Global Semiconductor Fab Infrastructure Bottlenecks Market, By Bottleneck Type (Power Supply & Energy Infrastructure Constraints, Water Supply & Wastewater Treatment Limitations, Cleanroom Construction & Facility Space Constraints, Equipment Lead Time & Installation Delays, Skilled Workforce & Talent Shortages, Others); By Fab Type (Foundry Fabs, Integrated Device Manufacturer (IDM) Fabs, Memory Fabs); By Node Size (Leading Edge (Below 10 nm), Advanced Nodes (10–28 nm), Mature Nodes (28–65 nm), Legacy Nodes (Above 65 nm)); By Infrastructure Component (Power & Energy Infrastructure, Water & Chemical Supply Systems, Cleanroom & Facility Construction, Fab Equipment & Installation, Automation & Digital Infrastructure, Waste Management & Recycling Systems); By End User (Logic & Foundry Manufacturers, Memory Manufacturers, Analog & Power Semiconductor Manufacturers, OSAT & Packaging Providers); By Region (North America, Europe, Asia Pacific (APAC), Latin America (LATAM), Middle East and Africa (MEA)); By Trend Analysis, Competitive Landscape & Forecast, 2021-2032

- Chemicals & Advanced Materials

- Feb 2026

- Pages 300

- Report Format: pdf

- Report Price: $3500 USD

Global Semiconductor Fab Infrastructure Bottlenecks Market, Size & Forecast 2021-2032

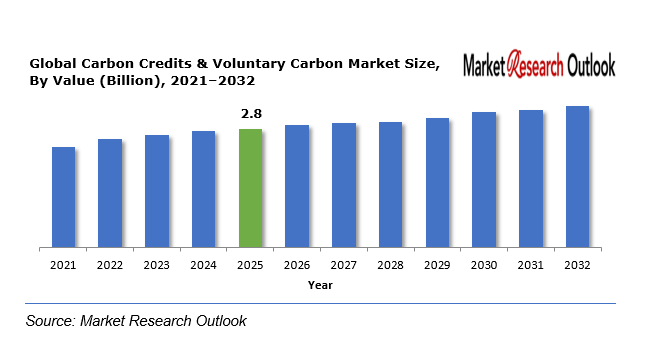

The Global Semiconductor Fab Infrastructure Bottlenecks Market size was estimated at USD 2.8 Billion in 2025. During the forecast period, the Global Semiconductor Fab Infrastructure Bottlenecks Market size is projected to grow at a CAGR of 12.9% reaching a value of USD 6.4 Billion by 2032. The market will grow because semiconductor fabrication facilities are being built and upgraded throughout Asia Pacific and North America and Europe. The United States CHIPS Act and European Chips Act and Japanese and South Korean and Indian government programs have supported massive semiconductor fabrication facilities because advanced chip demand and secure domestic production requirements create an urgent need for these facilities. However, project schedules and operational productivity face disruption from infrastructure bottlenecks which include electricity shortages and water scarcity and environmental approvals and supply chain delays. Semiconductor manufacturers are using resilient infrastructure planning and automation and resource optimization to build solutions which will help them treat operational obstacles and expand their production capabilities.

Semiconductor Fab Infrastructure Bottlenecks – Overview

Semiconductor fabrication facilities face infrastructure bottlenecks which arise from limitations and constraining factors that affect their physical assets, power resources, employee base, and material distribution systems. The bottlenecks restrict access to essential resources such as electrical power, ultra-pure water, cleanroom space, specialized manufacturing equipment, and trained professionals needed in semiconductor production.

Global Semiconductor Fab Infrastructure Bottlenecks Market

Growth Drivers

Expansion of Global Semiconductor Manufacturing Capacity

Governments and semiconductor companies are investing heavily in new fabrication facilities to strengthen domestic production capabilities and reduce dependency on external supply chains. The rising need for advanced chips in artificial intelligence and automotive electronics and consumer electronics and industrial automation fields is driving companies to build new semiconductor fabrication plants throughout the world. The fast development of the area creates multiple infrastructure problems which include power grid constraints and water resource deficits and delays in construction work. The construction of new semiconductor manufacturing facilities requires project teams to locate infrastructure bottlenecks because their discovery will help complete projects on schedule while maintaining operational efficiency.

Challenges

High Infrastructure Costs and Resource Constraints

Semiconductor fabs represent the most expensive industrial operations because their requirements for power generation and water treatment and waste management and cleanroom construction drive their total capital expenses. The combination of rising energy costs and water shortages in specific areas and environmental compliance obligations has resulted in higher operational costs for the company. The company faces workforce limitations because it lacks enough engineers and technicians who can operate advanced semiconductor equipment. The manufacturing process faces operational delays because these factors limit fab expansion while creating difficulties for manufacturers who want to increase production capacity.

Geopolitical Impact on Global Semiconductor Fab Infrastructure Bottlenecks Market

The Global Semiconductor Fab Infrastructure Bottlenecks Market experiences strong effects from geopolitical factors which disrupt semiconductor supply chains and technology transfer and infrastructure development. Trade tensions between major economies which include export restrictions on semiconductor equipment and regional technology alliances are shaping the global semiconductor manufacturing landscape. Government policies that promote domestic chip manufacturing are driving substantial growth throughout the United States and Europe and China and Japan and South Korea and India. The distribution of infrastructure resources experiences uneven patterns because geopolitical uncertainties and supply chain localization strategies create geopolitical uncertainties. The timelines for fab construction and equipment procurement depend on three factors which include energy availability and environmental regulations and cross-border technology restrictions.

Global Semiconductor Fab Infrastructure Bottlenecks Market

Segmental Coverage

Global Semiconductor Fab Infrastructure Bottlenecks Market – By Bottleneck Type

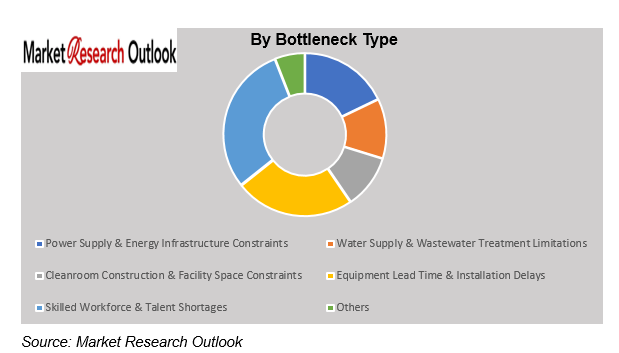

Based on bottleneck type, the market is segmented into Power Supply & Energy Infrastructure Constraints, Water Supply & Wastewater Treatment Limitations, Cleanroom Construction & Facility Space Constraints, Equipment Lead Time & Installation Delays, Skilled Workforce & Talent Shortages, Others. Power and energy infrastructure constraints will continue to serve as a significant operational hurdle because semiconductor fabrication facilities consume excessive energy while needing constant power supply. The semiconductor manufacturing process uses vast amounts of ultra-pure water which creates restrictions on both water supply and wastewater treatment capabilities. The construction and operational efficiency of fabs face two main challenges that require infrastructure planning and mitigation solutions because equipment lead time delays and skilled workforce shortages exist.

Global Semiconductor Fab Infrastructure Bottlenecks Market – By End User

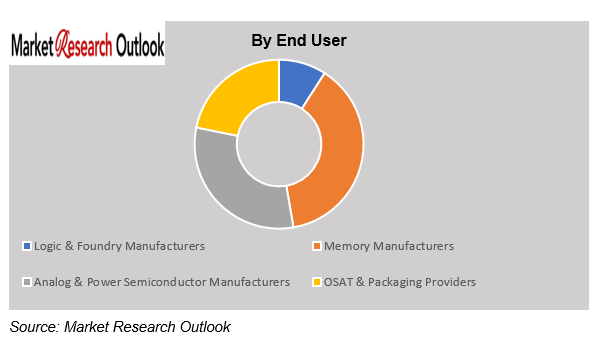

Based on end user, the market is segmented into Logic & Foundry Manufacturers, Memory Manufacturers, Analog & Power Semiconductor Manufacturers, and OSAT & Packaging Providers. The forecast period will see logic and foundry manufacturers control the market because advanced node fabrication facilities are expanding while demand for contract chip manufacturing services is increasing. Memory manufacturers are also increasing investments in new fabs to meet growing demand for high-capacity storage and computing applications. The growing production capacities of analog and power semiconductor manufacturers together with OSAT providers will create new needs for efficient infrastructure management and strategies to handle bottlenecks.

Competitive Landscape

Key participants in the Global Semiconductor Fab Infrastructure Bottlenecks market include Intel Corporation, Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, GlobalFoundries, Micron Technology, SK hynix, Texas Instruments, Infineon Technologies, STMicroelectronics, Applied Materials, ASML Holding, and Lam Research and other prominent players.

These companies are implementing strategic growth initiatives in order to gain a competitive advantage. The strategies being largely adopted include mergers and acquisitions, strategic alliances, joint ventures, licensing agreements, and new product launches. With the implementation of these strategies, the market participants aim to increase product portfolios, as well as enhance regional presence for long-term sustainable business growth in the Semiconductor Fab Infrastructure Bottlenecks industry of Global.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2021–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | Global |

| Product/ Service Segmentation | Bottleneck Type, Fab Type, Node Size, Infrastructure Component, End User, Region |

| Key Players | Intel Corporation, Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, GlobalFoundries, Micron Technology, SK hynix, Texas Instruments, Infineon Technologies, STMicroelectronics, Applied Materials, ASML Holding, and Lam Research and other prominent players. |

Market Segmentation

- By Bottleneck Type

- Power Supply & Energy Infrastructure Constraints

- Water Supply & Wastewater Treatment Limitations

- Cleanroom Construction & Facility Space Constraints

- Equipment Lead Time & Installation Delays

- Skilled Workforce & Talent Shortages

- Others

- By Fab Type

- Foundry Fabs

- Integrated Device Manufacturer (IDM) Fabs

- Memory Fabs

- By Node Size

- Leading Edge (Below 10 nm)

- Advanced Nodes (10–28 nm)

- Mature Nodes (28–65 nm)

- Legacy Nodes (Above 65 nm)

- By Infrastructure Component

- Power & Energy Infrastructure

- Water & Chemical Supply Systems

- Cleanroom & Facility Construction

- Fab Equipment & Installation

- Automation & Digital Infrastructure

- Waste Management & Recycling Systems

- By End User

- Logic & Foundry Manufacturers

- Memory Manufacturers

- Analog & Power Semiconductor Manufacturers

- OSAT & Packaging Providers

- By Region

- North America

- Europe

- Asia Pacific (APAC)

- Latin America (LATAM)

- Middle East and Africa (MEA)

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- Global Semiconductor Fab Infrastructure Bottlenecks Market Insights

- Growth Drivers

- Restraints

- Opportunities

- Challenges

- Technological Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Industry Value Chain & Entry Points

- Infrastructure Constraint Analysis

- Global Semiconductor Fab Infrastructure Bottlenecks Market: Regulatory Framework

- Global Semiconductor Fab Infrastructure Bottlenecks Market: Marketing Strategies

- Global Semiconductor Fab Infrastructure Bottlenecks Market Overview

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Bottleneck Type

- Power Supply & Energy Infrastructure Constraints

- Water Supply & Wastewater Treatment Limitations

- Cleanroom Construction & Facility Space Constraints

- Equipment Lead Time & Installation Delays

- Skilled Workforce & Talent Shortages

- Others

- By Fab Type

- Foundry Fabs

- Integrated Device Manufacturer (IDM) Fabs

- Memory Fabs

- By Node Size

- Leading Edge (Below 10 nm)

- Advanced Nodes (10–28 nm)

- Mature Nodes (28–65 nm)

- Legacy Nodes (Above 65 nm)

- By Infrastructure Component

- Power & Energy Infrastructure

- Water & Chemical Supply Systems

- Cleanroom & Facility Construction

- Fab Equipment & Installation

- Automation & Digital Infrastructure

- Waste Management & Recycling Systems

- By End User

- Logic & Foundry Manufacturers

- Memory Manufacturers

- Analog & Power Semiconductor Manufacturers

- OSAT & Packaging Providers

- By Region

- North America

- Europe

- Asia Pacific (APAC)

- Latin America (LATAM)

- Middle East and Africa (MEA)

- By Bottleneck Type

- Market Size & Forecast, 2021-2032

- North America Semiconductor Fab Infrastructure Bottlenecks Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- By Country

- United States

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Canada

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Europe Semiconductor Fab Infrastructure Bottlenecks Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- By Country

- Germany

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- United Kingdom

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Italy

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- France

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Spain

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Belgium

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Russia

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- The Netherlands

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Rest of Europe

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Asia Pacific Semiconductor Fab Infrastructure Bottlenecks Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- By Country

- China

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- India

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Japan

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- South Korea

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Australia & New Zealand

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Indonesia

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Malaysia

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Singapore

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Vietnam

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Rest of APAC

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Latin America Semiconductor Fab Infrastructure Bottlenecks Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- By Country

- Brazil

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Mexico

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Argentina

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Peru

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Rest of LATAM

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Middle East & Africa Semiconductor Fab Infrastructure Bottlenecks Market

- Market Size & Forecast, 2021-2032

- By Value (USD Billion)

- Market Share & Forecast

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- By Country

- Saudi Arabia

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- UAE

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Qatar

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Kuwait

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- South Africa

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Nigeria

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Algeria

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Rest of MEA

- By Bottleneck Type

- By Fab Type

- By Node Size

- By Infrastructure Component

- By End User

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution by End-Use Industry

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List of Key Players and Their Products

- Global Semiconductor Fab Infrastructure Bottlenecks Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Developments (Mergers, Acquisitions, Partnerships, etc.)

- Geopolitical Impact on Global Semiconductor Fab Infrastructure Bottlenecks Market

- Company Profile

- Intel Corporation

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Intel Corporation

- Saudi Arabia

- Market Size & Forecast, 2021-2032

- Brazil

- Market Size & Forecast, 2021-2032

- China

- Market Size & Forecast, 2021-2032

- Germany

- Market Size & Forecast, 2021-2032

- United States

- Market Size & Forecast, 2021-2032

**(same data pointers will be provided for the below companies)

- Taiwan Semiconductor Manufacturing Company

- Samsung Electronics

- GlobalFoundries

- Micron Technology

- SK hynix

- Texas Instruments

- Infineon Technologies

- STMicroelectronics

- Applied Materials

- ASML Holding

- Lam Research

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown of Primary Research Respondents, By Region

- Assumptions & Limitations

- Qualitative Research

*Financial information of case of non-listed companies can be provided as per availability.

**The segmentation and the companies are subject to modifications based on in-depth secondary research for the final deliverable