Global Chemical Supply Chain Disruptions & Cost Pass-Through Market, By Chemical Type (Petrochemicals, Specialty Chemicals, Agrochemicals, Industrial Gases, Polymers & Resins); By Disruption Type (Raw Material Shortage, Logistics & Transportation Bottlenecks, Geopolitical Trade Restrictions, Energy Price Volatility, Natural Disasters & Climate Events); By Cost Pass-Through Level (Full Cost Pass-Through, Partial Cost Pass-Through, Low / Delayed Pass-Through); By Supply Chain Stage (Upstream (Feedstock & Raw Materials), Midstream (Processing & Manufacturing), Downstream (Distribution & End-Use Industries)); By End-Use Industry (Automotive, Construction, Electronics, Pharmaceuticals, Agriculture, Consumer Goods); By Region (North America, Europe, Asia Pacific (APAC), Latin America (LATAM), Middle East and Africa (MEA)); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Chemicals & Advanced Materials

- Mar 2026

- Pages 350

- Report Format: pdf

- Report Price: $3500 USD

Global Chemical Supply Chain Disruptions & Cost Pass-Through Market, Size & Forecast 2021-2032

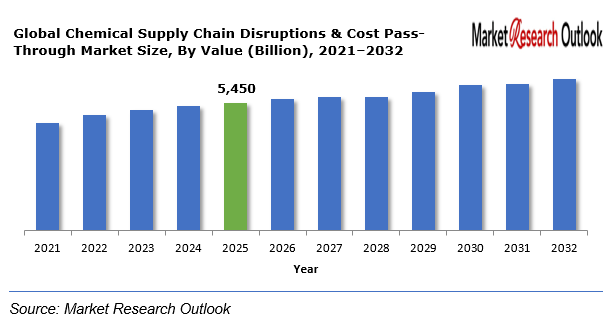

The Global Chemical Supply Chain Disruptions & Cost Pass-Through Market size was estimated at USD 5,450 Billion in 2025. During the forecast period, the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market size is projected to grow at a CAGR of 6.8% reaching a value of USD 8,650 Billion by 2032. Growth occurs because worldwide demand for petrochemicals and polymers and specialty chemicals used in automotive and electronics and pharmaceutical and consumer goods industries continues to increase. Supply chain disruptions occur repeatedly because of container shortages and port congestion and raw material shortages and energy crises which result in regional cost structure changes. The main factor that will determine long-term competitive advantage during the entire testing period will depend on a company’s capacity to control its pricing strategies while maintaining consistent supply chain operations.

Chemical Supply Chain Disruptions & Cost Pass-Through – Overview

Chemical supply chain disruptions occur when essential operations that handle feedstock sourcing and processing and distribution face interruptions or operational problems. The disruptions emerge from four main sources which include geopolitical conflicts and energy price surges and climate-related disasters and changes in global trade policies. Cost pass-through exists when chemical producers transfer their increased production expenses to downstream customers through their pricing methods.

Global Chemical Supply Chain Disruptions & Cost Pass-Through Market

Growth Drivers

Rising Feedstock Price Volatility and Energy Market Fluctuations

Global petrochemical production expenses face major challenges because crude oil and natural gas price fluctuations create market instability. Price changes in upstream petrochemical markets quickly affect the entire production process because petrochemicals function as basic materials for plastics and resins and synthetic materials. Geopolitical conflicts that disrupt energy-exporting countries currently create unpredictable patterns in feedstock price movements. The rising demand from electric vehicle production and renewable energy infrastructure development and semiconductor manufacturing operations leads to increased usage of specialty chemicals and polymers which causes supply-demand imbalances to tighten.

Challenges

Margin Compression and Limited Pricing Power in Downstream Segments

Integrated chemical production facilities have the ability to use dynamic pricing systems while midstream processing operations and specialty manufacturing plants face difficulties because their contracts prevent them from making pricing changes. Businesses experience decreased profit margins when their material expenses increase at a quick rate. The combination of transportation delays and container shortages and port congestion issues creates additional financial burdens which affect export-dependent markets throughout Asia Pacific and Europe.

