India Specialty Chemicals Market, By Product Type (Agrochemicals, Dyes & Pigments, Pharmaceutical Intermediates & APIs, Surfactants, Specialty Polymers & Additives, Flavors & Fragrances, Personal Care Ingredients, Construction Chemicals, Specialty Coatings Additives, Electronic Chemicals, Water Treatment Chemicals, Others); By Chemistry (Organic Specialty Chemicals, Inorganic Specialty Chemicals, Bio-Based / Green Specialty Chemicals, Hybrid Specialty Chemicals); By Application (Crop Protection, Pharmaceutical Synthesis, Textile Processing, Paint & Coating Formulation, Personal Care Formulation, Food Additives, Electronic Chemical Formulation, Construction Chemical Formulation, Water Treatment Formulation, Others); By Form (Liquid, Solid / Powder, Gas, Gel / Paste); By End-Use Industry (Agriculture & Crop Protection, Pharmaceuticals & Healthcare, Paints & Coatings, Textile & Leather, Personal Care & Cosmetics, Food & Beverages, Building & Construction, Automotive, Electronics & Electricals, Oil & Gas, Water Treatment, Others); By Sales Channel (Direct Sales / OEM Contracts, Distributors & Specialty Chemical Agents, Online / B2B Platforms, Contract Manufacturing (CRAMS), Export Channels); By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Chemicals & Advanced Materials

- Apr 2026

- Pages 140

- Report Format: pdf

- Report Price: $1800 USD

India Specialty Chemicals Market: China+1 Strategy & Sustainability-Led Innovation Power Structural Growth, Forecasts 2032

Report Description

| Study Duration | 2021-2032 |

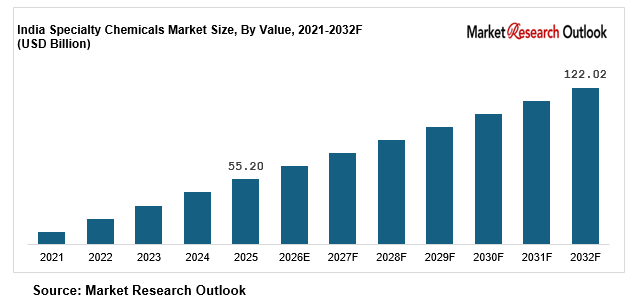

| Market Size (2025) | USD 55.20 Billion |

| CAGR (2026-2032) | 12.1% |

| Leading Segment | Agrochemicals |

| Fastest Growing Segment | Bio-Based & Green Specialty Chemicals |

| Market Size (2032) | USD 122 Billion |

Source: Market Research Outlook

Market Overview — India Specialty Chemicals Market

According to Market Research Outlook’s latest research, the India specialty chemicals market is projected to grow from USD 55.20 billion to USD 122 billion, registering a CAGR of 12.1%. Growth is being driven by strong demand from agrochemicals and pharmaceutical intermediates, rising consumption in paints, coatings, and personal care, and expanding opportunities under the China+1 strategy and CRAMS ecosystem.

India’s specialty chemicals market is entering a structural growth phase, shifting from cost-led manufacturing toward high-value, application-specific, and export-oriented chemistries. Increasing focus on sustainability, regulatory compliance, and product performance is reshaping demand across key end-use industries.

Key Report Takeaways — India Specialty Chemicals Market

- The India specialty chemicals market size is projected to grow from USD 55.20 billion in 2025 to USD 122 billion by 2032, registering a strong CAGR of 12.1 percent, driven by accelerated agrochemical and pharmaceutical intermediates demand, China+1 diversification, and the structural shift toward bio-based and green specialty chemistries.

- Agrochemicals dominate the India specialty chemicals market, accounting for approximately 22 to 25 percent of total demand, driven by strong adoption across crop protection, herbicides, fungicides, and insecticide intermediates supporting both domestic consumption and export markets.

- Bio-based and green specialty chemicals are emerging as the fastest-growing segment in the India specialty chemicals market, expected to grow at 15 to 18 percent annually as ESG mandates, CBAM compliance, and global sustainability-led procurement reshape formulation strategies.

