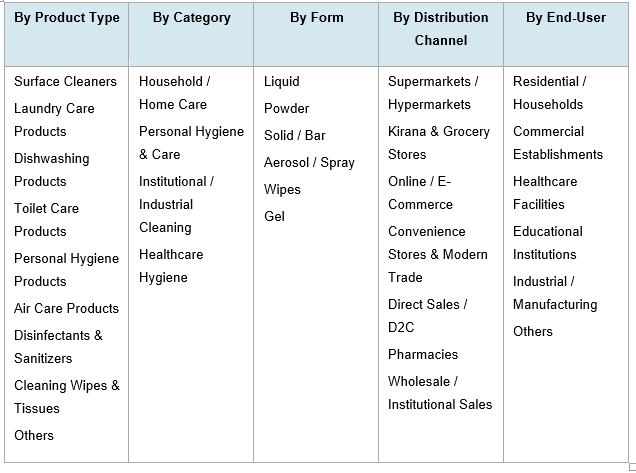

India Cleaning and Hygiene Products Market, By Product Type (Surface Cleaners, Laundry Care Products, Dishwashing Products, Toilet Care Products, Personal Hygiene Products, Air Care Products, Disinfectants & Sanitizers, Cleaning Wipes & Tissues, Others); By Category (Household / Home Care, Personal Hygiene & Care, Institutional / Industrial Cleaning, Healthcare Hygiene); By Form (Liquid, Powder, Solid / Bar, Aerosol / Spray, Wipes, Gel); By Ingredient Type (Synthetic / Conventional, Natural / Plant-Based, Bio-Based / Eco-Friendly, Antibacterial / Antimicrobial); By Pricing Tier (Mass Market, Premium, Super-Premium); By Distribution Channel (Supermarkets / Hypermarkets, Kirana & Grocery Stores, Online / E-Commerce, Convenience Stores & Modern Trade, Direct Sales / D2C, Pharmacies, Wholesale / Institutional Sales); By End-User (Residential / Households, Commercial Establishments, Healthcare Facilities, Educational Institutions, Industrial / Manufacturing, Others); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Consumer Goods & Retail

- Apr 2026

- Pages 150

- Report Format: pdf

- Report Price: $1800 USD

India Cleaning and Hygiene Products Market: Hygiene Awareness & Premiumization Wave Powers Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

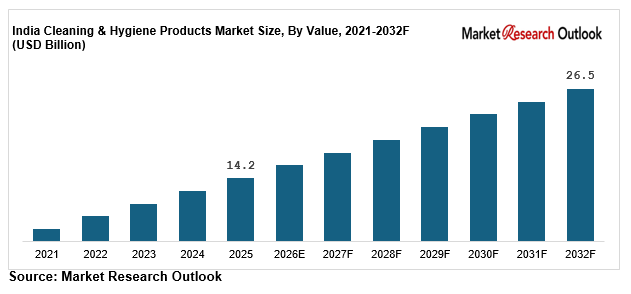

| Market Size (2025) | USD 14.2 Billion |

| CAGR (2026-2032) | 9.3% |

| Leading Segment | Personal Hygiene & Surface Cleaning Products |

| Fastest Growing Segment | Natural & Eco-Friendly Cleaning Products |

| Market Size (2032) | USD 26.5 Billion |

Source: Market Research Outlook

Market Overview: India Cleaning and Hygiene Products Market

The India cleaning and hygiene products market size is expanding rapidly, driven by sustained post-pandemic hygiene awareness, rising household cleaning consumption, and a clear shift toward natural and premium cleaning products. Valued at USD 14.2 billion in 2025, the market is projected to reach USD 26.5 billion by 2032, growing at a CAGR of 9.3%.

The India cleaning and hygiene products market growth is supported by strong demand across urban households, hospitality and food service, hospitals and clinics, educational institutions, and industrial cleaning applications. Personal hygiene products and surface cleaning solutions continue to dominate consumption, while natural, eco-friendly, and biodegradable cleaning products are emerging as the fastest-growing segment.

Regulatory and policy frameworks are reshaping the market landscape. Standards from the Bureau of Indian Standards, plastic waste rules under the Extended Producer Responsibility framework, and initiatives such as the Swachh Bharat Mission are driving demand for compliant, sustainable, and performance-driven hygiene products. At the same time, corporate ESG commitments are accelerating the shift toward low-impact formulations and recyclable packaging.

Global FMCG leaders such as Hindustan Unilever, Reckitt Benckiser, Procter & Gamble, SC Johnson, and Henkel are expanding India-focused manufacturing and innovation capabilities. Domestic companies including Godrej Consumer Products, Dabur, ITC Limited, Patanjali Ayurved, Nirma, and Jyothy Labs are strengthening their presence across mass, natural, and specialty cleaning segments.

As a result, the India cleaning and hygiene products market is evolving into a sustainability-led, brand-driven, and innovation-focused ecosystem, with strong long-term growth potential supported by premiumization, product differentiation, and expanding end-use applications.

Key Report Takeaways: India Cleaning and Hygiene Products Market

- The India cleaning and hygiene products market size is projected to grow from USD 14.2 billion in 2025 to USD 26.5 billion by 2032, at a CAGR of 9.3%, driven by rising hygiene awareness, premiumization, institutional demand, and adoption of eco-friendly cleaning products.

- Personal hygiene and surface cleaning products dominate the India cleaning and hygiene products market, accounting for over 55% of total demand, supported by strong usage of hand wash, sanitizers, soaps, dishwashing liquids, and household disinfectants.

- Natural and eco-friendly cleaning products are the fastest-growing segment, expected to grow at 14% to 17% annually, driven by sustainability trends, plastic packaging regulations, and increasing consumer preference for biodegradable formulations.

- Rapid expansion of institutional and healthcare cleaning demand, including hospitality, hospitals, corporate facilities, and educational institutions, is driving growth across B2B and B2B2C segments in the India cleaning and hygiene products market.

- Investments by global players such as Hindustan Unilever, Reckitt Benckiser, Procter & Gamble, SC Johnson, and Henkel are strengthening local manufacturing, R&D, and innovation, supporting long-term growth in the India cleaning and hygiene products market.

Key Market Drivers: India Cleaning and Hygiene Products Market

Heightened Hygiene Awareness and Structural Shift Toward Daily Sanitization

The India cleaning and hygiene products market is being strongly driven by sustained post-pandemic hygiene awareness and a clear shift toward daily sanitization practices in Indian households. The home care segment is growing at 10% to 12% annually, outpacing most FMCG categories.

Consumption of hand wash, surface disinfectants, and laundry hygiene products has moved from occasional use to routine daily usage, with strong penetration growth across urban and Tier-2 markets. Per capita spending on cleaning and hygiene products in India remains relatively low at USD 9 to USD 11, compared to developed markets, indicating significant long-term headroom for growth.

Leading companies such as Hindustan Unilever, Reckitt Benckiser, Procter & Gamble, Godrej Consumer Products, ITC Limited, and Dabur, along with emerging D2C brands, are expanding manufacturing capacity and strengthening product portfolios.

This sustained behavioural shift is creating strong demand for surface cleaning products, hand hygiene solutions, sanitizers, and laundry care products, reinforcing long-term growth across the India cleaning and hygiene products market.

Rapid Urbanization and Premiumization in Cleaning and Hygiene Categories

The India cleaning and hygiene products market is experiencing a clear shift toward premium and specialty cleaning products, growing at 12% to 15% annually, well ahead of mass-market categories. This growth is being driven by rapid urbanization, rising disposable income, increasing nuclear households, and expansion of India’s middle-class population.

Evolving consumer preferences are reshaping demand across detergents, surface cleaners, dishwashing products, and personal hygiene segments, with greater emphasis on convenience, product performance, and brand-led differentiation. Premium formats such as concentrated detergents, plant-based dishwashing liquids, fragrance-led floor cleaners, and dermatologically tested hand wash now account for 22% to 26% of total market value, up significantly from under 15% five years ago.

Leading companies such as Hindustan Unilever, Reckitt Benckiser, and Procter & Gamble are expanding premium product portfolios, while domestic players including Godrej Consumer Products and Dabur are strengthening natural and ayurveda-based offerings.

This structural shift toward premium, value-added, and differentiated cleaning and hygiene products is reinforcing long-term growth and reshaping competitive dynamics across the India cleaning and hygiene products market.

Government-Led Sanitation Initiatives Driving Institutional and Healthcare Hygiene Demand

The India cleaning and hygiene products market is being strongly supported by government-led sanitation initiatives and rising demand from institutional, hospitality, and healthcare segments. Programmes such as the Swachh Bharat Mission and the Jal Jeevan Mission are driving higher hygiene standards and consistent consumption of cleaning products across public and private infrastructure.

The institutional and industrial cleaning segment is growing at 11% to 13% annually, supported by increasing usage across hospitals, hotels, restaurants, airports, metro systems, schools, and corporate offices. This is creating strong demand for professional cleaning solutions and high-performance hygiene products.

Key players such as Diversey, SC Johnson (professional division), and Hindustan Unilever (HUL Professional), along with domestic suppliers, are expanding product portfolios and strengthening B2B distribution networks.

At the same time, healthcare expansion under the Ayushman Bharat programme, combined with stricter hygiene protocols in food service and hospitality sectors, is accelerating adoption of institutional-grade cleaning and hygiene products.

This structural shift is reinforcing long-term growth across premium and institutional segments, positioning the India cleaning and hygiene products market for sustained expansion through 2032.

Key Market Challenges: India Cleaning and Hygiene Products Market

Raw Material Price Volatility and Input Cost Pressure

The India cleaning and hygiene products market is highly sensitive to fluctuations in key raw materials such as linear alkyl benzene (LAB), SLES, fatty alcohols, soda ash, palm oil derivatives, fragrances, and packaging resins, which together account for a large share of production costs. These inputs are closely linked to crude oil and palm oil price movements, leading to cost volatility and margin pressure for manufacturers.

Dependence on imported specialty ingredients further increases exposure to global supply chain disruptions. In response, companies are focusing on backward integration, long-term sourcing contracts, and reformulation using locally available and natural ingredients to improve cost stability.

Fragmented Market and Competition from Unorganised Players

The India cleaning and hygiene products market remains fragmented, with unorganised and regional players accounting for a notable share of volume, particularly in detergents, soaps, and low-cost cleaning products. Counterfeit and imitation products continue to pose risks to brand equity and product quality in price-sensitive markets.

Leading FMCG companies are addressing these challenges through improved packaging, stronger distribution networks, and direct rural outreach, but brand protection and premiumization in rural markets remain ongoing challenges.

Regulatory Pressure on Ingredients, Packaging, and Sustainability

The market is also facing increasing regulatory complexity related to chemical ingredient standards, plastic packaging rules, and effluent management requirements. Frameworks such as the Central Pollution Control Board guidelines and Extended Producer Responsibility norms are raising compliance costs for manufacturers.

Global regulations including REACH regulation are further impacting export-oriented players, requiring stricter ingredient disclosure and sustainability compliance. At the same time, retailers and institutional buyers are adopting green procurement standards, pushing companies toward eco-friendly formulations and recyclable packaging.

While these regulatory developments increase operational complexity, they also create entry barriers that favour organised, innovation-led FMCG players in the India cleaning and hygiene products market.

Rapid Shift Toward Natural and Eco-Friendly Cleaning Products

The India cleaning and hygiene products market is witnessing strong adoption of natural, plant-based, and eco-friendly cleaning products, with this segment growing at 14% to 17% annually, significantly outpacing conventional categories. Rising consumer focus on ingredient transparency, biodegradable formulations, and sustainable packaging is reshaping product development across home care and personal hygiene segments.

Plant-based surfactants derived from coconut and corn, along with biodegradable detergents and ayurvedic cleaning products, are gaining traction among both households and institutional buyers. Leading companies such as Hindustan Unilever, Reckitt Benckiser, Procter & Gamble, SC Johnson, and Henkel are expanding natural and sustainable cleaning product portfolios in India.

Capacity Expansion by Global and Domestic Players

The India cleaning and hygiene products market growth is also being supported by significant capacity expansion across global majors and domestic FMCG companies. Investments in home care manufacturing, detergents, surface cleaners, and disinfectants are strengthening supply chains and improving product availability.

Companies such as Hindustan Unilever, Reckitt Benckiser, Procter & Gamble, and SC Johnson are expanding production capacity, while domestic players including Godrej Consumer Products, Dabur, ITC Limited, Patanjali Ayurved, Nirma, and Jyothy Labs are strengthening local manufacturing and product innovation capabilities.

Rising Role of E-Commerce and D2C Distribution Channels

E-commerce, D2C, modern retail, and quick-commerce platforms are emerging as key growth channels in the India cleaning and hygiene products market, expected to account for over 28% of total sales by 2032. Platforms such as Amazon, Flipkart, Reliance Retail, BigBasket, Blinkit, Zepto, and Swiggy Instamart are driving rapid adoption.

Leading FMCG brands are launching e-commerce-first cleaning products, premium variants, and quick-commerce packs, while D2C brands focused on natural, premium, and niche hygiene products are scaling rapidly.

This shift toward digital-first distribution and premium product positioning is reinforcing long-term growth across the India cleaning and hygiene products market, particularly in urban and Tier-2 markets.

Segmental Insights: India Cleaning and Hygiene Products Market

By Category: Personal Hygiene and Home Care Dominate Demand

The India cleaning and hygiene products market is led by personal hygiene and home care categories, which together account for 78% to 82% of total consumption. Personal hygiene products such as soaps, hand wash, and sanitizers contribute 38% to 42%, while home care products including laundry detergents, surface cleaners, and dishwashing liquids account for 36% to 40%.

Institutional and industrial cleaning contributes 12% to 14% of demand, supported by hospitality, corporate, and facility management segments. Healthcare hygiene products, including alcohol-based sanitizers and clinical disinfectants, account for 6% to 8%.

Leading companies such as Hindustan Unilever, Reckitt Benckiser, Procter & Gamble, Godrej Consumer Products, and Dabur continue to scale production and sourcing, reinforcing category dominance.

By Product Type: Personal Hygiene Leads, Natural Products Grow Fastest

Within the India cleaning and hygiene products market, personal hygiene products account for 28% to 30% of total demand, followed by laundry care (22% to 24%), surface cleaners (14% to 16%), dishwashing products (10% to 12%), and toilet care (8% to 10%). Disinfectants, wipes, and air care products make up the remaining share.

Natural and eco-friendly cleaning products are the fastest-growing segment, expanding at 14% to 17% annually, driven by sustainability trends, biodegradable formulations, and regulatory pressure on packaging and ingredients.

Regional Insights: West and South India Lead Market Activity

West and South India together account for 56% to 60% of the India cleaning and hygiene products market, supported by strong FMCG manufacturing clusters in Maharashtra, Gujarat, Karnataka, and Tamil Nadu, along with high urban consumption in major cities.

North India contributes 22% to 25% of demand, driven by Delhi NCR, Uttar Pradesh, Haryana, and Punjab, while East and Central India account for 16% to 20%, supported by growing rural penetration and rising hygiene awareness.

Capacity expansions by Hindustan Unilever, Reckitt Benckiser, Procter & Gamble, Godrej Consumer Products, and ITC Limited are strengthening regional supply chains and improving proximity to retail, institutional, and e-commerce demand hubs.

Recent Developments: India Cleaning and Hygiene Products Market

- The India cleaning and hygiene products market has witnessed strong momentum in capacity expansion and natural-product innovation during 2024 and 2025. Companies such as Hindustan Unilever, Reckitt Benckiser, Procter & Gamble, and SC Johnson have expanded manufacturing capacity across detergents, hand wash, disinfectants, and air care. Domestic players including Godrej Consumer Products, Dabur, ITC Limited, Patanjali Ayurved, and Jyothy Labs are strengthening capacity in natural and ayurvedic cleaning products, reinforcing India’s position as a competitive manufacturing hub.

- Downstream demand is being accelerated by modern trade, e-commerce, and quick-commerce platforms such as Reliance Retail, BigBasket, Amazon, Flipkart, Blinkit, Zepto, and Swiggy Instamart, which are scaling long-term sourcing partnerships with FMCG companies. At the same time, D2C brands focused on plant-based and biodegradable cleaning products are expanding rapidly. Institutional players such as Diversey, SC Johnson (professional division), Hindustan Unilever (HUL Professional), and Reckitt Benckiser (Reckitt Pro) are also strengthening B2B supply capabilities.

- Sustainability-led innovation is emerging as a key trend in the India cleaning and hygiene products market, with companies focusing on natural, biodegradable, and concentrated formulations. Global leaders such as Hindustan Unilever, Reckitt Benckiser, Procter & Gamble, SC Johnson, and Henkel are expanding sustainable product portfolios.

- Increasing collaboration between FMCG companies, contract manufacturers, fragrance houses, and packaging innovators is positioning India as an emerging hub for sustainable cleaning chemistries, supporting long-term growth and strengthening the India cleaning and hygiene products market outlook through 2032.

Key Market Players: India Cleaning and Hygiene Products Market

- Hindustan Unilever Limited

- Reckitt Benckiser (India) Limited

- Procter & Gamble Hygiene and Health Care Limited

- Godrej Consumer Products Limited

- ITC Limited

- Dabur India Limited

- Colgate-Palmolive (India) Limited

- Patanjali Ayurved Limited

- Nirma Limited

- Wipro Enterprises (P) Limited

- Jyothy Labs Limited

- SC Johnson Products Pvt. Ltd.

- Henkel Anand India Pvt. Ltd.

- Diversey India Pvt. Ltd.

- Amway India Enterprises Pvt. Ltd.

Report Scope

In this report, the India Cleaning and Hygiene Products Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

- By Product Type

- Surface Cleaners

- Laundry Care Products

- Dishwashing Products

- Toilet Care Products

- Personal Hygiene Products

- Air Care Products

- Disinfectants & Sanitizers

- Cleaning Wipes & Tissues

- Others

- By Category

- Household / Home Care

- Personal Hygiene & Care

- Institutional / Industrial Cleaning

- Healthcare Hygiene

- By Form

- Liquid

- Powder

- Solid / Bar

- Aerosol / Spray

- Wipes

- Gel

- By Ingredient Type

- Synthetic / Conventional

- Natural / Plant-Based

- Bio-Based / Eco-Friendly

- Antibacterial / Antimicrobial

- By Pricing Tier

- Mass Market

- Premium

- Super-Premium

- By Distribution Channel

- Supermarkets / Hypermarkets

- Kirana & Grocery Stores

- Online / E-Commerce

- Convenience Stores & Modern Trade

- Direct Sales / D2C

- Pharmacies

- Wholesale / Institutional Sales

- By End-User

- Residential / Households

- Commercial Establishments (Hotels, Restaurants, Offices)

- Healthcare Facilities (Hospitals, Clinics)

- Educational Institutions

- Industrial / Manufacturing

- Others

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Cleaning and Hygiene Products Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic cleaning and hygiene producers, specialty natural and ayurvedic cleaning specialists, global entrants, or niche segment leaders.

The India Cleaning and Hygiene Products Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021-2032

- By Product Type

- By Category

- By Form

- By Distribution Channel

- By End-User

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Cleaning and Hygiene Products Market

- India Cleaning and Hygiene Products Market Insights

- Market Dynamics

- Growth Drivers

- Heightened hygiene awareness post-pandemic and structural shift toward sanitization in Indian households driving sustained demand.

- Rapid urbanization, rising disposable income, and growing middle-class population fueling premiumization across cleaning and hygiene categories.

- Government-led sanitation initiatives such as Swachh Bharat Mission and expanding institutional, hospitality, and healthcare hygiene demand.

- Restraints

- Raw material price volatility linked to crude oil derivatives, surfactants, and palm oil pressuring producer margins across the India cleaning and hygiene products market.

- Intense competition from unorganized players and counterfeit products in price-sensitive rural and tier-3 / tier-4 markets creating brand and pricing risks.

- Tightening regulatory framework around chemical ingredients, plastic packaging, and effluent management raising compliance costs.

- Opportunities

- Rapid scale-up of natural, plant-based, and biodegradable cleaning products aligned with sustainability and green-label consumer mandates.

- High-growth demand from institutional cleaning, hospitality, healthcare, and corporate facility management supporting B2B value expansion.

- Emerging E-commerce, D2C, and quick-commerce channels enabling premium and niche cleaning brands to scale across urban India.

- Challenges

- Intense price-led competition between MNC majors and domestic players compressing margins across mass-market detergent, soap, and floor-cleaner segments.

- Shortage of skilled R&D formulators, fragrance chemists, and quality control personnel for natural and specialty product development.

- Fragmented retail landscape with diverse pricing tiers, regional preferences, and SKU complexity across urban, semi-urban, and rural markets.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Growth Drivers

- Industry Value Chain & Entry Points

- Upstream Raw Material Suppliers (surfactants, LAB, SLES, fatty alcohols, fragrances, packaging resins)

- Specialty Ingredient & Active Producers (antimicrobials, enzymes, plant-based extracts, essential oils)

- Bio-Based & Natural Ingredient Suppliers (renewable feedstock, ayurvedic and herbal actives)

- Contract Manufacturers & Formulators (third-party manufacturing, private-label production)

- Quality Control, R&D & Application Laboratories (BIS, FSSAI, CDSCO, ecolabels)

- Brand Owners & FMCG Manufacturers (HUL, Reckitt, P&G, Godrej, ITC, Dabur, Patanjali)

- Distributors, C&F Agents & Wholesale Networks

- Retail Channels (kirana stores, supermarkets, hypermarkets, modern trade, pharmacies)

- E-Commerce, D2C & Quick-Commerce Platforms

- End-Users (households, hospitality, healthcare, institutional, industrial)

- India Cleaning and Hygiene Products Market: Regulatory Framework

- India Cleaning and Hygiene Products Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (‘000 Tons)

- Market Share & Forecast

- By Product Type

- Surface Cleaners

- Laundry Care Products

- Dishwashing Products

- Toilet Care Products

- Personal Hygiene Products

- Air Care Products

- Disinfectants & Sanitizers

- Cleaning Wipes & Tissues

- Others

- By Category

- Household / Home Care

- Personal Hygiene & Care

- Institutional / Industrial Cleaning

- Healthcare Hygiene

- By Form

- Liquid

- Powder

- Solid / Bar

- Aerosol / Spray

- Wipes

- Gel

- By Ingredient Type

- Synthetic / Conventional

- Natural / Plant-Based

- Bio-Based / Eco-Friendly

- Antibacterial / Antimicrobial

- By Pricing Tier

- Mass Market

- Premium

- Super-Premium

- By Distribution Channel

- Supermarkets / Hypermarkets

- Kirana & Grocery Stores

- Online / E-Commerce

- Convenience Stores & Modern Trade

- Direct Sales / D2C

- Pharmacies

- Wholesale / Institutional Sales

- By End-User

- Residential / Households

- Commercial Establishments (Hotels, Restaurants, Offices)

- Healthcare Facilities (Hospitals, Clinics)

- Educational Institutions

- Industrial / Manufacturing

- Others

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Cleaning and Hygiene Products Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- Hindustan Unilever Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Hindustan Unilever Limited

- By Product Type

- Market Size & Forecast, 2021-2032

- Market Dynamics

*(Same Data Pointers Will Be Provided for The Below Companies)

- Reckitt Benckiser (India) Limited

- Procter & Gamble Hygiene and Health Care Limited

- Godrej Consumer Products Limited

- ITC Limited

- Dabur India Limited

- Colgate-Palmolive (India) Limited

- Patanjali Ayurved Limited

- Nirma Limited

- Wipro Enterprises (P) Limited

- Jyothy Labs Limited

- SC Johnson Products Pvt. Ltd.

- Henkel Anand India Pvt. Ltd.

- Diversey India Pvt. Ltd.

- Amway India Enterprises Pvt. Ltd.

- Other Prominent Players

** Financial information in case of non-listed companies will be provided as per availability*

*** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable*

Frequently Asked Questions

1. How large is the India cleaning and hygiene products market and what is its growth forecast?

Ans: The India cleaning and hygiene products market size is valued at USD 14.2 billion in 2025 and is projected to reach USD 26.5 billion by 2032, growing at a CAGR of 9.3%. Growth is driven by rising hygiene awareness, increasing household consumption, premiumization, and expanding institutional and healthcare cleaning demand. The report provides detailed market sizing, forecasts, and segment-wise growth analysis.

2. Which segments are driving demand in the India cleaning and hygiene products market?

Ans: Personal hygiene and home care dominate the India cleaning and hygiene products market, accounting for 78% to 82% of total demand. By product type, surface cleaners and personal hygiene products lead consumption, while natural and eco-friendly cleaning products are the fastest-growing segment, expanding at 14% to 17% annually.

3. What are the key drivers of growth in the India cleaning and hygiene products market?

Ans: Key drivers include sustained post-pandemic hygiene awareness, rapid urbanization and rising income levels driving premiumization, and government initiatives such as the Swachh Bharat Mission supporting institutional demand. Investments by companies like Hindustan Unilever, Reckitt Benckiser, and Procter & Gamble are also accelerating market growth.

4. Which regions are driving growth in the India cleaning and hygiene products market?

Ans: West and South India account for 56% to 60% of demand, driven by strong FMCG manufacturing and urban consumption. North India contributes 22% to 25%, while East and Central India account for 16% to 20%, supported by rising hygiene adoption and expanding distribution networks.

5. What are the latest trends in the India cleaning and hygiene products market?

Ans: Key trends include rising adoption of natural and biodegradable cleaning products, capacity expansion by global and domestic players, and rapid growth of e-commerce, D2C, and quick-commerce channels. Online and modern trade are growing at 18% to 22% annually, reshaping distribution across the India cleaning and hygiene products market.

Frequently Asked Questions

1. How large is the India cleaning and hygiene products market and what is its growth forecast?

Ans: The India cleaning and hygiene products market size is valued at USD 14.2 billion in 2025 and is projected to reach USD 26.5 billion by 2032, growing at a CAGR of 9.3%. Growth is driven by rising hygiene awareness, increasing household consumption, premiumization, and expanding institutional and healthcare cleaning demand. The report provides detailed market sizing, forecasts, and segment-wise growth analysis.

2. Which segments are driving demand in the India cleaning and hygiene products market?

Ans: Personal hygiene and home care dominate the India cleaning and hygiene products market, accounting for 78% to 82% of total demand. By product type, surface cleaners and personal hygiene products lead consumption, while natural and eco-friendly cleaning products are the fastest-growing segment, expanding at 14% to 17% annually.

3. What are the key drivers of growth in the India cleaning and hygiene products market?

Ans: Key drivers include sustained post-pandemic hygiene awareness, rapid urbanization and rising income levels driving premiumization, and government initiatives such as the Swachh Bharat Mission supporting institutional demand. Investments by companies like Hindustan Unilever, Reckitt Benckiser, and Procter & Gamble are also accelerating market growth.

4. Which regions are driving growth in the India cleaning and hygiene products market?

Ans: West and South India account for 56% to 60% of demand, driven by strong FMCG manufacturing and urban consumption. North India contributes 22% to 25%, while East and Central India account for 16% to 20%, supported by rising hygiene adoption and expanding distribution networks.

5. What are the latest trends in the India cleaning and hygiene products market?

Ans: Key trends include rising adoption of natural and biodegradable cleaning products, capacity expansion by global and domestic players, and rapid growth of e-commerce, D2C, and quick-commerce channels. Online and modern trade are growing at 18% to 22% annually, reshaping distribution across the India cleaning and hygiene products market.