Asia-Pacific Battery Chemicals Localization Readiness Market, By Chemical Type (Lithium Chemicals, Nickel Chemicals, Cobalt Chemicals, Manganese Chemicals, Electrolyte Chemicals, Others); By Battery Type (Lithium-ion Batteries, Lithium Iron Phosphate (LFP) Batteries, Nickel Manganese Cobalt (NMC) Batteries, Nickel Cobalt Aluminum (NCA) Batteries, Solid-State Batteries); By Supply Chain Stage (Raw Material Processing, Chemical Refining, Cathode & Anode Material Production, Electrolyte Production, Battery Cell Manufacturing Integration); By End-Use Industry (Electric Vehicles (EVs), Consumer Electronics, Energy Storage Systems (ESS), Industrial Equipment, E-Mobility (E-bikes, E-scooters)); By Country (China, India, Japan, South Korea, Australia & New Zealand, Indonesia, Malaysia, Singapore, Vietnam, Rest of Asia Pacific); By Trend Analysis, Competitive Landscape & Forecast, 2021–2032

- Chemicals & Advanced Materials

- Mar 2026

- Pages 250

- Report Format: pdf

- Report Price: $3000 USD

Asia Pacific Battery Chemicals Localization Readiness Market, Size & Forecast 2021-2032

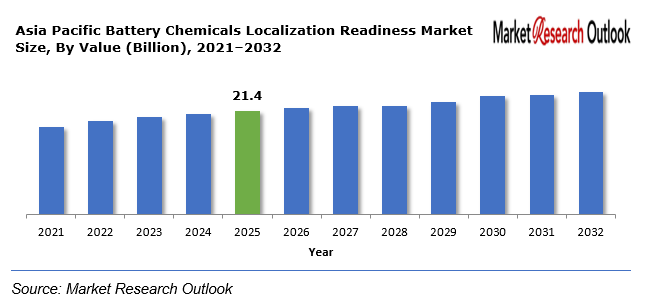

The Asia Pacific Battery Chemicals Localization Readiness Market size was estimated at USD 21.4 Billion in 2025. During the forecast period, the Asia Pacific Battery Chemicals Localization Readiness Market size is projected to grow at a CAGR of 14.6% reaching a value of USD 55.2 Billion by 2032. The growth of electric vehicle manufacturing and the development of gigafactories and the increasing need for energy storage solutions throughout the area will create this growth. The Asia-Pacific region currently controls a major portion of the worldwide lithium-ion battery supply chain because it operates extensive manufacturing facilities and develops cutting-edge battery technologies. China and South Korea and Japan have built advanced battery cell production and chemical processing capabilities while India and Indonesia and Vietnam have become emerging markets that attract investments to establish domestic battery material production facilities.

Battery Chemicals Localization Readiness – Overview

Battery chemicals localization refers to the development of domestic or regional production capabilities for essential battery materials which include lithium compounds nickel sulfate cobalt sulfate electrolyte solutions and cathode or anode materials. The localization strategies will establish supply chain resilience through two methods which include decreasing dependence on imported materials and maintaining consistent material availability for battery production.

Asia Pacific Battery Chemicals Localization Readiness Market

Growth Drivers

Rapid Expansion of Electric Vehicle Manufacturing

The battery chemicals localization readiness market experiences growth because electric vehicle production in Asia-Pacific countries expands at a rapid pace. The region’s governments implement electric mobility programs as their method for decreasing carbon emissions while developing environmentally sustainable transportation systems. The program provides financial support for electric vehicle adoption together with battery production subsidies and charging station development funding. The rising electric vehicle production creates higher demand for battery chemicals which include lithium carbonate and nickel sulfate and cobalt compounds and electrolyte solutions.

Challenges

Supply Chain Dependence on Critical Mineral Resources

The Asia-Pacific Battery Chemicals Localization Readiness Market exhibits high growth potential, yet the market encounters multiple obstacles because essential mineral resources remain inaccessible and their distribution remains limited. The battery industry depends on key materials which include lithium, nickel, cobalt and manganese; however these materials remain at risk of supply disruptions and price fluctuations because they originate from specific mining areas. The Asia-Pacific region relies on imported raw materials to produce battery chemicals, which creates supply risks that arise from geopolitical conflicts and trade limitations and global commodity market changes.

Geopolitical Impact on Asia Pacific Battery Chemicals Localization Readiness Market

The supply chain for battery chemicals in the Asia-Pacific region depends on the impact of geopolitical developments which determine its supply routes. Countries are competing worldwide to obtain essential battery materials because they want to ensure steady supplies for their electric vehicle manufacturing and renewable energy storage systems. The laws governing trade and export restrictions together with international resource treaties determine how battery chemicals and raw materials are priced and made accessible in the market. The Asia-Pacific region contains multiple countries which implement industrial policies that aim to decrease their reliance on foreign supply chains while they promote local production of battery materials.

Asia Pacific Battery Chemicals Localization Readiness Market

Segmental Coverage

Asia-Pacific Battery Chemicals Localization Readiness Market – By Chemical Type

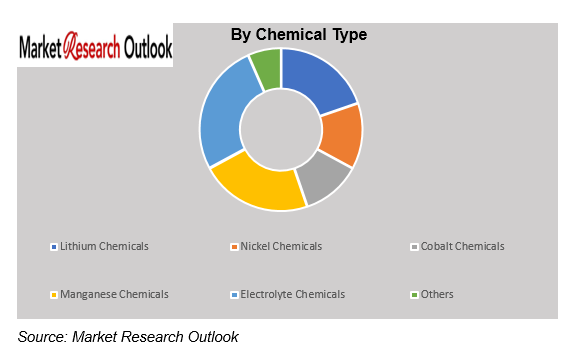

Based on chemical type, the Asia-Pacific Battery Chemicals Localization Readiness Market is segmented into Lithium Chemicals, Nickel Chemicals, Cobalt Chemicals, Manganese Chemicals, Electrolyte Chemicals, and Others. The Lithium Chemicals segment will bring a major market share during the forecast period because lithium compounds serve as essential materials for lithium-ion battery production. Lithium carbonate and lithium hydroxide serve as essential materials for producing cathode components used in electric vehicle batteries and energy storage devices. The rising adoption of electric vehicles throughout the Asia-Pacific region drives a substantial increase in demand for lithium chemicals.

Asia-Pacific Battery Chemicals Localization Readiness Market – By End-Use Industry

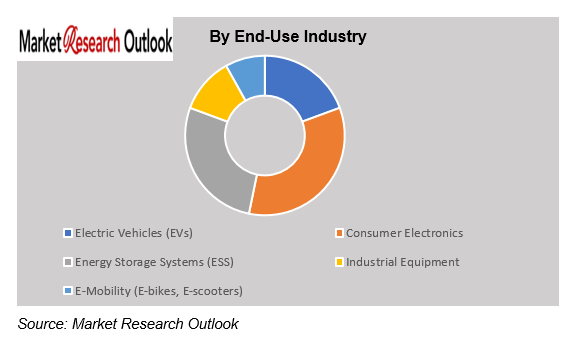

Based on end-use industry, the Asia-Pacific Battery Chemicals Localization Readiness Market is segmented into Electric Vehicles (EVs), Consumer Electronics, Energy Storage Systems (ESS), Industrial Equipment, and E-Mobility (E-bikes, E-scooters). The Electric Vehicles (EVs) segment will dominate the market because electric vehicle production needs substantial amounts of advanced lithium-ion batteries and their chemical components. Automotive manufacturers across Asia-Pacific are increasing investments in battery production facilities to support the transition toward electric mobility. Countries including China India South Korea and Japan have established government policies to promote electric vehicle adoption through subsidies and manufacturing incentives and emissions reduction targets. The initiatives create strong demand for battery chemicals which are essential in the production of EV batteries.

Competitive Landscape

Key participants in the Asia Pacific Battery Chemicals Localization Readiness market include Ganfeng Lithium Group Co., Ltd., Tianqi Lithium Corporation, Contemporary Amperex Technology Co., Limited, BYD Company Ltd., Sumitomo Metal Mining Co., Ltd., Mitsubishi Chemical Group Corporation, LG Chem Ltd., POSCO Future M Co., Ltd., BASF SE, Umicore N.V., Nichia Corporation, Jiangxi Special Electric Motor Co., Ltd., and Other Prominent Players.

These companies are implementing strategic growth initiatives in order to gain a competitive advantage. The strategies being largely adopted include mergers and acquisitions, strategic alliances, joint ventures, licensing agreements, and new product launches. With the implementation of these strategies, the market participants aim to increase product portfolios, as well as enhance regional presence for long-term sustainable business growth in the Battery Chemicals Localization Readiness industry of Asia Pacific.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | Asia Pacific |

| Product/ Service Segmentation | Chemical Type, Battery Type, Supply Chain Stage, End-Use Industry |

| Key Players | Ganfeng Lithium Group Co., Ltd., Tianqi Lithium Corporation, Contemporary Amperex Technology Co., Limited, BYD Company Ltd., Sumitomo Metal Mining Co., Ltd., Mitsubishi Chemical Group Corporation, LG Chem Ltd., POSCO Future M Co., Ltd., BASF SE, Umicore N.V., Nichia Corporation, Jiangxi Special Electric Motor Co., Ltd., and Other Prominent Players. |

Market Segmentation

- By Chemical Type

- Lithium Chemicals

- Nickel Chemicals

- Cobalt Chemicals

- Manganese Chemicals

- Electrolyte Chemicals

- Others

- By Battery Type

- Lithium-ion Batteries

- Lithium Iron Phosphate (LFP) Batteries

- Nickel Manganese Cobalt (NMC) Batteries

- Nickel Cobalt Aluminum (NCA) Batteries

- Solid-State Batteries

- By Supply Chain Stage

- Raw Material Processing

- Chemical Refining

- Cathode & Anode Material Production

- Electrolyte Production

- Battery Cell Manufacturing Integration

- By End-Use Industry

- Electric Vehicles (EVs)

- Consumer Electronics

- Energy Storage Systems (ESS)

- Industrial Equipment

- E-Mobility (E-bikes, E-scooters)

- By Country

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- Indonesia

- Malaysia

- Singapore

- Vietnam

- Rest of Asia Pacific

Asia Pacific Battery Chemicals Localization Readiness Market, 2032

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- Asia Pacific Battery Chemicals Localization Readiness Market Insights

- Growth Drivers

- Restraints

- Opportunities

- Challenges

- Localization feasibility

- Technology Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Industry Value Chain & Entry Points

- Asia Pacific Battery Chemicals Localization Readiness Market: Regulatory Framework

- Asia Pacific Battery Chemicals Localization Readiness Market: Marketing Strategies

- Asia Pacific Battery Chemicals Localization Readiness Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- Lithium Chemicals

- Nickel Chemicals

- Cobalt Chemicals

- Manganese Chemicals

- Electrolyte Chemicals

- Others

- By Battery Type

- Lithium-ion Batteries

- Lithium Iron Phosphate (LFP) Batteries

- Nickel Manganese Cobalt (NMC) Batteries

- Nickel Cobalt Aluminum (NCA) Batteries

- Solid-State Batteries

- By Supply Chain Stage

- Raw Material Processing

- Chemical Refining

- Cathode & Anode Material Production

- Electrolyte Production

- Battery Cell Manufacturing Integration

- By End-Use Industry

- Electric Vehicles (EVs)

- Consumer Electronics

- Energy Storage Systems (ESS)

- Industrial Equipment

- E-Mobility (E-bikes, E-scooters)

- By Country

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- Indonesia

- Malaysia

- Singapore

- Vietnam

- Rest of Asia Pacific

- By Chemical Type

- Market Size & Forecast, 2021-2032

- China Battery Chemicals Localization Readiness Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Supply Chain Stage

- By End-Use Industry

- Market Size & Forecast, 2021-2032

- India Battery Chemicals Localization Readiness Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Supply Chain Stage

- By End-Use Industry

- Japan Battery Chemicals Localization Readiness Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Supply Chain Stage

- By End-Use Industry

- South Korea Battery Chemicals Localization Readiness Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Supply Chain Stage

- By End-Use Industry

- Australia & New Zealand Battery Chemicals Localization Readiness Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Supply Chain Stage

- By End-Use Industry

- Indonesia Battery Chemicals Localization Readiness Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Supply Chain Stage

- By End-Use Industry

- Malaysia Battery Chemicals Localization Readiness Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Supply Chain Stage

- By End-Use Industry

- Singapore Battery Chemicals Localization Readiness Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Supply Chain Stage

- By End-Use Industry

- Vietnam Battery Chemicals Localization Readiness Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Supply Chain Stage

- By End-Use Industry

- Rest of Asia Pacific Battery Chemicals Localization Readiness Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Supply Chain Stage

- By End-Use Industry

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution by End-Use Industry

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List of Key Players and Their Offerings

- Asia Pacific Battery Chemicals Localization Readiness Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, etc.)

- Geopolitical Impact on Asia Pacific Battery Chemicals Localization Readiness Market

- Company Profile

- Ganfeng Lithium Group Co., Ltd.

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Ganfeng Lithium Group Co., Ltd.

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

- Market Size & Forecast, 2021-2032

**(same data pointers will be provided for the below companies)

- Tianqi Lithium Corporation

- Contemporary Amperex Technology Co., Limited

- BYD Company Ltd.

- Sumitomo Metal Mining Co., Ltd.

- Mitsubishi Chemical Group Corporation

- LG Chem Ltd.

- POSCO Future M Co., Ltd.

- BASF SE

- Umicore N.V.

- Nichia Corporation

- Jiangxi Special Electric Motor Co., Ltd.

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown of Primary Research Respondents, By Region

- Assumption & Limitation

- Qualitative Research

* Financial information in case of non-listed companies will be provided as per availability

**The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. What is the expected growth rate of the Asia Pacific Battery Chemicals Localization Readiness Market during the forecast period?

Ans: The Asia Pacific Battery Chemicals Localization Readiness Market size was estimated at USD 21.4 billion in 2025.

2. What is the expected growth rate of the Asia Pacific Battery Chemicals Localization Readiness Market during the forecast period?

Ans: Asia Pacific Battery Chemicals Localization Readiness Market is expected to grow at a CAGR of around 14.6% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Asia Pacific Battery Chemicals Localization Readiness Market by 2032?

Ans: The Asia Pacific Battery Chemicals Localization Readiness Market is projected to reach a value of approximately USD 55.2 billion by 2032.

4. What are the major factors driving the growth of the Asia Pacific Battery Chemicals Localization Readiness Market?

Ans: The growth of electric vehicle manufacturing and the development of gigafactories and the increasing need for energy storage solutions throughout the area will create this growth.

5. Name the key players operating in the Asia Pacific Battery Chemicals Localization Readiness Market.

Ans: The key players of Asia Pacific Battery Chemicals Localization Readiness Market are Ganfeng Lithium Group Co., Ltd., Tianqi Lithium Corporation, Contemporary Amperex Technology Co., Limited, BYD Company Ltd., Sumitomo Metal Mining Co., Ltd., Mitsubishi Chemical Group Corporation, LG Chem Ltd., POSCO Future M Co., Ltd., BASF SE, Umicore N.V., Nichia Corporation, Jiangxi Special Electric Motor Co., Ltd., and Other Prominent Players.

6. Which is the fastest-growing end-use industry segment in the Asia Pacific Battery Chemicals Localization Readiness Market?

Ans: The Electric Vehicles (EVs) segment will dominate the market because electric vehicle production needs substantial amounts of advanced lithium-ion batteries and their chemical components..

7. Which country contributes significantly to the growth of the Asia Pacific Battery Chemicals Localization Readiness Market?

Ans: The Asia-Pacific Battery Chemicals Localization Readiness Market will see major growth in China throughout the forecast period because the country currently leads the world in battery production and electric vehicle development.

Frequently Asked Questions

1. What is the expected growth rate of the Asia Pacific Battery Chemicals Localization Readiness Market during the forecast period?

Ans: The Asia Pacific Battery Chemicals Localization Readiness Market size was estimated at USD 21.4 billion in 2025.

2. What is the expected growth rate of the Asia Pacific Battery Chemicals Localization Readiness Market during the forecast period?

Ans: Asia Pacific Battery Chemicals Localization Readiness Market is expected to grow at a CAGR of around 14.6% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Asia Pacific Battery Chemicals Localization Readiness Market by 2032?

Ans: The Asia Pacific Battery Chemicals Localization Readiness Market is projected to reach a value of approximately USD 55.2 billion by 2032.

4. What are the major factors driving the growth of the Asia Pacific Battery Chemicals Localization Readiness Market?

Ans: The growth of electric vehicle manufacturing and the development of gigafactories and the increasing need for energy storage solutions throughout the area will create this growth.

5. Name the key players operating in the Asia Pacific Battery Chemicals Localization Readiness Market.

Ans: The key players of Asia Pacific Battery Chemicals Localization Readiness Market are Ganfeng Lithium Group Co., Ltd., Tianqi Lithium Corporation, Contemporary Amperex Technology Co., Limited, BYD Company Ltd., Sumitomo Metal Mining Co., Ltd., Mitsubishi Chemical Group Corporation, LG Chem Ltd., POSCO Future M Co., Ltd., BASF SE, Umicore N.V., Nichia Corporation, Jiangxi Special Electric Motor Co., Ltd., and Other Prominent Players.

6. Which is the fastest-growing end-use industry segment in the Asia Pacific Battery Chemicals Localization Readiness Market?

Ans: The Electric Vehicles (EVs) segment will dominate the market because electric vehicle production needs substantial amounts of advanced lithium-ion batteries and their chemical components..

7. Which country contributes significantly to the growth of the Asia Pacific Battery Chemicals Localization Readiness Market?

Ans: The Asia-Pacific Battery Chemicals Localization Readiness Market will see major growth in China throughout the forecast period because the country currently leads the world in battery production and electric vehicle development.