Geopolitical Impact on Global Chemical Supply Chain Disruptions & Cost Pass-Through Market

The market reacts strongly to geopolitical changes which include trade barriers and sanctions and international tariff regulations. Export controls on petrochemical feedstocks and specialty chemicals can disrupt global supply balances and lead to sudden pricing adjustments. Regional conflicts involving major energy-production countries generate disruptions that impact chemical manufacturing centers. The European and North American environmental regulations together with carbon border adjustment mechanisms are creating new trade routes which will shape international commerce. Manufacturers are increasingly relocating or diversifying production facilities to regions with favorable regulatory frameworks and stable energy access.

Global Chemical Supply Chain Disruptions & Cost Pass-Through Market

Segmental Coverage

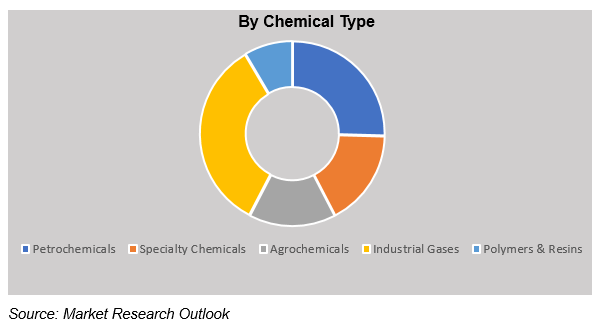

Global Chemical Supply Chain Disruptions & Cost Pass-Through Market – By Chemical Type

Based on chemical type, the market is segmented into Petrochemicals, Specialty Chemicals, Agrochemicals, Industrial Gases, and Polymers & Resins. Petrochemicals maintain their leading market position because manufacturing industries use them extensively while crude oil and natural gas prices create market uncertainties. The specialty chemicals market shows continuous expansion because high-value applications in electronics and pharmaceuticals and advanced materials drive demand. The demand for agrochemicals follows seasonal patterns while trade regulations impact availability. The semiconductor fabrication industry and healthcare infrastructure development drive industrial gases market growth. The pricing of polymers and resins products depends on two main factors which include feedstock availability and sustainability regulations.

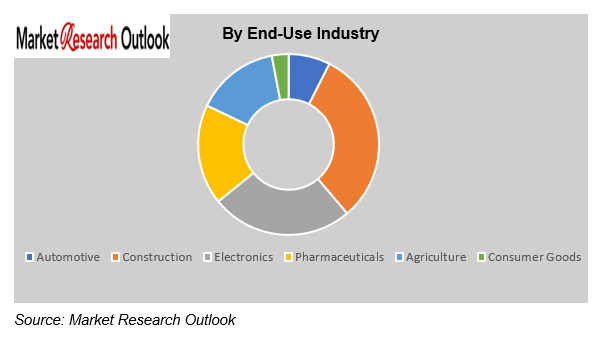

Global Chemical Supply Chain Disruptions & Cost Pass-Through Market – By End-Use Industry

Based on end-use industry, the market is segmented into Automotive, Construction, Electronics, Pharmaceuticals, Agriculture, and Consumer Goods. The Automotive and Electronics industries face major problems when supply chains break down because of their use of just-in-time manufacturing processes and their need for specialized materials. The Pharmaceutical and Agricultural industries depend on steady chemical deliveries to produce active ingredients and fertilizers, which makes cost pass-through methods essential for maintaining profit margins. Consumer Goods manufacturers face retail competition, which drives down prices and forces them to pass on chemical price increases to customers who supply their materials.

Competitive Landscape

Key participants in the Global Chemical Supply Chain Disruptions & Cost Pass-Through market include BASF SE, Dow Inc., SABIC, LyondellBasell Industries N.V., INEOS Group Holdings S.A., ExxonMobil Chemical Company, Shell Chemicals, DuPont de Nemours, Inc., Evonik Industries AG, LG Chem Ltd., Mitsubishi Chemical Group Corporation, Sumitomo Chemical Co., Ltd., and other prominent players.

These companies are implementing strategic growth initiatives in order to gain a competitive advantage. The strategies being largely adopted include mergers and acquisitions, strategic alliances, joint ventures, licensing agreements, and new product launches. With the implementation of these strategies, the market participants aim to increase product portfolios, as well as enhance regional presence for long-term sustainable business growth in the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | Global |

| Product/ Service Segmentation | Infrastructure, Cooling Technology, Data Center Type, AI Workload, End User, Region |

| Key Players | BASF SE, Dow Inc., SABIC, LyondellBasell Industries N.V., INEOS Group Holdings S.A., ExxonMobil Chemical Company, Shell Chemicals, DuPont de Nemours, Inc., Evonik Industries AG, LG Chem Ltd., Mitsubishi Chemical Group Corporation, Sumitomo Chemical Co., Ltd., and other prominent players. |

Market Segmentation

- By Chemical Type

- Petrochemicals

- Specialty Chemicals

- Agrochemicals

- Industrial Gases

- Polymers & Resins

- By Disruption Type

- Raw Material Shortage

- Logistics & Transportation Bottlenecks

- Geopolitical Trade Restrictions

- Energy Price Volatility

- Natural Disasters & Climate Events

- By Cost Pass-Through Level

- Full Cost Pass-Through

- Partial Cost Pass-Through

- Low / Delayed Pass-Through

- By Supply Chain Stage

- Upstream (Feedstock & Raw Materials)

- Midstream (Processing & Manufacturing)

- Downstream (Distribution & End-Use Industrys)

- By End-Use Industry

- Automotive

- Construction

- Electronics

- Pharmaceuticals

- Agriculture

- Consumer Goods

- By Region

- North America

- Europe

- Asia Pacific (APAC)

- Latin America (LATAM)

- Middle East and Africa (MEA)

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- Global Chemical Supply Chain Disruptions & Cost Pass-Through Market Insights

- Growth Drivers

- Restraints

- Opportunities

- Challenges

- Technological Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Industry Value Chain & Entry Points

- Global Chemical Supply Chain Disruptions & Cost Pass-Through Market: Regulatory Framework

- Margin Impact Modelling

- Raw Material Cost Escalation Impact

- Energy Cost Sensitivity Analysis

- Pass-Through Rate Assessment

- EBITDA Margin Stress Scenarios

- Regional Profitability Comparison

- Global Chemical Supply Chain Disruptions & Cost Pass-Through Market: Marketing Strategies

- Global Chemical Supply Chain Disruptions & Cost Pass-Through Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- Petrochemicals

- Specialty Chemicals

- Agrochemicals

- Industrial Gases

- Polymers & Resins

- By Disruption Type

- Raw Material Shortage

- Logistics & Transportation Bottlenecks

- Geopolitical Trade Restrictions

- Energy Price Volatility

- Natural Disasters & Climate Events

- By Cost Pass-Through Level

- Full Cost Pass-Through

- Partial Cost Pass-Through

- Low / Delayed Pass-Through

- By Supply Chain Stage

- Upstream (Feedstock & Raw Materials)

- Midstream (Processing & Manufacturing)

- Downstream (Distribution & End-Use Industrys)

- By End-Use Industry

- Automotive

- Construction

- Electronics

- Pharmaceuticals

- Agriculture

- Consumer Goods

- By Region

- North America

- Europe

- Asia Pacific (APAC)

- Latin America (LATAM)

- Middle East and Africa (MEA)

- By Chemical Type

- Market Size & Forecast, 2021-2032

- North America Chemical Supply Chain Disruptions & Cost Pass-Through Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- By Country

- United States

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Canada

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Europe Chemical Supply Chain Disruptions & Cost Pass-Through Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- By Country

- Germany

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- United Kingdom

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Italy

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- France

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Spain

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Belgium

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Russia

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- The Netherlands

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Rest of Europe

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Asia Pacific Chemical Supply Chain Disruptions & Cost Pass-Through Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- By Country

- China

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- India

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Japan

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- South Korea

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Australia & New Zealand

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Indonesia

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Malaysia

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Singapore

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Vietnam

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Rest of APAC

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Latin America Chemical Supply Chain Disruptions & Cost Pass-Through Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- By Country

- Brazil

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Mexico

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Argentina

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Peru

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Rest of LATAM

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Middle East & Africa Chemical Supply Chain Disruptions & Cost Pass-Through Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- By Country

- Saudi Arabia

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- UAE

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Qatar

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Kuwait

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- South Africa

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Nigeria

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Algeria

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Rest of MEA

- By Chemical Type

- By Disruption Type

- By Cost Pass-Through Level

- By Supply Chain Stage

- By End-Use Industry

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution by End-Use Industry

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List of Key Players and Their Products

- Global Chemical Supply Chain Disruptions & Cost Pass-Through Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Developments (Mergers, Acquisitions, Partnerships, etc.)

- Geopolitical Impact on Global Chemical Supply Chain Disruptions & Cost Pass-Through Market

- Company Profile

- BASF SE

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- SWOT Analysis

- BASF SE

- Saudi Arabia

- Market Size & Forecast, 2021-2032

- Brazil

- Market Size & Forecast, 2021-2032

- China

- Market Size & Forecast, 2021-2032

- Germany

- Market Size & Forecast, 2021-2032

- United States

- Market Size & Forecast, 2021-2032

**(same data pointers will be provided for the below companies)

- Dow Inc.

- SABIC

- LyondellBasell Industries N.V.

- INEOS Group Holdings S.A.

- ExxonMobil Chemical Company

- Shell Chemicals

- DuPont de Nemours, Inc.

- Evonik Industries AG

- LG Chem Ltd.

- Mitsubishi Chemical Group Corporation

- Sumitomo Chemical Co., Ltd.

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown of Primary Research Respondents, By Region

- Assumptions & Limitations

- Qualitative Research

*Financial information of case of non-listed companies can be provided as per availability.

**The segmentation and the companies are subject to modifications based on in-depth secondary research for the final deliverable

Frequently Asked Questions

1. What is the expected growth rate of the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market during the forecast period?

Ans: The Global Chemical Supply Chain Disruptions & Cost Pass-Through Market size was estimated at USD 5,450 billion in 2025.

2. What is the expected growth rate of the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market during the forecast period?

Ans: Global Chemical Supply Chain Disruptions & Cost Pass-Through Market is expected to grow at a CAGR of around 6.8% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market by 2032?

Ans: The Global Chemical Supply Chain Disruptions & Cost Pass-Through Market is projected to reach a value of approximately USD 8,650 Billion by 2032.

4. What are the major factors driving the growth of the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market?

Ans: Growth occurs because worldwide demand for petrochemicals and polymers and specialty chemicals used in automotive and electronics and pharmaceutical and consumer goods industries continues to increase.

5. Name the key players operating in the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market.

Ans: The key players of Global Chemical Supply Chain Disruptions & Cost Pass-Through Market are BASF SE, Dow Inc., SABIC, LyondellBasell Industries N.V., INEOS Group Holdings S.A., ExxonMobil Chemical Company, Shell Chemicals, DuPont de Nemours, Inc., Evonik Industries AG, LG Chem Ltd., Mitsubishi Chemical Group Corporation, Sumitomo Chemical Co., Ltd., and other prominent players.

6. Which is the fastest-growing chemical type segment in the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market?

Ans: Petrochemicals maintain their leading market position because manufacturing industries use them extensively while crude oil and natural gas prices create market uncertainties.

7. Which region contributes significantly to the growth of the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market?

Ans: The Global Chemical Supply Chain Disruptions and Cost Pass-Through Market will experience continuous growth throughout Europe between the years 2026 and 2032.

Frequently Asked Questions

1. What is the expected growth rate of the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market during the forecast period?

Ans: The Global Chemical Supply Chain Disruptions & Cost Pass-Through Market size was estimated at USD 5,450 billion in 2025.

2. What is the expected growth rate of the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market during the forecast period?

Ans: Global Chemical Supply Chain Disruptions & Cost Pass-Through Market is expected to grow at a CAGR of around 6.8% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market by 2032?

Ans: The Global Chemical Supply Chain Disruptions & Cost Pass-Through Market is projected to reach a value of approximately USD 8,650 Billion by 2032.

4. What are the major factors driving the growth of the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market?

Ans: Growth occurs because worldwide demand for petrochemicals and polymers and specialty chemicals used in automotive and electronics and pharmaceutical and consumer goods industries continues to increase.

5. Name the key players operating in the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market.

Ans: The key players of Global Chemical Supply Chain Disruptions & Cost Pass-Through Market are BASF SE, Dow Inc., SABIC, LyondellBasell Industries N.V., INEOS Group Holdings S.A., ExxonMobil Chemical Company, Shell Chemicals, DuPont de Nemours, Inc., Evonik Industries AG, LG Chem Ltd., Mitsubishi Chemical Group Corporation, Sumitomo Chemical Co., Ltd., and other prominent players.

6. Which is the fastest-growing chemical type segment in the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market?

Ans: Petrochemicals maintain their leading market position because manufacturing industries use them extensively while crude oil and natural gas prices create market uncertainties.

7. Which region contributes significantly to the growth of the Global Chemical Supply Chain Disruptions & Cost Pass-Through Market?

Ans: The Global Chemical Supply Chain Disruptions and Cost Pass-Through Market will experience continuous growth throughout Europe between the years 2026 and 2032.