- Accelerated growth of the Indian pharmaceutical industry, led by Sun Pharma, Dr. Reddy’s, Cipla, Lupin, and Aurobindo Pharma, combined with the government’s PLI scheme and bulk drug parks, is structurally expanding demand for pharmaceutical intermediates, KSMs, and APIs across the India specialty chemicals market.

- Rising investments by global specialty chemical majors such as BASF, Clariant, Evonik, Lanxess, and Solvay in India-specific manufacturing capacity and CRAMS partnerships are strengthening local innovation and supporting the India specialty chemicals market forecast 2032.

Key Market Drivers — India Specialty Chemicals Market

The India specialty chemicals market is witnessing strong growth, driven by expanding demand across agrochemicals, pharmaceuticals, paints and coatings, and personal care. These sectors are growing at a steady pace of around 10 to 14 percent annually, consistently outpacing broader chemical segments and creating sustained demand for specialty intermediates and performance chemicals. Agrochemicals remain the largest contributor, accounting for nearly 25 percent of total consumption, supported by strong export demand for crop protection products across Latin America and Africa, while pharmaceuticals and personal care together contribute around 30 to 35 percent.

A key structural advantage for the India specialty chemicals market lies in its low per capita consumption, currently estimated at USD 40 to 45 compared to USD 180 to 240 in developed markets, indicating significant headroom for long-term demand expansion. In response, leading companies such as SRF, PI Industries, Navin Fluorine, Aarti Industries, and Deepak Nitrite are accelerating capacity expansion and investing in high-value segments including fluorochemicals, custom synthesis, and specialty intermediates.

This ongoing investment cycle, estimated at over USD 6 billion, is strengthening domestic manufacturing capabilities while positioning India as a preferred global sourcing hub for specialty chemicals, supporting sustained market growth and improving export competitiveness.

Structural Shift Toward Bio-Based, Green, and Sustainable Specialty Chemistries Aligned with ESG Mandates

A structural shift is underway in the India specialty chemicals market, with bio-based and green chemistries growing at 15 to 18 percent annually, outpacing conventional alternatives. This transition is driven by stricter environmental norms such as CPCB and global regulations like REACH and TSCA, along with increasing demand from global buyers for sustainable and compliant products.

Green specialty chemicals are moving into mainstream adoption, offering up to 30 to 40 percent lower carbon intensity while maintaining performance. With global players like BASF, Clariant, and Evonik expanding in India and domestic companies investing in sustainable capabilities, the market is steadily shifting toward higher-value, sustainability-led growth.

China+1 Strategy and Government-Led PLI Scheme Accelerating India’s Specialty Chemicals Manufacturing Capacity

The India specialty chemicals market is gaining strong momentum from the China+1 strategy, as global companies diversify supply chains away from China. India is emerging as a preferred manufacturing hub, supported by competitive costs, improving infrastructure, and a skilled workforce, with an estimated USD 15 to 20 billion of specialty chemical sourcing expected to shift to India by 2030.

Government initiatives such as the PLI scheme, bulk drug parks, and Make in India are accelerating this transition, while the CRAMS segment is growing at 12 to 14 percent annually. Together, these factors are positioning the India specialty chemicals market as a strategic global hub for manufacturing, exports, and custom synthesis.

Key Market Challenges — India Specialty Chemicals Market

Feedstock Price Volatility Linked to Crude Oil and Petrochemical Cycles

Feedstock price volatility remains a major challenge in the India specialty chemicals market, as production costs are closely linked to global crude oil and petrochemical cycles. Key raw materials such as benzene, methanol, and propylene account for nearly 55 to 70 percent of total costs, with crude price fluctuations driving 20 to 30 percent swings in input pricing and directly impacting margins.

This volatility, combined with India’s dependence on imported intermediates, creates pricing uncertainty across pharma, agrochemicals, and coatings. In response, specialty chemical companies are focusing on backward integration, long-term sourcing contracts, and selective adoption of bio-based inputs to improve cost stability and reduce crude-linked risks.

Heavy Import Dependence for Key Starting Materials and Specialty Intermediates

A key challenge in the India specialty chemicals market is its continued dependence on imports for high-value intermediates and key starting materials. Around 60 to 70 percent of advanced intermediates—especially in pharmaceuticals, agrochemicals, and electronic chemicals—are still sourced from countries such as China, Japan, and the United States.

