bosch (BSH Home Appliances) commissioned new appliance capacity. Domestic players including Voltas, Godrej Appliances, Havells India, Bajaj Electricals, IFB Industries, and Blue Star expanded white goods and small appliance capacity. PLI scheme-linked supply to new manufacturing clusters and downstream retail capacity additions by Croma, Reliance Digital, Vijay Sales, Amazon India, and Flipkart are structurally reinforcing demand growth in the India consumer electronics and appliances market.

Rising Role of Premium Televisions, Air Conditioners, and Wearables in Consumer Electronics Demand

Premium televisions above 32 inches, inverter-based air conditioners, and smart wearables are emerging as high-growth pull-through segments for the India consumer electronics and appliances market, collectively expected to account for over 38% of total consumer electronics demand by 2032. The Indian air conditioner market is growing at 20% to 25% annually following the September 2025 GST rate cut on televisions above 32 inches from 28% to 18%, while smartwatches and wearables are expanding at 16% to 20%, with smart and IoT features used extensively in fitness tracking, health monitoring, and connected lifestyle applications. Leading players including Samsung, LG, Sony, Voltas, Bajaj Electricals, Boat, Noise, and Apple have scaled capacity and launched premium product ranges. This structural pull-through is reinforcing the India consumer electronics and appliances market forecast 2032 across both domestic and export-oriented segments.

Segmental Insights: India Consumer Electronics and Appliances Market

By Category: Major Appliances / White Goods Dominate the India Consumer Electronics and Appliances Market

The major appliances and white goods category dominates the India consumer electronics and appliances market, accounting for an estimated 42% to 45% of total consumer electronics and appliances consumption, driven by strong demand from refrigerators, air conditioners, washing machines, and microwave ovens in residential and commercial segments. Inverter-based and BEE 5-star energy-efficient appliances are the dominant categories within this segment, with smart and IoT-enabled products rapidly gaining share. Entertainment electronics including televisions and audio systems contribute another 24% to 27% of demand, while computing and mobile devices including smartphones and laptops contribute 22% to 25%. In 2025, leading appliance companies including Samsung, LG, Voltas, Godrej, and Whirlpool scaled up production tied to new capacity additions, reinforcing the segment’s dominance in the India consumer electronics and appliances market.

By Product Type: Refrigerators and Air Conditioners Lead While Smart Wearables and AI Devices Grow Fastest

Refrigerators and air conditioners lead the India consumer electronics and appliances market product landscape, accounting for approximately 28% to 32% of total consumption combined, driven by their high household penetration, urbanisation-led demand, and compatibility with smart and energy-efficient formats. Smartphones contribute another 22% to 24%, followed by televisions at 14% to 16%, and washing machines at 10% to 12%. Smart wearables, AI-powered devices, and 5G-enabled smartphones are the fastest-growing categories within the India consumer electronics and appliances market, expanding at 14% to 17% annually, driven by digital adoption, premiumisation, and global lifestyle commitments across health, fitness, and connected home applications.

Regional Insights: India Consumer Electronics and Appliances Market

Regional analysis of the India consumer electronics and appliances market shows that North India and West India collectively account for approximately 54% to 58% of total consumer electronics and appliances production and consumption, driven by the concentration of manufacturing clusters in Noida, Sri City, Pune, Aurangabad, and Sanand, along with strong urban consumption hubs in Delhi NCR, Mumbai, Pune, and Ahmedabad. South India contributes around 24% to 27% of demand, led by Bengaluru, Chennai, and Hyderabad, supported by IT-sector affluence, early adoption of smart appliances, and expanding manufacturing in Sri City and Sriperumbudur. East and Central India together account for 16% to 20% of demand, supported by West Bengal’s urban demand and growing consumer activity in Odisha, Jharkhand, and Madhya Pradesh. In 2025, capacity additions by LG in Andhra Pradesh, Samsung in Uttar Pradesh and Tamil Nadu, Bosch (BSH) in Maharashtra, and Apple/Foxconn in Tamil Nadu and Karnataka reinforced regional supply hubs, supporting closer collaboration with retailers and channel partners across the India consumer electronics and appliances market.

Recent Developments: India Consumer Electronics and Appliances Market

- The India consumer electronics and appliances market has witnessed strong momentum in capacity expansion and smart product innovation during 2024 and 2025. LG Electronics announced a USD 600 million investment in its third manufacturing plant in Sri City, Andhra Pradesh, Samsung introduced its Bespoke AI series of air conditioners and refrigerators with AI algorithms optimised for local power supply, BSH Home Appliances launched its XXL Top Freezer Refrigerator range, and Apple scaled iPhone manufacturing through Foxconn and Tata Electronics. Domestic players including Voltas, Godrej Appliances, Havells India, and Bajaj Electricals announced capacity additions for premium and connected appliances, reinforcing India as a globally competitive consumer electronics manufacturing hub.

- Downstream retail and e-commerce platforms have deepened India sourcing of consumer electronics and appliances, with Croma (Tata), Reliance Digital, Vijay Sales, Amazon India, and Flipkart scaling long-term supply contracts with domestic and global OEMs in 2025. New entrants and Indian D2C brands including Boat, Noise, Atomberg, and Mivi commissioned major capacity, driving further structural consumer electronics demand. Quick commerce and omnichannel retailers including BigBasket, Blinkit, and Tata Cliq also expanded electronics and small appliance ranges, reinforcing downstream linkage across the India consumer electronics and appliances market.

- Sustainability-led innovation has gained strong traction in the India consumer electronics and appliances market. In September 2025, the GST Council reduced the GST rate on televisions above 32 inches from 28% to 18%, sparking 30% to 35% sales growth on the first day of the new GST rate. In January 2025, the government enforced The Safety of Household, Commercial and Similar Electrical Appliances (Quality Control) Order-QCO 2025, mandating stricter BIS certification. In 2025, global majors including Samsung, LG, Sony, Panasonic, and Bosch launched expanded BEE 5-star, energy-efficient, and AI-enabled product portfolios, strengthening long-term competitive positioning in the India consumer electronics and appliances market forecast 2032.

Key Market Players: India Consumer Electronics and Appliances Market

- Samsung India Electronics Pvt. Ltd.

- LG Electronics India Pvt. Ltd.

- Sony India Pvt. Ltd.

- Panasonic Life Solutions India Pvt. Ltd.

- Voltas Limited

- Whirlpool of India Limited

- Haier Appliances India Pvt. Ltd.

- Godrej Appliances (Godrej Enterprises Group)

- Bajaj Electricals Limited

- Havells India Limited

- Blue Star Limited

- IFB Industries Limited

- Xiaomi Technology India Pvt. Ltd.

- Apple India Pvt. Ltd.

- BSH Home Appliances India (Bosch)

Report Scope

In this report, the India Consumer Electronics and Appliances Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Televisions & Display Devices

- Smartphones & Mobile Devices

- Laptops & Computing Devices

- Refrigerators

- Air Conditioners

- Washing Machines

- Microwave Ovens & Kitchen Appliances

- Audio & Speaker Systems

- Wearables (Smartwatches, Earbuds, Headphones)

- Small Home Appliances

- Others

- By Category

- Major Appliances / White Goods

- Small Home Appliances

- Entertainment Electronics

- Personal Care Electronics

- Computing & Mobile Devices

- By Technology

- Smart / IoT-Enabled Devices

- AI-Powered Devices

- 5G-Enabled Devices

- Energy-Efficient / BEE Star-Rated Devices

- Conventional Devices

- By Price Range

- Premium

- Mid-Range

- Entry-Level / Mass

- By Distribution Channel

- Specialty Electronics Stores

- Hypermarkets & Supermarkets

- Brand Exclusive Outlets

- E-Commerce Platforms

- Quick Commerce

- Direct-to-Consumer (D2C)

- By End-User

- Residential

- Commercial & Institutional

- HoReCa

- Office & Workplace

- Others

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Consumer Electronics and Appliances Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic consumer electronics producers, premium appliance specialists, global entrants, or niche segment leaders.

