Global AI Data Center Power & Cooling Capacity Crunch Market, By Infrastructure (Power Infrastructure, Cooling Infrastructure, Rack & IT Load Systems, Energy Storage Systems); By Cooling Technology (Air-Based Cooling, Liquid Cooling (Direct-to-Chip), Immersion Cooling, Hybrid Cooling Systems); By Data Center Type (Hyperscale AI Data Centers, Colocation Data Centers, Enterprise AI Data Centers, Edge AI Data Centers); By AI Workload (Generative AI, Machine Learning Training, Inference Workloads, High-Performance Computing (HPC)); By End User (Cloud Service Providers, AI Startups, Research Institutions, Government & Defense, BFSI & Enterprise); By Region (North America, Europe, Asia Pacific (APAC), Latin America (LATAM), Middle East and Africa (MEA)); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Chemicals & Advanced Materials

- Mar 2026

- Pages 350

- Report Format: pdf

- Report Price: $3500 USD

Global AI Data Center Power & Cooling Capacity Crunch Market, Size & Forecast 2021-2032

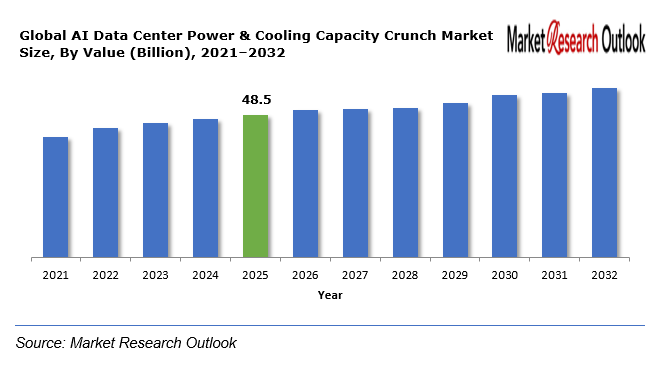

The Global AI Data Center Power & Cooling Capacity Crunch Market size was estimated at USD 48.5 Billion in 2025. During the forecast period, the Global AI Data Center Power & Cooling Capacity Crunch Market size is projected to grow at a CAGR of 18.7% reaching a value of USD 161.2 Billion by 2032. The expansion results from two factors which include fast deployment of hyperscale AI clusters and high-performance GPU deployments and increased cloud service provider capital expenditures. AI training workloads need rack power densities which exceed 40 to 80 kW per rack to function properly whereas traditional enterprise data centers require lower power densities. The rising demand for advanced cooling systems has created a need for both direct-to-chip liquid cooling and immersion cooling technologies. The United States and Europe and Asia Pacific face grid congestion issues which create a need for on-site energy storage solutions and power optimization methods. Market momentum will continue at a strong pace because these developments will maintain their positive impact throughout the forecast period.

AI Data Center Power & Cooling Capacity Crunch – Overview

AI Data Center Power & Cooling refers to the specialized electrical and thermal management infrastructure which exists to support high-density computing environments that operate with artificial intelligence workloads. AI facilities need more electrical power than traditional data centers because they require high-capacity transformers and backup power systems and cooling systems that can handle extreme temperature conditions. The power infrastructure of a facility consists of substations and switchgear and UPS systems and backup generators and energy storage solutions while cooling infrastructure of the facility includes advanced air-based systems and liquid cooling and immersion cooling technologies.

Global AI Data Center Power & Cooling Capacity Crunch Market

Growth Drivers

Explosion of Generative AI and High-Density GPU Deployments

The widespread use of generative AI applications together with extensive model training operations creates higher power requirements for data centers. Hyperscale operators are building AI-focused facilities designed to handle megawatt-scale training clusters. The deployments need advanced power distribution systems together with liquid cooling solutions which can keep equipment at safe operating temperatures during persistent major processing activities. Cloud providers and AI startups are investing heavily in modular and scalable power architectures to meet rapidly evolving AI workload requirements.

Challenges

Grid Limitations and Cooling Efficiency Constraints

The market currently faces its main challenge because key AI development regions lack sufficient grid capacity. The power infrastructure of local areas faces difficulty because AI clusters demand more electricity than current networks can deliver which results in extended periods before new facilities become operational. Metropolitan areas face power supply challenges because utilities cannot provide immediate megawatt capacity, which forces operators to develop energy storage and on-site generation capabilities. Traditional air-based cooling systems have reached their maximum efficiency level because rack densities continue to increase. The shift from traditional cooling methods to liquid and immersion cooling systems requires organizations to spend large amounts of money while facing technical difficulties.

Geopolitical Impact on Global AI Data Center Power & Cooling Capacity Crunch Market

The market experiences changes because geopolitical factors create disruptions in semiconductor supply chains and advanced AI chip export controls and trade restrictions impact regional energy security. The implementation of advanced GPU export restrictions together with cross-border technology transfer bans will create obstacles that will hinder the development of AI infrastructure across specific geographical areas. The implementation of energy policy changes and carbon pricing systems together with international trade disputes leads to changes in both the availability and expenses of power equipment which includes transformers and switchgear and cooling systems. Government incentives together with regulatory frameworks will determine how countries allocate their investments during the period from 2026 to 2032 as they compete to establish themselves as AI innovation hubs.

Global AI Data Center Power & Cooling Capacity Crunch Market

Segmental Coverage

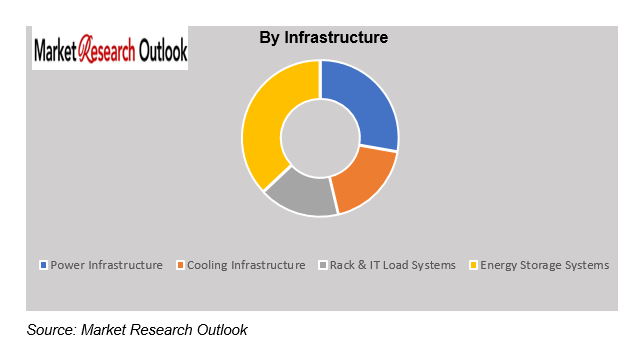

Global AI Data Center Power & Cooling Capacity Crunch Market – By Infrastructure

Based on infrastructure, the market is segmented into Power Infrastructure, Cooling Infrastructure, Rack & IT Load Systems, and Energy Storage Systems. Power Infrastructure holds a dominant share due to rising investments in substations, UPS systems, and high-capacity transformers. The Cooling Infrastructure sector will experience its fastest growth period because AI rack densities are increasing and liquid cooling systems are being adopted at a rapid pace. Energy Storage Systems are gaining traction to mitigate grid instability and manage peak load demand. Rack & IT Load Systems have developed new technology to support higher wattage GPUs and AI accelerators while maintaining modular scalability in hyperscale environments.

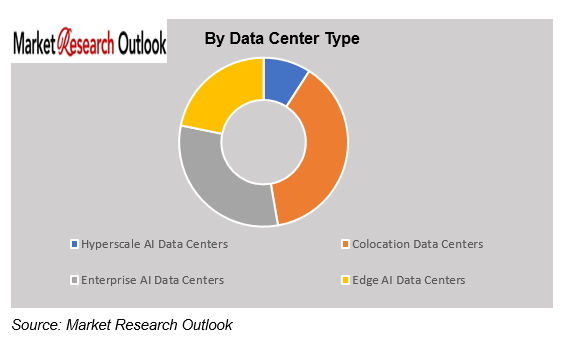

Global AI Data Center Power & Cooling Capacity Crunch Market – By Data Center Type

Based on data center type, the market is segmented into Hyperscale AI Data Centers, Colocation Data Centers, Enterprise AI Data Centers, and Edge AI Data Centers. The market will be dominated by Hyperscale AI Data Centers because cloud service providers continue to invest in AI training infrastructure. Colocation providers are expanding their AI-ready facilities to provide high-performance computing solutions for both startups and enterprise customers. Enterprise AI Data Centers are modernizing their existing systems to enable artificial intelligence analytics and automation. Edge AI Data Centers provide support for applications that need low latency in autonomous vehicles and smart city infrastructure.

Competitive Landscape

Key participants in the Global AI Data Center Power & Cooling Capacity Crunch market include Schneider Electric SE, Vertiv Holdings Co., ABB Ltd., Siemens AG, Eaton Corporation plc, Huawei Digital Power Technologies Co., Ltd., Delta Electronics, Inc., Johnson Controls International plc, Trane Technologies plc, STULZ GmbH, Rittal GmbH & Co. KG, Asetek A/S. and other prominent players.

These companies are implementing strategic growth initiatives in order to gain a competitive advantage. The strategies being largely adopted include mergers and acquisitions, strategic alliances, joint ventures, licensing agreements, and new product launches. With the implementation of these strategies, the market participants aim to increase product portfolios, as well as enhance regional presence for long-term sustainable business growth in the Global AI Data Center Power & Cooling Capacity Crunch Market.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | Global |

| Product/ Service Segmentation | Infrastructure, Cooling Technology, Data Center Type, AI Workload, End User, Region |

| Key Players | Schneider Electric SE, Vertiv Holdings Co., ABB Ltd., Siemens AG, Eaton Corporation plc, Huawei Digital Power Technologies Co., Ltd., Delta Electronics, Inc., Johnson Controls International plc, Trane Technologies plc, STULZ GmbH, Rittal GmbH & Co. KG, Asetek A/S. and other prominent players. |

Market Segmentation

- By Infrastructure

- Power Infrastructure

- Cooling Infrastructure

- Rack & IT Load Systems

- Energy Storage Systems

- By Cooling Technology

- Air-Based Cooling

- Liquid Cooling (Direct-to-Chip)

- Immersion Cooling

- Hybrid Cooling Systems

- By Data Center Type

- Hyperscale AI Data Centers

- Colocation Data Centers

- Enterprise AI Data Centers

- Edge AI Data Centers

- By AI Workload

- Generative AI

- Machine Learning Training

- Inference Workloads

- High-Performance Computing (HPC)

- By End User

- Cloud Service Providers

- AI Startups

- Research Institutions

- Government & Defense

- BFSI & Enterprise

- By Region

- North America

- Europe

- Asia Pacific (APAC)

- Latin America (LATAM)

- Middle East and Africa (MEA)

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- Global AI Data Center Power & Cooling Capacity Crunch Market Insights

- Growth Drivers

- Restraints

- Opportunities

- Challenges

- AI-Driven Load Stress Analysis

- Technological Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Industry Value Chain & Entry Points

- Global AI Data Center Power & Cooling Capacity Crunch Market: Regulatory Framework

- Global AI Data Center Power & Cooling Capacity Crunch Market: Marketing Strategies

- Global AI Data Center Power & Cooling Capacity Crunch Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Infrastructure

- Power Infrastructure

- Cooling Infrastructure

- Rack & IT Load Systems

- Energy Storage Systems

- By Cooling Technology

- Air-Based Cooling

- Liquid Cooling (Direct-to-Chip)

- Immersion Cooling

- Hybrid Cooling Systems

- By Data Center Type

- Hyperscale AI Data Centers

- Colocation Data Centers

- Enterprise AI Data Centers

- Edge AI Data Centers

- By AI Workload

- Generative AI

- Machine Learning Training

- Inference Workloads

- High-Performance Computing (HPC)

- By End User

- Cloud Service Providers

- AI Startups

- Research Institutions

- Government & Defense

- BFSI & Enterprise

- By Region

- North America

- Europe

- Asia Pacific (APAC)

- Latin America (LATAM)

- Middle East and Africa (MEA)

- By Infrastructure

- Market Size & Forecast, 2021-2032

- North America AI Data Center Power & Cooling Capacity Crunch Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- By Country

- United States

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Canada

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- United States

- Market Size & Forecast, 2021-2032

- Europe AI Data Center Power & Cooling Capacity Crunch Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- By Country

- Germany

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- United Kingdom

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Italy

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- France

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Spain

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Belgium

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Russia

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- The Netherlands

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Rest of Europe

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Asia Pacific AI Data Center Power & Cooling Capacity Crunch Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- By Country

- China

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- India

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Japan

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- South Korea

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Australia & New Zealand

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Indonesia

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Malaysia

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Singapore

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Vietnam

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Rest of APAC

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Latin America AI Data Center Power & Cooling Capacity Crunch Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- By Country

- Brazil

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Mexico

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Argentina

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Peru

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Rest of LATAM

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Middle East & Africa AI Data Center Power & Cooling Capacity Crunch Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- By Country

- Saudi Arabia

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- UAE

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Qatar

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Kuwait

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- South Africa

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Nigeria

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Algeria

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Rest of MEA

- By Infrastructure

- By Cooling Technology

- By Data Center Type

- By AI Workload

- By End User

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution by End-Use Industry

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List of Key Players and Their Products

- Global AI Data Center Power & Cooling Capacity Crunch Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Developments (Mergers, Acquisitions, Partnerships, etc.)

- Geopolitical Impact on Global AI Data Center Power & Cooling Capacity Crunch Market

- Company Profile

- Schneider Electric SE

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Schneider Electric SE

- Saudi Arabia

- Market Size & Forecast, 2021-2032

- Brazil

- Market Size & Forecast, 2021-2032

- China

- Market Size & Forecast, 2021-2032

- Germany

- Market Size & Forecast, 2021-2032

**(same data pointers will be provided for the below companies)

- Vertiv Holdings Co.

- ABB Ltd.

- Siemens AG

- Eaton Corporation plc

- Huawei Digital Power Technologies Co., Ltd.

- Delta Electronics, Inc.

- Johnson Controls International plc

- Trane Technologies plc

- STULZ GmbH

- Rittal GmbH & Co. KG

- Asetek A/S

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown of Primary Research Respondents, By Region

- Assumptions & Limitations

- Qualitative Research

*Financial information of case of non-listed companies can be provided as per availability.

**The segmentation and the companies are subject to modifications based on in-depth secondary research for the final deliverable

Frequently Asked Questions

1. What is the expected growth rate of the Global AI Data Center Power & Cooling Capacity Crunch Market during the forecast period?

Ans: The Global AI Data Center Power & Cooling Capacity Crunch Market size was estimated at USD 48.5 billion in 2025.

2. What is the expected growth rate of the Global AI Data Center Power & Cooling Capacity Crunch Market during the forecast period?

Ans: Global AI Data Center Power & Cooling Capacity Crunch Market is expected to grow at a CAGR of around 18.7% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Global AI Data Center Power & Cooling Capacity Crunch Market by 2032?

Ans: The Global AI Data Center Power & Cooling Capacity Crunch Market is projected to reach a value of approximately USD 161.2 Billion by 2032.

4. What are the major factors driving the growth of the Global AI Data Center Power & Cooling Capacity Crunch Market?

Ans: The expansion results from two factors which include fast deployment of hyperscale AI clusters and high-performance GPU deployments and increased cloud service provider capital expenditures.

5. Name the key players operating in the Global AI Data Center Power & Cooling Capacity Crunch Market.

Ans: The key players of Global AI Data Center Power & Cooling Capacity Crunch Market are Schneider Electric SE, Vertiv Holdings Co., ABB Ltd., Siemens AG, Eaton Corporation plc, Huawei Digital Power Technologies Co., Ltd., Delta Electronics, Inc., Johnson Controls International plc, Trane Technologies plc, STULZ GmbH, Rittal GmbH & Co. KG, Asetek A/S. and other prominent players.

6. Which is the fastest-growing data center type segment in the Global AI Data Center Power & Cooling Capacity Crunch Market?

Ans: The market will be dominated by Hyperscale AI Data Centers because cloud service providers continue to invest in AI training infrastructure.

7. Which region contributes significantly to the growth of the Global AI Data Center Power & Cooling Capacity Crunch Market?

Ans: The Global AI Data Center Power and Cooling Capacity Crunch Market will experience major growth in the Asia Pacific region. The region’s growth occurs because businesses adopt digital technologies at a fast pace while organizations use artificial intelligence in their operations and major investments are made for hyperscale data center construction across China India Japan South Korea Singapore and Australia.

Frequently Asked Questions

1. What is the expected growth rate of the Global AI Data Center Power & Cooling Capacity Crunch Market during the forecast period?

Ans: The Global AI Data Center Power & Cooling Capacity Crunch Market size was estimated at USD 48.5 billion in 2025.

2. What is the expected growth rate of the Global AI Data Center Power & Cooling Capacity Crunch Market during the forecast period?

Ans: Global AI Data Center Power & Cooling Capacity Crunch Market is expected to grow at a CAGR of around 18.7% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Global AI Data Center Power & Cooling Capacity Crunch Market by 2032?

Ans: The Global AI Data Center Power & Cooling Capacity Crunch Market is projected to reach a value of approximately USD 161.2 Billion by 2032.

4. What are the major factors driving the growth of the Global AI Data Center Power & Cooling Capacity Crunch Market?

Ans: The expansion results from two factors which include fast deployment of hyperscale AI clusters and high-performance GPU deployments and increased cloud service provider capital expenditures.

5. Name the key players operating in the Global AI Data Center Power & Cooling Capacity Crunch Market.

Ans: The key players of Global AI Data Center Power & Cooling Capacity Crunch Market are Schneider Electric SE, Vertiv Holdings Co., ABB Ltd., Siemens AG, Eaton Corporation plc, Huawei Digital Power Technologies Co., Ltd., Delta Electronics, Inc., Johnson Controls International plc, Trane Technologies plc, STULZ GmbH, Rittal GmbH & Co. KG, Asetek A/S. and other prominent players.

6. Which is the fastest-growing data center type segment in the Global AI Data Center Power & Cooling Capacity Crunch Market?

Ans: The market will be dominated by Hyperscale AI Data Centers because cloud service providers continue to invest in AI training infrastructure.

7. Which region contributes significantly to the growth of the Global AI Data Center Power & Cooling Capacity Crunch Market?

Ans: The Global AI Data Center Power and Cooling Capacity Crunch Market will experience major growth in the Asia Pacific region. The region’s growth occurs because businesses adopt digital technologies at a fast pace while organizations use artificial intelligence in their operations and major investments are made for hyperscale data center construction across China India Japan South Korea Singapore and Australia.