Global Green Hydrogen Market, By Production Pathway (Alkaline Electrolysis, PEM Electrolysis, Solid Oxide Electrolysis (SOEC), Anion Exchange Membrane (AEM), Biomass/Waste-to-Hydrogen with Renewable Power, Other Emerging Routes); By Renewable Power Source (Solar-to-H2, Wind-to-H2, Hydro-to-H2, Hybrid RE Systems, Grid-Connected Low-Carbon Mix); By Delivery & Storage Form (Compressed Gaseous Hydrogen, Liquid Hydrogen (LH2), Ammonia (NH3) Carrier, Liquid Organic Hydrogen Carriers (LOHC), Pipeline/On-Site Supply); By End-Use Sector (Green Ammonia & Fertilizers, Refining & Petrochemicals, Steel & Metals (DRI-EAF), Heavy-Duty Mobility (Trucks, Buses), Marine & Aviation E-Fuels, Power Generation & Grid Balancing, Industrial Heat & Process Applications); By Project Scale (On-Site Captive, Regional Hub/Cluster, Export-Oriented Mega Projects); By Commercial Model (Merchant Supply, Offtake/Contracted Supply, Hydrogen-as-a-Service, Integrated Producer–Consumer, Government-Backed CfD/Auction Models); By Region (North America, Europe, Asia Pacific (APAC), Latin America (LATAM), Middle East and Africa (MEA)); By Trend Analysis, Policy & Incentive Landscape, Competitive Landscape & Forecast, 2022–2032

- Chemicals & Advanced Materials

- Mar 2026

- Pages 300

- Report Format: pdf

- Report Price: $3500 USD

Global Green Hydrogen Market, Size & Forecast 2022–2032

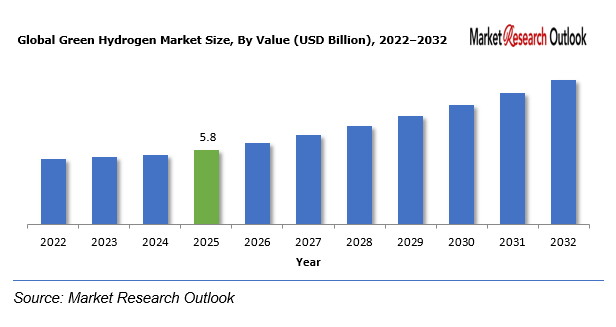

The Global Green Hydrogen Market size was estimated to reach USD 5.8 Billion in 2025. The market is expected to grow at a CAGR of 48.9% during the forecast period and reach USD 118.7 Billion by 2032. The market is growing due to increasing net-zero targets, strengthened requirements for industrial decarbonization, and robust policy support measures, such as production support, hydrogen auctions/CfDs, and renewable energy subsidies.

In order to increase the number of green hydrogen projects and close the cost gap to grey hydrogen, various project developers and equipment manufacturers are working to increase the production scale of electrolyzers, increase the stack efficiency of electrolyzers, and optimize the levelized cost of hydrogen production through access to low-cost renewable electricity and higher utilization rates. In addition, offtake-driven project structuring is becoming more advanced, including the use of long-term contracts, index-linked hydrogen pricing, hydrogen clusters, and green ammonia/e-fuels production to make the market more bankable while maintaining affordability for industry and mobility applications.

Green Hydrogen Market – Overview

Green hydrogen is basically hydrogen made using clean electricity. Instead of producing hydrogen from fossil fuels, companies split water into hydrogen and oxygen using electrolysis powered by renewables like solar, wind, or hydro. This matters because it can help cut emissions in sectors where decarbonization is genuinely hard, like steel, chemicals, refining, shipping, and heavy transport, either by replacing fossil-based hydrogen or by enabling low-carbon fuels and feedstocks.

That said, it isn’t “cheap and easy” yet. The business case depends heavily on the cost of renewable power, the upfront cost of electrolyzers, access to water and treatment, and the extra cost of storing and moving hydrogen (compressing it, liquefying it, or converting it to carriers like ammonia). On top of that, many regions still need new infrastructure, pipelines, terminals, conversion facilities, and refueling networks. As projects scale up, developers are increasingly leaning on long-term offtake contracts, government-backed support schemes, and hub-style supply chains to reduce risk and make projects financeable.

Global Green Hydrogen Market: Growth Drivers

Stronger climate policies and net-zero push

Across the world, governments are tightening emissions rules and rolling out hydrogen-focused programs, especially for industry and heavy mobility. Tools like carbon pricing, clean fuel standards, renewable hydrogen targets, and financial support (tax credits, grants, auctions, and contracts-for-difference) are helping improve project economics and close the gap versus grey hydrogen. At the same time, large industrial buyers, refineries, ammonia producers, steelmakers, and chemical companies, are under pressure to meet decarbonization targets, so more of them are signing long-term contracts to lock in future green hydrogen supply.

Renewables + Electrolyzers are Scaling Fast

The biggest lever for cheaper green hydrogen is cheaper, reliable renewable electricity, and that’s improving in many markets. At the same time, electrolyzer technology is getting better and factories are scaling up production, which should bring costs down over time. New designs, higher efficiency, modular systems, and “learning-by-doing” from larger projects are pushing the market forward. Another big accelerator is the rise of hydrogen hubs, projects that combine renewables, electrolysis, storage, and big local customers in one ecosystem, because that boosts utilization and lowers the delivered cost.

Challenges

High Delivered Cost and Tougher Project Financing

Even with all the momentum, green hydrogen is still more expensive than conventional hydrogen in most places unless it gets policy support. Financing is also not straightforward: power prices can be volatile, electrolyzer performance over long periods is still being proven at scale, permitting can be slow, and many projects struggle to secure strong offtake agreements at prices buyers will accept. Storage and transport also add significant cost, especially for export projects where hydrogen is shipped as liquid hydrogen, ammonia, or LOHC.

Infrastructure and Demand Readiness Are Still Catching Up

Hydrogen needs supporting infrastructure, pipelines, terminals, ammonia cracking, and refueling, much of which is still limited or in early development. On the customer side, many end users must modify equipment, update safety systems, and adapt processes before they can consume hydrogen at scale. This means real adoption can move slower than policy roadmaps suggest. On top of that, certification rules and guarantees-of-origin differ across regions, which complicates cross-border trade and even the definition of what qualifies as “renewable” hydrogen.

Geopolitical Impact on the Global Green Hydrogen Market

Green hydrogen is becoming strategic, not just commercial. Countries are competing for leadership in electrolyzer supply chains and for access to critical materials used in electrolyzers and renewable infrastructure. Trade policies, energy security priorities, and competition for low-cost renewable resources are shaping where projects get built and who becomes an exporter.

Export plans in regions like the Middle East, Australia, Latin America, and parts of Africa depend on shipping routes, port readiness, and changing import standards, especially in Europe and parts of Asia. Meanwhile, power market instability, grid constraints, and differences in policy definitions (for example, what counts as “renewable” hydrogen and how certification works) can make some regions far more competitive than others. From 2026 to 2032, we’re likely to see more cross-border hydrogen deals and hub development, but also more strategic competition for technology, capital, and long-term offtake commitments.

Global Green Hydrogen Market: Segmental Coverage

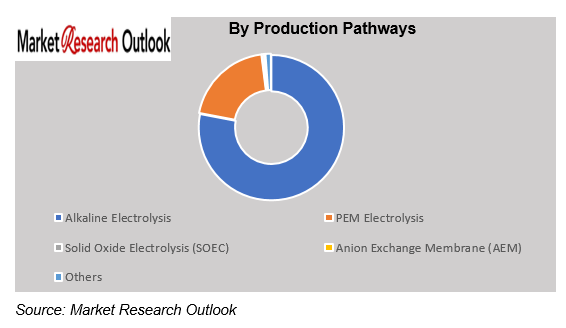

Global Green Hydrogen Market – By Production Pathway

Alkaline electrolysis is currently the most widely deployed route for green hydrogen because it is mature, well-understood, and generally the most cost-effective to scale. The technology benefits from a long operating history, a broad base of suppliers, and standardized system designs that make engineering, procurement, and financing easier. It is particularly attractive for large projects aiming for low levelized hydrogen cost, especially where developers can secure stable, low-cost renewable power and operate the electrolyzer at high utilization. The main limitation is that alkaline systems are typically less flexible than newer technologies when it comes to fast ramping and frequent start-stop operation, which can matter when renewable power supply is highly variable without buffering.

PEM electrolysis is gaining traction because it is better suited to dynamic operation. It can ramp quickly and respond smoothly to fluctuating renewable electricity, making it a strong fit for projects connected to variable solar and wind profiles or for configurations where grid services and operational flexibility create additional value. PEM systems are also compact and can be easier to integrate into space-constrained industrial sites, hydrogen hubs, or mobility-oriented supply chains. The trade-off is that PEM has historically faced higher equipment costs and greater dependence on specialized components, which can influence both capex and supply chain risk.

Solid oxide electrolysis is emerging as a promising option where high-temperature heat integration is possible. Its value proposition is centered on potentially higher efficiency when paired with industrial waste heat or dedicated high-temperature energy sources. This makes it especially interesting for integrated industrial clusters where heat and hydrogen demand coexist. However, it remains early in commercialization due to challenges around long-term durability, materials stability under thermal cycling, and the need for stronger operating track records at large scale before lenders and offtakers are fully comfortable.

Anion exchange membrane electrolysis sits even earlier in the adoption curve and is often viewed as a “next-generation” pathway aiming to combine cost advantages with operational flexibility. In theory, it can reduce reliance on expensive materials while still supporting responsive operation, which would be ideal for renewable-driven hydrogen production. In practice, most deployments are still at pilot or demonstration scale, with ongoing work needed to prove performance consistency, lifetime, and bankability under real-world operating conditions.

Biomass or waste-to-hydrogen routes paired with renewable power occupy a niche because their feasibility is highly location-specific. These pathways can be compelling where there is reliable access to suitable feedstocks, supportive waste management economics, and policy incentives that reward circularity or emissions reductions. At the same time, they introduce added complexity, feedstock logistics, permitting, contaminants management, and consistency of output, which can make scaling more challenging than electrolysis-based projects that primarily depend on electricity and water inputs.

Other emerging routes remain concentrated in research, pilot projects, and early demonstrations. They include novel electrochemical concepts, hybrid processes, and breakthrough approaches that could improve efficiency, reduce system cost, or simplify storage and transport integration. While these alternatives are not yet meaningful contributors to near-term supply, they matter strategically because they broaden the technology pipeline and could unlock step-changes in economics if technical hurdles, scale-up, and reliability validation are successfully achieved.

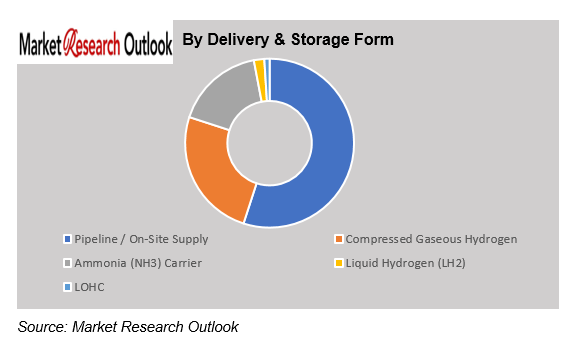

Global Green Hydrogen Market – By Delivery & Storage Form

In the near-term green hydrogen market, pipeline and on-site supply models dominate because most early projects are being built around “make-and-use” economics, hydrogen is produced close to where it will be consumed, especially in industrial clusters such as refineries, ammonia plants, steel sites, and chemical parks. This approach minimizes the biggest cost and complexity drivers in hydrogen commercialization: storage, long-distance transport, and repeated handling. Where demand is concentrated and predictable, short pipelines or dedicated on-site systems also offer the most straightforward pathway for safety approvals, permitting, and bankable offtake structures, which is why they are preferred in the first wave of deployment.

Compressed gaseous hydrogen remains the most common non-pipeline option for local distribution and smaller volumes. It fits well with decentralized demand, mobility refueling, distributed industrial users, backup supply, and early-stage hub networks, because compression is a mature technology and does not require major conversion infrastructure. The tradeoff is economics: once volumes rise or distances increase, compression and cylinder/trailer logistics become expensive, energy-intensive, and operationally cumbersome compared with pipelines or chemical carriers. As a result, compressed gas plays a key bridging role, useful for pilots and early commercial rollouts, but less competitive for large-scale, long-distance delivery.

For longer-distance movement and future international trade, ammonia is emerging as the most practical carrier because it benefits from established global infrastructure and decades of operational know-how in storage, handling, and shipping. Converting hydrogen into ammonia improves volumetric energy density and makes transport easier than moving gaseous hydrogen, particularly across oceans. It also has direct end-use demand in fertilizers and can serve as a feedstock for e-fuels, which strengthens its case beyond being only a transport medium. The main constraint is that the value chain becomes more complex, ammonia synthesis adds capex and energy losses, and “cracking” ammonia back into hydrogen requires additional investment, efficiency penalties, and purity management. Even so, the maturity of ammonia logistics makes it the leading pathway for cross-border hydrogen trade strategies.

Liquid hydrogen remains comparatively limited because liquefaction is energy-intensive, technically demanding, and requires specialized cryogenic infrastructure across the entire chain, production, storage, transport, and end-use handling. While it offers advantages for high-density storage and may fit specific applications (particularly some mobility and aerospace-adjacent use cases), the overall cost and infrastructure burden slows broader adoption. Liquid hydrogen is expected to grow selectively where the value of compact storage is high and where dedicated cryogenic ecosystems can be built.

LOHC pathways are still in the early commercial stage and tend to be pursued where users want a liquid-like logistics model that leverages existing fuel handling practices. LOHC can simplify storage and transport from a safety and handling perspective, but it introduces additional conversion steps, hydrogenation and dehydrogenation, each adding cost, equipment, and efficiency losses. As a result, LOHC is best viewed as a niche solution today, with potential to expand in specific corridors or applications if technology improvements reduce losses, improve catalyst performance, and make the economics more competitive versus ammonia and liquid hydrogen.

Competitive Landscape

Key participants in the Global Green Hydrogen market span the full value chain, renewable developers, hydrogen project developers/integrators, electrolyzer OEMs, industrial gas majors, and downstream offtakers in ammonia, refining, steel, and mobility. On the project development side, the landscape includes large-scale renewable and energy players such as Air Products, ACWA Power / NEOM Green Hydrogen Company, ENGIE, Iberdrola, Ørsted, Shell, bp, TotalEnergies, Masdar, and Fortescue (among others), who are building hub-based projects and export-linked green ammonia platforms, often in partnership with industrial customers and governments.

Competition is equally shaped by electrolyzer technology leaders across alkaline, PEM, and emerging platforms. Prominent electrolyzer manufacturers and technology providers include thyssenkrupp nucera, Nel, Siemens Energy, ITM Power, Cummins/Accelera, Plug Power, LONGi, Asahi Kasei, Sunfire (SOEC), and Bloom Energy (solid oxide systems), with differentiation driven by stack efficiency, dynamic performance, footprint, lifetime/availability, manufacturing scale, and bankable track records.

Across the market, companies are pursuing strategic growth initiatives such as partnership-led hub development, joint ventures with offtakers, technology licensing, local manufacturing scale-up, and M&A/alliances to secure supply chains and accelerate commercialization. A defining competitive factor is the ability to structure bankable projects, typically via long-term offtake agreements, policy-backed pricing mechanisms (auctions/CfDs), and integrated renewable power sourcing that locks in delivered cost and reduces volatility.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2022–2024

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2027–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | Global |

| Product/ Service Segmentation | Production pathway, renewable power source, delivery & storage form, end-use sector, project scale, commercial model, and region |

| Key Players | Air Products, ACWA Power / NEOM Green Hydrogen Company, ENGIE, Iberdrola, Ørsted, Shell, bp, TotalEnergies, Masdar, and Fortescue (among others) |

Market Segmentation

- By Production Pathway

- Alkaline Electrolysis

- PEM Electrolysis

- Solid Oxide Electrolysis (SOEC)

- Anion Exchange Membrane (AEM)

- Biomass/Waste-to-Hydrogen with Renewable Power

- Other Emerging Routes

- By Renewable Power Source

- Solar-to-H2

- Wind-to-H2

- Hydro-to-H2

- Hybrid Renewable Systems

- Grid-Connected Low-Carbon Mix

- By Delivery & Storage Form

- Compressed Gaseous Hydrogen

- Liquid Hydrogen (LH2)

- Ammonia (NH3) Carrier

- Liquid Organic Hydrogen Carriers (LOHC)

- Pipeline / On-Site Supply

- By End-Use Sector

- Green Ammonia & Fertilizers

- Refining & Petrochemicals

- Steel & Metals (DRI-EAF)

- Heavy-Duty Mobility (Trucks, Buses)

- Marine & Aviation E-Fuels

- Power Generation & Grid Balancing

- Industrial Heat & Process Applications

- By Project Scale

- On-Site Captive

- Regional Hub / Cluster

- Export-Oriented Mega Projects

- By Commercial Model

- Merchant Supply

- Offtake / Contracted Supply

- Hydrogen-as-a-Service

- Integrated Producer–Consumer

- Government-Backed CfD / Auction Models

- By Region

- North America

- Europe

- Asia Pacific (APAC)

- Latin America (LATAM)

- Middle East & Africa (MEA)

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- Global Green Hydrogen Market Insights

- Growth Drivers

- Restraints

- Opportunities

- Challenges

- Technological Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Industry Value Chain & Entry Points

- Global Green Hydrogen Market Regulatory Framework

- Global Green Hydrogen Market Marketing Strategies

- Global Green Hydrogen Market Pricing Analysis & Consumer Response Modeling

- Global Green Hydrogen Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Production Pathway

- Alkaline Electrolysis

- PEM (Proton Exchange Membrane) Electrolysis

- Solid Oxide Electrolysis (SOEC)

- Anion Exchange Membrane (AEM) Electrolysis

- Biomass / Waste-to-Hydrogen with Renewable Power

- Other Emerging Hydrogen Production Routes

- By Renewable Power Source

- Solar-to-Hydrogen (Solar-to-H2)

- Wind-to-Hydrogen (Wind-to-H2)

- Hydro-to-Hydrogen (Hydro-to-H2)

- Hybrid Renewable Energy Systems (Solar + Wind + Storage, etc.)

- Grid-Connected Low-Carbon Mix (with Additionality/Certification)

- By Delivery & Storage Form

- Pipeline / On-Site Supply

- Compressed Gaseous Hydrogen

- Liquid Hydrogen (LH2)

- Ammonia (NH3) as Hydrogen Carrier

- Liquid Organic Hydrogen Carriers (LOHC)

- By End-Use Sector

- Green Ammonia & Fertilizers

- Refining & Petrochemicals

- Steel & Metals (DRI-EAF and Industrial Reduction)

- Heavy-Duty Mobility (Trucks, Buses)

- Marine & Aviation E-Fuels (SAF, e-methanol, e-ammonia)

- Power Generation & Grid Balancing

- Industrial Heat & Process Applications

- By Commercial Model

- Merchant Supply (Spot / Short-Term Sales)

- Offtake / Long-Term Contracted Supply

- Hydrogen-as-a-Service (HaaS)

- Integrated Producer–Consumer (Captive / Backward-Integrated)

- Government-Backed CfD / Auction / Subsidy-Linked Models

- By Region

- North America

- Europe

- Asia Pacific (APAC)

- Latin America (LATAM)

- Middle East and Africa (MEA)

- By Production Pathway

- Market Size & Forecast, 2021-2032

- North America Green Hydrogen Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- By Country

- United States

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Canada

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Europe Green Hydrogen Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- By Country

- Germany

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- United Kingdom

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Italy

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- France

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Spain

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Belgium

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Russia

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- The Netherlands

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Rest of Europe

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Asia Pacific Green Hydrogen Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- By Country

- China

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- India

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Japan

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- South Korea

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Australia & New Zealand

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Indonesia

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Malaysia

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Singapore

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Vietnam

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Rest of APAC

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Latin America Green Hydrogen Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- By Country

- Brazil

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Mexico

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Argentina

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Peru

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Rest of LATAM

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Middle East & Africa Green Hydrogen Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- By Country

- Saudi Arabia

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- UAE

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Qatar

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Kuwait

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- South Africa

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Nigeria

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Algeria

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Rest of MEA

- By Production Pathways

- By Renewable Power Source

- By Delivery & Storage Form

- By End Use Sector

- By Commercial Model

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution By Commercial Model

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List of Key Players and Their Products

- Global Green Hydrogen Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Developments (Mergers, Acquisitions, Partnerships, etc.)

- Geopolitical Impact on Global Green Hydrogen Market

- Company Profile

- Amcor plc

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Amcor plc

- Saudi Arabia

- Market Size & Forecast, 2021-2032

- Brazil

- Market Size & Forecast, 2021-2032

- China

- Market Size & Forecast, 2021-2032

- Germany

- Market Size & Forecast, 2021-2032

- United States

- Market Size & Forecast, 2021-2032

**(same data pointers will be provided for the below companies)

- Berry Global Inc.

- Tetra Pak International S.A.

- Mondi Group

- Smurfit Westrock (WestRock + Smurfit Kappa)

- DS Smith Plc

- Sealed Air Corporation

- Huhtamaki Oyj

- Sonoco Products Company

- Ball Corporation

- Crown Holdings, Inc.

- International Paper Company

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown of Primary Research Respondents, By Region

- Assumptions & Limitations

- Qualitative Research

*Financial information of case of non-listed companies can be provided as per availability.

**The segmentation and the companies are subject to modifications based on in-depth secondary research for the final deliverable

Frequently Asked Questions

1. What is the Global Green Hydrogen Market?

Ans: It covers hydrogen produced via electrolysis using renewable electricity and delivered to end users either locally (on-site/pipeline) or through storage and transport carriers such as ammonia, LH2, or LOHC.

2. What is driving green hydrogen adoption globally?

Ans: Stronger decarbonization mandates, policy incentives, renewable expansion, and demand pull from hard-to-abate sectors such as ammonia, refining, steel, and heavy transport.

3. Who are the key players in the market?

Ans: The ecosystem includes major project developers (renewables + energy majors), industrial gas leaders, and electrolyzer OEMs such as Air Products, ACWA Power/NEOM, ENGIE, Iberdrola, Shell, and electrolyzer manufacturers such as thyssenkrupp nucera, Nel, Siemens Energy, ITM Power, Plug Power, Cummins/Accelera, and others.

4. What are the biggest competitive differentiators?

Ans: Access to low-cost renewable electricity, ability to secure long-term offtake, electrolyzer performance and reliability, speed of permitting/execution, and integration across conversion (ammonia/e-fuels), storage, and logistics.

5. Which regions are most active?

Ans: Activity is concentrated in regions combining strong policy support with renewables potential and industrial demand, especially Europe, parts of APAC, North America, and export-led MEA and Australia-linked corridors (project-specific).

Frequently Asked Questions

1. What is the Global Green Hydrogen Market?

Ans: It covers hydrogen produced via electrolysis using renewable electricity and delivered to end users either locally (on-site/pipeline) or through storage and transport carriers such as ammonia, LH2, or LOHC.

2. What is driving green hydrogen adoption globally?

Ans: Stronger decarbonization mandates, policy incentives, renewable expansion, and demand pull from hard-to-abate sectors such as ammonia, refining, steel, and heavy transport.

3. Who are the key players in the market?

Ans: The ecosystem includes major project developers (renewables + energy majors), industrial gas leaders, and electrolyzer OEMs such as Air Products, ACWA Power/NEOM, ENGIE, Iberdrola, Shell, and electrolyzer manufacturers such as thyssenkrupp nucera, Nel, Siemens Energy, ITM Power, Plug Power, Cummins/Accelera, and others.

4. What are the biggest competitive differentiators?

Ans: Access to low-cost renewable electricity, ability to secure long-term offtake, electrolyzer performance and reliability, speed of permitting/execution, and integration across conversion (ammonia/e-fuels), storage, and logistics.

5. Which regions are most active?

Ans: Activity is concentrated in regions combining strong policy support with renewables potential and industrial demand, especially Europe, parts of APAC, North America, and export-led MEA and Australia-linked corridors (project-specific).