The India Consumer Electronics and Appliances Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Category

- By Technology

- By Price Range

- By Distribution Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Consumer Electronics and Appliances Market

- India Consumer Electronics and Appliances Market Insights

- Market Dynamics

- Growth Drivers

- Rising disposable income, urbanisation, and tier-2 and tier-3 city affluence driving consumer durables penetration.

- Make in India and Production Linked Incentive (PLI) scheme accelerating local manufacturing and reducing import dependence.

- Accelerated adoption of smart, IoT-enabled, and energy-efficient devices across smartphones, televisions, and home appliances.

- Restraints

- High import dependence for semiconductors, display panels, and key components linked to global supply chain disruptions.

- Counterfeit products, grey market imports, and unorganised retail fragmentation pressuring brand margins.

- Compliance complexity around BIS certification, BEE energy efficiency norms, and e-waste management regulations raising compliance cost.

- Opportunities

- Rapid scale-up of premium televisions, refrigerators, air conditioners, and smart wearables driven by GST rate cuts and EMI affordability.

- High-growth demand from D2C, e-commerce, and quick commerce platforms across tier-2 and tier-3 city consumers.

- Emerging export opportunity for India-manufactured consumer electronics and appliances to Middle East, Africa, and Southeast Asian markets.

- Challenges

- Intense price-led competition between global majors, Chinese brands, and domestic producers compressing margins.

- After-sales service network gaps, right-to-repair compliance burden, and skilled technician shortage limiting customer lifecycle value.

- Rapid technology obsolescence and short product lifecycles raising inventory risk and channel write-down exposure.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Component Suppliers (semiconductors, display panels, batteries, compressors, motors)

- Electronic Component Producers (PCBs, sensors, ICs, connectors, power modules)

- Software & AI Platform Providers (operating systems, IoT firmware, AI assistants, smart home platforms)

- Consumer Electronics & Appliances OEMs & Assembly Operations (TVs, smartphones, refrigerators, washing machines, ACs)

- Quality Control, R&D & Application Laboratories (BIS, BEE star ratings, e-waste norms, ecolabels)

- Distributors, National Distributors & B2B Marketplaces

- Retailers & Distribution Channels (specialty stores, hypermarkets, brand outlets, e-commerce, quick commerce)

- Brand Owners & Manufacturers (Samsung, LG, Sony, Panasonic, Voltas, Godrej, Havells, Whirlpool, Haier, Bajaj)

- Installation & Service Channels (technicians, after-sales centers, AMC providers, right-to-repair networks)

- End-Use Segments (residential, commercial, institutional, HoReCa, office and workplace)

- India Consumer Electronics and Appliances Market: Regulatory Framework

- India Consumer Electronics and Appliances Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- By Volume (Million Units)

- Market Share & Forecast

- By Product Type

- Televisions & Display Devices

- Smartphones & Mobile Devices

- Laptops & Computing Devices

- Refrigerators

- Air Conditioners

- Washing Machines

- Microwave Ovens & Kitchen Appliances

- Audio & Speaker Systems

- Wearables (Smartwatches, Earbuds, Headphones)

- Small Home Appliances

- Others

- By Category

- Major Appliances / White Goods

- Small Home Appliances

- Entertainment Electronics

- Personal Care Electronics

- Computing & Mobile Devices

- By Technology

- Smart / IoT-Enabled Devices

- AI-Powered Devices

- 5G-Enabled Devices

- Energy-Efficient / BEE Star-Rated Devices

- Conventional Devices

- By Price Range

- Premium

- Mid-Range

- Entry-Level / Mass

- By Distribution Channel

- Specialty Electronics Stores

- Hypermarkets & Supermarkets

- Brand Exclusive Outlets

- E-Commerce Platforms

- Quick Commerce

- Direct-to-Consumer (D2C)

- By End-User

- Residential

- Commercial & Institutional

- HoReCa

- Office & Workplace

- Others

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Consumer Electronics and Appliances Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Samsung India Electronics Pvt. Ltd.

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Samsung India Electronics Pvt. Ltd.

- Market Size & Forecast, 2021-2032

*(Same Data Pointers Will Be Provided for The Below Companies)

- LG Electronics India Pvt. Ltd.

- Sony India Pvt. Ltd.

- Panasonic Life Solutions India Pvt. Ltd.

- Voltas Limited

- Whirlpool of India Limited

- Haier Appliances India Pvt. Ltd.

- Godrej Appliances (Godrej Enterprises Group)

- Bajaj Electricals Limited

- Havells India Limited

- Blue Star Limited

- IFB Industries Limited

- Xiaomi Technology India Pvt. Ltd.

- Apple India Pvt. Ltd.

- BSH Home Appliances India (Bosch)

- Other Prominent Players

** Financial information in case of non-listed companies will be provided as per availability*

*** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable*

Frequently Asked Questions

1. How large is the India consumer electronics and appliances market and what is its growth forecast?

Ans: The India consumer electronics and appliances market size is valued at USD 86.5 billion in 2025 and is projected to reach USD 175.8 billion by 2032, growing at a CAGR of around 10.7%. This strong India consumer electronics and appliances market growth is driven by accelerated disposable income growth, rising tier-2 and tier-3 city penetration, structural shift toward smart and energy-efficient devices, and major domestic and global capacity expansions under the PLI scheme. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India consumer electronics and appliances market?

Ans: The India consumer electronics and appliances market segmentation shows that major appliances and white goods dominate with approximately 42% to 45% share, followed by entertainment electronics at 24% to 27% and computing and mobile devices at 22% to 25%. Refrigerators and air conditioners lead by product type with 28% to 32% combined share, while smart and IoT-enabled devices are the fastest-growing segment, expanding at 14% to 17% annually. The report breaks down demand across product types, categories, technologies, price ranges, distribution channels, and end-users, helping businesses understand where growth is accelerating across the India consumer electronics and appliances market.

3. What are the key drivers of growth in the India consumer electronics and appliances market?

Ans: Key India consumer electronics and appliances market drivers include rising household disposable income growing at 9% to 11% annually, structural shift toward smart, IoT-enabled, and energy-efficient devices driven by BEE star-rating norms and Smart Cities Mission, and accelerated localised manufacturing under the Make in India and PLI scheme. Global consumer electronics majors such as Samsung, LG, Sony, Panasonic, Apple, and Bosch are investing in India-specific manufacturing capacity and R&D centers. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends shaping the India consumer electronics and appliances market.

4. Which regions are driving growth in the India consumer electronics and appliances market?

Ans: Regional analysis of the India consumer electronics and appliances market shows that North and West India together account for nearly 54% to 58% of total demand, driven by manufacturing clusters in Noida, Sri City, Pune, and Sanand, along with strong urban consumption hubs in Delhi NCR, Mumbai, and Ahmedabad. South India contributes around 24% to 27%, supported by IT-sector affluence in Bengaluru, Chennai, and Hyderabad, and growing manufacturing in Sri City and Sriperumbudur. East and Central India together account for 16% to 20%, supported by West Bengal’s urban demand and growing consumer activity. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India consumer electronics and appliances market?

Ans: Recent trends in the India consumer electronics and appliances market include rapid adoption of smart, IoT-enabled, and AI-powered devices growing at 14% to 17% annually, capacity expansion by global majors and domestic producers under the PLI scheme, rising role of premium televisions, inverter air conditioners, and smart wearables, and accelerated category innovation by Samsung (Bespoke AI), LG (ThinQ), Sony, Panasonic, and Apple. The September 2025 GST rate cut on televisions above 32 inches from 28% to 18% has sparked 30% to 35% sales growth, while the BIS QCO 2025 enforcement is reshaping product compliance. The report covers latest product launches, partnerships, capacity expansions, and competitive moves shaping the long-term India consumer electronics and appliances market forecast 2032.

Frequently Asked Questions

1. How large is the India consumer electronics and appliances market and what is its growth forecast?

Ans: The India consumer electronics and appliances market size is valued at USD 86.5 billion in 2025 and is projected to reach USD 175.8 billion by 2032, growing at a CAGR of around 10.7%. This strong India consumer electronics and appliances market growth is driven by accelerated disposable income growth, rising tier-2 and tier-3 city penetration, structural shift toward smart and energy-efficient devices, and major domestic and global capacity expansions under the PLI scheme. The report provides detailed market sizing, forecast modelling, and segment-wise growth analysis across value and volume terms, helping businesses identify high-opportunity areas and plan long-term strategies.

2. Which segments are driving demand in the India consumer electronics and appliances market?

Ans: The India consumer electronics and appliances market segmentation shows that major appliances and white goods dominate with approximately 42% to 45% share, followed by entertainment electronics at 24% to 27% and computing and mobile devices at 22% to 25%. Refrigerators and air conditioners lead by product type with 28% to 32% combined share, while smart and IoT-enabled devices are the fastest-growing segment, expanding at 14% to 17% annually. The report breaks down demand across product types, categories, technologies, price ranges, distribution channels, and end-users, helping businesses understand where growth is accelerating across the India consumer electronics and appliances market.

3. What are the key drivers of growth in the India consumer electronics and appliances market?

Ans: Key India consumer electronics and appliances market drivers include rising household disposable income growing at 9% to 11% annually, structural shift toward smart, IoT-enabled, and energy-efficient devices driven by BEE star-rating norms and Smart Cities Mission, and accelerated localised manufacturing under the Make in India and PLI scheme. Global consumer electronics majors such as Samsung, LG, Sony, Panasonic, Apple, and Bosch are investing in India-specific manufacturing capacity and R&D centers. The report provides in-depth analysis of growth drivers, supported by data-backed insights and real market trends shaping the India consumer electronics and appliances market.

4. Which regions are driving growth in the India consumer electronics and appliances market?

Ans: Regional analysis of the India consumer electronics and appliances market shows that North and West India together account for nearly 54% to 58% of total demand, driven by manufacturing clusters in Noida, Sri City, Pune, and Sanand, along with strong urban consumption hubs in Delhi NCR, Mumbai, and Ahmedabad. South India contributes around 24% to 27%, supported by IT-sector affluence in Bengaluru, Chennai, and Hyderabad, and growing manufacturing in Sri City and Sriperumbudur. East and Central India together account for 16% to 20%, supported by West Bengal’s urban demand and growing consumer activity. The report offers state-level and regional insights, helping businesses identify high-growth markets and optimise expansion strategies.

5. What are the latest trends in the India consumer electronics and appliances market?

Ans: Recent trends in the India consumer electronics and appliances market include rapid adoption of smart, IoT-enabled, and AI-powered devices growing at 14% to 17% annually, capacity expansion by global majors and domestic producers under the PLI scheme, rising role of premium televisions, inverter air conditioners, and smart wearables, and accelerated category innovation by Samsung (Bespoke AI), LG (ThinQ), Sony, Panasonic, and Apple. The September 2025 GST rate cut on televisions above 32 inches from 28% to 18% has sparked 30% to 35% sales growth, while the BIS QCO 2025 enforcement is reshaping product compliance. The report covers latest product launches, partnerships, capacity expansions, and competitive moves shaping the long-term India consumer electronics and appliances market forecast 2032.