This reliance exposes manufacturers to supply disruptions, longer lead times of up to 8 to 16 weeks, and cost volatility. While Indian companies such as SRF, Navin Fluorine, and Aarti Industries are gradually expanding domestic capabilities, large-scale import substitution will take time. In the near term, ensuring supply reliability and cost stability remains a critical priority across the India specialty chemicals market.

Environmental Compliance, Effluent Management, and Regulatory Complexity

Environmental compliance is a major challenge in the India specialty chemicals market, as manufacturers face rising costs from stricter regulatory requirements. High water and energy usage makes the sector resource-intensive, with CPCB norms, wastewater treatment rules, and Zero Liquid Discharge requirements increasing compliance costs by around 8 to 12 percent.

Export-oriented companies must also meet global standards such as REACH, TSCA, and emerging frameworks like CBAM, while downstream industries are demanding higher purity, traceability, and sustainability standards. As a result, larger and more integrated players are better positioned to manage compliance, while smaller manufacturers face growing pressure, driving gradual consolidation across the market.

Key Market Trends — India Specialty Chemicals Market

Rapid Adoption of Bio-Based, Green, and Sustainable Specialty Chemistries in India

A major trend in the India specialty chemicals market is the rapid shift toward bio-based and sustainable chemistries, with these segments growing at 15 to 18 percent annually, faster than conventional alternatives. This transition is being driven by stricter environmental norms, including CPCB regulations and global standards such as REACH, TSCA, and CBAM.

At the same time, global companies across pharmaceuticals, personal care, and coatings are prioritising low-carbon and compliant inputs, accelerating demand for bio-based solvents, fermentation-derived intermediates, and low-VOC formulations. Leading players such as BASF, Clariant, and Evonik are expanding their green chemistry portfolios in India, reinforcing a long-term shift toward sustainability-led and higher-value specialty chemical production.

Capacity Expansion by Global Majors and Domestic Producers Reshaping Supply

Capacity expansion is a major trend in the India specialty chemicals market, with investments exceeding USD 8 billion between 2023 and 2025, reflecting strong long-term demand visibility. Global players such as BASF, Clariant, and Evonik are expanding their India operations, while domestic companies including SRF, Navin Fluorine, and Aarti Industries are scaling high-value segments like fluorochemicals, specialty intermediates, and custom synthesis.

This expansion is closely aligned with rising downstream demand, as pharmaceutical and agrochemical companies such as Sun Pharma, Dr. Reddy’s, Cipla, Lupin, and UPL continue to increase production. As a result, the India specialty chemicals market is strengthening its position as a key global manufacturing and supply hub.

Rising Role of CRAMS, Electronic Chemicals, and Personal Care Ingredients

A defining trend in the India specialty chemicals market is the growing contribution of high-value segments such as CRAMS, electronic chemicals, and personal care ingredients, which are expected to account for over 30 percent of demand by 2032. The CRAMS segment is expanding at around 12 to 14 percent annually, driven by increasing outsourcing from global pharmaceutical and agrochemical companies.

At the same time, electronic chemicals are gaining momentum with India’s semiconductor push, while personal care ingredients are benefiting from premiumisation trends. Companies such as Divis Laboratories, Syngene International, and PI Industries are expanding contract manufacturing capabilities, reinforcing a shift toward specialised, high-margin, and application-driven growth in the India specialty chemicals market.

Segmental Insights — India Specialty Chemicals Market

By End-Use Industry — Agriculture and Pharmaceuticals Lead Demand

The India specialty chemicals market is primarily driven by agriculture and pharmaceuticals, which together account for nearly 45 to 50 percent of total demand. Strong export activity in crop protection chemicals and India’s leadership in generic drug manufacturing continue to support demand for specialty intermediates, APIs, and high-performance formulations.

Agrochemicals remain a key contributor, while the pharmaceutical sector drives steady demand for complex intermediates. Beyond these, paints and coatings account for around 14 to 16 percent of the market, and personal care contributes 10 to 12 percent, supported by rising construction activity and consumer premiumisation.

With companies such as Sun Pharma, Dr. Reddy’s, Cipla, and UPL expanding production, demand for specialty chemicals is strengthening across sectors, reinforcing a stable and diversified growth base for the India specialty chemicals market.

