Global Food Supply Chain Vulnerability to Climate & Energy Market, By Vulnerability Type (Climate Risk Exposure, Energy Price Volatility Risk, Water Scarcity Risk, Extreme Weather Disruption Risk, Transportation & Logistics Disruption, Input Cost Inflation Risk); By Supply Chain Stage (Agricultural Production, Post-Harvest & Storage, Processing & Manufacturing, Transportation & Distribution, Retail & Food Service); By Energy Dependency Type (Fossil Fuel Dependent Operations, Grid-Dependent Cold Chain, Renewable-Integrated Operations, Hybrid Energy Systems); By Food Category (Grains & Cereals, Fruits & Vegetables, Meat & Poultry, Dairy Products, Seafood, Processed & Packaged Foods); By End User (Food Producers, Food Processors, Retail Chains, Food Service Providers, Government & Public Agencies); By Region (North America, Europe, Asia Pacific (APAC), Latin America (LATAM), Middle East and Africa (MEA)); By Trend Analysis, Competitive Landscape & Forecast, 2022-2032

- Chemicals & Advanced Materials

- Mar 2026

- Pages 300

- Report Format: pdf

- Report Price: $3500 USD

Global Food Supply Chain Vulnerability to Climate & Energy Market, Size & Forecast 2021-2032

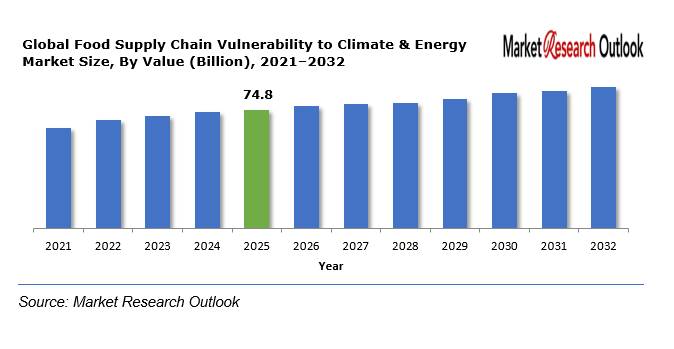

The Global Food Supply Chain Vulnerability to Climate & Energy Market size was estimated at USD 74.8 Billion in 2025. During the forecast period, the Global Food Supply Chain Vulnerability to Climate & Energy Market size is projected to grow at a CAGR of 8.7% reaching a value of USD 134.6 Billion by 2032. Market expansion is driven by increasing climate disruptions which include droughts and floods and hurricanes and global energy market instability which affects fuel and fertilizer and transportation costs. The combination of rising food demand from a growing world population and ongoing geopolitical conflicts and trade barriers creates extra risks to supply chain operations. The global investment in climate-risk modeling and energy transition planning and supply chain digitalization has increased because organizations now recognize resilience planning as a critical business function.

Food Supply Chain Vulnerability to Climate & Energy – Overview

Food supply chain vulnerability describes how agricultural production and processing and storage and distribution systems become vulnerable to climate-related shocks and energy market disruptions. Climate change impacts crop yields and livestock productivity and water availability while energy volatility affects operational costs and cold storage reliability and logistics efficiency.

Global Food Supply Chain Vulnerability to Climate & Energy Market

Growth Drivers

Rising Climate Instability and Extreme Weather Events

The rising occurrence and intense nature of droughts floods hurricanes and heatwaves disrupt agricultural production in essential food-growing areas. Climate variability causes decreased crop production and harmful effects on animal well-being and higher need for artificial irrigation systems. The storage and processing and distribution systems experience multiple disruptions that lead to subsequent problems.

Challenges

ROI Expectation Gap and Implementation Complexity

Food supply chains require substantial energy resources for their cold chain logistics systems and their large-scale food processing operations. Operational expenses experience significant growth whenever there are sudden increases in oil gas or electricity charges. The financial resources of small and medium-sized food producers especially limit their ability to withstand economic challenges.

Geopolitical Impact on Global Food Supply Chain Vulnerability to Climate & Energy Market

The Global Food Supply Chain Vulnerability to Climate & Energy Market faces major impacts from three factors which include geopolitical tensions and trade restrictions and global energy policies. Conflicts in major grain-exporting regions create obstacles for international food trade because sanctions and fuel supply constraints result in higher transportation costs which affect all countries. Food production and logistics costs see direct effects from energy policy changes which include carbon pricing and fossil fuel subsidy elimination. The combination of export bans and food protectionism measures creates price volatility and supply instability because they restrict food availability. Between 2026 and 2032, geopolitical uncertainties combined with climate risks are expected to drive greater investment in resilient, diversified, and energy-efficient food supply systems.

Global Food Supply Chain Vulnerability to Climate & Energy Market

Segmental Coverage

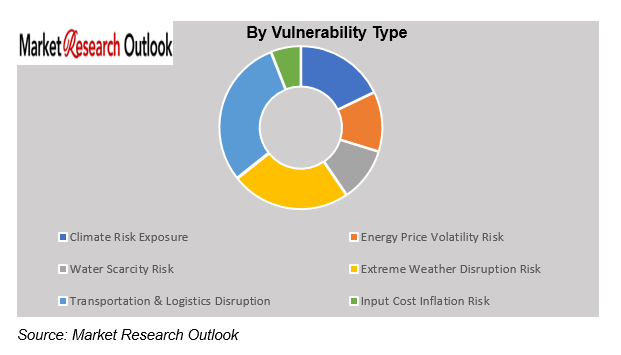

Global Food Supply Chain Vulnerability to Climate & Energy Market – By Vulnerability Type

Based on vulnerability type, the market is segmented into Climate Risk Exposure, Energy Price Volatility Risk, Water Scarcity Risk, Extreme Weather Disruption Risk, Transportation & Logistics Disruption, and Input Cost Inflation Risk. The two dominant market sectors need to measure climate risk exposure and energy price volatility risk because these two factors affect all stages of supply chain operations. The growing significance of Water Scarcity Risk affects Asian Pacific and Middle Eastern regions which depend on irrigation for their agricultural needs. The extreme weather events together with worldwide trade bottlenecks have created increased challenges for Transportation & Logistics operations. Rising fertilizer and feed costs further amplify Input Cost Inflation Risk across agricultural systems.

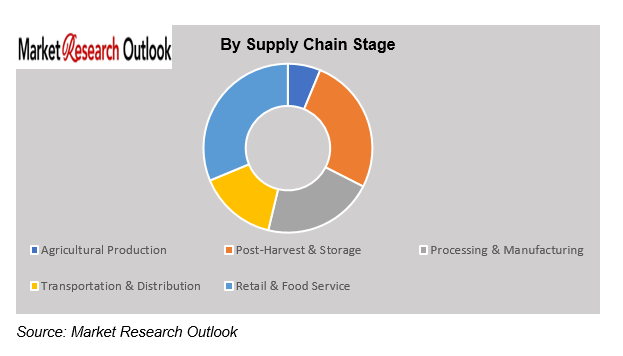

Global Food Supply Chain Vulnerability to Climate & Energy Market – By Supply Chain Stage

Based on supply chain stage, the market is segmented into Agricultural Production, Post-Harvest & Storage, Processing & Manufacturing, Transportation & Distribution, and Retail & Food Service. Agricultural Production stands as the most climate-sensitive phase because it experiences high vulnerability to both temperature changes and precipitation fluctuations. Transportation & Distribution faces two major threats which come from both fuel price changes and weather-related damage to its infrastructure. The Processing & Manufacturing industry confronts two main challenges which include energy cost uncertainties and supply chain disruptions. Retail & Food Service sectors are increasingly investing in diversified sourcing and inventory management systems to mitigate disruptions.

Competitive Landscape

Key participants in the Global Food Supply Chain Vulnerability to Climate & Energy market include Cargill, Incorporated, Archer Daniels Midland, Bunge Limited, Louis Dreyfus Company, Nestlé S.A., PepsiCo, Inc., The Coca-Cola Company, Tyson Foods, Inc., JBS S.A., Sysco Corporation, Walmart Inc., Maersk A/S, and other prominent players.

These companies are implementing strategic growth initiatives in order to gain a competitive advantage. The strategies being largely adopted include mergers and acquisitions, strategic alliances, joint ventures, licensing agreements, and new product launches. With the implementation of these strategies, the market participants aim to increase product portfolios, as well as enhance regional presence for long-term sustainable business growth in the Global Food Supply Chain Vulnerability to Climate & Energy Market.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | Global |

| Product/ Service Segmentation | Vulnerability Type, Supply Chain Stage, Energy Dependency Type, Food Category, End User, Region |

| Key Players | Cargill, Incorporated, Archer Daniels Midland, Bunge Limited, Louis Dreyfus Company, Nestlé S.A., PepsiCo, Inc., The Coca-Cola Company, Tyson Foods, Inc., JBS S.A., Sysco Corporation, Walmart Inc., Maersk A/S, and other prominent players. |

Market Segmentation

- By Vulnerability Type

- Climate Risk Exposure

- Energy Price Volatility Risk

- Water Scarcity Risk

- Extreme Weather Disruption Risk

- Transportation & Logistics Disruption

- Input Cost Inflation Risk

- By Supply Chain Stage

- Agricultural Production

- Post-Harvest & Storage

- Processing & Manufacturing

- Transportation & Distribution

- Retail & Food Service

- By Energy Dependency Type

- Fossil Fuel Dependent Operations

- Grid-Dependent Cold Chain

- Renewable-Integrated Operations

- Hybrid Energy Systems

- By Food Category

- Grains & Cereals

- Fruits & Vegetables

- Meat & Poultry

- Dairy Products

- Seafood

- Processed & Packaged Foods

- By End User

- Food Producers

- Food Processors

- Retail Chains

- Food Service Providers

- Government & Public Agencies

- By Region

- North America

- Europe

- Asia Pacific (APAC)

- Latin America (LATAM)

- Middle East and Africa (MEA)

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- Global Food Supply Chain Vulnerability to Climate & Energy Market Insights

- Growth Drivers

- Restraints

- Opportunities

- Challenges

- Shock Exposure Modelling (Climate & Energy Scenarios)

- Technological Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Industry Value Chain & Entry Points

- Global Food Supply Chain Vulnerability to Climate & Energy Market: Regulatory Framework

- Global Food Supply Chain Vulnerability to Climate & Energy Market: Marketing Strategies

- Global Food Supply Chain Vulnerability to Climate & Energy Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Vulnerability Type

- Climate Risk Exposure

- Energy Price Volatility Risk

- Water Scarcity Risk

- Extreme Weather Disruption Risk

- Transportation & Logistics Disruption

- Input Cost Inflation Risk

- By Supply Chain Stage

- Agricultural Production

- Post-Harvest & Storage

- Processing & Manufacturing

- Transportation & Distribution

- Retail & Food Service

- By Energy Dependency Type

- Fossil Fuel Dependent Operations

- Grid-Dependent Cold Chain

- Renewable-Integrated Operations

- Hybrid Energy Systems

- By Food Category

- Grains & Cereals

- Fruits & Vegetables

- Meat & Poultry

- Dairy Products

- Seafood

- Processed & Packaged Foods

- By End User

- Food Producers

- Food Processors

- Retail Chains

- Food Service Providers

- Government & Public Agencies

- By Region

- North America

- Europe

- Asia Pacific (APAC)

- Latin America (LATAM)

- Middle East and Africa (MEA)

- By Vulnerability Type

- Market Size & Forecast, 2021-2032

- North America Food Supply Chain Vulnerability to Climate & Energy Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- By Country

- United States

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Canada

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- United States

- Market Size & Forecast, 2021-2032

- Europe Food Supply Chain Vulnerability to Climate & Energy Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- By Country

- Germany

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- United Kingdom

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Italy

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- France

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Spain

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Belgium

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Russia

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- The Netherlands

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Rest of Europe

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Asia Pacific Food Supply Chain Vulnerability to Climate & Energy Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- By Country

- China

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- India

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Japan

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- South Korea

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Australia & New Zealand

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Indonesia

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Malaysia

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Singapore

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Vietnam

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Rest of APAC

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Latin America Food Supply Chain Vulnerability to Climate & Energy Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- By Country

- Brazil

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Mexico

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Argentina

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Peru

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Rest of LATAM

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Middle East & Africa Food Supply Chain Vulnerability to Climate & Energy Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- By Country

- Saudi Arabia

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- UAE

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Qatar

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Kuwait

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- South Africa

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Nigeria

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Algeria

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Rest of MEA

- By Vulnerability Type

- By Supply Chain Stage

- By Energy Dependency Type

- By Food Category

- By End User

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution by End User

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List of Key Players and Their Products

- Global Food Supply Chain Vulnerability to Climate & Energy Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Developments (Mergers, Acquisitions, Partnerships, etc.)

- Geopolitical Impact on Global Food Supply Chain Vulnerability to Climate & Energy Market

- Company Profile

- Cargill, Incorporated

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Cargill, Incorporated

- Saudi Arabia

- Market Size & Forecast, 2021-2032

- Brazil

- Market Size & Forecast, 2021-2032

- China

- Market Size & Forecast, 2021-2032

- Germany

- Market Size & Forecast, 2021-2032

**(same data pointers will be provided for the below companies)

- Archer Daniels Midland

- Bunge Limited

- Louis Dreyfus Company

- Nestlé S.A.

- PepsiCo, Inc.

- The Coca-Cola Company

- Tyson Foods, Inc.

- JBS S.A.

- Sysco Corporation

- Walmart Inc.

- Maersk A/S

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown of Primary Research Respondents, By Region

- Assumptions & Limitations

- Qualitative Research

*Financial information of case of non-listed companies can be provided as per availability.

**The segmentation and the companies are subject to modifications based on in-depth secondary research for the final deliverable

Frequently Asked Questions

1. What is the expected growth rate of the Global Food Supply Chain Vulnerability to Climate & Energy Market during the forecast period?

Ans: The Global Food Supply Chain Vulnerability to Climate & Energy Market size was estimated at USD 74.8 billion in 2025.

2. What is the expected growth rate of the Global Food Supply Chain Vulnerability to Climate & Energy Market during the forecast period?

Ans: Global Food Supply Chain Vulnerability to Climate & Energy Market is expected to grow at a CAGR of around 8.7% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Global Food Supply Chain Vulnerability to Climate & Energy Market by 2032?

Ans: The Global Food Supply Chain Vulnerability to Climate & Energy Market is projected to reach a value of approximately USD 134.6 Billion by 2032.

4. What are the major factors driving the growth of the Global Food Supply Chain Vulnerability to Climate & Energy Market?

Ans: Market expansion is driven by increasing climate disruptions which include droughts and floods and hurricanes and global energy market instability which affects fuel and fertilizer and transportation costs.

5. Name the key players operating in the Global Food Supply Chain Vulnerability to Climate & Energy Market.

Ans: The key players of Global Food Supply Chain Vulnerability to Climate & Energy Market are Cargill, Incorporated, Archer Daniels Midland, Bunge Limited, Louis Dreyfus Company, Nestlé S.A., PepsiCo, Inc., The Coca-Cola Company, Tyson Foods, Inc., JBS S.A., Sysco Corporation, Walmart Inc., Maersk A/S, and other prominent players.

6. Which is the fastest-growing supply chain stage segment in the Global Food Supply Chain Vulnerability to Climate & Energy Market?

Ans: Agricultural Production stands as the most climate-sensitive phase because it experiences high vulnerability to both temperature changes and precipitation fluctuations.

7. Which region contributes significantly to the growth of the Global Food Supply Chain Vulnerability to Climate & Energy Market?

Ans: The forecast period will show substantial growth for North America because three factors will impact agricultural production. The first factor is climate change which creates unpredictable weather patterns. The second factor involves energy prices which experience unpredictable market changes. The third factor consists of government regulations which aim to strengthen food system resilience.

8.

Ans:

Frequently Asked Questions

1. What is the expected growth rate of the Global Food Supply Chain Vulnerability to Climate & Energy Market during the forecast period?

Ans: The Global Food Supply Chain Vulnerability to Climate & Energy Market size was estimated at USD 74.8 billion in 2025.

2. What is the expected growth rate of the Global Food Supply Chain Vulnerability to Climate & Energy Market during the forecast period?

Ans: Global Food Supply Chain Vulnerability to Climate & Energy Market is expected to grow at a CAGR of around 8.7% during the forecast period between 2026 and 2032.

3. What is the forecast value of the Global Food Supply Chain Vulnerability to Climate & Energy Market by 2032?

Ans: The Global Food Supply Chain Vulnerability to Climate & Energy Market is projected to reach a value of approximately USD 134.6 Billion by 2032.

4. What are the major factors driving the growth of the Global Food Supply Chain Vulnerability to Climate & Energy Market?

Ans: Market expansion is driven by increasing climate disruptions which include droughts and floods and hurricanes and global energy market instability which affects fuel and fertilizer and transportation costs.

5. Name the key players operating in the Global Food Supply Chain Vulnerability to Climate & Energy Market.

Ans: The key players of Global Food Supply Chain Vulnerability to Climate & Energy Market are Cargill, Incorporated, Archer Daniels Midland, Bunge Limited, Louis Dreyfus Company, Nestlé S.A., PepsiCo, Inc., The Coca-Cola Company, Tyson Foods, Inc., JBS S.A., Sysco Corporation, Walmart Inc., Maersk A/S, and other prominent players.

6. Which is the fastest-growing supply chain stage segment in the Global Food Supply Chain Vulnerability to Climate & Energy Market?

Ans: Agricultural Production stands as the most climate-sensitive phase because it experiences high vulnerability to both temperature changes and precipitation fluctuations.

7. Which region contributes significantly to the growth of the Global Food Supply Chain Vulnerability to Climate & Energy Market?

Ans: The forecast period will show substantial growth for North America because three factors will impact agricultural production. The first factor is climate change which creates unpredictable weather patterns. The second factor involves energy prices which experience unpredictable market changes. The third factor consists of government regulations which aim to strengthen food system resilience.

8.

Ans: