Vietnam Ready-To-Eat Food Market, By Product Type (Instant Noodles & Instant Soups, Frozen Meals & Snacks, Canned & Preserved Food, Chilled / Refrigerated Ready Meals, Bakery & Confectionery, Other RTE Products); By Consumption (Household / Home Consumption, Food Service / HoReCa, Institutional (Schools, Hospitals, Offices), Retail / Convenience Stores, Supermarkets & Hypermarkets, E-commerce / Online Delivery, Street Food Vendors, Travel & On-the-go, Workplace Canteens, Tourism & Hospitality); By End-Use Industry (Food Manufacturing Companies, Foodservice Chains & QSRs, Retail Chains & Supermarkets, Convenience Stores & Kiosks, Online Food Delivery Platforms, Others); By Sales Channel (Supermarkets & Hypermarkets, Convenience Stores & Wet Markets, Online / E-commerce Platforms, Foodservice & HoReCa, Institutional / Government Procurement), By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Food, Beverage & Nutrition

- Mar 2026

- Pages 110

- Report Format: pdf

- Report Price: $2500 USD

Vietnam Ready-To-Eat Food Market, Size & Forecast 2021-2032

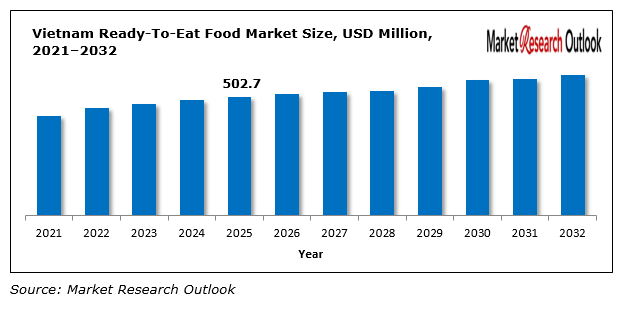

The Vietnam Ready-To-Eat Food Market size was estimated at USD 502.7 Million in 2025. During the forecast period, the Vietnam Ready-To-Eat Food Market size is projected to grow at a CAGR of 16.8% reaching a value of USD 1,490.0 Million by 2032. The expansion of frozen and chilled ready meals business operations receives support from two factors which include the development of cold chain systems and the advancement of packaging technologies. The growing frozen and chilled prepared meals market receives support from rising investments made by local companies and international enterprises which strengthen production capabilities and drive product development.

Vietnam Ready-To-Eat Food Market – Overview

Market Trends

- Vietnam RTE food market shows a major trend because customers increasingly prefer healthy and high-quality ready-to-eat meals which include low-sodium and organic and clean-label products. Consumers are becoming more health-conscious and are actively seeking products with transparent ingredient lists and nutritional benefits.

- Another key trend is the rapid growth of online food delivery and e-commerce platforms which are transforming the way consumers purchase ready-to-eat food. The integration of digital platforms with foodservice providers and retailers enables customers to receive their orders more quickly while accessing a broader range of products and experiencing better service.

Geopolitical Impact on Vietnam Ready-To-Eat Food Market

The Vietnam ready-to-eat food market gets affected by geopolitical factors which control trade policies and import-export regulations and supply chain operations. Vietnam uses its global trade agreements to enable raw material imports and processed food product exports. Global commodity price changes together with supply chain interruptions create effects on production expenses. The market gets shaped by government regulations which control food safety and quality standards and product labeling requirements. The growing regional economy together with expanding tourism brings higher demands for convenient food options.

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Million |

| Market Coverage | Vietnam |

| Segmentation | Product Type, Consumption, End-Use Industry, Sales Channel |

Segmental Coverage

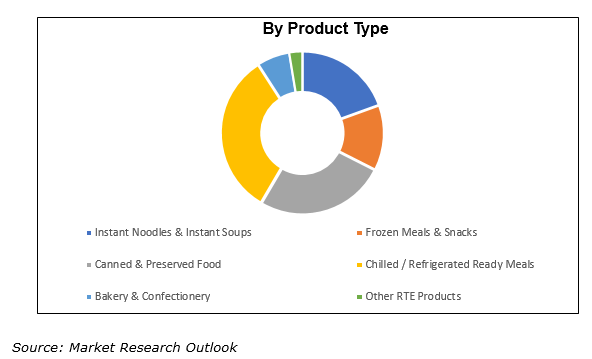

By Product Type

Based on product type, the Vietnam Ready-To-Eat Food Market is segmented into instant noodles and soups, frozen meals and snacks, canned and preserved food, chilled/refrigerated ready meals, bakery and confectionery, and other RTE products. The market sees instant noodles and soups as the dominant product because Vietnamese people consider these items to be both affordable and easy to prepare while they maintain strong cultural ties to their country. The popularity of frozen meals and snacks continues to grow in urban areas because cold chain logistics have improved and consumer tastes have shifted. Canned and preserved foods maintain constant demand because they provide extended shelf life, whereas chilled and refrigerated products have emerged as high-end market options. The bakery and confectionery industry experiences substantial growth because more people now choose to snack between meals.

By Consumption

Based on consumption, the Vietnam Ready-To-Eat Food Market is segmented household/home consumption, food service/HoReCa, institutional use, retail/convenience stores, supermarkets/hypermarkets, e-commerce/online delivery, street food vendors, travel and on-the-go consumption, workplace canteens, and tourism and hospitality. People in households spend most of their time at home because they want to experience the comfort of their home environment. The foodservice industry and the HoReCa sector experience rapid growth because of their connection to tourism and the dining habits found in urban areas. E-commerce and online delivery services experience rapid growth while street food sellers and mobile food service continue to provide their own specialized functions within Vietnam’s culinary system.

Competitive Landscape

In the competitive landscape of the Vietnam Ready-To-Eat Food market, the organisation has covered major players of the market and their details.

Here are some of the leading players that are playing a major role in the Vietnam Ready-To-Eat Food market:

- Acecook Vietnam Joint Stock Company

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- Swot Analysis

**(Same Data Pointers Will Be Provided for The Below Companies)

- Masan Consumer Corporation

- Vifon (Vietnam Food Industries Joint Stock Company)

- Nestlé Vietnam Ltd.

- CJ Foods Vietnam

- CP Vietnam Corporation

- Saigon Food Joint Stock Company

- Cholimex Food Joint Stock Company

- Ajinomoto Vietnam Co., Ltd.

- Orion Food Vina Co., Ltd.

- Other Prominent Players

Segmentation

- By Product Type

- Instant Noodles & Instant Soups

- Frozen Meals & Snacks

- Canned & Preserved Food

- Chilled / Refrigerated Ready Meals

- Bakery & Confectionery

- Other RTE Products

- By Consumption

- Household / Home Consumption

- Food Service / HoReCa

- Institutional (Schools, Hospitals, Offices)

- Retail / Convenience Stores

- Supermarkets & Hypermarkets

- E-commerce / Online Delivery

- Street Food Vendors

- Travel & On-the-go

- Workplace Canteens

- Tourism & Hospitality

- By End-Use Industry

- Food Manufacturing Companies

- Foodservice Chains & QSRs

- Retail Chains & Supermarkets

- Convenience Stores & Kiosks

- Online Food Delivery Platforms

- Others

- By Sales Channel

- Supermarkets & Hypermarkets

- Convenience Stores & Wet Markets

- Online / E-commerce Platforms

- Foodservice & HoReCa

- Institutional / Government Procurement

Vietnam Ready-To-Eat Food Market, 2032

- Research Framework

- Market Segmentation

- Research Objective

- Research Methodology

- Qualitative Research

- Primary Research

- Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Demand Side

- Supply Side

- Breakdown Of Primary Research Respondents, By Country

- Assumption & Limitation

- Qualitative Research

- Executive Summary

- Market Overview, 2021–2032

- By Product Type

- By Consumption

- By End-Use Industry

- By Sales Channel

- Analyst Recommendations

- Market Overview, 2021–2032

- Geopolitical Impact on Vietnam Ready-To-Eat Food Market

- Vietnam Ready-To-Eat Food Market Insights

- Market Dynamics

- Growth Drivers

- Rapid urbanization and busy lifestyles increasing demand for convenient food options

- Growing middle-class population with rising disposable income

- Expansion of modern retail and e-commerce food delivery platforms

- Restraints

- Consumer preference for fresh and traditional home-cooked meals

- Concerns regarding preservatives, additives, and food safety

- Limited cold chain infrastructure in some regions

- Opportunities

- Growing demand for healthy, organic, and clean-label ready-to-eat meals

- Expansion of convenience stores and online food delivery services

- Product innovation with local flavors and traditional Vietnamese cuisine

- Challenges

- Maintaining product quality and freshness during storage and distribution

- Compliance with food safety regulations and quality standards

- Intense competition from both local and international brands

- Technological Advancements

- Recent Technological Advancements

- Prior to 2020

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Growth Drivers

- Market Dynamics

- Industry Value Chain & Entry Points

- Raw Material Sourcing

- Ingredient Processing & Preparation

- Food Manufacturing & Cooking

- Packaging

- Cold Chain Storage & Warehousing

- Distribution & Logistics

- Retail & Sales Channels

- End Consumers

- Vietnam Ready-To-Eat Food Market: Regulatory Framework

- Vietnam Ready-To-Eat Food Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Million)

- Market Share & Forecast

- By Product Type

- Instant Noodles & Instant Soups

- Frozen Meals & Snacks

- Canned & Preserved Food

- Chilled / Refrigerated Ready Meals

- Bakery & Confectionery

- Other RTE Products

- By Consumption

- Household / Home Consumption

- Food Service / HoReCa

- Institutional (Schools, Hospitals, Offices)

- Retail / Convenience Stores

- Supermarkets & Hypermarkets

- E-commerce / Online Delivery

- Street Food Vendors

- Travel & On-the-go

- Workplace Canteens

- Tourism & Hospitality

- By End-Use Industry

- Food Manufacturing Companies

- Foodservice Chains & QSRs

- Retail Chains & Supermarkets

- Convenience Stores & Kiosks

- Online Food Delivery Platforms

- Others

- By Sales Channel

- Supermarkets & Hypermarkets

- Convenience Stores & Wet Markets

- Online / E-commerce Platforms

- Foodservice & HoReCa

- Institutional / Government Procurement

- By Product Type

- Market Size & Forecast, 2021-2032

- Competitive Landscape

- Vietnam Ready-To-Eat Food Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, Etc.)

- List of Emerging players

- Company Profile

- Acecook Vietnam Joint Stock Company

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Competitors

- Financial Analysis

- Swot Analysis

- Acecook Vietnam Joint Stock Company

**(Same Data Pointers Will Be Provided for The Below Companies)

- Masan Consumer Corporation

- Vifon (Vietnam Food Industries Joint Stock Company)

- Nestlé Vietnam Ltd.

- CJ Foods Vietnam

- CP Vietnam Corporation

- Saigon Food Joint Stock Company

- Cholimex Food Joint Stock Company

- Ajinomoto Vietnam Co., Ltd.

- Orion Food Vina Co., Ltd.

- Other Prominent Players

* Financial information in case of non-listed companies will be provided as per availability

**The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. What is the market size of the Vietnam Ready-To-Eat Food Market in 2025?

Ans: The Vietnam Ready-To-Eat Food market is projected to reach approximately USD 502.7 Million by 2032.

2. What is the expected growth rate of the Vietnam Ready-To-Eat Food Market during the forecast period?

Ans: The Vietnam Ready-To-Eat Food market is expected to grow at a CAGR of around 7.5% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Vietnam Ready-To-Eat Food Market by 2032?

Ans: The Vietnam Ready-To-Eat Food market is projected to reach approximately USD 1,490.0 Million by 2032.

4. What are the major factors driving the growth of the Vietnam Ready-To-Eat Food Market?

Ans: The expansion of frozen and chilled ready meals business operations receives support from two factors which include the development of cold chain systems and the advancement of packaging technologies.

5. Name the key players operating in the Vietnam Ready-To-Eat Food Market.

Ans: Key players operating in the Vietnam Ready-To-Eat Food market include Acecook Vietnam Joint Stock Company, Masan Consumer Corporation, Vifon (Vietnam Food Industries Joint Stock Company), Nestlé Vietnam Ltd., CJ Foods Vietnam, CP Vietnam Corporation, Saigon Food Joint Stock Company, Cholimex Food Joint Stock Company, Ajinomoto Vietnam Co., Ltd., Orion Food Vina Co., Ltd., and other prominent players.

Frequently Asked Questions

1. What is the market size of the Vietnam Ready-To-Eat Food Market in 2025?

Ans: The Vietnam Ready-To-Eat Food market is projected to reach approximately USD 502.7 Million by 2032.

2. What is the expected growth rate of the Vietnam Ready-To-Eat Food Market during the forecast period?

Ans: The Vietnam Ready-To-Eat Food market is expected to grow at a CAGR of around 7.5% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Vietnam Ready-To-Eat Food Market by 2032?

Ans: The Vietnam Ready-To-Eat Food market is projected to reach approximately USD 1,490.0 Million by 2032.

4. What are the major factors driving the growth of the Vietnam Ready-To-Eat Food Market?

Ans: The expansion of frozen and chilled ready meals business operations receives support from two factors which include the development of cold chain systems and the advancement of packaging technologies.

5. Name the key players operating in the Vietnam Ready-To-Eat Food Market.

Ans: Key players operating in the Vietnam Ready-To-Eat Food market include Acecook Vietnam Joint Stock Company, Masan Consumer Corporation, Vifon (Vietnam Food Industries Joint Stock Company), Nestlé Vietnam Ltd., CJ Foods Vietnam, CP Vietnam Corporation, Saigon Food Joint Stock Company, Cholimex Food Joint Stock Company, Ajinomoto Vietnam Co., Ltd., Orion Food Vina Co., Ltd., and other prominent players.