By Product Type — Agrochemicals Lead While Bio-Based and Green Specialty Chemicals Grow Fastest

In the India specialty chemicals market, agrochemicals hold the largest share, accounting for around 22 to 25 percent of total consumption, supported by strong export demand for crop protection products. Pharmaceutical intermediates and APIs follow with a 20 to 22 percent share, reflecting India’s strength in generics and contract manufacturing.

Other key segments include dyes and pigments at 12 to 14 percent and specialty polymers and additives at 10 to 12 percent, driven by demand from textiles, coatings, packaging, and automotive applications.

At the same time, the fastest growth is seen in high-value segments such as bio-based chemicals, electronic chemicals, and specialty fluorochemicals, expanding at 15 to 18 percent annually. This shift toward sustainable, high-performance, and application-specific products is moving the India specialty chemicals market toward higher-value, innovation-led growth.

Regional Insights — India Specialty Chemicals Market

The India specialty chemicals market is highly concentrated in West and South India, which together account for around 62 to 66 percent of total production and consumption. Key manufacturing clusters in Gujarat and Maharashtra—such as Dahej, Ankleshwar, and Tarapur—benefit from strong infrastructure, port access, and integrated supply chains, while South India hubs like Hyderabad and Visakhapatnam support pharmaceutical intermediates and CRAMS activity.

North India contributes 18 to 22 percent of demand, led by pharma and agrochemical manufacturing in Baddi and surrounding regions, while East and Central India account for 14 to 18 percent, supported by dyes, pigments, and emerging industrial activity.

With continued investments from companies such as BASF, SRF, and Aarti Industries, regional clusters are strengthening supply chain integration and reinforcing India’s position as a global specialty chemicals manufacturing hub.

Recent Developments — India Specialty Chemicals Market

- The India specialty chemicals market is witnessing strong momentum in capacity expansion and green chemistry investments during 2024 and 2025. Global companies such as BASF and Clariant are strengthening their India footprint, while domestic players including SRF, Navin Fluorine, and Aarti Industries are expanding into high-value segments like fluorochemicals and specialty intermediates.At the same time, companies such as PI Industries, Deepak Nitrite, Atul, Vinati Organics, and Jubilant Ingrevia are investing in advanced and sustainable chemistries. This wave of expansion is reinforcing India’s position as a reliable, scalable, and globally competitive hub for specialty chemical manufacturing.

- Demand in the India specialty chemicals market continues to strengthen, driven by rising reliance on domestic sourcing across pharmaceuticals, agrochemicals, and consumer segments. Leading companies such as Sun Pharma, Dr. Reddy’s, Cipla, and UPL are expanding long-term procurement partnerships with specialty chemical manufacturers.CRAMS activity is also gaining pace, with firms like Divis Laboratories, Piramal Pharma Solutions, and Syngene International securing new custom synthesis contracts. In parallel, consumer brands including Hindustan Unilever, ITC, Dabur, and Marico are increasing the use of bio-based and sustainable ingredients, further supporting demand for high-value specialty chemicals.

- Sustainability is becoming a core growth driver in the India specialty chemicals market, moving beyond compliance into long-term strategy. In 2025, global players such as BASF, Clariant, Evonik, Lanxess, and Solvay expanded their portfolios of bio-based, low-carbon, and green specialty chemicals tailored for India.At the same time, strategic partnerships across specialty chemical producers, pharmaceutical companies, and agrochemical firms are increasing, particularly in green solvents, fermentation-based intermediates, and low-emission processes. This shift is positioning India as a key hub for sustainable specialty chemicals and CRAMS-led innovation, supporting long-term competitiveness through 2032.

Key Market Players — India Specialty Chemicals Market

- SRF Limited

- PI Industries Limited

- Navin Fluorine International Limited

- Aarti Industries Limited

- Deepak Nitrite Limited

- Atul Limited

- Vinati Organics Limited

- Gujarat Fluorochemicals Limited (GFL)

- Tata Chemicals Limited

- Jubilant Ingrevia Limited

- Pidilite Industries Limited

- BASF India Limited

- Clariant Chemicals (India) Limited

- Laxmi Organic Industries Limited

Report Scope

In this report, the India Specialty Chemicals Market has been segmented into the following categories, in addition to detailed analysis of key industry trends, market dynamics, competitive landscape, and growth opportunities across the forecast period:

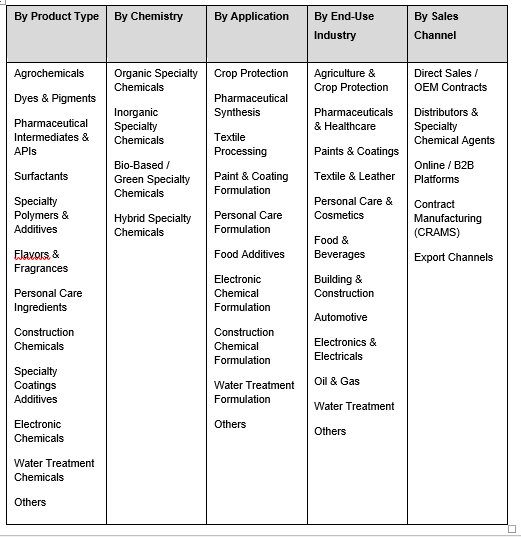

- By Product Type

- Agrochemicals

- Dyes & Pigments

- Pharmaceutical Intermediates & APIs

- Surfactants

- Specialty Polymers & Additives

- Flavors & Fragrances

- Personal Care Ingredients

- Construction Chemicals

- Specialty Coatings Additives

- Electronic Chemicals

- Water Treatment Chemicals

- Others

- By Chemistry

- Organic Specialty Chemicals

- Inorganic Specialty Chemicals

- Bio-Based / Green Specialty Chemicals

- Hybrid Specialty Chemicals

- By Application

- Crop Protection

- Pharmaceutical Synthesis

- Textile Processing

- Paint & Coating Formulation

- Personal Care Formulation

- Food Additives

- Electronic Chemical Formulation

- Construction Chemical Formulation

- Water Treatment Formulation

- Others

- By Form

- Liquid

- Solid / Powder

- Gas

- Gel / Paste

- By End-Use Industry

- Agriculture & Crop Protection

- Pharmaceuticals & Healthcare

- Paints & Coatings

- Textile & Leather

- Personal Care & Cosmetics

- Food & Beverages

- Building & Construction

- Automotive

- Electronics & Electricals

- Oil & Gas

- Water Treatment

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Specialty Chemical Agents

- Online / B2B Platforms

- Contract Manufacturing (CRAMS)

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

Competitive Landscape

Company Profiles:

Detailed analysis of the leading companies operating in the India Specialty Chemicals Market, including business overview, product portfolio, strategic initiatives, competitive positioning, and recent developments.

Company Information

Detailed profiling and strategic analysis of additional market players (up to five companies), including emerging domestic specialty chemical producers, green chemistry specialists, global entrants, or niche segment leaders.

The India Specialty Chemicals Market report is part of our ongoing research coverage. For early access, customised insights, or to confirm the release timeline, please contact our team at sarita@marketresearchoutlook.com

Table of Contents

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Primary Research Respondents

- Assumption & Limitation

- Executive Summary

- Market Overview, 2021–2032

- By Product Type

- By Application

- By End-Use Industry

- By Chemistry

- By Sales Channel

- By Region

- Analyst Recommendations

- Geopolitical Impact on India Specialty Chemicals Market

- India Specialty Chemicals Market Insights

- Market Dynamics

- Growth Drivers

- Rapid expansion of agrochemicals, pharmaceuticals, paints, and personal care industries driving core specialty chemicals consumption.

- Structural shift toward bio-based, green, and sustainable specialty chemistries driven by ESG mandates and global sustainability commitments.

- China+1 strategy of global chemical majors and government-led PLI scheme accelerating India’s specialty chemicals manufacturing capacity.

- Restraints

- Feedstock price volatility linked to crude oil, petrochemical cycles, and global supply disruptions pressuring producer margins.

- Heavy import dependence for key starting materials (KSMs) and specialty intermediates creating supply risk.

- Environmental compliance, effluent management, and tightening ZLD regulatory complexity raising compliance costs.

- Opportunities

- Rapid scale-up of CRAMS and custom synthesis services for global pharma and agrochem majors aligned with China+1 diversification.

- High-growth export opportunity to North America, Europe, Japan, and Middle East driven by supply chain diversification and regulatory-compliant manufacturing.

- Emerging opportunity in bio-based, green, and sustainable specialty chemicals aligned with ESG mandates and CBAM compliance.

- Challenges

- Intense price-led competition from Chinese specialty chemical producers compressing margins across commodity and mid-tier categories.

- Shortage of skilled chemists, process engineers, and R&D talent limiting scale-up speed of new capacity and innovation pipelines.

- Complex multi-jurisdictional regulatory compliance across CPCB, BIS, REACH, TSCA, FDA, and CBAM frameworks increasing operational complexity.

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Industry Value Chain & Entry Points

- Upstream Petrochemical & Mineral Feedstock (crude oil, naphtha, benzene, natural gas, phosphate, fluorspar)

- Key Starting Materials (KSMs) & Intermediate Producers (basic organic & inorganic chemicals, fluorochemicals, aromatics)

- Bio-Based Feedstock Producers (renewable feedstocks, fermentation-derived intermediates, agro-based raw materials)

- Specialty Chemical Synthesis & Manufacturing Operations (batch, semi-continuous, continuous flow chemistry)

- Quality Control, R&D & Application Laboratories (BIS, REACH, TSCA, FDA, ecolabels)

- Distributors, Specialty Chemical Agents & B2B Marketplaces

- Downstream Formulators (agrochem, pharma, paints, textiles, personal care, food, electronics)

- Brand Owners & Manufacturers (pharma brands, agrochem brands, paint brands, FMCG brands)

- Contract Research & Manufacturing Services (CRAMS) Channels

- End-Use Industries (agriculture, healthcare, construction, automotive, electronics, personal care, oil & gas)

- India Specialty Chemicals Market: Regulatory Framework

- India Specialty Chemicals Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- By Volume (‘000 Tons)

- Market Share & Forecast

- By Product Type

- Agrochemicals

- Dyes & Pigments

- Pharmaceutical Intermediates & APIs

- Surfactants

- Specialty Polymers & Additives

- Flavors & Fragrances

- Personal Care Ingredients

- Construction Chemicals

- Specialty Coatings Additives

- Electronic Chemicals

- Water Treatment Chemicals

- Others

- By Chemistry

- Organic Specialty Chemicals

- Inorganic Specialty Chemicals

- Bio-Based / Green Specialty Chemicals

- Hybrid Specialty Chemicals

- By Application

- Crop Protection

- Pharmaceutical Synthesis

- Textile Processing

- Paint & Coating Formulation

- Personal Care Formulation

- Food Additives

- Electronic Chemical Formulation

- Construction Chemical Formulation

- Water Treatment Formulation

- Others

- By Form

- Liquid

- Solid / Powder

- Gas

- Gel / Paste

- By End-Use Industry

- Agriculture & Crop Protection

- Pharmaceuticals & Healthcare

- Paints & Coatings

- Textile & Leather

- Personal Care & Cosmetics

- Food & Beverages

- Building & Construction

- Automotive

- Electronics & Electricals

- Oil & Gas

- Water Treatment

- Others

- By Sales Channel

- Direct Sales / OEM Contracts

- Distributors & Specialty Chemical Agents

- Online / B2B Platforms

- Contract Manufacturing (CRAMS)

- Export Channels

- By Geography

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- India Specialty Chemicals Market Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging Players

- Company Profile

- SRF Limited

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- SWOT Analysis

- SRF Limited

- By Product Type

- Market Size & Forecast, 2021-2032

*(Same Data Pointers Will Be Provided for The Below Companies)

- PI Industries Limited

- Navin Fluorine International Limited

- Aarti Industries Limited

- Deepak Nitrite Limited

- Atul Limited

- Vinati Organics Limited

- Gujarat Fluorochemicals Limited (GFL)

- Tata Chemicals Limited

- Jubilant Ingrevia Limited

- Pidilite Industries Limited

- BASF India Limited

- Clariant Chemicals (India) Limited

- Laxmi Organic Industries Limited

- Other Prominent Players

** Financial information in case of non-listed companies will be provided as per availability

*** The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable